The original text comes fromFour Pillars

Compiled by / Odaily Planet Daily Golem (@web 3_golem)

Editor's note: On June 16, the Korean exchange Bithumb launched a new meme coin called Spacecoin, followed closely by Upbit launching an outdated meme coin SPX6900. The community generally believes that the reason these two major crypto exchanges in Korea launched these two tokens is that their names happen to be similar to the stock ticker of SpaceX, and the exchanges want to leverage the hype around "meme coins" to attract trading volume.

Amid a weakening crypto market where Korean crypto investors are turning to stock trading, the performance of Korean exchanges collectively declined in Q1 2026, making it urgent for them to take measures to reverse the downturn. However, unlike other overseas exchanges that can transform into "everything exchanges" and list a large number of tokenized stocks to meet the demand of crypto traders, Korea categorizes tokenized stocks as securities, thereby prohibiting crypto exchanges from engaging in such trades and also restricting domestic crypto exchanges from dealing in cryptocurrency futures, derivatives, or exchange-traded funds (ETFs).

The regulatory measures in Korea aimed at protecting investors have, paradoxically, pushed crypto exchanges into the most speculative corner of the market. After all revenue sources and new product lines, such as derivatives, tokenized stocks, and prediction markets, were banned, exchanges are inclined to list those “meme” tokens that attract attention and are also more speculative to increase platform trading volume.

Upbit and Bithumb launch "pseudo SpaceX stock", shocking the Korean community

Bithumb and Upbit launched tokens resembling SpaceX's stock ticker

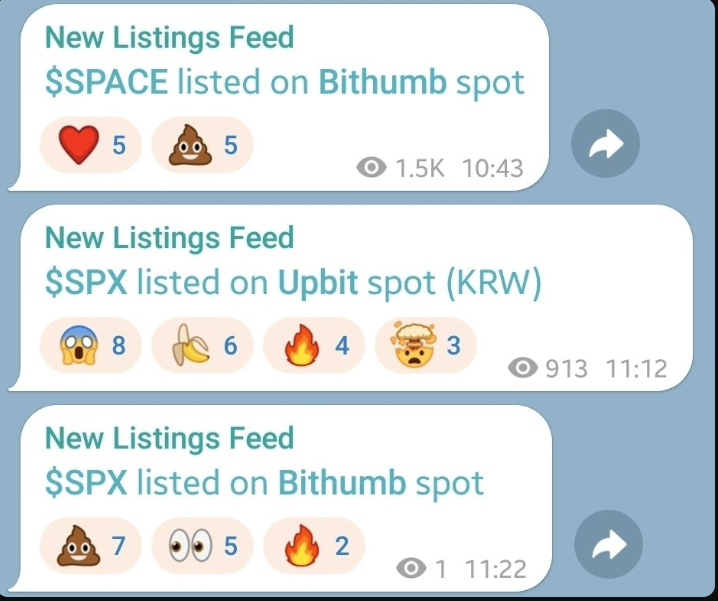

On the morning of June 16, the hottest topic in the Korean community was Bithumb's listing of an unknown project token Spacecoin (SPACE) and Upbit's listing of the meme coin SPX6900. One might ask, isn't this just a regular token listing announcement? What actually sparked the community's reaction was not the listing itself, but the token names and the timing of their listings.

Four days earlier, on June 12, SpaceX went public on NASDAQ under the ticker SPCX. It is well known that SpaceX's IPO set a record high, and as stock-related topics have become dominant in the Korean cryptocurrency community, SpaceX also emerged as the hottest topic over the weekend.

Therefore, after Upbit and Bithumb issued their listing announcements, a suspicion spread within the community that these two exchanges were listing tokens with names and codes very similar to SPCX, ostensibly to ride the hype and gain trading volume. While this connection is merely coincidental, this interpretation not only seems reasonable but also reflects the current situation of Korean exchanges.

Currently, overseas platforms such as Coinbase, Binance, and Bybit allow users to trade SpaceX and other foreign stocks directly within their exchanges, but due to regulatory restrictions, Korean exchanges cannot offer such products, so they may only list a token similar in name to SpaceX.

However, this matter should not be seen merely as a joke; it precisely reflects the difficult position of Korean crypto exchanges in competing with their overseas counterparts.

Status of Korean Exchanges

Overall performance decline, even losses

The performance of Korea's two major exchanges in Q1 2026 was poor.

Upbit Q1 2026 performance. Source: FSS DART

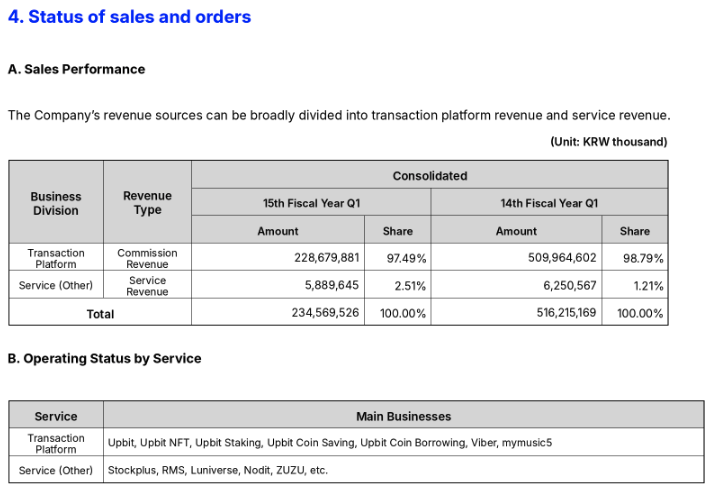

According to the quarterly report published on May 15 through the electronic disclosure system of the Korean Financial Supervisory Service, Dunamu, which operates Upbit, reported consolidated revenue of 234.6 billion KRW, a 54.6% decrease year-on-year, with operating profit down 77.8% to 88 billion KRW, and net profit down 78.3% to 69.5 billion KRW. Upbit’s fee revenue fell 55.2%, down to about 200 billion KRW, while operating costs rose by 22% during the same period, causing a squeeze on profit margins.

Bithumb Q1 2026 performance. Source: FSS DART

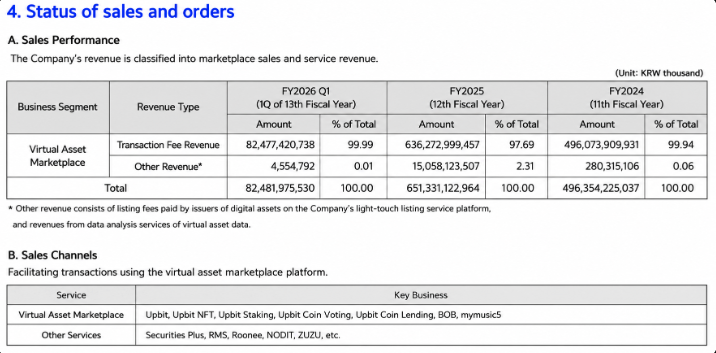

Bithumb's situation is even more severe. Q1 revenue fell 57.6% to 82.5 billion KRW, operating profit plummeted 95.8% to 2.9 billion KRW, and the company reported a net loss of 86.9 billion KRW, marking its second consecutive quarter of net losses. The direct cause of the loss is the shrinkage of trading volume which led to an 87% decrease in fee revenue. Additionally, Bithumb was fined 36.9 billion KRW by the Korean financial intelligence agency for violating the Specific Financial Transaction Information Act and subjected to a partial business suspension of six months, which also reflected in the Q1 performance.

The biggest issue with Korean exchanges is that their revenue structure relies almost entirely on trading fees. Trading fees account for about 97.5% of Dunamu’s revenue and 99.99% of Bithumb’s revenue, making fees effectively their entire income. Rather than a negligence in the operational methods of the exchanges, this structure is created by the regulatory environment faced by Korean crypto exchanges (as detailed below).

Narrow business scope, can only support crypto spot trading

In reality, the business that Korean crypto exchanges can engage in is limited to crypto spot trading, with other areas mostly restricted, either explicitly or implicitly evaded. Here are the businesses that Korean crypto exchanges are prohibited from engaging in:

- Tokenized stocks: In June 2026, the Korean Financial Services Commission and Financial Supervisory Service classified tokenized stocks as securities rather than virtual assets. Regardless of how they are issued, securities are governed by the Capital Markets Act; according to the Electronic Securities Act, only licensed electronic registration institutions can conduct electronic rights registration. If a crypto exchange other than such institutions issues or circulates security-type tokens, it amounts to unlicensed operations. In other words, the rapidly developing tokenized stocks abroad are not permitted assets structurally within Korean currency exchanges, and this situation is unlikely to change.

- Futures and derivatives: Korean crypto exchanges can only offer spot trading and cannot provide domestic users with derivatives such as perpetual futures or options. This is less a clear legal prohibition and more a shadow left by a previous attempt. One of Korea's five major exchanges, Coinone, operated a leveraged contract trading service with up to four times leverage starting in December 2016 for about a year. At the end of 2017, as government regulatory measures and police investigations were launched, this service was completely shut down. In 2018, police classified the service as gambling due to its operation without financial regulatory body approval and referred CEO Cha Myung-hoon and others to prosecutors, even arresting 20 users with trading volumes exceeding 3 billion KRW for gambling charges. The case was closed three years later in 2021 without prosecution due to a lack of evidence. However, since then, no Korean crypto exchange has been involved in leveraged trading or futures trading.

- Self-regulatory implicit avoidance: Korean crypto exchanges are subject to self-regulatory oversight by the Digital Asset Trading Alliance (DAXA), which consists of five major won exchanges. Their listing review standards include opacity caused by de-identification, the possibility of securitization, and the potential for money laundering. These standards effectively exclude privacy coins that emphasize anonymity and lead exchanges to avoid listing tokens that may be seen as securities. For the same reasons, assets likely to trigger disputes over securities or gambling, such as exchange tokens or prediction market tokens, are seldom seen on Korean exchanges.

In summary, almost all new fields being expanded by overseas exchanges, such as crypto derivatives, tokenized stocks, privacy coins, and prediction markets, are restricted in Korean exchanges.

Korean exchanges have fallen behind in competing with global exchanges

Did Korean exchanges lower their token listing standards?

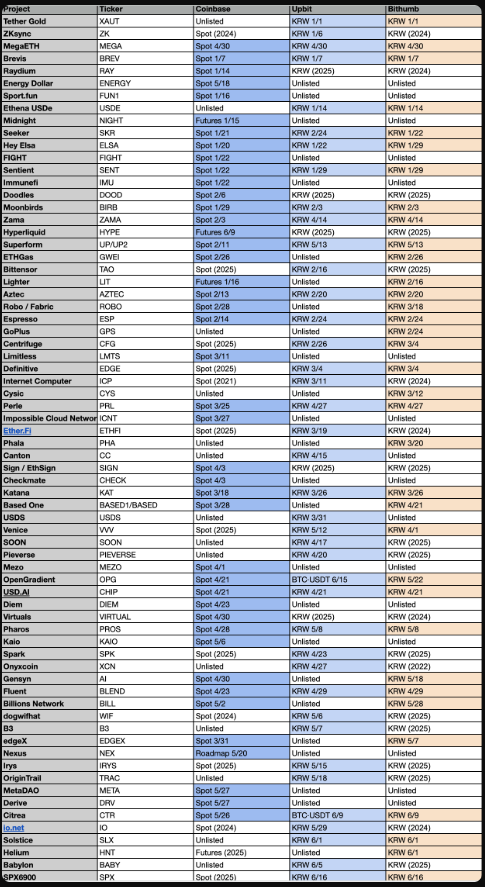

Recently, the community has accused Upbit and Bithumb of loosening their token listing review standards. The following table is a complete comparative list of tokens listed by Coinbase, Upbit, and Bithumb in 2026:

Tokens listed by Coinbase, Upbit, and Bithumb in 2026. Source: Four Pillars (@c4lvin)

In terms of the number of tokens listed, Coinbase leads the way. Coinbase has listed many assets that the two Korean exchanges do not offer, a significant portion of which not only provide spot trading but also offer contract trading, providing trading opportunities earlier than other trading platforms. From the perspective of frequency and timing, Coinbase is actually more proactive.

In 2026, among the many new KRW tokens listed on Upbit, a considerable share had already been listed on Bithumb, such as Bittensor (TAO), Internet Computer (ICP), Ether.fi (ETHFI), io.net, dogwifhat, Spark (SPK), and Babylon, most of which had low trading volume on Bithumb. They are not newly issued assets but tokens that already existed in the market, only cataloged after listing on Upbit, which may result in Upbit's listings seeming less fresh.

This perception of a decline in token quality is not due to a lowering of standards, but rather the diminishing trading volume effect that comes with token listings. In an environment where trading volumes from single token listings quickly diminish and new assets worth listing are becoming increasingly scarce, Upbit is maintaining listing speeds by listing existing tokens from Bithumb.

Ultimately, Korean users' complaints are less directed at a specific name than at the gap they feel in convenience compared to other markets, as other markets have newer products like tokenized stocks.

Korean exchanges excluded from the SpaceX listing feast

Meanwhile, the developmental direction of large overseas exchanges is entirely different. They are striving to break through the limitations of virtual assets to create what is described as an "everything exchange," a single application capable of trading all assets.

Among the most notable is Coinbase. In its Q4 2025 shareholder letter, Coinbase stated that in addition to cryptocurrencies and derivatives, it has begun trading stocks and ETFs within its app and has opened approximately 3000 assets to early users, aiming to integrate traditional and digital assets into a unified investment experience. The letter also emphasized that Coinbase has become the first company in the industry to launch 24-hour U.S. perpetual contract products, thereby increasing its share of the derivatives market.

Binance's approach is more direct. Starting from June 1, 2026, Binance opened U.S. stock trading to eligible users, allowing them to directly trade over 7000 American-listed stocks and ETFs. Additionally, Binance launched bStocks, a token that tokenizes U.S. stocks on a one-to-one basis, with settlements in stablecoins that can be withdrawn to users’ self-custodial wallets, supporting round-the-clock trading.

Bybit joined the xStocks alliance and launched tokenized stocks created by a regulated Swiss issuing institution, with price-tracking tokens backed by real stocks and traded in stablecoins around the clock.

In summary, overseas crypto trading platforms have emphasized promoting tokenized stocks. The disparity in trading environments between Korea and abroad is most vividly illustrated by the SpaceX listing process, where overseas exchanges viewed it as a test of competition in tokenized stocks, all launching pre-market contract products and tokenized stocks.

Within 24 hours of the launch of SpaceX-related products, the entire cryptocurrency market's trading volume reached approximately $9 billion, with Binance alone accounting for $5.6 billion.

In contrast, Korean crypto exchanges missed out on this feast, as neither tokenized stocks, perpetual contracts, nor any products tracking SpaceX are allowed for trade in Korea. While the world's major exchanges engaged in billions of dollars' worth of trading around the same hot topic, Korean crypto exchanges had no channels to participate.

Korean exchanges are suffocating under regulation

For an exchange unable to compete on product variety with the rest of the world, the only battlefield left is the crypto market. The revenue of Korean exchanges actually relies on spot trading fees, and in an environment where they cannot list derivatives or stocks, the only way to increase trading volume is to list tokens that attract investors’ attention at the right moment.

Korea's strict regulation of crypto exchanges aims to protect investors. It classifies leveraged trading as gambling and prohibits it; it filters out securities-type tokens with opaque rights structures and excludes those that can be easily used for money laundering or price manipulation from the listing review process.

However, as this protective mechanism gradually strips the exchanges of their revenue sources and product lines, their only remaining means is to list crypto spot trades. As the trading volume in the crypto market continues to shrink, Korean exchanges tend to lean towards listing more speculative assets that generate higher attention. The protective measures of the product stage ultimately promote the influx of speculative assets during the listing phase, as exemplified by the recent listings of tokens with names similar to SpaceX's stock ticker by the two major exchanges.

A deeper issue lies in the fact that even this protective mechanism is not entirely effective. Korean investors wanting to purchase perpetual contracts or tokenized stocks will not easily give up their demand, and they will turn to overseas platforms like Binance, Bybit, and Hyperliquid.

In other words, Korean regulation itself cannot eliminate high-risk trading for investors; it merely pushes high-risk trading into markets that the Korean authorities cannot monitor. When tax and cross-border information exchange (CARF) are fully implemented in 2027, the scale of this offshore trading will be reflected in the data. Ultimately, investors will bear speculative risks regardless while losing domestic regulatory protections, while Korean exchanges miss out on the income these trades would have generated.

This structure also renders Korean exchanges themselves vulnerable, with a single product, almost all revenue coming from trading fees, and fully exposed to the fluctuations of trading volume cycles. Coinbase diversifies its income across custodial, stablecoin, tokenized stocks, and derivatives operations to buffer against market downturns, while Korean exchanges must endure the same cyclical fluctuations due to reliance on a single product. As this gap accumulates season by season, it ends up evolving into discrepancies in investment capacity and product competitiveness, and this difference will resurface, much like the convenience gap felt by domestic users.

Of course, the Korean government is also vigorously promoting cryptocurrency regulation. A series of plans, including the second phase of the Basic Law on Digital Assets, the institutionalization of Security Token Offerings (STOs), approval for company trading, issuance of KRW stablecoins and spot ETFs, will all be launched simultaneously in 2026, fully reflecting the government's determination. However, even if these new regulations are eventually rolled out, they may not be operated by existing crypto exchanges but rather be assigned to licensed agencies such as securities firms and electronic registration institutions.

Therefore, what is happening now is not a transformation of crypto exchanges into securities companies but rather securities firms and banks acquiring stakes in crypto exchanges and integrating them into the same system. In 2026, Hanwha Investment & Securities increased its stake in Dunamu to 9.84%, becoming the third-largest shareholder; Hana Financial Group holds 6.55%; Samsung Securities, Samsung Credit Card, and Samsung SDS each hold 4%. Korbit was acquired by Future Asset Group; Korea Investment Securities signed a strategic equity investment agreement to acquire 20% of Coinone, becoming its third-largest shareholder. As financial regulatory bodies take a cautious approach towards the separation of finance and cryptocurrency and lean towards loosening restrictions, such alliances are rapidly increasing.

Will Korea allow crypto exchanges to develop into "everything exchanges" like abroad? The likelihood of that is minimal.

But this article does not advocate for an immediate deregulation; rather, it suggests that the protective framework designed for a certain era, which has caused more hidden costs as the market rapidly trends towards asset integration. In such a grim environment, Korean crypto exchanges operating in a bear market like the current one will pass these costs onto users, ultimately leading to a resurgence of transient "meme coins" in high demand, resulting in more victims.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。