CoinW Research Institute

Recently, the SpaceX IPO has become a focal point of attention for both global capital markets and the cryptocurrency market. According to the official announcement released by SpaceX on June 4, it plans to issue 555,555,555 shares of Class A common stock to the public, with an expected issue price of $135 per share. SpaceX has applied for listing on the Nasdaq Global Select Market and Nasdaq Texas, with the stock symbol SPCX. If the issuance process goes smoothly, SpaceX shares are expected to begin trading on June 12.

The reason this event has garnered significant attention from the cryptocurrency market is not only because SpaceX could become one of the largest IPOs in global history, but more importantly, even before the stock officially lists on Nasdaq, the cryptocurrency market has already formed a pre-IPO trading market around SpaceX. Trade.xyz on Hyperliquid has launched SpaceX pre-IPO perpetual contracts, and centralized exchanges like Coinbase, Binance, and CoinW have successively introduced pre-IPO perpetual contracts related to SpaceX, while Kraken and Bybit have opened access to SpaceX IPO through the xStocks framework.

However, what is truly worth discussing regarding pre-IPO products is that they are transforming the pre-IPO valuation discrepancies, which originally belonged solely to investment banks, private equity funds, high-net-worth clients, and a few primary market intermediaries, into price signals that ordinary users can also observe and trade. Issues arise as well: is Pre-IPO truly lowering the participation threshold for ordinary users, or is it merely amplifying emotional premiums in advance? When there is a significant price difference between the SpaceX pre-IPO contract prices on platforms like Hyperliquid and the expected $135 issue price, what is being traded in the market is the value of SpaceX itself or the premium of the "early entry rights"?

In the following sections, CoinW Research Institute will analyze the background of SpaceX's listing, the price differences of pre-IPO contracts, the structure of pre-IPO products, sources of user participation earnings, differentiation of CoinW products, and deeper market changes.

Table of Contents

1. SpaceX is about to go public, and the super IPO opens market imagination

1.1 Issuance Scale and Valuation Level

1.2 SpaceX is not an ordinary commercial space IPO

1.3 The cryptocurrency market is concerned with pre-listing pricing power

2. Pre-IPO contracts price in advance, price differences behind are entry rights premiums

2.1 The issue price and the on-chain price show significant divergence

2.2 Early entry rights are being priced into the market

2.3 Premium does not equal real value

3. What exactly is Pre-IPO: first, look at the product structure

3.1 Structured earnings mapping: the underlying is notes or yield rights

3.2 Tokenized IPO access: the underlying is the subscription and allocation process

3.3 Pre-IPO perpetual: trading is exposure to valuation

4. Why participate in Pre-IPO: where does the profit come from

4.1 From being optimistic but unable to buy, to being able to express viewpoints in advance

4.2 From private placement valuation to public market pricing, there exists a tradable window in between

4.3 Liquidity itself can also be priced

4.4 Earnings are gradually released along the event timeline

4.5 Pre-IPO may become an alternative growth exposure for cryptocurrency users

5. How to make money by participating in Pre-IPO: actionable paths and boundaries

5.1 New share earnings: the price difference between the issue price and the opening price

5.2 Directional trading: trading on valuation upgrades or premium pullbacks

5.3 Cross-platform price differences: it looks like arbitrage, but essentially it is basis trading

5.4 Cross-asset hedging: integrate SpaceX into the framework of tech stocks and macro risks

6. Differentiation of CoinW Pre-IPO products

6.1 From single-point contracts to TradFi asset layers

6.2 Managing cross-asset portfolios under the same account

6.3 USDT-based pricing reduces settlement complexity

7. Pre-IPO is changing the direction of RWA

7.1 From stable RWA to growth-oriented RWA

7.2 Pre-IPO trades valuation differences

7.3 A "shadow price layer" is forming

7.4 The next competitive point is standardization and trust

8. Conclusion: The opportunity in Pre-IPO lies in price discovery, and the risk also lies in price discovery

8.1 SpaceX is a real stress test for pre-IPO products

8.2 Platform competition will shift from speed of going live to credibility of rules

8.3 Investors need to be alert: price exposure does not equate to real equity

1. SpaceX is about to go public, and the super IPO opens market imagination

1.1 Issuance Scale and Valuation Level

From the perspective of traditional capital markets, the most direct focus of the SpaceX IPO is its scale. Based on an issue price of $135 and approximately 555.5 million shares, this IPO's foundational financing scale is about $75 billion. If the issuance is completed at this price, SpaceX's valuation will be approximately $1.75 trillion, and the financing scale will surpass Alibaba's historical record of approximately $21.8 billion during its IPO in 2014, making it one of the most watched IPOs in the history of global capital markets.

From the valuation perspective, SpaceX's listing is not an ordinary growth stock IPO, but rather a test of global risk appetite. A $1.75 trillion valuation means the market is not just pricing a rocket company but is also pricing a combination of commercial space travel, satellite internet, future deep space exploration, and Musk's personal narrative. Whether it can be absorbed by the public market will directly impact the market expectations for other high-valuation, non-listed tech companies.

1.2 SpaceX is not an ordinary commercial space IPO

If SpaceX is understood solely as a commercial space company, it may underestimate the market significance of this IPO. SpaceX embodies several narratives: reusable rockets reduce launch costs, Starlink represents the global satellite internet infrastructure, NASA and government contracts provide long-term cash flow imaginations, and future deep space exploration carries Musk's personal narrative and technological risk appetite.

In other words, SpaceX is not a traditional single-business company; it is more like a "commercial space + global communication network + technological infrastructure + Musk's asset portfolio" composite pricing. After it goes public, the market will not only trade current revenue and profits but also the imagination of commercial space, satellite internet, and space infrastructure over the next ten years.

1.3 The cryptocurrency market is concerned with pre-listing pricing power

For this reason, SpaceX's listing will simultaneously impact multiple markets. U.S. stock investors are concerned about whether it can enter the valuation system of tech giants, whether it affects Nasdaq index weights and the space economy sector; primary market investors focus on whether it will reassess the valuations of non-listed tech companies post-listing; the cryptocurrency market is more concerned with another matter: if top unlisted assets like SpaceX can be traded in advance, will pre-IPO assets become the next important product line after RWA?

This is also the biggest difference between this round of events and ordinary IPOs. In the past, the core game before an IPO mainly occurred between investment banks, institutional investors, private equity funds, and high-net-worth clients, with ordinary users often only able to participate in the secondary market after the stock officially lists. In the case of this SpaceX event, cryptocurrency exchanges and on-chain platforms have brought "pre-listing price discovery" to ordinary users ahead of time. Users may not be able to obtain actual SpaceX shares, nor can they necessarily obtain IPO allocations, but they can already trade around the changing valuation of SpaceX.

2. Pre-IPO contracts price in advance, price differences behind are entry rights premiums

2.1 The issue price and the on-chain price show significant divergence

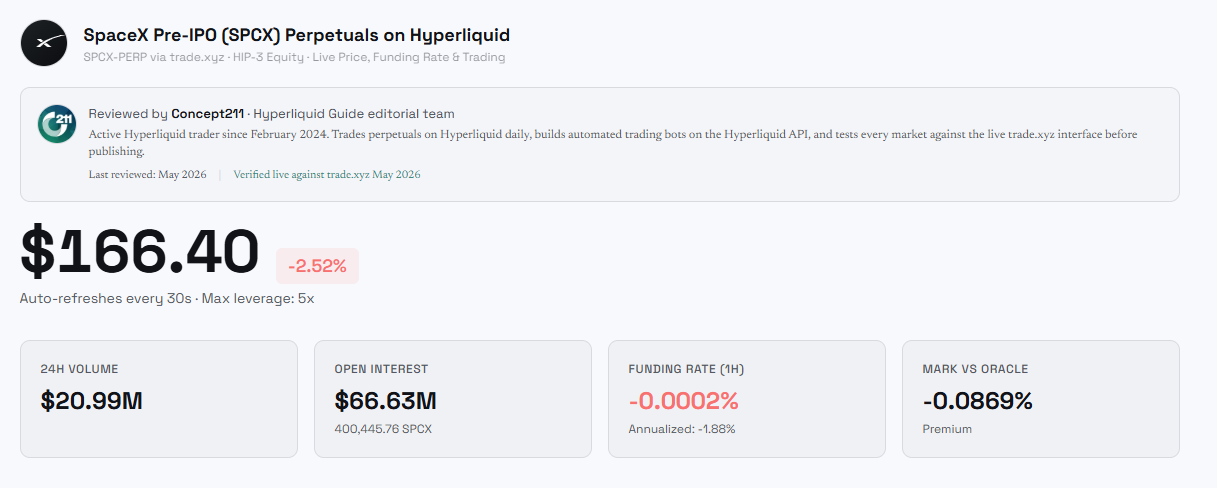

Currently, SpaceX's expected IPO issue price is $135 per share. Trade.xyz launched the SPCX-USDC, which is the SpaceX Pre-IPO perpetual contract, on Hyperliquid on May 18. This contract does not represent actual SpaceX equity; rather, it is a cash-settled derivative based on price, tracking the market’s implied expected price per share of SpaceX Class A common stock.

At the time of launch, Trade.xyz initially used approximately 11.87 billion fully diluted total shares (i.e., total shares assuming that all potential shares from employee options, restricted stock, convertible instruments, etc., are converted into common stock) as a reference example: the initial reference price was about $150, corresponding to an approximate reference market value of $1.78 trillion; the price at one point surged to around $216, implying an approximate valuation of $2.56 trillion based on the same standard.

However, it needs to be especially noted that on June 10, TradeXYZ officially clarified: total shares and market value are not input parameters for the rules of this contract, oracle pricing, or final conversion mechanism; the 11.87 billion shares were merely a teaching example in early documents and have now been removed to avoid misunderstanding; SPCX will not undergo Rebase due to changes in share capital and will switch to standard external oracle pricing after SpaceX completes its IPO and sufficient external price data is available, with prices converging directly to publicly traded stock prices post-listing.

This clarification changed the method of comparison. For platforms that employ capital adjustment mechanisms, implicit valuations must still be restored through "price × shares" before making comparisons; the SPCX on Trade.xyz anchors the price per share itself, allowing its contract price to be directly compared with the IPO issue price. Following this logic, the initial reference price of $150 for SPCX carries an approximate premium of 11% over the expected IPO issue price of $135, while the peak of $216 again reflects an even higher premium.

Regardless of the method employed, the directional conclusion remains consistent: the cryptocurrency market has not passively waited for SpaceX to officially list; rather, it has re-priced it through pre-IPO synthetic perpetual contracts before formal trading begins, and the pricing consistently exceeds the issuance range provided by traditional capital markets. Therefore, the cross-platform price differences and arbitrage activities arising from the variance in share count and Rebase rules themselves constitute a part of this on-chain repricing process.

2.2 Early entry rights are being priced into the market

The third-party market data page Hyperliquid Guide indicates that the current SPCX contract is priced around $166.40 in their snapshot, with a 24-hour trading volume of about $20.99 million and an open interest of about $66.63 million.

Source: https://hyperliquidguide.com/markets/xyz/spcx

This kind of price difference is not difficult to understand. What is being traded in the market is not just SpaceX itself, but the "early entry rights." If users cannot participate in SpaceX's pre-listing pricing through traditional brokerages, investment banks, or private channels, then pre-IPO contracts become one of the few tradable exits. As long as the market believes there might be a high opening after the formal listing, the pre-IPO price may reflect this optimistic expectation in advance.

2.3 Premium does not equal real value

It is important to note that pre-IPO perpetual contracts are not SpaceX stock and are not equivalent to IPO allocations. Taking the SPCX on Hyperliquid as an example, it is essentially a cash-settled perpetual contract built around SpaceX's valuation, with no actual stock delivery and no shareholder rights provided. Such contracts reference valuation indices pre-listing, and they will convert or adjust based on the final IPO price and share count post-listing, while also carrying risks such as insufficient liquidity and margin calls.

Therefore, the price difference of pre-IPO contracts resembles an accumulation of several types of premiums: the first is scarcity premium, as ordinary investors find it difficult to participate directly in SpaceX's primary market; the second is emotional premium, as SpaceX holds a significant market attention; the third is leverage premium, as perpetual contracts allow users to long or short the valuation changes in advance; the fourth is liquidity premium, where a few tradable venues can more easily form short-term crowding conditions before the actual stock is listed.

3. What exactly is Pre-IPO: first, look at the product structure

3.1 Structured earnings mapping: the underlying is notes or yield rights

Before discussing Pre-IPO, it is important to clarify what exactly users are buying. Currently, Pre-IPO products on the market are not the same thing. The first category is structured earnings mapping, where the core does not allow users to hold the target company's stock directly but packages the future performance of an unlisted company into an investable product through SPVs, trusts, fund shares, or structured notes. Tokens here serve more as on-chain certificates, corresponding to some economic rights, yield rights, or future payment rights.

Republic's rSPAX is a typical case. rSPAX represents the user's investment in RepublicX or payment notes, with the final payment amount referenced against the future performance of SpaceX common stock. However, users do not directly obtain SpaceX equity, nor do they possess the voting rights, ownership, or governance rights of SpaceX shareholders. This means that these products reflect the earnings arrangements provided by the intermediary structure rather than SpaceX stock itself.

The key issue with this type of product is clarity of the underlying structure: who issues the notes, whether there are real assets or reference assets to support them, what events will trigger payment in the future, how the payment amounts are calculated, and if users can transfer or redeem. If these terms are unclear, tokenization itself cannot reduce risk.

3.2 Tokenized IPO access: the underlying is the subscription and allocation process

The second category involves tokenized IPO access, where the core is to enable traditional IPO subscriptions, allocations, or stock-related rights post-listing to be made into more easily accessible participation entries through tokenization.

Products launched by Kraken and Bybit around SpaceX are closer to this direction. Users can submit subscription intentions or requests on the platform, and if they ultimately receive allocations, they will gain corresponding SpaceX xStock tokens. However, this does not equate to directly subscribing to SpaceX shares in the traditional brokerage sense. What users typically receive is tokenized stock or a certificate of related rights, providing price exposure related to the performance of SpaceX shares, but this does not necessarily mean users are directly registered as SpaceX shareholders, nor do they typically enjoy voting rights or other shareholder rights.

Therefore, when participating in such products, users need to verify three critical questions: first, whether they genuinely receive IPO allocations or merely submit subscription intentions; second, how final allocation ratios are determined, and whether situations of partial allocation or no allocation exist; third, whether what they receive after listing is tokenized stocks, certificates of rights, or some synthetic assets. If these questions are not made clear, users may mistakenly equate an "entry for subscription" with "certainty of holding shares."

3.3 Pre-IPO perpetual: trading is exposure to valuation

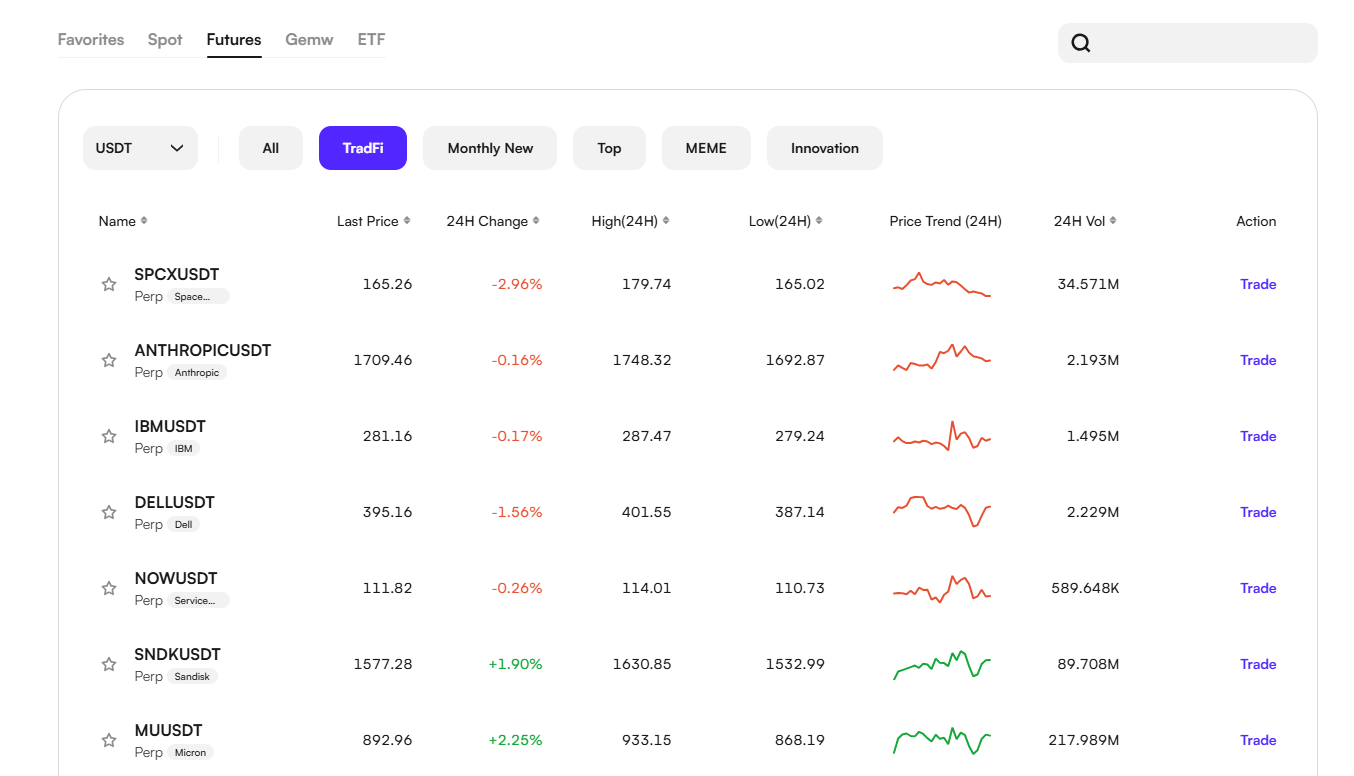

The third category is Pre-IPO perpetual or pre-market contracts, such as SpaceX-related contracts on platforms like Hyperliquid, Coinbase, Binance, and CoinW. This type of product differs significantly from the first two categories. It does not try to enable users to obtain SpaceX stock, yield rights, or IPO allocation qualifications; instead, it creates a tradable contract market built around SpaceX's pre-IPO valuation.

Users trade on valuation expectations, price differences, liquidity, and market sentiment. Its advantages lie in a lower participation threshold, rapid launch speed, and flexible trading options, allowing for both long and short positions. It does not require actually moving SpaceX equity onto the blockchain; rather, it first turns market judgments about SpaceX's pre-IPO valuation into tradable objects.

What users purchase is a cash-settled or contract-settled price exposure. It is suitable for directional judgments, trading price differences, or observing market sentiment.

4. Why participate in Pre-IPO: where does the profit come from

4.1 From being optimistic but unable to buy, to being able to express viewpoints in advance

When Pre-IPO no longer points to crypto-native projects but instead refers to traditional star companies like OpenAI, SpaceX, and Anthropic, the logic for user participation clearly changes. It is no longer just about betting on the token narrative of a Web3 ecosystem; it leverages on-chain and cryptocurrency exchange channels to transform previously inaccessible primary and secondary market assets into a form of financial exposure to express viewpoints.

This transformation is crucial. In the past, even if ordinary users were optimistic about SpaceX, it was difficult for them to genuinely participate before the listing. Relevant shares were mainly held by institutional investors, high-net-worth individuals, participants in employee stock plans, private equity funds, and a few secondary transfer intermediaries. What ordinary investors could typically do was wait until the company officially IPO-ed and then purchase at the public market price. The appeal of Pre-IPO products primarily stems from the emergence of tradable entry points that were previously nonexistent.

As a result, users are not just buying the name of SpaceX; they are buying a redistribution of participation rights. Regardless of whether it ultimately manifests as tokenized rights, structured notes, or pre-market perpetuals, fundamentally, it answers the same question: can ordinary users express judgments about the value changes of top unlisted companies before the traditional public market opens its doors?

4.2 From private placement valuation to public market pricing, there exists a tradable window in between

The second motivation for users participating in Pre-IPO is to capture the reassessment window of enterprises transitioning from private placement valuations to public market pricing. For companies like SpaceX, the market often forms a strong consensus on growth; however, before the formal IPO, its value primarily remains at the level of private financing, off-market transfers, media valuations, and investor expectations, without being fully priced through continuous public trading.

Pre-IPO products effectively open this previously closed price range. What users desire to engage in is not traditional short-term speculation but rather the possible reaffirmation of valuations during a company's transition from private capital markets to public capital markets. If the public market is willing to assign a higher liquidity premium and a higher growth valuation, early participants might gain profits; if the public market's absorption ability is insufficient, then pre-IPO prices may drop in advance.

4.3 Liquidity itself can also be priced

The appeal of Web3 channels also stems from reduced friction and stronger liquidity expectations. Traditional Pre-IPO assets often face issues such as high minimum investment amounts, strong transfer restrictions, slow information updates, and long settlement cycles. Even if investors are optimistic about the targets, they find it challenging to trade flexibly. In contrast, on-chain shares, stablecoin settlements, pre-market contracts, and perpetual trading break down the expected returns of unlisted assets into smaller, more easily tradable units.

However, there is a finer point here: users pursue not just the assets themselves but also pay a price for "liquidity improvements." A Pre-IPO share that is completely non-transferable differs in market pricing from a Pre-IPO contract that allows expression of long or short positions at any time in the exchange, even if the underlying reference assets are the same. The better the liquidity, the more participants there are, and prices often reflect additional premiums.

Consequently, embedded within pre-IPO prices are not only the company value and listing expectations but also the inherent value of trading convenience itself. For users, this is both an advantage and a risk. The advantage lies in more flexible exit pathways; the risk is that, when liquidity premiums are too high, purchase prices may deviate significantly from the fundamentals.

4.4 Earnings are gradually released along the event timeline

From the user's perspective, Pre-IPO earnings do not necessarily crystallize at the moment of the IPO; rather, they are likely to be gradually released along the event timeline. The first stage involves fundamental reassessments related to business data, financing news, or updates to the prospectus; the second stage involves heightened emotions as the listing date approaches, the issue price is confirmed, and market attention increases; and the third stage occurs on the first trading day when a new price is formed in the public market.

What is unique about SpaceX is that these three lines occur almost simultaneously. It has long-term stories of commercial space and satellite internet, has a clear IPO timetable, and has formed pre-IPO trading prices across multiple cryptocurrency platforms in advance. SpaceX Pre-IPO is not merely betting on "how much it will increase on the first trading day," but rather trading on the pricing path after the convergence of enterprise growth, the IPO event, and cryptocurrency market liquidity.

This also explains why Pre-IPO attracts traders. It does not resemble ordinary spot trading, which merely focuses on the current price, nor does it act like traditional primary markets that can only wait for exit events. Instead, it transforms multiple nodes before and after the listing into tradable variables.

4.5 Pre-IPO may provide an alternative growth exposure for cryptocurrency users

In addition to pursuing returns from a single target, some users participating in traditional companies' Pre-IPO also have deeper allocation motivations. Previously, the asset portfolios of cryptocurrency users were often highly concentrated in BTC, ETH, platform tokens, or other high-volatility digital assets, with their earnings closely correlated to the cryptocurrency market cycle.

However, traditional star companies like SpaceX, OpenAI, and Anthropic are driven by factors that do not entirely stem from on-chain narratives; rather, they are largely influenced by technological innovation, competitive industry dynamics, revenue growth, market risk appetite, and progress towards going public. They are just as volatile as cryptocurrency assets but have different sources of volatility. For some users, Pre-IPO offers a new way of exposure: without leaving the cryptocurrency account system, they can still obtain exposure to risks related to technology growth assets.

This does not mean that Pre-IPO can naturally diversify risks; under extreme market conditions, high-risk assets often decline together. However, in terms of asset structure, it truly allows cryptocurrency users' portfolios to extend beyond betting solely on the cryptocurrency cycle to betting on global technology growth and capital market repricing.

Overall, the appeal of Pre-IPO products arises from the early participation rights of scarce assets, but their most dangerous aspect also lies here. The more users feel they have secured "opportunities that were originally unattainable," the easier it is to overlook the differences in product structures. Real equity, SPV shares, structured notes, tokenized rights, perpetual contracts, and so forth all present vastly different risks.

Therefore, Pre-IPO should truly be understood as a product where "opportunity front-loading" and "risk front-loading" occur simultaneously. It allows ordinary users to engage earlier with star unlisted companies, while also exposing them to valuation uncertainties, insufficient liquidity, complex terms, and platform credit risks sooner. For users, the most crucial task is to clarify which type of money they are truly earning: is it the price discount relative to the issue price, an upgraded pre-listing valuation, or short-term liquidity premiums, etc.? Only by delineating the sources of earnings can one truly differentiate the sources of risks.

5. How to make money by participating in Pre-IPO: actionable paths and boundaries

5.1 New share earnings: the price difference between the issue price and the opening price

The easiest way for ordinary users to understand how to make money is by participating in new shares on platforms like Kraken, similar to the price difference earnings of traditional IPOs. If users acquire real IPO allocations, tokenized IPO access, or some products linked to post-listing rights through the platform, and if the opening price on SpaceX's listing day exceeds the issue price, then theoretically, users can profit from the price difference between the issue price and the post-listing trading price.

Taking SpaceX as an example, the official expected issue price is $135. If the public market price exceeds $135 following the listing, users who obtain effective allocations or rights mappings may benefit. However, there are two prerequisites: first, the product received by the user must genuinely correlate to the post-listing rights or settlement price; second, users need to confirm whether there are lock-in periods, redemption restrictions, insufficient allocation ratios, or delays in converts post-listing. Many so-called "entry for new shares" do not guarantee that users will necessarily receive allocations, nor do they ensure that immediate exits will be possible post-listing.

Thus, new share earnings appear to be the simplest but actually rely heavily on the product terms. Users must assess whether they actually obtained effective costs below the market price.

5.2 Directional trading: trading on valuation upgrades or premium pullbacks

The second method is directional trading. Pre-IPO perpetuals and pre-market contracts allow users to go long or short based on the valuation changes of unlisted companies. If users believe that the market will assign a higher valuation post-IPO for SpaceX, they can go long on the Pre-IPO contract; if they think the contract price has already anticipated the expectations, or that post-listing high valuations will be difficult for the public market to absorb, they can short the related contracts.

The source of these trading profits is not equity dividends, nor is it traditional primary market dividends, but rather changes in valuation expectations. For example, updates to the prospectus, confirmation of final issue prices, proximity to the listing date, changes in macro risk appetites, or overall tech stock adjustments can all impact Pre-IPO contract prices. For traders, the real judgment to make is whether the current contract price's implied SpaceX valuation has already surpassed what the public market might accept.

5.3 Cross-platform price differences: it looks like arbitrage, but essentially it is basis trading

The third method is cross-platform price difference trading, also the "arbitrage" direction that is easiest for the market to discuss. Since platforms like Hyperliquid, Coinbase, Binance, and CoinW may simultaneously launch SpaceX-related Pre-IPO contracts, price discrepancies may arise between different platforms. Theoretically, if platform A's price is significantly higher than platform B's, traders can short the high-priced platform while going long on the low-priced platform, waiting for the price difference to converge.

However, it is crucial to note that these types of trades cannot simply be described as risk-free arbitrage; they are closer to basis trading. This is because different platforms may have different contract specifications, collateral assets, leverage limits, funding rates, marked prices, index sources, post-listing conversion mechanisms, etc. Even if two products are both called SpaceX Pre-IPO, they may not settle in the same way at the same time.

For example, if a specific platform's SPCX contract price is substantially higher than the $135 issue price while another platform's price is closer to the issue price, traders might attempt to short the high-premium contract and long the低-premium contract, betting on the price difference converging. But if liquidity suddenly drops on the high-price platform, if the funding rates continually remain negative, if the index rules change, or if the low-price platform halts trading, what was thought of as arbitrage may turn into losses on both sides. Hence, cross-platform price differences do not represent "easy profits" but instead entail a holistic assessment of contract rules, settlement pathways, and liquidity.

5.4 Cross-asset hedging: integrate SpaceX into the risk framework of tech stocks and macro risks

The fourth method is cross-asset hedging. SpaceX is not an isolated asset; it relates to tech growth stocks, AI infrastructures, commercial space initiatives, Musk-related assets, and market risk appetite. Thus, professional traders may not only trade the single SPCX contract but will also observe the performances of TSLA, NVDA, Nasdaq-related assets, gold, and crude oil.

This is also a key observation point for CoinW's TradFi asset layer. It is reported that the CoinW TradFi section already supports popular U.S. stocks like TSLA, AAPL, NVDA, CRCL, as well as perpetual trading of core commodities like gold and crude oil. If the platform positions Pre-IPO within the same TradFi asset framework, users will not only trade SpaceX in isolation but will also be able to observe it within a larger risk portfolio.

Source: https://www.coinw.com/market/futures/TradFi

For example, if users are optimistic about SpaceX but concerned about an overall tech stock pullback, they can lower leverage or hedge with other risk assets; if users believe that SpaceX's momentum could boost the space economy and high-growth tech narratives, they can also monitor the interrelations with related stocks and indices. Cross-asset hedging cannot eliminate Pre-IPO risks but can help users avoid misinterpreting all fluctuations as changes in SpaceX's fundamentals.

In summary, participating in Pre-IPO is not limited to one method of "making money from new shares." Earnings may derive from the difference between the issue price and the opening price, from directional trading such as valuation upgrades or premium pullbacks, etc. However, these sources of earnings share a commonality: the earlier a Pre-IPO opens, the stronger the information asymmetry; the easier it is to trade the product, the more leverage and emotional aspects can be magnified; the more significant the price difference, the greater the underlying rule variations and liquidity risks likely to be. Truly profitable individuals in the long term are not merely those who rush in early, but those who can comprehend what type of money they actually earn—whether it is an issuance discount, an emotional premium, etc. Only by clarifying these distinctions can Pre-IPO avoid becoming a mere trend chase and instead function as a market where risks can be priced.

6. Differentiation of CoinW Pre-IPO products

6.1 From single-point contracts to TradFi asset layers

CoinW launch<|vq_12784|>

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。