For more than half a month, $1600, 30%+ return, but what I want to say in this article is not how to make money.

Written by: Tyler

A couple of days ago, the article I built an investment workbench for myself with AI shared several tools I coded: a cross-market asset panel, investment mapping, personal content operation platform, and a frequently used Polymarket betting monitoring panel.

In this more than half a month, I tested with about $1600 in capital, achieving a return of 30%+. The panel's real-time data statistics and the final actual net profit roughly aligned, with only about $6 difference, which is minor errors from orders/liquidity rewards and such.

However, what I want to say in this article is not "Polymarket is great for making money," nor do I want to present it as an arbitrage tutorial.

On the contrary, after running this round, I increasingly feel that Polymarket is not a place suitable for charging in with an "arbitrage" mentality.

1. Let's start with what this panel is about

I started coding this panel around May 21.

The initial need was very simple; I didn't want to open several betting pages to switch back and forth between yes/no changes, nor did I want to fill records manually in Excel.

That's right, before this, I had been using Excel to record buy-sell transactions, unrealized profits and losses, settlement points, event types, using a clumsy method.

But those who have actually played know that many bets on Polymarket can easily go out of control because the functionality of manual record-keeping is very poor: for instance, I might initially want to make a small bet, but once the odds shift, I want to increase my stake, as it lacks an intuitive grasp; or, if a certain betting event suddenly moves, and I don't update the spreadsheet data in time, I might miss the stop-loss/add-position window, among other similar situations.

Ultimately, the process is too fragmented, and without a system, people can easily make decisions based on emotions.

So from the beginning, I built this panel to put each bet back into a unified framework, turning this feeling into a relatively visual and horizontally comparable information presentation.

After several iterations, I split it into two tabs: "Position Dashboard" + "Opportunity Monitoring."

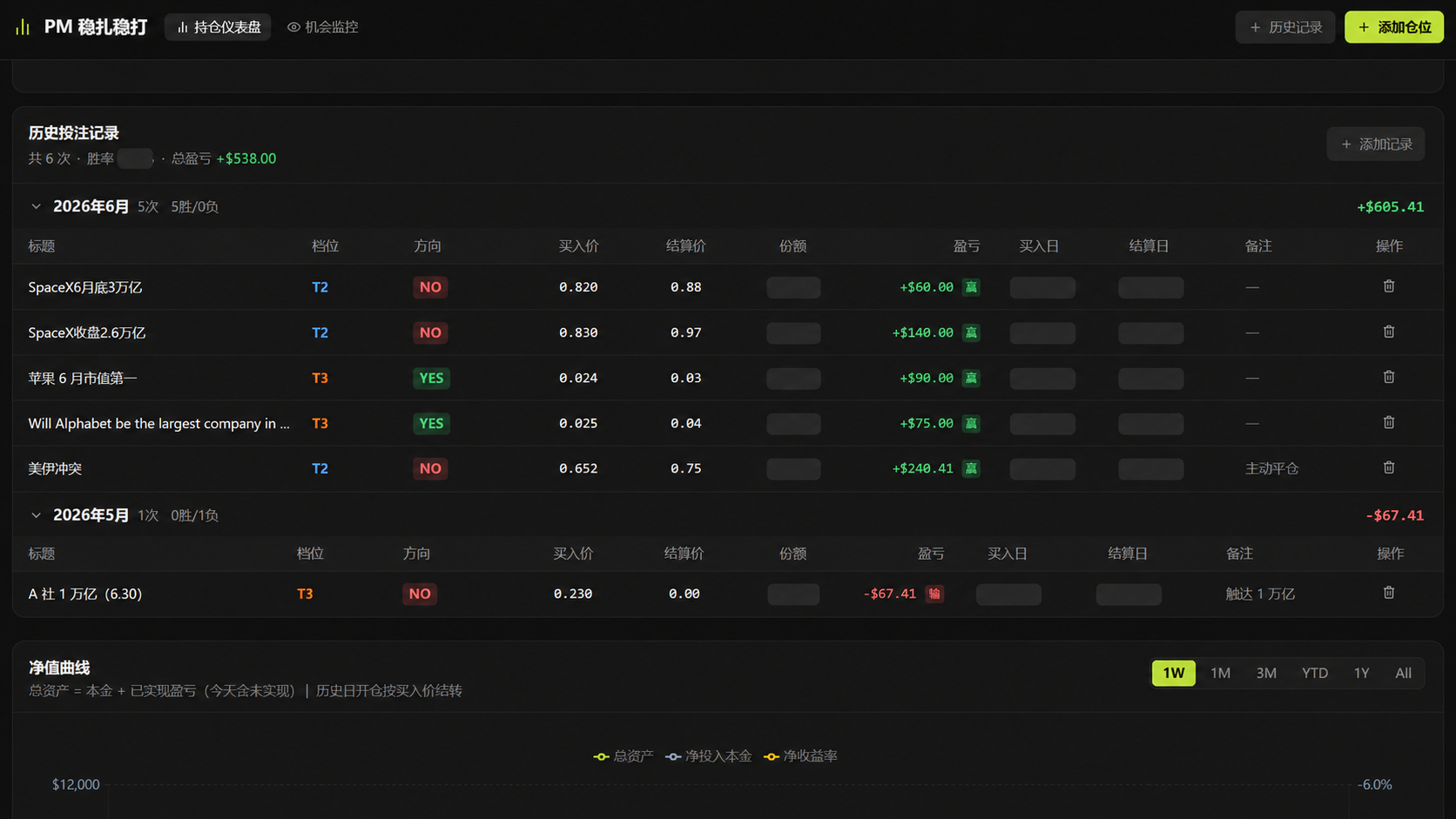

The "Position Dashboard," as the core of the entire panel, is a dynamic system that can fetch PM real-time data and recalculate, divided into several functional areas (you can refer to the image at the beginning):

Overview Bar: Total capital (planned, actual reference is not very significant), invested capital, position value, unrealized profits, total unrealized profits (including closed positions), all at a glance;

Tier Proportion: This is the core risk control module of the panel, and I believe it is the most counterintuitive and important area in the whole panel, I’ll tease more about this, and detail it in the next chapter;

Thematic Cluster Exposure: I tagged each bet with a "thematic cluster," dividing it into East Asia, the Middle East, Crypto, US stocks, Pre-IPO (can customize additions/deletions), and the panel automatically summarizes the proportion of each cluster, setting a maximum threshold of 12% for a single cluster, why design it this way? Primarily to counter the most hidden traps on PM — false diversification, which I will discuss in detail in the next chapter;

Single Position Details: Tier, direction, buy price, settlement price, shares, profit/loss, buy date, settlement date, remarks, etc., clearly arranged in a line, and can be sorted in ascending or descending order and filtered by tags;

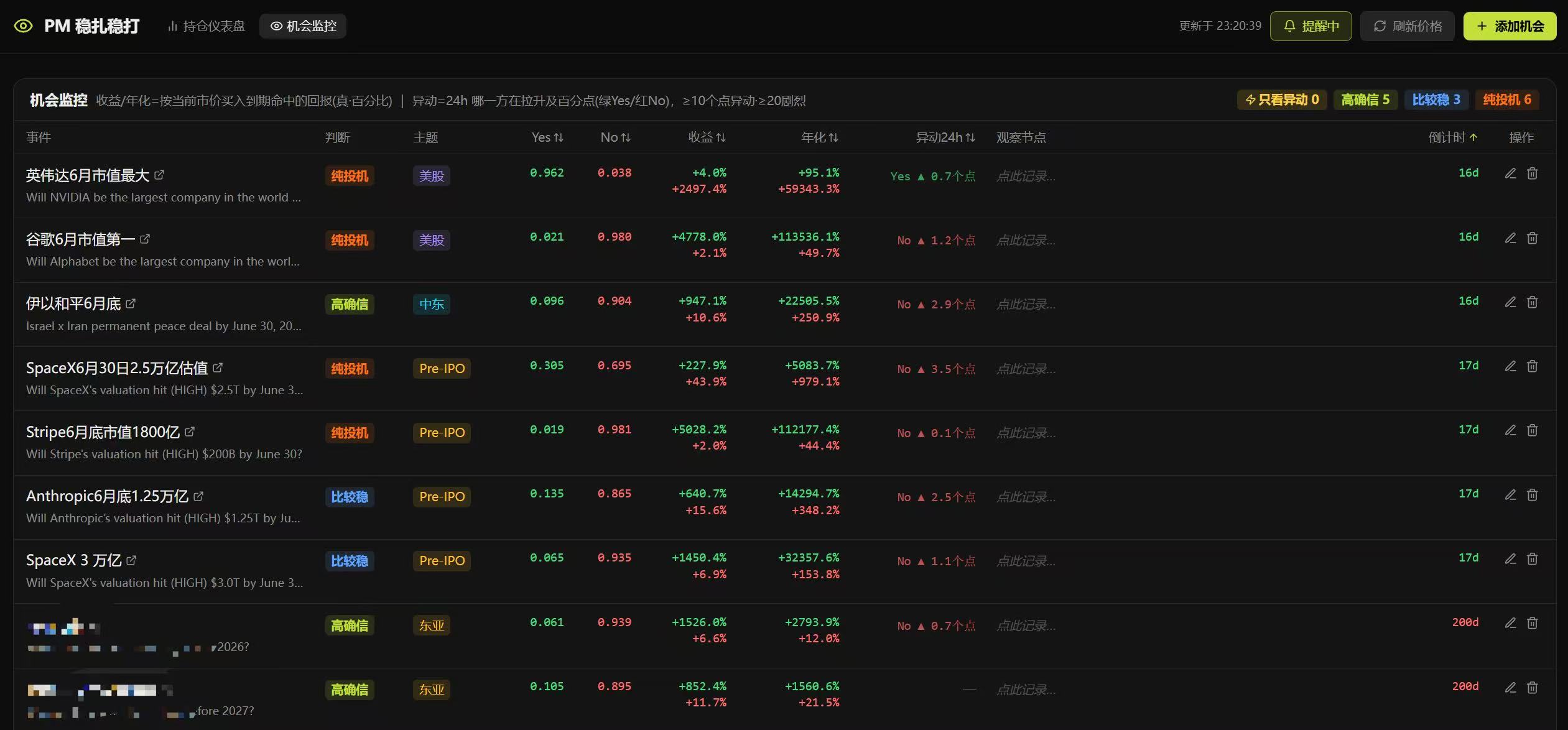

The "Opportunity Monitoring" is a watchlist where I place markets I am interested in but have not yet wagered on.

Each market records several key fields, including event name (with hyperlinks for direct access to the trading page), T1/T2/T3 tiered judgments, current yes/no prices, returns, annualized returns, anomalies (customizable thresholds, for example, if there’s movement exceeding 20% within 24 hours, as long as the webpage is open, it will pop up reminders), my set observation nodes, and a countdown to the expiry of the bet.

Here are two small designs I’m quite satisfied with: first, I found the right interface for PM, directly parsing the webpage link of betting events, which automatically prompts yes/no options, corresponding prices, and categories for different options under the same event, significantly reducing manual entry trouble; second, the Tier affiliation of the same bet will automatically reshuffle with remaining days.

Not long ago, before Anthropic released Mython, there was a significant price movement in the watchlist, which could basically be judged as a high-probability certainty event; at that time, entering the market could yield about a 10-point return — such opportunities are hard to capture consistently without a watchlist.

2. PM's Mathematical Expectation Trap and the "T1, T2, T3" Design Principles

The above is a simple introduction, but I want to discuss a thought I've had after testing in practice.

That is, in binary markets like PM, there exists a significant structural trap that is unfriendly to players who enjoy "single heavy positions," but is more suitable for those who are used to "opening a supermarket and buying a bunch."

I will try to clarify my thoughts; if there are errors or omissions, just pretend you didn’t see them:

Assuming a certain betting event's yes price c is 0.80, meaning the market believes there’s an 80% chance this event will occur, while if I judge the event's actual occurrence probability q to be 0.90, it means the expected return rate for this bet can be roughly calculated as:

EV = q / c - 1 = 0.90/0.80 - 1 = 12.5%

This looks good, but PM is not a bond; this 12.5% hides a sharp tail risk: if you judge incorrectly, the loss is not 12.5%, but 100%.

Thus, in the panel, I do not only look at "expected return rate" but also focus on two things simultaneously:

One is the gap between my own probability judgment and the market price, that is, q - c (I set an automatic stop-profit reminder target value, which is the midpoint between buying price and 100), which is the core of whether edge truly exists;

The other is the impact of a single position going to zero on the overall account;

The second reason is also the source of the T1, T2, T3 tiering I mentioned in the first chapter.

In simple terms, I divided it into three categories:

T1 High Certainty: For me, the comfort zone involves East Asia and some geopolitics where I feel there’s an East-West information gap, verified multiple times before adding;

T2 Relatively Stable: There are some feelings where the implied probability is clearly higher than the actual yes or no pricing;

T3 Pure Speculation: Those with very high odds, but these should not be taken frequently; it’s best to bet against the market to capture short-term returns);

However, it’s also essential to note that T1 comes with an implicit cost, especially for long-term targets; for instance, a static return of 18% from a T1 level bet might settle in 180 days, but the annualized IRR could only be 3-4%, which is worse than just holding the money, and during this time, the principal is locked up, causing you to miss later high IRR opportunities.

So I further split T1 internally into several time slots (this part is purely personal thinking and won't be shared here) generally speaking, short-term T1-A can be more aggressive, while long-term T1-C should be restrained; having too many low IRR long-term targets constitutes an implicit loss of capital efficiency.

T2 has edge but should allow room for “judgment error,” with a single bet limit of 8-10%, meaning even if this bet loses completely, the total loss in the account is controlled within 10%, not affecting continued participation in subsequent opportunities.

T3 has very appealing odds but should use the smallest position for observation, not expecting to earn big money from it, but rather to bet against the market, capturing short-term returns — enabling oneself to continue tracking high-odds events and accumulating a sense of these types of bets.

Overall, the position upper limit is essentially providing room for “I might be wrong” while keeping the costs bearable.

There is a particularly important but counterintuitive point that high certainty does not equal high position. Even if you think an event has a 95% chance of occurring, as long as there’s still a 5% probability of going to zero, the position must be limited.

To give a more extreme example, suppose you continuously make 10 bets you believe have a 95% win rate; it sounds like each one is stable, but as long as they are independent of each other, the probability of at least one being wrong is approximately 1 - 0.95^10 ≈ 40%.

The more you do, the more you will encounter that wrong bet.

This is just for independent events; in reality, many PM markets are not independent; they often have correlations, for example, “Will the US-Iran talks reach an agreement?”, “Will the Strait of Hormuz reopen?”, “Will the Middle East situation escalate within the month?” These three bets may seem like three independent markets, but the underlying variable is almost the same — the directional geopolitical policy of the Middle East; once the wrong direction is judged, all three will bleed simultaneously.

This has also been the greatest help for me, not in increasing the win rate, but in limiting my major mistakes. In plain terms, the core value of this panel is not profit statistics, but risk control.

3. After running this round, my true view of Polymarket

After more than half a month of in-depth testing, my biggest realization is that there are opportunities on Polymarket, but it is definitely not the kind of arbitrage market that many people imagine.

Previously, when we played on-chain arbitrage, the rules were mostly clear, and price discrepancies could be locked in, but Polymarket is different; it really tests your logical understanding of different directional shifts of a bet (this point seems hard to express precisely with words).

For instance, in East Asia-related political and economic dynamics, Chinese users may indeed possess some information gap advantages, which is worth exploring, but that does not mean you will definitely win. Polymarket ultimately does not settle based on "your understanding of reality," but according to market rules and specified data sources (issues of UMA manipulation are also frequent).

Moreover, just because you think something is certain in the Chinese context, it does not mean the definitions within the English rules are the same, especially in the settings of each bet, there often are some textual traps.

So based on my practical experience, PM does not offer that many arbitrage opportunities; it mainly relies on information gaps and position diversification; even high certainty occurrences may encounter black swans.

If you encounter one, it's the complete loss of capital.

As a friend said, “In investment, even if there’s only a 1% chance of going to zero, one should not harbor any luck.”

Because such a mathematical expectation, in the long run, is negative.

So my current understanding of PM is more conservative:

First, do not treat it as a stable profit tool; even for high-certainty investments, especially after a few consecutive wins, do not think you’ve found a cash machine; the most terrifying aspect of a binary market is that after you win consecutively, it will lead you to mistakenly believe you can judge everything, and then you’ll take a big position on the last bet, directly returning the previous profits;

Second, don't equate high win rates with good trades; a 90% win rate event, if the market price is already 0.95, may actually be a negative expected return; conversely, a 40% win rate event, if the market only gives 0.20, might have a positive expected return;

Third, do not underestimate tail risks, this point is particularly important; many people see 10% or 20% returns and think it’s stable, but as long as that trade goes wrong is zero, then it’s not low-risk return in the traditional sense (from this perspective, I even feel that there’s no such thing as low-risk opportunities on PM; every one is high risk);

Fourth, do not engage in false diversification, buying multiple different stakes does not necessarily mean you are diversified; for example, the previously mentioned bets on "Will the US-Iran talks reach an agreement?", "Will the Strait of Hormuz reopen?", "Will the Middle East situation escalate within the month?", these three bets seem to be three independent markets, but the underlying variables are nearly the same;

So now I prefer to view PM as a judgment training ground.

It perfectly aligns with my daily preference for brushing up on political, economic, technological, and financial news, turning those judgments that usually only linger at the "I think" level into something that can be positively reinforced.

These abilities are equally useful beyond PM.

By the way, besides this PM betting panel, I also created a private market valuation dynamic monitoring panel using Codex, primarily tracking the valuation changes of unicorn companies that are not yet listed — Anthropic, OpenAI, Stripe, Kraken, etc., in the private market and the relationship between those changes and corresponding bets on PM.

Polymarket is essentially a prediction market; sometimes signals in the private market are already changing, but PM prices have not yet moved; at other times, PM prices shift first, while actual data hasn’t caught up, the misalignment between the two is worth continuous observation.

Of course, this is not risk-free arbitrage; private market valuations are not entirely transparent, and there may be differences between different data sources, but as an observation framework, it is quite interesting, and I will find an opportunity to write a separate article about it later.

Tyler's Summary

What I wanted to say from the beginning is never "I earned 30% with the panel, and you can too."

I think it is more useful to create a tool that helps you turn feelings into frameworks and frameworks into discipline; often, many people making money does not indicate they found some secret method, but rather that their judgment was simply correct this round.

This distinction is very important.

I also suggest everyone start trying Vibe Coding; it doesn’t have to be with Claude Code, Codex, or even Kimi’s recently launched Kimi Work can also be experienced; if anyone encounters any inconveniences when subscribing overseas, I can share some smooth methods I use later.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。