Original author: Curie, Deep Tide TechFlow

In the days around SpaceX's listing, the pre-market price of SPCX on Hyperliquid was trending, but very few people took a closer look at who was behind the deployment of this market.

In fact, it was a team called Trade.xyz. An anonymous team, which only surfaced this year, has already captured over 90% of the pre-market contract trading volume on Hyperliquid. The excitement over SpaceX's on-chain Pre-IPO has basically been driven by them alone.

However, just three days after SpaceX rang the bell, on June 15th, another team doing the same business announced its closure.

That team, called Ventuals, is backed by Paradigm, and it was also dealing with SpaceX's pre-market contracts, in addition to OpenAI and Anthropic. It launched at the beginning of this year and took only nine months from opening to shutting down.

Same chain, same HIP-3 gameplay, same track. One made SpaceX the largest market in the arena, while the other, holding OpenAI and Anthropic in its hands, ended up failing.

One aspect worth pondering is the way Ventuals exited. According to their official account's posts on social media, they didn’t go bankrupt and flee, but rather announced that they were acquired, with the whole team merging into another project within the Hyperliquid ecosystem. They returned the principal 1:1 to users, marking a decent exit.

But here's the problem. Holding the two most scarce brands, OpenAI and Anthropic, they should logically be the last to exit. What went wrong?

Trade XYZ vs. Ventuals

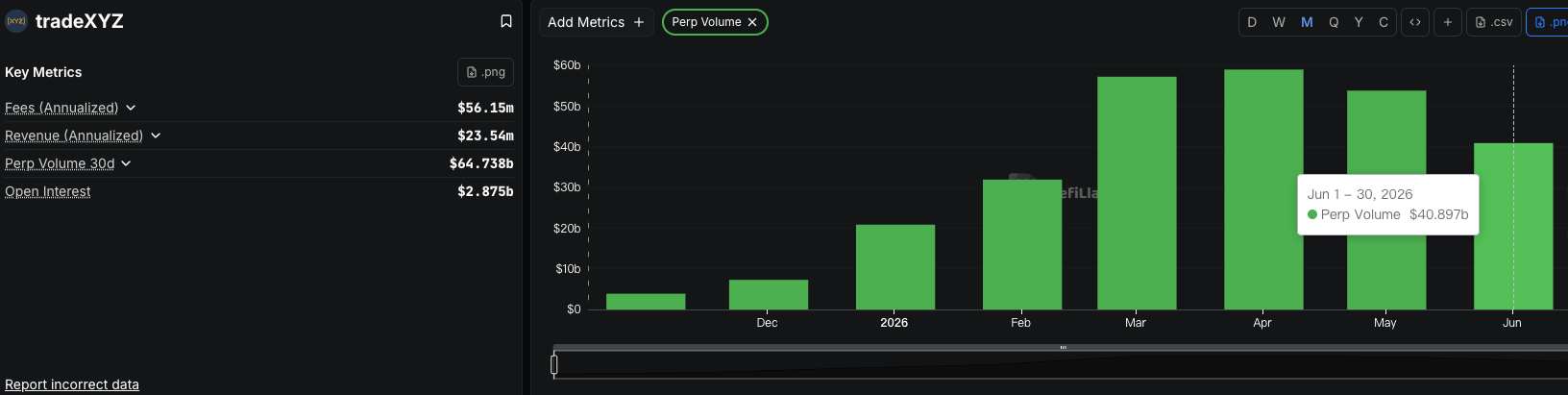

The one that is currently doing well, Trade.xyz, remains anonymous to this day.

The project founder has only hinted at his background in an interview with Hyperliquid founder Jeff Yan, where he mentioned that he bought his first Bitcoin for $66 in 2013 and has since been an investor without participating in projects; had it not been for Jeff, he would have exited the space long ago.

This person who ventured into the field midway created the largest pre-market market on Hyperliquid. According to Colossus, Trade.xyz has seen a weekly growth of 38% since last October, with a total trading volume exceeding $130 billion.

It first dealt with silver, then oil, followed by the S&P 500, and only then moved on to SpaceX.

They chose SpaceX very wisely.

With SpaceX set to ring the bell on Nasdaq on June 12th, the offering price and listing date were both certain. By listing the pre-market contracts, Trade.xyz was essentially betting on something that would eventually have an answer revealed; on opening day, Nasdaq would provide a true price. This true price acts like a tether, preventing the pre-market price from drifting too far. Even if there were discrepancies in between, the moment the bell rang, it would be pulled back.

And that’s how it turned out. In the days leading up to the SPCX listing, the reported price ranged from $154 to $172, betting on a premium above the $135 offering price, and indeed, the opening day shot up, proving correct.

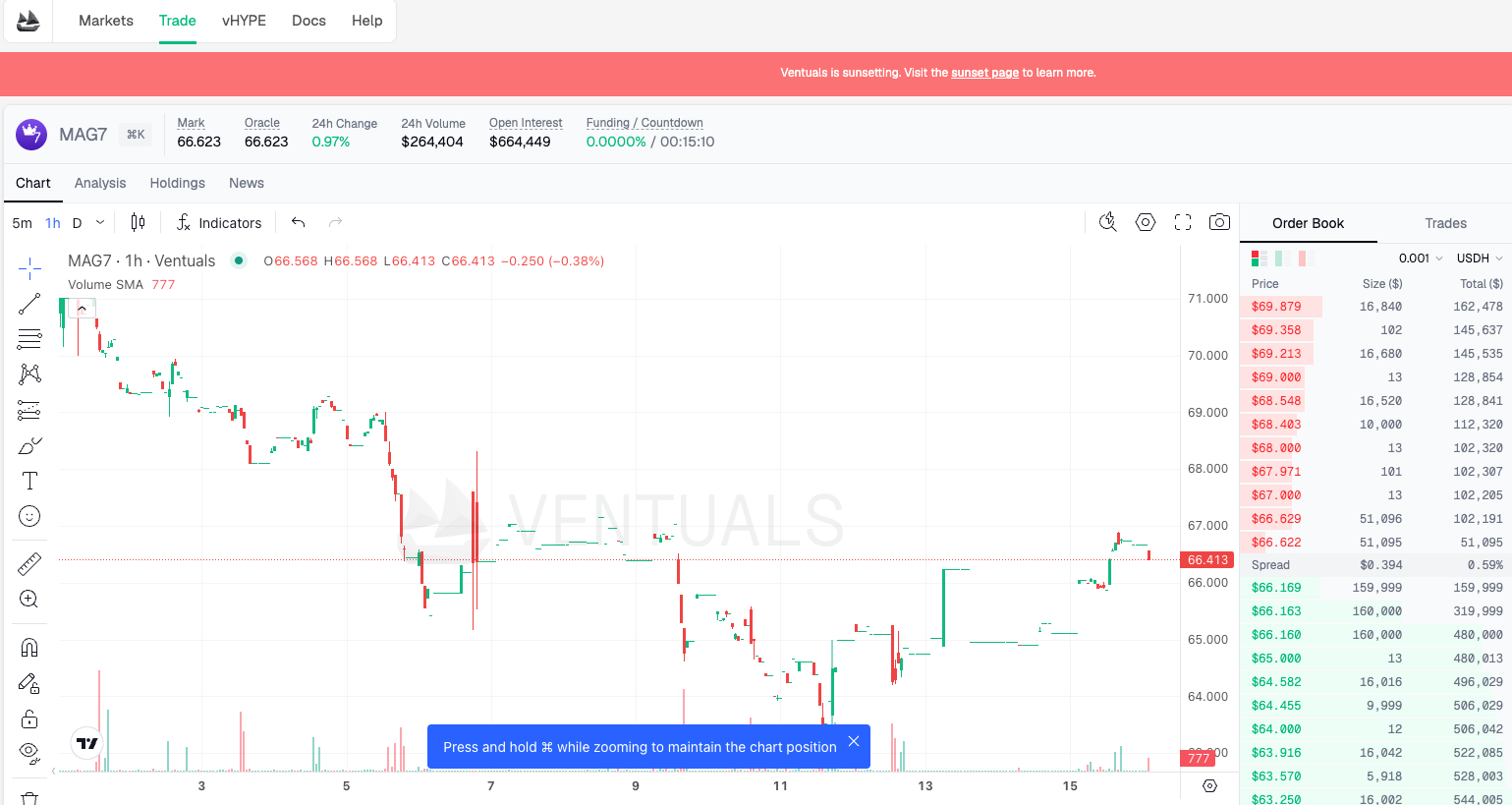

Ventuals chose an entirely different target.

Backed by Paradigm, one of the top venture capitals in the crypto space, it has a much more reputable background than the anonymous Trade.xyz. The brand it chose was also bigger: OpenAI and Anthropic, the two most scarce assets in the market.

But these two companies had no listing date in the near future.

There are no lack of anchoring prices for them outside. According to Bloomberg, Anthropic has allowed employees to sell old shares this year at a $350 billion valuation, and OpenAI also does this regularly. However, these prices are set privately, often involving existing shareholders who already hold substantial stakes, meaning assets have not truly exchanged hands in an open market.

Such pricing may be accurate at times, but it lacks an open order book that everyone can participate in to correct errors.

When Ventuals moved this pricing onto the chain to create contracts, it effectively hung the entire market on one or two internal price quotes. More troublesome still, they imposed a self-competitive mechanism on this price.

On-chain analysts have scrutinized Ventuals' pricing logic:

Its oracle price comes half from external transactions of old shares and financing valuations, and half from the average price of the contracts themselves. In other words, part of the price is referencing itself. As buying pressure pushes prices up, the average price increases, the oracle follows suit, raising the price ceiling, and thus continues to rise.

The result is that the prices of contracts for OpenAI and Anthropic remain permanently close to the ceiling, making it difficult for sell orders and settlements to transact. The charts may look like they’re steadily rising, but in reality, they’re structurally stuck, having little to do with real supply and demand.

Source of the chart: MAG7 targets on Ventuals, showing intermittent candlestick charts with some periods lacking transactions.

Thus, this Pre-IPO does not seem like the market is telling you how much OpenAI is worth, but rather a machine pushing the price up, then raising it along with its own output.

Trade.xyz bet on a target that would eventually be cleared by Nasdaq, which has a true price as a safety net if wrong; Ventuals bet on a target that only existed in internal quotes, and added a layer of self-circular pricing, leaving the price suspended in mid-air, with no foundation below.

Closure stock price reference: OpenAI $1300, Anthropic $1600

As it is about to close, does the final price it reported count?

When Ventuals shut down, it had to set a final price for its contracts to clear everyone's positions. Their method was to freeze the average price of the past 24 hours. OpenAI ended up at $1341.80 per share, and Anthropic at $1618.90.

These two numbers are now etched into the settlement records, becoming the last quoted prices left by these two companies on-chain.

As mentioned earlier, this price references half from external old stock prices and half from its own price average, continually climbing to the ceiling. In other words, the $1341.80 figure contains a significant portion that represents a result of the machine raising the price it had already established.

It is precise to two decimal places, but it may not be true.

The most ironic thing is that this price has indeed been taken seriously by some outside.

According to Bloomberg, employees of SpaceX, OpenAI, and Anthropic, as well as some late-stage investors, have approached Ventuals, saying they are using this platform to value their stock options.

I think this situation needs to be dissected.

These people hold valuable old stocks and are expected to know their worth better than anyone else. However, primary market quotes are squeezed into a toothpaste tube only once a year, leaving a blank space between rounds of financing, where no one knows whether the stock price has risen or fallen.

On the other hand, places like Ventuals, no matter how unreliable, at least report a number around the clock, allowing for observation of fluctuations.

Thus, a confusing situation arises. Those who should have the most pricing power, the insiders, end up fixating on a number from a retail market, seeking some psychological comfort.

This is the most twisted aspect of the pre-market pricing business.

The most scarce targets are in dire need of a fair price; the more missing price, the more people are willing to seize upon any number that resembles a price, even if it’s generated by a machine competing with itself.

Ventuals has closed down, thus those two final prices are frozen in place. However, the demand for references based on such numbers surely hasn’t decreased at all.

The pre-market pricing business, players are eager to enter

While demand hasn’t diminished, supply has instead increased and become more regulated.

In the same week that Ventuals shut down, Coinbase launched its own perpetual pre-market contracts, with the first target being SpaceX, aimed at users outside the United States.

Not only Coinbase. Polymarket has opened a prediction market for private company valuations using Nasdaq data, while Citi introduced tokenized private company shares for wealth and institutional clients. The crypto sector is entering this space, and traditional investment banks are also getting involved.

This is no longer just a few anonymous teams engaging in small skirmishes on Hyperliquid. Providing unlisted companies with prices that can be traded at any time is becoming a legitimate business that everyone wants a piece of.

For domestic readers, this demand is not unfamiliar. Initial public offerings require a queue, and primary market shares are divided only between institutions and high net worth individuals, leaving ordinary people without even the chance to touch it. Now, there are people quoting prices for companies like OpenAI and SpaceX, available for trading 24/7, offering many a first-time opportunity to engage with such assets. The demand is genuine.

However, Ventuals' closure in the past six months has exposed the critical vulnerability of this business.

The notion of price is not just about having people willing to trade; it requires an open market where anyone can step in and correct errors. Changing the operator to Coinbase won’t automatically resolve this vulnerability. It merely shifts from the banner of an anonymous team to that of a more reputable name. The underlying company still hasn’t gone public, and that fair price still doesn’t exist.

Will the next person taking over the pricing do it more accurately than Ventuals? The answer might only become clear once OpenAI actually stands on the day it rings the bell.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。