Original Authors: Jim, Frank, MSX Maitong

This week, the most important macro event in the U.S. stock market is undoubtedly the June FOMC.

However, this time, what the market is truly concerned about is not merely a simple question of "Will there be an interest rate hike?" or "Will there be a cut?".

According to current market expectations, it is highly likely that the Federal Reserve will remain on hold in this meeting, keeping the federal funds rate in the range of 3.50%—3.75%. In other words, the decision to keep rates unchanged in June is not surprising and has even been anticipated by the market in advance.

What is truly significant is that this is the first complete interest rate meeting led by Kevin Walsh since he assumed the role of Federal Reserve Chairman.

More importantly, this meeting also includes an economic projections summary, meaning the market will simultaneously see the rate decision, policy statement, dot plot, and economic forecasts. For investors, this is not just an ordinary meeting, but the first full appearance of Walsh's version of the Federal Reserve.

Therefore, the core question for this week's FOMC is not whether Walsh is hawkish or dovish, but rather what is it that we should really focus on?

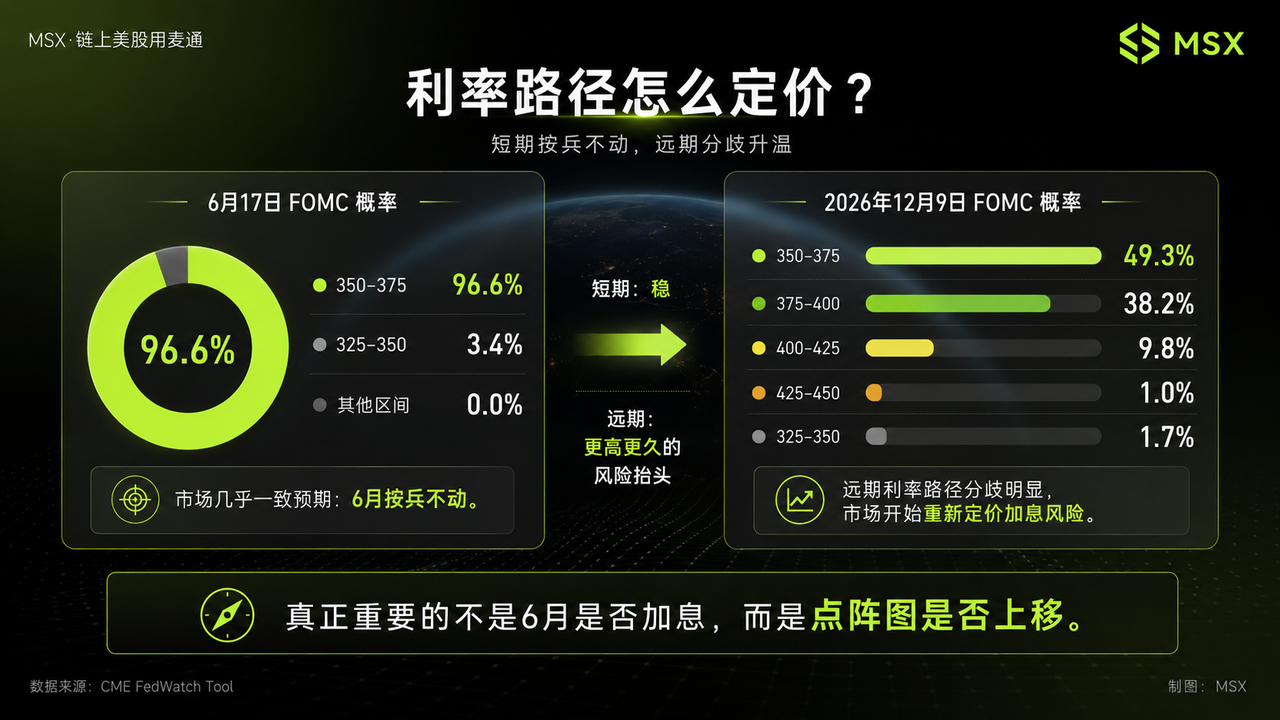

1. High likelihood of staying put in June, but the market is trading the "next steps"

To conclude, the Federal Reserve is highly likely to stay put this week.

From the perspective of interest rate futures pricing and mainstream institutional expectations, maintaining interest rates at the June meeting has almost no suspense, as the market generally expects the Federal Reserve to keep the benchmark rate in the range of 3.50%—3.75%. The CME FedWatch also shows that the probability of staying in this range on June 17 is as high as 96.6%.

Therefore, the real points of divergence in the market are not in June, but in several meetings in the second half of this year, which is also the aspect of the FOMC that is most prone to misinterpretation.

If we only look at the June interest rate decision, it is easy to conclude with a simple judgment: since there is no rate hike, does this mean good news for U.S. stocks?

Not necessarily.

What U.S. stocks truly fear is not the lack of a rate cut this time, but rather that the "rate cut path" the market originally traded is suddenly overturned.

For some time now, risk assets, especially AI, semiconductors, software, and small-cap growth stocks, have been enjoying two layers of expectations: one that the economy is not showing significant recession, and the other that the Federal Reserve still has room for rate cuts in the future. As long as these two expectations hold, high-valued assets still have reasons to maintain a high risk appetite.

But now the situation has become more complex. In May, the U.S. CPI year-on-year rose back to 4.2%, with energy prices increasing by 23.5% year-on-year, and gasoline prices rising by 40.5%. This indicates that the situation in the Middle East, fluctuations in oil prices, and disruptions to the supply chain are starting to reflect in inflation data. Meanwhile, core CPI rose 0.2% month-on-month and 2.9% year-on-year; although not completely out of control, it still exceeds the Federal Reserve's target of 2%.

This set of data is very awkward for the Federal Reserve.

If Walsh continues to emphasize rate cut possibilities, the market may question whether the Federal Reserve is underestimating the inflation rebound; but if he directly signals a rate hike, high-valued assets may soon be reassessed.

Thus, the most likely scenario for this meeting is not a clear dovish signal, nor a direct hawkish shift, but a transition of the Federal Reserve from "more likely to rate cut next" to "maintaining options."

But the key lies here, this statement sounds mild, but it is not mild for market pricing.

Because once a rate cut is no longer the default path, the valuation anchor for the U.S. stock market needs to be recalibrated. Especially those growth stocks that have already seen substantial increases and their valuations are overly extended, what they fundamentally fear is not whether rates change today, but rather that the market suddenly realizes: the second half of the year is not waiting for a rate cut, but is expected to reassess the risks of rate hikes.

Thus, what we should really watch this week is not whether there are changes to the June interest rate, but whether the Federal Reserve officials' assessments of the rate path for the next 12 months have shifted upward.

The dot plot is the first trump card for this meeting.

2. Walsh finds it hard to be directly dovish; key is how he explains inflation

Walsh's current position is very delicate.

On the one hand, his past policy orientation is closer to that of the Trump administration, leading the market to believe that he may be more willing than Powell to support low rates; on the other hand, he must establish his policy credibility during his first appearance, especially in the context of rising inflation.

This makes it difficult for him to come out swinging with a dovish stance right away.

Moreover, the complexity of the current inflation issue lies in the fact that it includes both short-term disturbances from energy shocks and potential risks of spreading to other prices.

If we only look at core CPI, the market can still argue that underlying inflation is under control; but when looking at the overall CPI and energy prices, the Federal Reserve finds it difficult to ignore inflationary pressures completely. More troubling is that the Federal Reserve's Beige Book also shows that several regions have recently reported rising cost and price pressures, with energy-related costs spilling over into transportation, packaging, food, fertilizers, etc., and non-labor input costs rising faster than sales prices.

This means that Walsh cannot just focus on a 0.2% month-on-month increase in core CPI. The real question he needs to answer is whether current inflation is merely a one-time energy disturbance or is evolving into broader secondary inflation pressures?

If Walsh believes that oil price shocks and tariff disturbances are mostly one-time events and that core inflation remains controllable, the market will interpret this as the Federal Reserve not rushing to hike rates, allowing risk assets to have space to breathe.

However, if he emphasizes that energy prices are transmitting to transportation, food, wages, and service prices, or explicitly mentions the risk of inflation spreading, then the market will interpret this press conference as a hawkish turn.

Thus, the importance of the press conference is no less than that of the interest rate decision itself.

The market wants to hear not whether Walsh says "inflation is high," but how he characterizes this round of inflation.

If he defines inflation as a "short-term shock," it would signal a friendly stance; if he defines it as “potentially spreading pressure,” it suggests that the Federal Reserve still needs to maintain a tighter policy stance; if he further emphasizes that the Federal Reserve must re-anchor inflation expectations, the market will start worrying that the forthcoming dot plot, balance sheet reduction, and interest rate path will all turn hawkish.

For the U.S. stock market, the difference here is enormous.

The former implies that valuations can continue to be supported by liquidity and risk appetite, while the latter suggests that U.S. Treasury yields may rise again, and high-valued tech stocks may be the first to face revaluation by the market.

And because of this, the true spotlight of this FOMC is not whether Walsh personally is "hawkish" or "dovish," but whether he will lower the Federal Reserve's tolerance for inflation.

This is the signal the market cares about the most.

3. More important than interest rates are balance sheet, communication style, and liquidity expectations

The biggest difference between Walsh and Powell may not lie solely in interest rates but in the balance sheet and communication style.

In recent years, the market has become accustomed to the high transparency of the Powell era: there is a press conference after each meeting, officials speak frequently, and the dot plot provides path references, allowing the market to trade around these statements on "rate cut expectations" and "tightening expectations" repeatedly.

However, Walsh has always been cautious about this excessive forward guidance; he prefers to reduce the Federal Reserve's explicit commitments to future interest rate paths and does not want the market to rely excessively on central bank statements to bet on asset prices.

This could bring about a significant change, namely that future transactions with the Federal Reserve may not just focus on a single question of "will there be a rate cut," but will need to return to the data itself.

In the short term, Walsh is likely not to completely scrap the dot plot right away nor will he immediately require the Federal Reserve to enter what is referred to as a "communication black box." But he might lower the market's dependence on the dot plot and forward guidance through fewer commitments, fewer path hints, and a greater emphasis on data dependency.

This may not be friendly for risk assets. In recent years, the valuation support for many high-valued assets has come from the market's premature speculation about the liquidity environment. As long as the market believes that the Federal Reserve will eventually cut rates, long-term growth stocks will react in advance. But if Walsh allows the Federal Reserve to reduce commitments, the market must bear greater interest rate uncertainty.

Another angle pertains to the balance sheet. As of June 10, the Federal Reserve's total assets were approximately $6.725 trillion. For Walsh, balance sheet normalization may offer a "middle path," meaning rates initially remain unchanged, but the tightening signal is released through balance sheet normalization.

This has a very subtle impact on the market.

If Walsh merely states that the balance sheet will continue to normalize gradually, the market is likely to accept it; however, if he suggests that balance sheet reduction could take on a larger role in curbing inflation and reducing liquidity reliance in the future, then the U.S. stock market will need to reassess liquidity discounts.

Especially for AI, semiconductors, software, and high-quality growth stocks, the core trade over the past period has not just been about earnings growth but also the alignment of rates and liquidity environments. Once the market begins to understand that "Walsh's version of the Federal Reserve is not in a hurry to cut rates, nor wishes to continue letting the market rely on the central bank for support," high-valued sectors may quickly encounter valuation pressures.

Thus, for the U.S. stock market, the three most important signals this week are very clear:

- First, whether the dot plot has shifted upward, especially whether it has transitioned from "there is still room for rate cuts" to "not cutting rates may even pose a risk of rate hikes";

- Second, how Walsh explains inflation—whether he sees energy shocks as short-term disturbances or emphasizes secondary inflation and transmission risks;

- Third, whether balance sheet reduction and communication style will be positioned more prominently, becoming the starting point for Walsh to reshape the Federal Reserve's policy framework;

If the final result is to stay put, the dot plot is mildly revised, and Walsh emphasizes data dependence but is not in a hurry to raise rates, then the market may fluctuate in the short term but may not necessarily damage the main trend of AI and tech stocks, as long as oil prices continue to retreat and the 10-year U.S. Treasury yield does not rise again, high-quality tech stocks still have the opportunity for recovery.

However, if the dot plot clearly shifts upward, Walsh emphasizes the risk of inflation spreading, or positions balance sheet reduction as a more important tightening tool, then the U.S. stock market needs to be cautious about a short-term reassessment of valuations—and the pressure will still be greatest on high-valued tech stocks, small-cap growth stocks, and long-duration assets that are most sensitive to interest rates.

In other words, the best outcome from this FOMC is not that Walsh goes fully dovish, but that he acknowledges inflation risks without rushing to tighten; the worst outcome is not simply not cutting rates in June, but the market discovering that the narrative of the Federal Reserve's rate cuts has officially ended.

Therefore, strategy-wise this week, it is not recommended to blindly bet on a direction before the FOMC.

Conclusion: Do not bet on answers in advance; wait for the market to provide direction

Thus, strategy-wise this week, it is not recommended to blindly bet on a direction before the FOMC.

Before and after the meeting, the market may easily experience an upward surge followed by a drop, or a drop followed by a surge. A more prudent approach is to wait for the dot plot, press conference, and U.S. Treasury yield signals to materialize before determining whether to increase positions.

In summary, this FOMC is not about whether Walsh's statement is hawkish or dovish, but whether he will redefine the Federal Reserve's reaction function.

If the answer is "no," risk-on trades still have space to continue; if the answer is "yes," then the market will need to relearn how to price a Federal Reserve that is less committed, places a greater emphasis on inflation, and highlights liquidity discipline.

Let us wait and see.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。