Introduction

After the start of the 2026 World Cup, prediction markets suddenly became one of the most intensely discussed topics in the crypto industry. The football matches themselves are not new, nor are fans predicting champions, dark horses, scores, and advancement paths. The real change lies in the fact that these judgments, which used to stay on social media, forums, traditional betting, and sports odds, are being transformed into tradable, observable, and real-time fluctuating market prices by platforms such as Polymarket, Kalshi, and predict.fun.

If the 2024 U.S. election allowed prediction markets to prove they could serve as a real-time thermometer for political expectations, then the 2026 World Cup presents prediction markets for the first time in a global sports scenario, facing scrutiny from mainstream users, compliant platforms, exchange entrances, wallet gateways, institutional traders, and regulators. Prediction markets are evolving from trading tools concentrated around hot events into a pricing layer for the probabilities of real-world events, and the core of future industry competition will shift from the number of markets to user entry points, liquidity networks, and regulatory capabilities.

1. The World Cup Ignites Prediction Markets: Why Sports Become the Best Mainstream Entry

Prediction markets are not a new concept. Their basic mechanism is to break down a future event into tradable contracts, allowing users to buy “Yes” or “No” shares; the contract prices usually fluctuate between $0 and $1, which can be understood as the market's pricing of the probability of a specific outcome occurring. In recent years, prediction markets have made significant inroads in U.S. elections, macro data, geopolitics, regulatory decisions, crypto events, and corporate news. Many times, the price changes on Polymarket reflected shifts in market expectations even earlier than traditional media reports, polls, and expert commentary.

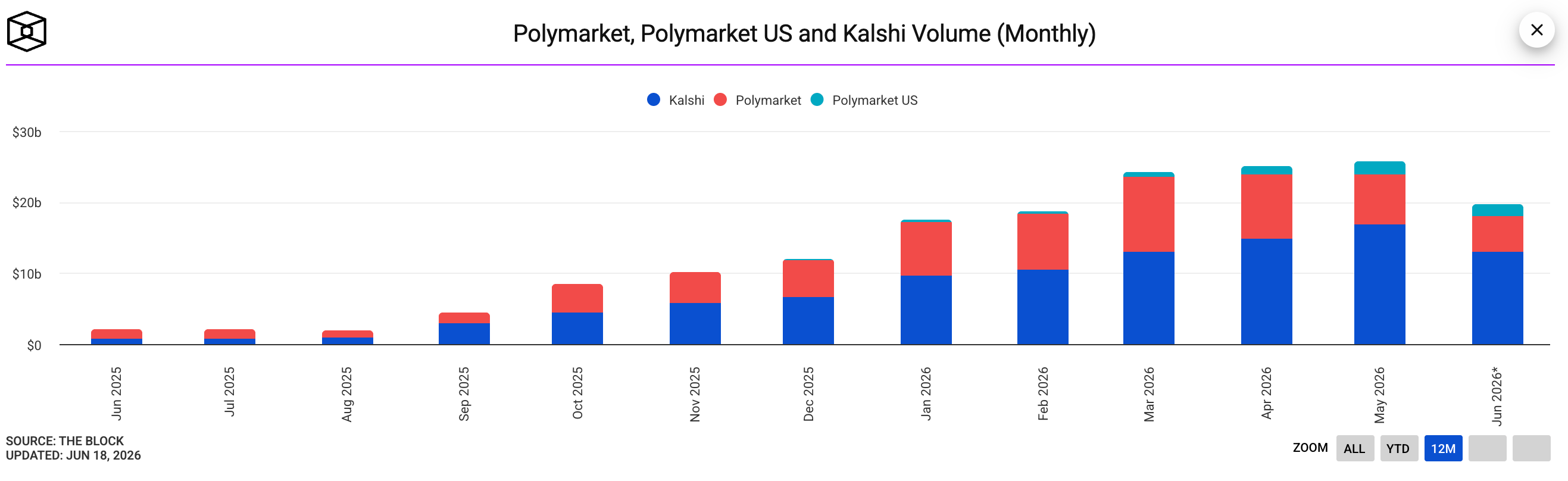

As of June 18, 2026, the monthly trading volume of the two major prediction market platforms, Polymarket and Kalshi, reached nearly $20 billion, while a year ago, the combined monthly trading volume was only about $2 billion. In just one year, the industry's overall trading scale grew nearly tenfold.

However, for a long time, prediction markets have faced obvious bottlenecks:

First, many events have a high cognitive threshold, such as Federal Reserve policy paths, court rulings, geopolitical conflicts, and corporate regulatory matters, and are not suitable for general user participation.

Second, on-chain prediction markets require wallets, USDC, on-chain authorizations, gas, cross-chain understanding, and order book comprehension, making the participation cost for ordinary users high.

Third, events such as politics, wars, and regulations may have high trading values but also more easily trigger legal and ethical controversies.

The World Cup happens to solve part of these problems:

First, sports events have global consensus. Even if they are not deep fans, users can understand who wins and loses, who can advance from the group stage, who can reach the quarterfinals, and who might win the championship. Compared to macroeconomic data or political contracts, the cognitive cost of the World Cup market is lower.

Second, sports events have high-frequency information flows. Pre-match lineups, injuries, yellow and red cards, goals, substitutions, tactical changes, and standings will all affect market prices in real-time. Prediction markets not only trade the final results but also engage in the continuous adjustment of market consensus as information changes.

Third, sports events have strong social attributes. The World Cup inherently features group chats, sharing, debates, team loyalties, and emotional resonance. Prediction markets transform this social discussion into quantifiable, tradable, and verifiable probability curves, turning watching the event from pure content consumption into active participation.

Fourth, the settlement of sports events is relatively clear. Compared to political promises, geopolitical events, or vague regulatory statements, football match results, standings, and advancement paths usually have official data sources, leading to fewer settlement disputes. This makes the World Cup an ideal scenario for testing prediction market matching, liquidity, settlement, and user experience.

This can also be seen from the trading structure of prediction markets. Since 2024, markets related to sports, politics, and crypto assets have contributed 91% of Kalshi's volume and 90% of Polymarket's volume; among them, sports markets account for about 80% of Kalshi's total trading volume, and about 39% of Polymarket's total trading volume. During the World Cup, prediction markets appeared not only on the Polymarket platform but also began to enter CEXs, wallets, and ecosystem activities. Gate has integrated Polymarket, and Bitget Wallet has also integrated Polymarket, allowing users to participate directly in real event trading within the wallet. Additionally, Binance Wallet has integrated Predict.fun, a decentralized prediction market application built on BSC. It is clear that prediction markets are gradually evolving from standalone applications into basic functional modules of exchanges, wallets, and information platforms.

This indicates that the focus of the next stage of competition in prediction markets is shifting from “is there a market” to “who can become the entry point”. Polymarket provides underlying liquidity and event markets, CEXs offer account systems, USDT balances, trading interfaces, and user reach; wallets may expand the entry point of prediction markets from asset management to real-world event participation. Users do not necessarily have to understand crypto first to engage in prediction markets; they may first be interested in the World Cup and later have their first on-chain application experience through a simple prediction.

2. Growth and Retention: Can Trading Volume Convert into Real Capital Accumulation

The World Cup indeed significantly amplified prediction market data, but studying prediction markets cannot solely focus on trading volume. Especially in order book markets like Polymarket, cumulative trading volume represents the nominal amount of contracts being bought and sold, which does not equal the amount of new capital of the same scale settling in the market, nor does it mean that the market has formed a belief of equal strength regarding a specific outcome.

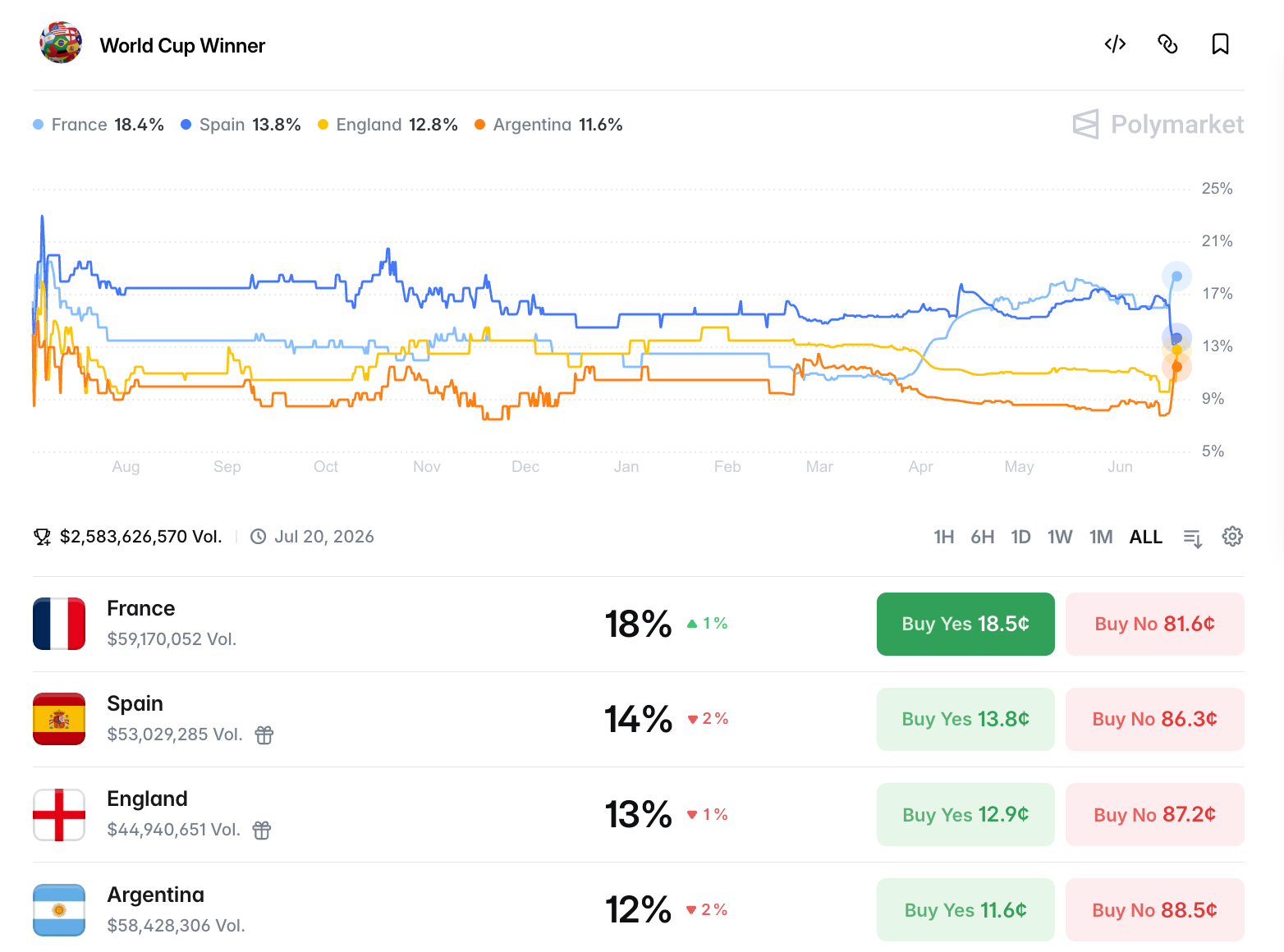

As of June 17, 2026, 19:03 (Beijing time), Polymarket's “World Cup Winner” market showed that the cumulative trading volume for this event was approximately $2.58 billion, with market liquidity around $535 million, and open positions around $46.18 million. A World Cup champion market has already become one of the most important liquidity centers on Polymarket.

Source: https://polymarket.com/event/world-cup-winner

The most critical comparison is that the cumulative trading volume is about 56 times the open positions. This means that a trading volume of $2.58 billion does not represent $2.58 billion in funds being bet on the World Cup champion, but includes market making, turnover, arbitrage, short-term trading, liquidity incentives, and nominal trading formed by the same capital being traded multiple times.

What illustrates the issue even more is the divergence between trading volumes of different teams and their implied probabilities. According to Polymarket's data at the same time, France, Spain, England, and Argentina have the highest market implied probabilities, but the highest trading volumes do not exclusively belong to these popular teams. Teams like South Korea, the United States, Ivory Coast, Australia, and the Democratic Republic of the Congo have much lower championship probabilities than France, Spain, and Argentina, yet their cumulative trading volumes are higher. This does not mean the market believes South Korea or the Democratic Republic of the Congo are more likely to win, but illustrates that prediction market trading volume reflects the intensity of contract turnover, not simply the strength of probability belief.

The reasons may include several aspects.

First, low-priced contracts are more likely to produce high-frequency turnover. Contracts with extremely low probabilities approach $0, allowing users to buy large numbers of shares with relatively small funds, and even slight price fluctuations may lead to high percentage changes, thereby attracting short-term traders.

Second, liquidity incentives may change trading behavior. Polymarket introduced liquidity incentives during the World Cup to enhance market depth. The incentives themselves help improve spreads and order book thickness but may also attract market makers to frequently quote, transact, and adjust positions around the incentive rules, thereby driving up nominal trading volume.

Third, popular team contracts may not necessarily have the highest turnover. The probabilities of popular teams are relatively stable, and price ranges are more concentrated, so they may not generate as much extreme volatility and high-frequency arbitrage space as underdog teams.

Fourth, multiple binary contracts amplify nominal transactions. The World Cup champion market is not a singular multi-choice pool but consists of multiple teams corresponding to different Yes/No contracts. Users can trade Yes or No on multiple teams simultaneously, and market makers can also perform combined quotations and risk hedging between different teams, further amplifying total trading volume.

Therefore, judging the quality of growth in prediction markets cannot simply be based on nominal trading volume; it is also essential to observe open positions, active addresses, net deposits, market depth, spreads, liquidity retention, post-event user retention, and the migration situation of different categories. This is also the first hurdle that prediction markets must face as they transition from hot products to financial infrastructure: if the market can only generate attractive nominal trading volume without settling real users, real capital, and sustainable liquidity, then the World Cup is more like a peak of traffic rather than a long-term turning point.

3. The Competition for Entry in Prediction Markets: Liquidity, Compliance, and Ecological Competition

During the World Cup, the competition in prediction markets is no longer just a growth story of Polymarket alone, but rather a direct competition among different growth paths. As prediction markets gradually evolve from crypto-native products to mainstream financial products, the industry is forming four representative expansion routes: liquidity-driven represented by Polymarket, compliance-driven represented by Kalshi, ecology-driven represented by predict.fun, and channel-driven represented by exchanges and wallets.

From a longer-term perspective, the focus of competition in prediction markets is also changing. The early competition centered on the number of markets and the range of events covered; as products mature, the real determinants of industry structure will become user entry points, liquidity network effects, and distribution capabilities. The performance of various platforms during the World Cup essentially serves to validate the growth efficiency and long-term competitiveness of different paths.

3.1 Liquidity-Driven: Polymarket Builds Event Trading Network Effects

Polymarket's core advantage is not merely the number of event markets it has but the liquidity network effects gradually accumulated over the past few years. Prediction markets, like exchanges, have deeper liquidity leading to higher price discovery efficiency; users are more willing to participate in trading; while more users and trading volumes will attract market makers to provide deeper order books and lower trading costs, further reinforcing the platform's advantage. This positive feedback mechanism makes liquidity one of the most important competitive barriers for prediction markets.

During the World Cup, Polymarket's leading position becomes further strengthened. Since the start of the World Cup, the cumulative trading volume related to Polymarket events has exceeded $1.7 billion, with over $63 million in transactions completed in the past 24 hours. Simultaneously, the platform continues to expand its football-related resources during the event, establishing partnerships with sports ecosystems such as OneFootball and Liga MX, further enhancing content and user reach capabilities.

However, what is even more noteworthy is that Polymarket's value is extending from a trading platform to an information platform. When users want to understand the market expectations of a certain real-world event, Polymarket has gradually become the default query entry point for some crypto users. Its prices not only serve trading actions but are also increasingly cited by media, research institutions, and social platforms, becoming a visual representation of market consensus. From this perspective, Polymarket's competitive advantage is no longer just about "having the lines," but rather in constructing a probability pricing network centered around real-world events.

3.2 Compliance-Driven: Kalshi Opens Up the Traditional Financial Market

If Polymarket represents the development path of crypto-native prediction markets, then Kalshi is exploring a completely different avenue: incorporating prediction markets into traditional financial regulatory frameworks. Kalshi is an event contract platform regulated under the U.S. CFTC framework, with its long-term goal not being to compete for on-chain users, but to standardize event contracts akin to options and futures as financial products. In this model, prediction markets are not viewed as crypto applications but rather as a new type of risk management and price discovery tool within traditional financial markets.

During the World Cup, Kalshi's sports market trading activities grew significantly. Kalshi's daily nominal trading volume for sports reached $1.09 billion, crossing $1 billion for two consecutive days, while Polymarket's daily nominal trading volume was about $350 million during the same period. Although the statistical criteria across different platforms are not entirely consistent, this data still illustrates that compliant platforms are attracting a large number of traditional financial users to participate in event trading.

For the entire industry, Kalshi is significant not for short-term trading volume, but for verifying a critical question: Can prediction markets become regulated financial products? If the answer is positive, then the potential user base for prediction markets will shift from crypto users to a broader spectrum of traditional financial investors, providing new growth opportunities for market size.

3.3 Ecology-Driven: predict.fun Validates the Distribution Capability of Super Ecosystems

In contrast to Polymarket's liquidity advantage and Kalshi's compliance advantage, predict.fun represents an ecology-driven development path. As a native prediction market on the BNB Chain, predict.fun’s growth logic does not rely solely on independent customer acquisition but instead depends more on the traffic entry points and user base provided by the Binance ecosystem. During the World Cup, predict.fun launched the Predict Cup World Cup prediction event, with a total prize pool of $2 million and reached users through entry points like Binance Wallet. After the World Cup started, the daily active users of the platform reached 20,000, and daily trading transactions exceeded 180,000.

Compared to traditional prediction market platforms, predict.fun distinguishes itself by being closer to an ecological application rather than an independent product. Users do not need to actively search for a prediction market platform but instead encounter and participate in prediction activities within an ecosystem where they already hold assets and have completed account system setups.

This model bears certain similarities to the logic of super applications in the mobile internet era. Users do not necessarily enter the ecosystem because of the prediction market itself but rather discover and use prediction market features passively within the ecosystem. For the industry, this indicates that future competition may occur not only at the protocol and product levels but also at the ecological and traffic layers. From a long-term perspective, ecological distribution capability may become one of the important ways for prediction markets to acquire new users.

3.4 Channel-Driven: CEXs and Wallets are Reshaping User Entry Points

In addition to independent prediction market platforms, exchanges and wallets are also becoming important forces for industry expansion. Gate has integrated Polymarket, Bitget Wallet has incorporated prediction market services, and several wallets are initiating prediction activities around the World Cup, all reflecting a common trend: prediction markets are being embedded into existing crypto product systems.

For instance, Hotcoin has launched a prediction market product, allowing users to make prediction trades on the price trends of crypto assets, football events, and more, along with a World Cup special event. Compared to traditional on-chain prediction markets, its product design emphasizes lowering participation barriers: users do not need to create independent wallets, manage on-chain assets, or pay gas fees but can participate in trading directly using USDT in their platform accounts.

For most ordinary users, the biggest obstacle to participating in prediction markets is often not the prediction itself but the barriers of wallet creation, asset cross-chain, gas payments, and transaction authorization during on-chain interactions. When exchanges and wallets encapsulate these complex processes, users can participate in event trading directly using familiar account balances and operation interfaces, making their experience closer to spot trading or contract trading, rather than traditional on-chain applications.

From the perspective of industry development, CEXs and wallets hold the most mature user channels and asset entry points. As prediction markets gradually become a standardized feature, they may not necessarily exist in the form of independent applications but are more likely to be widely embedded into exchange and wallet systems like swap, wealth management, staking, or payment functions. This means that the future growth of prediction markets may rely not entirely on a single platform but rather on the continued education and distribution of users by multiple channels.

The four paths can be compared as follows:

Path | Representative Platform | Core Advantage | Main Challenge |

Liquidity-Driven | Polymarket | Network Effects and Market Depth | Compliance and Regulation |

Compliance-Driven | Kalshi | Regulatory Recognition and Institutional Participation | Innovation Speed |

Ecology-Driven | BNB Ecological Traffic Distribution | User Retention | |

Channel-Driven | CEX, Wallet | User Entry and Asset Accumulation | Product Homogeneity |

In summary, from Polymarket and Kalshi to predict.fun, and then to the collective involvement of exchanges and wallets, a clear industry trend is forming: prediction markets are shifting from product competition to entry competition. The World Cup is just an important catalyst in this round of entry competition, but not the end point. What truly deserves attention is which platforms can convert short-term traffic into long-term users after the hype of the World Cup fades and which entry points can become sustained usage habits. For prediction markets, this might be even more important than the trading volume itself.

4. The Financialization Process of Prediction Markets: Opportunities, Risks, and Regulatory Challenges

The World Cup validated the growth potential of prediction markets and accelerated their process of financialization. In recent years, prediction markets have been more regarded as experimental products of the crypto industry, with their user scale, trading depth, and social influence relatively limited. However, with the continuous push of global events like the U.S. election and World Cup, prediction markets are gradually shedding the label of “niche betting tools” and evolving into financial products. In this process, the industry gains new growth space while facing long-standing challenges in traditional financial markets regarding regulation, manipulation, and market structure.

4.1 From Information Tools to Pricing Layers: Prediction Markets are Becoming Pricing Mechanisms for Real Events

The most significant value of prediction markets is not providing trading opportunities but rather providing prices. Traditional financial markets can continuously price stocks, bonds, commodities, exchange rates, and interest rates, but they often lack a unified and real-time pricing mechanism for numerous real-world events. For instance, whether a particular bill will pass, whether a company will complete its IPO, whether a candidate can win an election, or whether a team can ultimately win a championship. In traditional systems, these judgments mainly rely on expert analyses, media surveys, or institutional predictions. Prediction markets, on the other hand, convert dispersed information, opinions, and expectations into continuously changing market prices, making probabilities themselves a tradable asset.

In recent years, Polymarket's performance in U.S. elections, macro policies, tech company events, and sports events has demonstrated this potential. An increasing number of media outlets are beginning to reference prediction market prices as significant indicators of market expectations, a role that is gradually resonating with leading indicators in traditional financial markets, such as interest rate curves, implied volatility of options, or credit spreads. If the market scale continues to expand, prediction markets may not only serve as trading platforms but potentially also become vital pricing discovery layers for real-world events. From this perspective, what prediction markets trade is not the events themselves but the consensus regarding future outcomes.

4.2 Sports Events Validate High-Frequency Demand but Also Strengthen Controversies Regarding Gambling

The rapid growth of trading volume during the World Cup proves the significant value of the sports context for prediction markets. Compared to infrequent events like presidential elections or macro policies, sports events have natural advantages: low cognitive barriers for users, high event frequency, clear outcomes, and strong global attention. Events like the World Cup, Champions League, NBA, NFL, and MLB can continuously provide a large number of tradable events throughout the year, allowing prediction markets to escape their dependency on a few major political events.

For the industry, this suggests that prediction markets now possess the potential to build daily trading scenarios for the first time. However, this advantage comes with contention. As the share of the sports market continues to rise, the boundary between prediction markets and traditional sports betting begins to blur. Whether regarding user behavior or trading experiences, certain sports prediction markets have become highly similar to sports betting products.

This is also one of the core issues currently drawing the attention of regulators. If prediction markets are primarily driven by sports trading, their regulatory attributes may be closer to gambling products; whereas if their core functions are information aggregation and probability pricing, they are more likely to be classified as financial products or event contract markets. Whether the industry can establish clear product boundaries in the future will directly impact the regulatory environment and long-term developmental space of prediction markets.

4.3 Institutional Funds Begin to Enter; Prediction Markets are Forming a New Asset Class

Previously, prediction markets were mainly driven by retail users, whose functions were more about expressing opinions and participating in discussions surrounding hot events. However, as the market scales, an increasing number of professional trading institutions are beginning to view prediction markets as new trading venues.

Recently, several overseas media reports indicated that the commodities hedge fund Moreton Capital has established a dedicated prediction market trading department and plans to introduce external funding to carry out related strategies. Concurrently, some quantitative trading teams are also starting to focus on event-driven trading, cross-platform arbitrage, news trading, and probability pricing models.

The entry of institutions indicates that prediction markets are shifting from being interest-driven to capital-driven markets. From the perspective of asset attributes, prediction markets exhibit distinct differences from traditional financial assets: stocks trade future cash flows of companies; bonds trade future interest rates and credit risks; commodities trade based on supply and demand relationships; prediction markets trade future event outcomes. This unique attribute gives them the potential to become an independent asset class. If a mature market-making system, derivatives system, and risk management tools can be established in the future, prediction markets could evolve into a new track akin to the options market or event-driven strategy market.

4.4 “Collective Wisdom” Does Not Always Come from the Crowd: Markets Are Moving Towards Professionalization

Prediction markets have long been seen as a representation of “collective wisdom.” Their core logic is that the market price can more accurately reflect future outcomes than expert predictions, as many participants independently express their views. However, as institutions and professional traders enter the market structure, changes are occurring.

Research related to Polymarket indicates that, during the observation period, whale accounts, high-frequency traders, and highly active professional traders contributed over 80% of the nominal trading volume, while ordinary users occupy a relatively limited share of trades. This phenomenon suggests that prediction market prices are increasingly likely to be dominated by a few professional participants rather than widely expressed public consensus.

From the market efficiency perspective, this is not necessarily a bad thing. Professional market makers can enhance liquidity, quantitative institutions can accelerate information reflection, and high-frequency traders can reduce bid-ask spreads. However, there is also the possibility of information advantage concentration, liquidity monopolies, and pricing power being centralized among a few institutions. Whether prediction markets ultimately evolve into “crowd wisdom markets” or “professional pricing markets” remains to be seen.

4.5 Regulatory and Manipulation Risks: Challenges Prediction Markets Must Cross in Financialization

As prediction market scales expand, the issues they face are increasingly aligned with those in traditional financial markets. The most critical challenges arise from insider information and market manipulation.

Compared to the stock market, prediction markets often revolve around single event outcomes, making prices extremely sensitive to key information. For example, corporate IPO plans, policy release timings, internal sports event news, and regulatory approval results can create significant informational advantages. When a few participants possess critical facts in advance, prediction markets may experience significant information asymmetry issues. At the same time, due to limited liquidity in some markets, large funds may also affect price trends by concentrating trades, thereby impacting the credibility of market signals.

For regulatory bodies, prediction markets are neither comparable to securities nor to gambling; their legal positioning is still evolving. The ongoing scrutiny by the U.S. CFTC over sports prediction markets, discussions in Europe about the compliance of event contracts, and different attitudes toward political prediction markets across countries suggest that the industry is still in the formative stages of establishing regulatory frameworks. For prediction markets, the biggest future challenge may not be technical but rather how to balance openness, market efficiency, and regulatory requirements.

5. Outlook and Conclusion: Can Prediction Markets Become a Pricing Infrastructure for the Real World?

The World Cup will eventually end, and the traffic peak will gradually decline. However, for prediction markets, the truly important question is not how much trading volume was created during the World Cup, but rather what remains after the World Cup.

In the past year, global hotspots such as the U.S. election, crypto ETFs, macro policy events, and the World Cup have collectively pushed prediction markets into the mainstream view. However, historical experience shows that while hotspots can drive traffic, they do not necessarily accumulate long-term value. Whether prediction markets can emerge from cyclical hotspots ultimately depends on whether they can establish stable user demand, sustainable liquidity, and widely recognized price discovery abilities. From the current developmental stage, the industry still needs to answer five key questions in the future.

5.1 Can User Demand Expand from Sports to Broader Real-World Events?

The World Cup proves that the sports context has strong user acquisition capability, but sports do not represent all of the value of prediction markets. If users are only active during the World Cup, European Championship, or U.S. election, then prediction markets essentially remain event-driven products, highly reliant on hotspot cycles. A truly mature prediction market should enable users to transition from sporting events to a broader range of real-world topics such as macroeconomics, financial markets, technological innovations, regulatory policies, corporate events, and social issues.

In the long run, the core competitiveness of prediction markets lies not in how many hot events they cover but whether they can become a daily tool for users to understand future uncertainties. When users begin to habitually judge the future through market prices rather than expert opinions, prediction markets will truly hold long-term value.

5.2 Can Trading Volume Accumulate into Sustainable Liquidity?

Most of the growth during the World Cup is reflected in trading volume. However, trading volume itself does not fully capture market quality. In the development of financial markets, indicators that possess long-term value commonly include open positions, order book depth, bid-ask spreads, capital retention rates, and the extent of market maker participation. These metrics jointly determine the liquidity quality and price discovery efficiency of the market.

For prediction markets, the future key lies not in creating higher nominal trading volumes but in establishing deeper, more stable, and sustained liquidity pools. Only when liquidity can continually exist beyond individual event cycles can prediction markets shed the hotspot-driven model and transition into the developmental phases of mature financial markets.

5.3 Can Prices Become Trusted Market Consensus?

The greatest value of prediction markets lies in their prices. Whether pertaining to the U.S. election, World Cup champion, macro policies, or corporate events, market prices continuously relay probability judgments about future outcomes to the external world.

However, the more widely prices are referenced, the higher the importance of their accuracy and credibility. Market prices do not inherently represent the truth; they encompass both information advantages and liquidity premiums, emotional fluctuations, funding costs, and trading behavior biases. Therefore, the future industry needs to continuously validate a core question: Are prediction market prices more accurate than traditional surveys, expert forecasts, and media views?

If prediction markets can prove their stability and verifiability in predictive capabilities through long-term practice, their role will elevate from a trading tool to an information infrastructure with societal significance. Conversely, if prices are persistently influenced by manipulation, emotions, or liquidity shortages, their financial value will be constrained.

5.4 Can a Market Integrity System Support Mainstream Development?

The development of any financial market is built on trust. For prediction markets, one of the greatest challenges ahead is market governance.

As institutional funds continue to flow in, platforms need to establish more comprehensive market monitoring, insider trading identification, anomalous account review, conflict of interest disclosure, settlement dispute resolution, and user protection mechanisms. Especially in sensitive areas such as politics, regulation, corporate events, and sports events, market integrity will directly determine whether prediction markets can gain recognition from regulators, institutional investors, and mainstream society. Historically, all successful financial markets have ultimately undergone a transition from unregulated growth to rule-based governance. Prediction markets cannot bypass this stage.

5.5 Will Prediction Markets Become a New Financial Infrastructure?

From a longer-term perspective, the most significant imaginative space for prediction markets may not lie in trading itself. Prediction markets attempt to solve the problem of pricing future events. If sufficient liquidity can be established, price validity continuously verified, and regulatory recognition achieved, prediction markets could potentially become the pricing layers for real-world uncertainties. At that point, prediction markets will provide not just trading opportunities but also a new method of information organization and decision-making reference system.

From enterprise strategic formulation to investment decisions, from macro analysis to public policy discussions, the market's probability judgments about the future may become important references. This is also fundamentally what distinguishes prediction markets from traditional betting products.

Conclusion

The explosive growth during the World Cup has allowed prediction markets to first enter the global view as a mainstream product. On the surface, people are trading the champions' ownership, game results, and advancement probabilities; but at a deeper level, the market is truly trading judgments about the future.

From Polymarket's liquidity network to Kalshi's compliance exploration; from predict.fun's ecological expansion to exchanges like Hotcoin integrating prediction markets into their existing product systems, the industry is experiencing an evolution from crypto-native experimental products to mainstream financial tools. The World Cup may simply be an important node in this process.

In the long term, the value of prediction markets lies not only in providing trading opportunities but also in offering continuous pricing capabilities for real-world uncertainties. If search engines address information retrieval issues and financial markets address asset pricing issues, then prediction markets aim to solve the probability pricing problem of future events.

About Us

Hotcoin Research, as the core research institution of Hotcoin Exchange, is dedicated to transforming professional analysis into your tactical weapon. We analyze market trends through “Weekly Insights” and “In-Depth Research Reports”; using our exclusive column “Hotcoin Selection” (AI + Expert Dual Screening), we identify potential assets and reduce trial-and-error costs. Every week, our researchers also interact directly with you through live broadcasts, interpreting hotspots and predicting trends. We believe that warm companionship and professional guidance can help more investors navigate through cycles and seize Web3 value opportunities.

Risk Warning

The cryptocurrency market is highly volatile, and investment itself carries risks. We strongly advise investors to invest based on a complete understanding of these risks and under a strict risk management framework to ensure fund safety.

Website: https://www.hotcoin.com/zh_CN/learn/index/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。