Original author: Bu Shuqing

Original source: Wall Street News

Amid the craze of AI infrastructure construction, an unprecedented debt expansion is quietly taking shape—yet the most dangerous part of it has never appeared on any balance sheet.

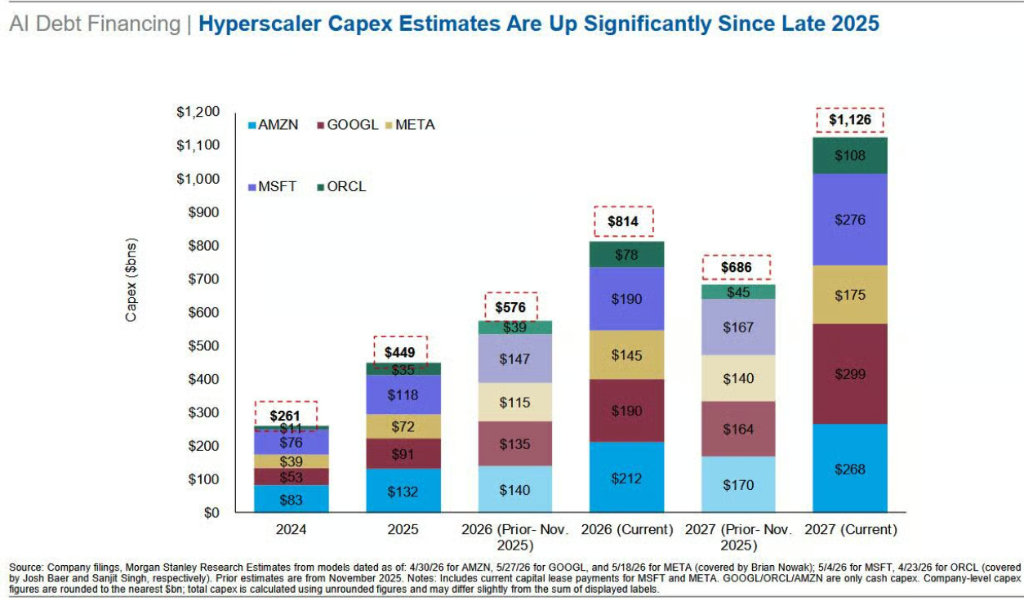

Goldman's latest report predicts that capital expenditures of super-large cloud computing companies will reach $1.1 trillion to $1.4 trillion by 2027, far exceeding market consensus. However, according to Morgan Stanley's in-depth research, this jaw-dropping figure is merely the tip of the iceberg.

Nearly $1 trillion in procurement commitments, over $800 billion in unactivated lease contracts, and tens of billions in supplier financing arrangements together constitute about $1.8 trillion in off-balance-sheet exposure—these liabilities are outside the balance sheet, yet they genuinely lock in future cash outflows.

The market has yet to fully price these risks.

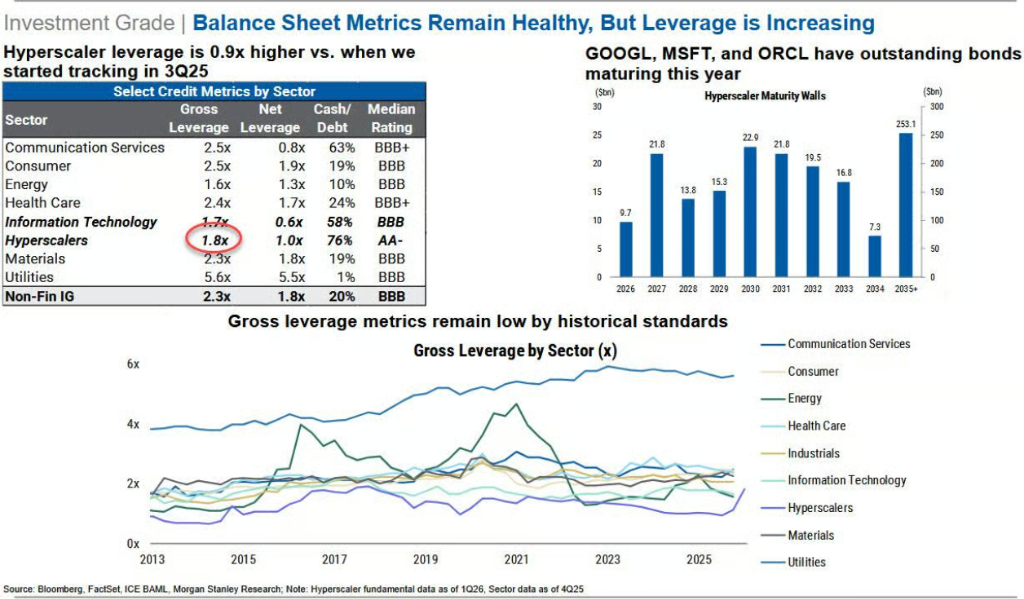

Morgan Stanley warns that the leverage of super-large cloud companies has skyrocketed from 0.9x to 1.8x in just two quarters, with the growth rate of capital expenditures continually outpacing that of revenue and free cash flow, while the real impact of depreciation pressure has yet to arrive.

Meanwhile, private credit institutions represented by Apollo and Blackstone are transferring leverage to the supply chain through SPVs (special purpose vehicles), forming a highly circular and opaque financing structure. If the commercializing process of AI falls short of expectations, or if enterprise clients shift en masse to cheaper alternatives, the fragility of the entire financing chain will be painfully exposed.

Debt Issuance Frenzy: AI Has Become the Biggest Variable in the Public Market

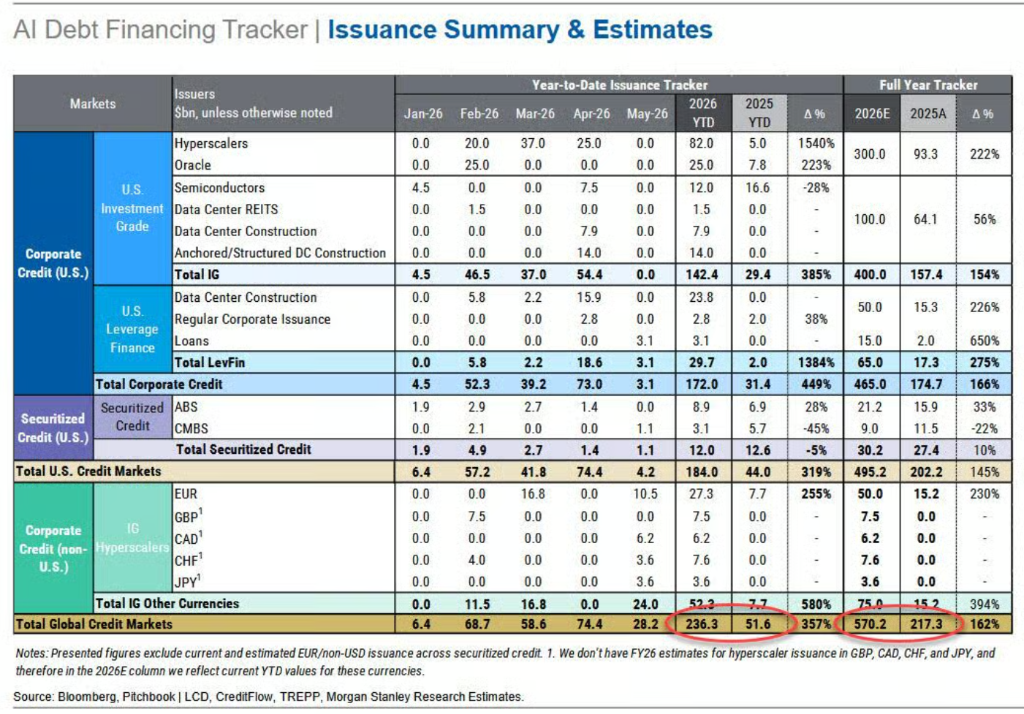

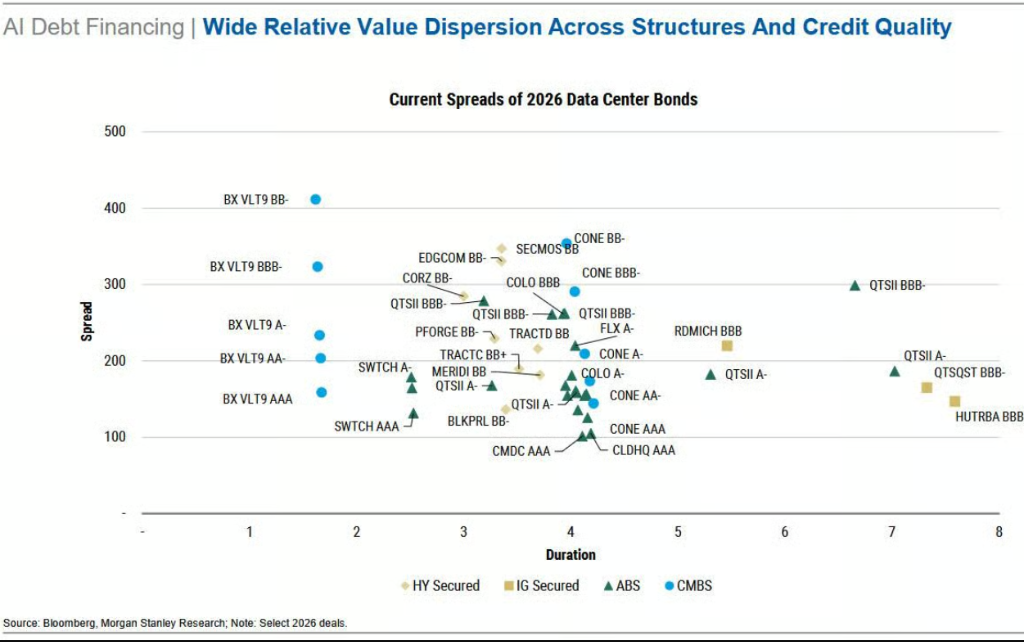

According to Morgan Stanley's latest "AI Debt Financing Tracking Report," as of the end of May 2026, global AI-related bond issuance has reached $236 billion, a staggering increase of 357% compared to the same period in 2025.

Morgan Stanley expects that the total issuance of AI debt will exceed $570 billion for the year, with issuance rates further accelerating in the second half of the year as capital expenditure financing needs are concentrated and released.

In April alone, AI-related bond issuance exceeded $74 billion, setting a new annual record, with project financing structures (for data center construction) accounting for 85% of high-yield bond supply and 40% of investment-grade bond supply. Meanwhile, the five super-large cloud companies—Amazon, Meta, Google, Microsoft, and Oracle—currently account for 4% of the entire investment-grade bond index.

In terms of leverage, the overall gross leverage ratio of super-large cloud companies has risen from 0.9x in Q3 2025 to the current 1.8x, increasing by about 0.3x each quarter, surpassing the leverage level of the entire energy sector.

Morgan Stanley points out that due to supply pressure, the relevant credit spreads have drifted from the AA range to the A range and may widen further. Meta's credit spread is currently wider than the CDX IG benchmark.

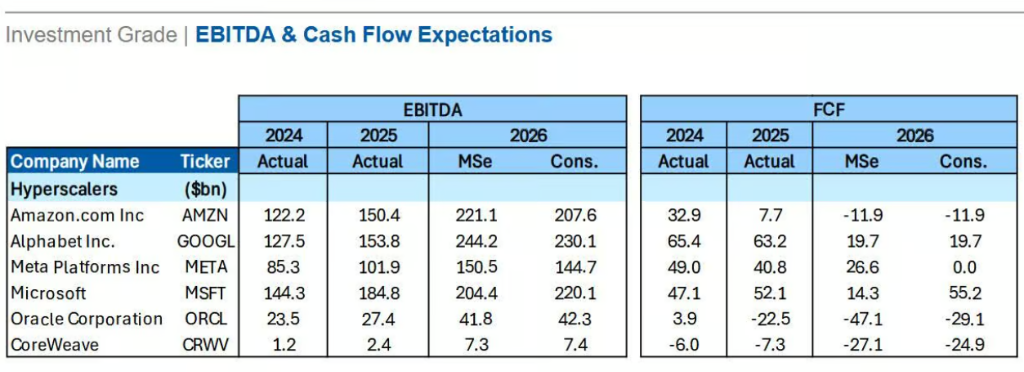

In terms of free cash flow, Morgan Stanley predicts that free cash flow for Amazon and Meta in 2026 will approach zero or even turn negative, at which point incremental financing will almost entirely rely on new debt.

$1.8 Trillion in Off-Balance-Sheet Exposure: Invisible Liabilities, Locked Cash Outflows

Todd Castagno of Morgan Stanley's global valuation, accounting, and tax team points out in the report that focusing solely on capital expenditure figures will severely underestimate the real financial commitments of the AI construction cycle. In addition to disclosed capital expenditures, three key types of off-balance-sheet exposure exist:

Procurement commitments of about $982 billion. Long-term procurement contracts between super-large cloud companies and Nvidia total nearly $1 trillion. According to accounting standards, these obligations are not counted as liabilities until the company expects a contract loss, meaning nearly $1 trillion in future cash outflows currently does not reflect as any liabilities on the balance sheet.

It is noteworthy that Nvidia's own inventory and procurement obligations have risen to about 32% of the consensus revenue forecast for fiscal year 2027, far exceeding the historical range of 15% to 20%, and the risk of supply chain commitments has extended to the chip supplier end.

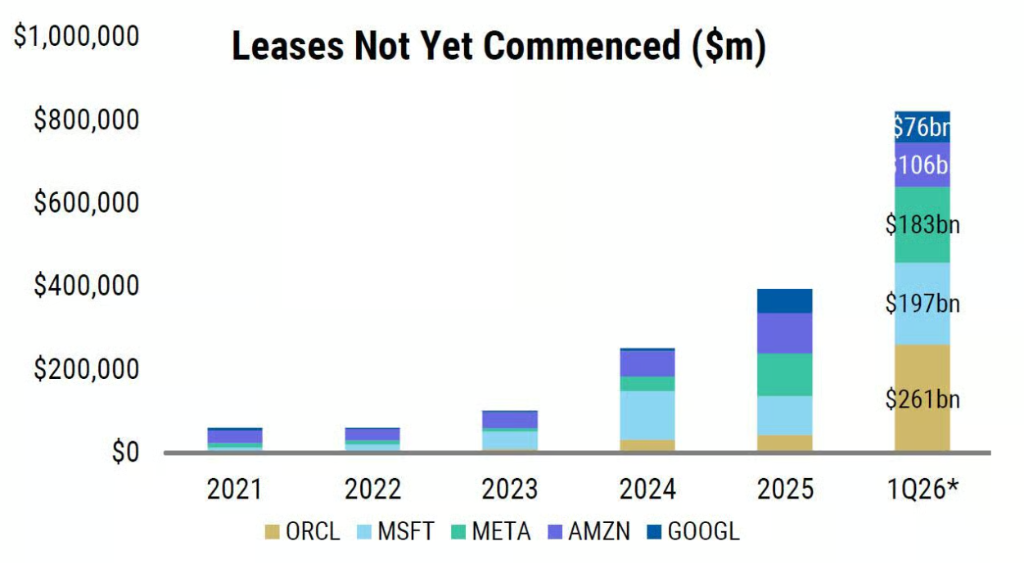

Unactivated lease commitments of about $822 billion. Over $800 billion in lease contracts have been signed but are yet to commence, not counted in current lease liabilities. Additionally, variable lease payments, renewal options, and guaranteed residual values also remain off the balance sheet.

Morgan Stanley estimates that if financing leases are included, Microsoft's capital expenditure to sales ratio will leap from 33%/50% (2026/2027 fiscal years) to 44%/64%, while Oracle could rise from 76%/115% to 101%/189%.

Unpaid capital expenditures within accounts payable of about $110 billion. The days payable outstanding (DPO) for super-large cloud companies have significantly lengthened—Oracle increased by 370% year-over-year, Meta by 73%, and Microsoft by 69%—indicating that the entire supply chain is effectively pre-financing AI construction, with suppliers bearing liquidity pressures that should be the responsibility of buyers.

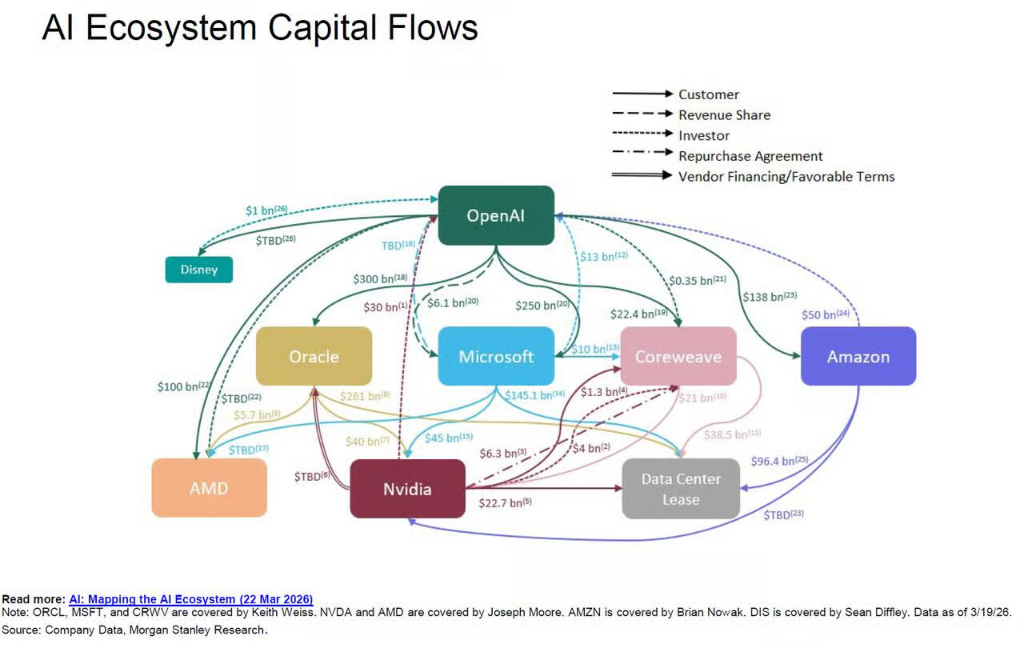

SPVs and Circular Financing: Leverage Transferred to the Shadows

Another core dimension of off-balance-sheet risk is the circular financing structure built through SPVs.

This week, Apollo and Blackstone jointly completed a $35 billion "chip collateral" private credit transaction for Anthropic, exemplifying the operational logic of this model:

Broadcom provided backing for the SPV, and Anthropic used the raised funds to purchase Google chips manufactured by Broadcom, while Google holds a 14% equity stake in Anthropic; Morgan Stanley, which arranged the transaction, also provided loans to investors participating in the deal.

Morgan Stanley's financing association map of the AI ecosystem shows numerous circular relations among OpenAI, Oracle, Nvidia, Microsoft, CoreWeave, AMD, and Amazon, with the same funds repeatedly circulating among a few entities, with SPVs serving as the core tool to realize this cycle.

It is reported that Apollo’s insurance subsidiary Athene is particularly active in the above structure—raising funds by selling annuities to retirees and then injecting those funds into SPVs to participate in AI infrastructure financing.

This model transfers leverage from the visible balance sheets of super-large cloud companies to the supply chain and private credit ecosystem, making the true systemic risk exposure difficult for external observers to identify and summarize.

The Depreciation Cliff and Monetization Gap: Deferred Impacts

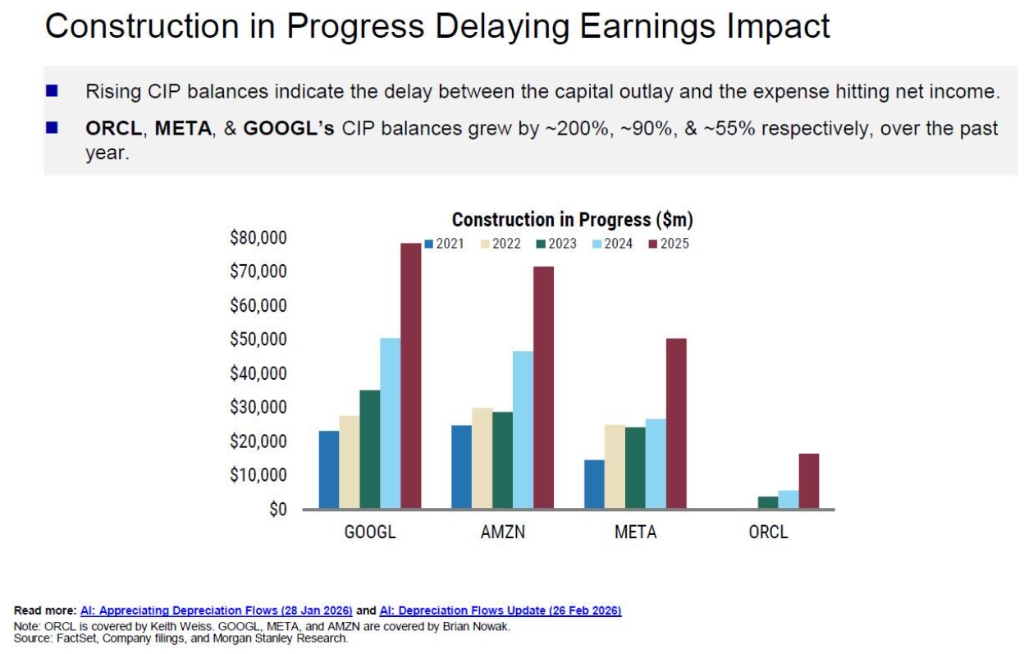

Current financial data exhibits a systematic optimism bias. A significant amount of capital expenditures is currently recorded as "construction in progress" (CIP) and has not yet begun to depreciate, artificially inflating reported profit margins and underestimating future expense pressures.

The balances of construction in progress for Oracle, Meta, and Google have seen year-over-year increases of approximately 200%, 90%, and 55%, respectively.

Once these assets begin to transition into depreciation, the impact will be concentrated and released.

Morgan Stanley predicts that the cumulative depreciation of Microsoft, Oracle, Meta, and Google over the next three years will exceed $520 billion. For example, Oracle's depreciation-to-revenue ratio may rise from the current 7% to 28% in the 2028 fiscal year; Meta could rise from 9% to 19%.

Against this backdrop, the only way to maintain profit margins is through substantial revenue growth—yet the current upward revisions to revenue forecasts lag far behind those of capital expenditure forecasts.

Data shows that Google's 2026 capital expenditure consensus forecast has been revised upward by 139% compared to a year ago, while Meta and Amazon have seen upward revisions of 85% and 81%, respectively, with Oracle having the largest increase at 175%.

At the same time, the amendments to revenue forecasts are significantly lagging, and the structural mismatch of capital expenditure ahead of commercialization is becoming increasingly evident.

Moreover, over $2 trillion in remaining performance obligations (RPO) are highly concentrated in a few large long-term contracts, and the counterparty concentration risk cannot be ignored—any issues with any major participant in the circular system could trigger a chain reaction.

Timing Mismatches Instead of Immediate Payment Crises

Morgan Stanley concludes that the above risks do not currently constitute an imminent solvency crisis, but rather a combination of timing mismatches and information disclosure gaps: deferred depreciation pressures, capital expenditures outpacing monetization progress, leverage shifting to suppliers and private credit layers, and the comparability of capital intensity between different companies significantly affected by accounting classification differences.

Super-large cloud companies are clearly aware of the limited window of current market sentiment and are seizing the opportunity to maximize their financing scale.

Goldman analyst Ryan Hammond points out that if AI infrastructure investment reaches 2% to 3% of GDP, analogous to historical construction cycles in the railway and automotive industries, capital expenditure in 2027 could potentially reach $1.1 trillion; in extreme scenarios, combining super-large cloud companies' cash flows and investment-grade credit market capacity, the ceiling could reach $1.4 trillion.

However, all of this hinges on whether large language models (LLMs) can continue to enhance token pricing and maintain sufficient enterprise customer stickiness. An increasing number of companies are turning their attention to AI products that offer similar performance but at significantly lower prices.

Once structural shifts occur on the demand side, the meticulously constructed financing system will face fundamental stress testing.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。