Original | Odaily Planet Daily (@OdailyChina)

Author | Qin Xiaofeng (@QinXiaofeng888)

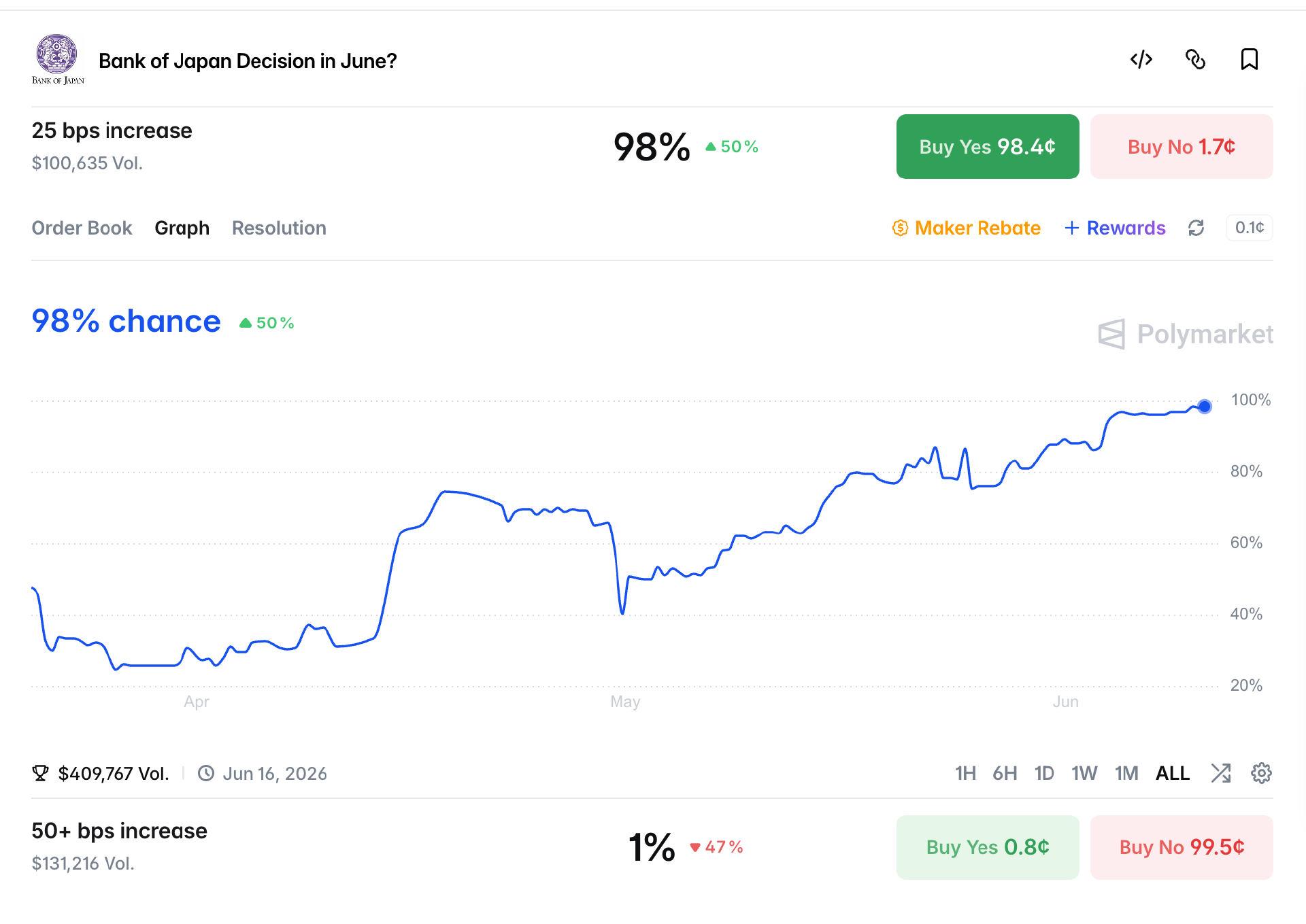

According to Nikkei News, the Bank of Japan (BoJ) is expected to raise the short-term policy interest rate from 0.75% to 1.0% at its monetary policy meeting from June 15 to 16, which will be the highest policy rate level since 1995. Currently, the market pricing for a rate hike is extremely high, with the probability of a "25bp hike" on PolyMarket soaring from 25% in early April to 98%.

The BoJ's rate hike is imminent, and many investors who have engaged in yen carry trades may be forced to sell overseas assets, convert back to yen, and repay loans, triggering a chain reaction that amplifies the volatility of global risk assets — a typical case being the flash crash in August 2024, when the yen surged sharply, causing a short-term plunge in global stock markets, and Bitcoin plummeted nearly $20,000 in a single day, with a maximum drop of 15%.

Odaily Planet Daily will analyze the macro background and transmission mechanism of the BoJ's rate hike, with a focus on assessing its risk impact on AI tech stocks and cryptocurrencies for readers' reference.

1. Inflation Risks Driving BoJ Rate Hike

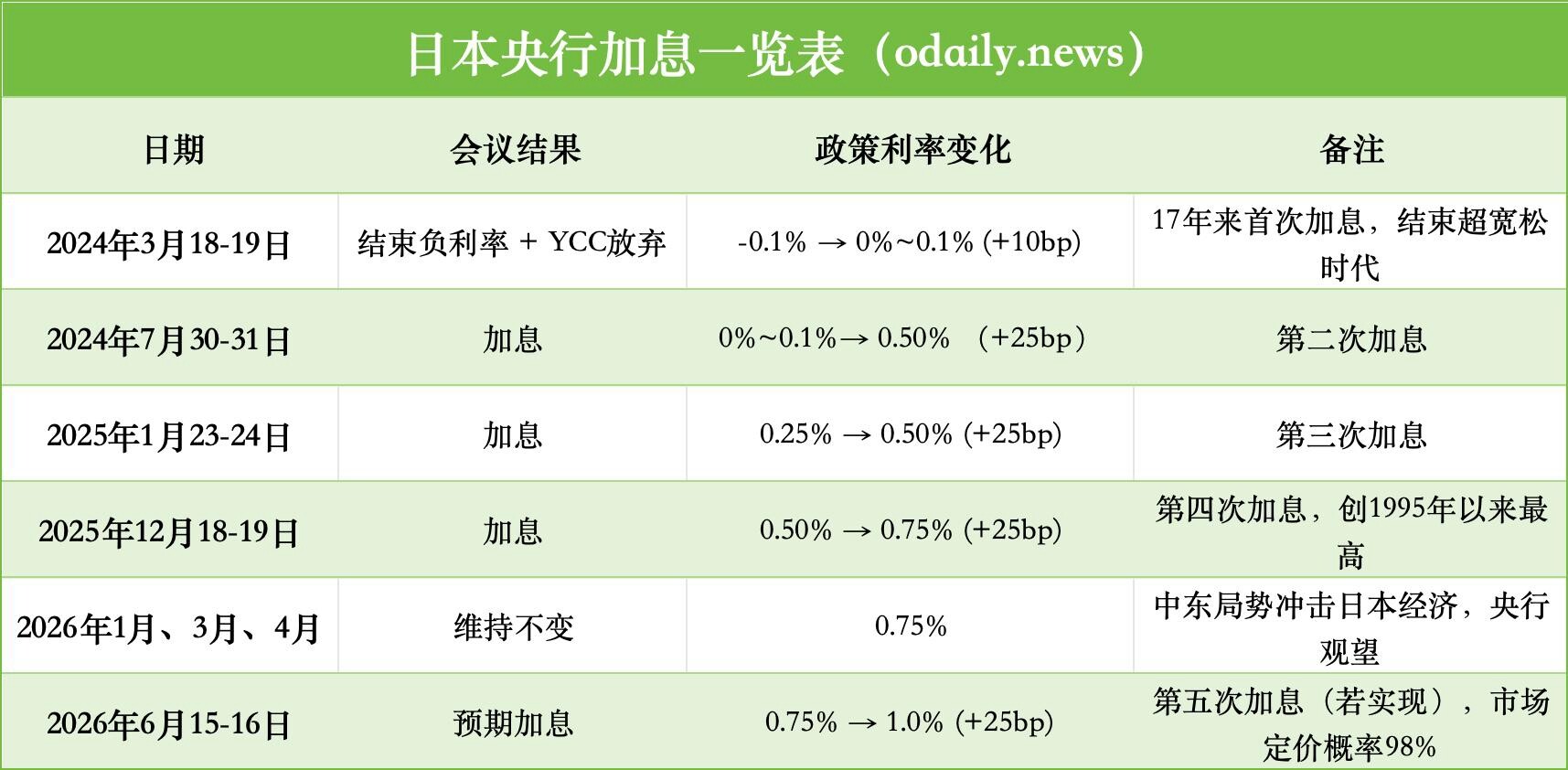

Over the past two years, the hawkish voices within the BoJ have grown stronger, ultimately ending a 17-year negative interest rate policy in March 2024, raising the policy rate from -0.1% to a range of 0% to 0.1%, marking the first rate hike in this cycle. In July 2024, the BoJ raised the rate again by 15bp to 0.25% and announced a gradual balance sheet reduction; in January and December 2025, the rate was increased by 25bp, reaching 0.75%; the first three meetings of 2026 maintained the rate unchanged. The following are the BoJ's recent rate hike situations:

Why has the BoJ, after maintaining interest rates at the same level for half a year, hastily begun a new round of rate hikes? This rate increase is primarily driven by two factors.

The first is energy shocks and imported inflation pressure. As conflicts in the Middle East caused oil prices to fluctuate in the first half of the year, Japan, as a country heavily reliant on imported energy, saw significant increases in import costs. The Corporate Goods Price Index (CGPI) in May rose 6.3% year-on-year, the fastest growth rate since 2023, with petroleum products rising 9.6% and utilities rising 8.5%. The BoJ expects that the core CPI for the fiscal year 2026 will rise to 2.5-3.0%, far exceeding the established target of 2%.

The second is the weakness of the yen exacerbating imported inflation. Currently, the USD/JPY exchange rate has been hovering near the high range of 158-160, approaching a historically extreme weakness zone. The significant depreciation of the yen directly weakens the purchasing power of Japanese companies for imports, leading to substantial increases in import costs for energy, raw materials, and other bulk commodities, further pushing up domestic price levels. Although the Japanese Ministry of Finance has intervened multiple times in the foreign exchange market, the effects have been limited and difficult to sustain. This situation is forcing the BoJ to tighten monetary policy (i.e., raise interest rates) in the June meeting to avoid losing control of inflation expectations.

BoJ Governor Kazuo Ueda, in a speech on June 3, clearly shifted to an anti-inflation narrative, emphasizing that if the risk of price increases outweighs the risk of economic downturn, the pros and cons of rate hikes must be discussed.

Reuters cited three informed sources reporting that unless the Middle East conflict escalates sharply, the BoJ will raise interest rates in June and may slow down the pace of bond balance sheet reduction to maintain market stability. Bloomberg and institutions like ING maintain similar assessments and expect the BoJ to raise interest rates by a total of 50bp in 2026.

This series of changes marks Japan's shift from being the "last lender of the world" to a normalization central bank, posing a direct challenge to global assets reliant on cheap yen financing.

2. Yen Carry Trades Being Closed, Liquidity Continues to Tighten

The Bank of Japan has long maintained an ultra-loose monetary policy, and yen carry trades have also been an important part of global liquidity over the past decade. Investors borrow yen at near-zero interest rates to invest in U.S. stocks, tech stocks, emerging markets, cryptocurrencies, and other high-yield assets, earning interest spreads and capital gains.

The BoJ's rate hike will directly increase the cost of yen financing and may lead to yen appreciation (USD/JPY down), forcing leveraged investors to close their positions, creating a positive feedback loop: yen appreciation leads to expanded currency losses → financing costs rise → investors forced to deleverage → massive sell-off of risk assets → asset prices further decline → more stop-loss orders triggered → closing pressures intensify.

Historically, every tightening signal from the BoJ has triggered significant market volatility.

On July 31, 2024, the BoJ raised rates by 15bp to 0.25% and announced gradual balance sheet reduction, combined with weak U.S. employment data, causing significant turmoil in global markets. At that time, South Korea's two major indices (KOSPI and KOSDAQ) both plummeted and triggered circuit breakers; Japanese stocks crashed, with the Nikkei 225 dropping 12.4% in a single day, a cumulative decline exceeding 20% in a week, marking the worst performance since 1987; global stock markets fell in tandem, with U.S. stocks and tech stocks adjusting simultaneously, and the VIX fear index surged. Cryptocurrencies were similarly hard hit, with Bitcoin and ETH crashing over 30% in just one week, and leveraged liquidations surged.

According toMorgan Stanley estimates, although a significant number of positions have been gradually closed since 2024, there are stillapproximately $500 billion in outstanding yen financing positions in the market. Although the market has priced in some risks in advance, these positions still pose significant hidden dangers. Morgan Stanley warns that a rapid appreciation of the yen could trigger chain liquidations during thin liquidity periods, especially affecting high-leverage assets severely.

J.P. Morgan's Global Market Strategist Dubravko Lakos-Bujas and Forex Strategist Meera Chandan both pointed out that the policy divergence between the BoJ and the Federal Reserve will exacerbate the instability of carry trade liquidations, potentially leading to a reassessment of global risk asset valuations.

3. Global Risk Assets Hurt, U.S. Stocks and Crypto Not Unscathed

The AI-driven tech boom has been the main story for U.S. stocks in the first half of 2026, with semiconductor stocks like Nvidia and Broadcom and mega-scale cloud service providers leading the Nasdaq to record highs.

However, in June, the market saw notable rotation and pullback, particularly on June 5, when U.S. stocks experienced their most severe single-day pullback of 2026 to date. The Nasdaq plunged 4.18%, marking the largest single-day decline since April 2025; the S&P 500 fell 2.64%, ending a nine-week streak of increases; the Dow dropped 1.35%, and the Philadelphia Semiconductor Index plunged over 10%, severely impacting core AI stocks like Nvidia, Broadcom, Micron, and Marvell (Recommended Reading: “Nasdaq Drops 4.2% in a Single Day, Does ‘Black Friday’ Burst the U.S. Stock Bubble?”).

The pullback in U.S. stocks is attributed not only to geopolitical tensions and uncertainties in Federal Reserve policy but also to the potential impacts of a rate hike by the BoJ that cannot be ignored.

First, tightening liquidity will directly hit high-valuation growth stocks. AI companies have massive capital expenditures and rely heavily on cheap financing. The unwinding of yen carry trades will reduce global risk appetite and capital inflow, with high-beta tech stocks bearing the brunt. Semiconductors like Nvidia and Broadcom, as well as hyperscalers like Meta and Microsoft, have extremely high valuation sensitivity and are easily subjected to sell-offs. Investing.com analysis points out that high-valuation growth sectors are most sensitive to changes in global liquidity, often witnessing rapid deleveraging once carry trade unwinding begins.

Second, rising energy costs will significantly compress AI profit margins. The Middle East conflict has driven up oil prices, leading to significant increases in electricity and cooling costs for data centers, together with the BoJ's rate hike, creating a “stagflationary” macro environment that severely tests the sustainability of AI business models.

Arthur Hayes, founder of BitMex, in his latest article “Reality Test”, clearly warns: “The reality of energy is testing the current 'dreaming' state of the market.” High oil prices not only raise operational costs but may also slow down the growth of enterprise token usage, further undermining AI-related revenue expectations.

Finally, there is the impact of large IPO supply shocks and political regulatory risks. Giants like SpaceX, Anthropic, and OpenAI plan to go public intensively in the second half of 2026, with valuations often at a hundred times sales, and the release of lock-up periods will bring immense supply pressure. At the same time, Trump may turn against AI for the midterm elections, increasing regulatory uncertainty.

Cryptocurrencies, as the highest beta risk assets globally, face an even bleaker outlook. On one hand, a rate hike in yen increases financing costs, directly increasing global leveraged trading costs, forcing large-scale closures of crypto leverage positions; on the other hand, in the competition for liquidity with AI, AI capital expenditure has absorbed significant market funds, while crypto had already fallen behind, and the BoJ's actions will further tighten marginal liquidity.

Yahoo Finance analyst Lockridge Okoth has stated that a 98% probability rate hike could trigger the next round of liquidity shock for Bitcoin. Investing.com analysis indicates that yen appreciation and Bitcoin weakness are often highly synchronized and are a typical signal of rising global risk aversion.

Arthur Hayes has also emphasized in multiple analyses that the dynamics of yen carry trades remain one of the key variables affecting Bitcoin liquidity, reminding investors to pay attention to the short-term liquidity shocks caused by policy signals. In his recent article, Arthur Hayes stressed the need to be wary of the combined impacts of short-term energy costs and monetary policy risks; BTC/ETH may adjust in the short term along with risk assets, while the long-term outlook depends on the resumption of liquidity.

Conclusion:

The renewed worries over the BoJ's rate hike are not an isolated event but a signal of tightening global marginal liquidity. Particularly, the current geopolitical conflicts in the Middle East are pushing up oil prices, AI capital expenditures are consuming liquidity, and uncertainties in Federal Reserve policy are compounding, further compressing buffer space.

For investors, in the short term, global risk assets, especially high-leverage, high-valuation sectors (AI tech stocks and cryptocurrencies) may face significant pullback pressures, and volatility will notably rise, requiring heightened vigilance and awareness of leverage risks.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。