Author: Billy Gao

Translation: Jiahua, ChainCatcher

This is the most powerful cryptographic system in history, and it can't even keep a secret.

The most ironic aspect of the encryption industry is: we have built the most powerful cryptographic system in history, stuffed with mathematical formulas almost more than anything else, but the one thing it fails to do is protect the privacy of your funds. Every position you hold, every payment you make, every dollar you transfer is by default broadcast to the entire world.

We seem to have accepted this norm as a given.

But this is precisely the biggest reason why the trillions of dollars in funding that should be on-chain have yet to enter the market. So let’s return to the fundamentals: how did we get here, where are the flaws, and what is the one solution that is finally becoming feasible now.

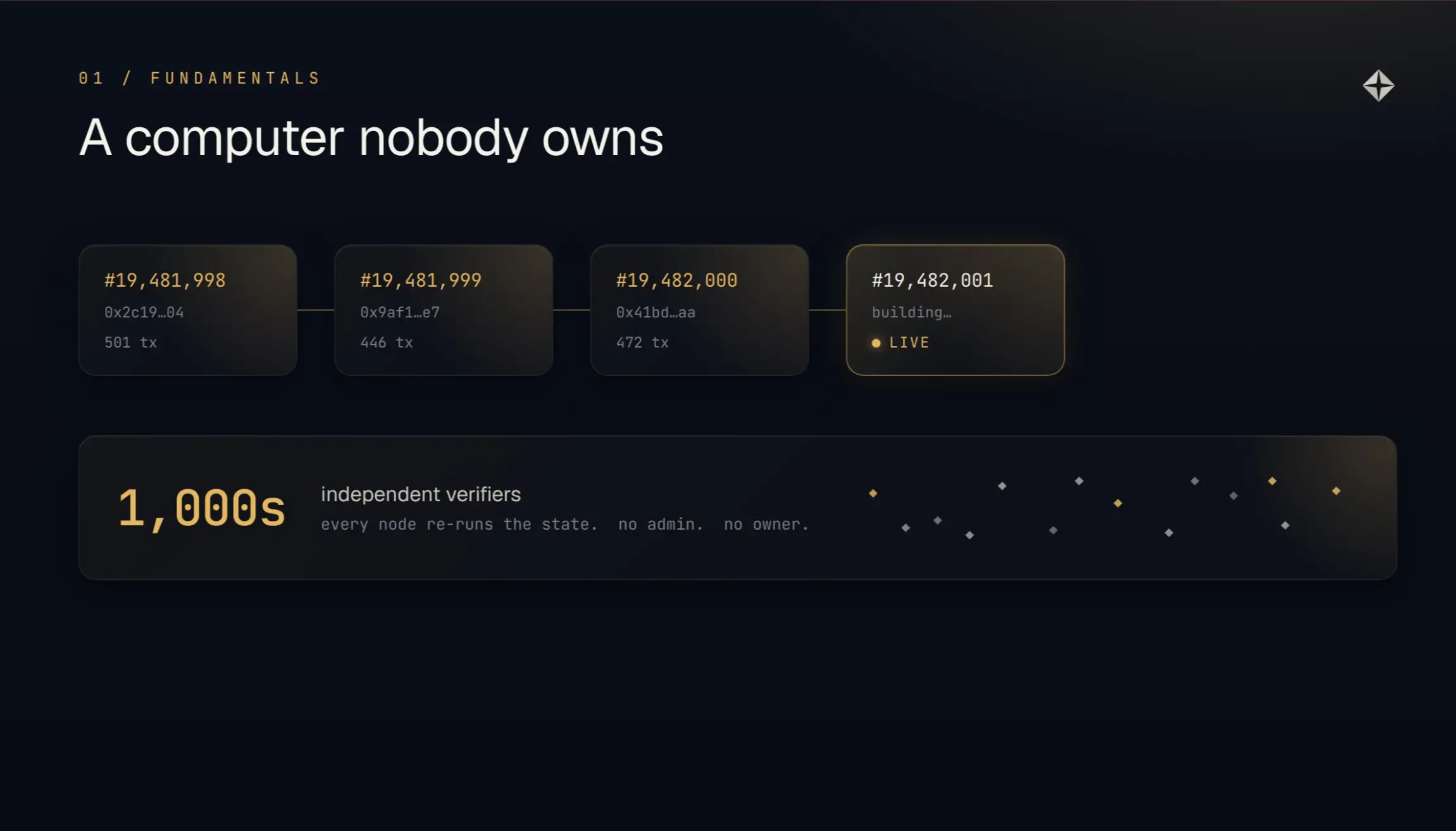

Blockchain is a slow, expensive computer owned by no one

If we strip away the narrative layers accumulated over the past fifteen years, blockchain is actually just a shared computer, with performance that is even worse than the laptop you are using to read this article. That is its entire essence.

Let’s go back to the basic principles of 2012, principles that have fallen out of discussion simply because they sound too simple. Blockchain is essentially a list of blocks linked by hashes. Each block contains a payload: transactions, status changes, and so on.

Each block cryptographically points to the previous one, so no one can tamper with history unnoticed. Anyone can run a verification program to check whether the entire system is valid. Although consensus mechanisms have been shifting—from proof of work and proof of stake to new mechanisms in the future—the core premise has never budged an inch.

It’s slower, more expensive, and bulkier than your laptop. Its only unique feature, and the entire reason for its existence, is that no one can prevent you from using it, and no one can deceive you about the results. There is no administrator, and no privileged party that you must consult.

But this unique feature comes at a high cost. Each node must rerun your calculations and permanently store your data. Therefore, the only reasonable use of this machine is to store those few things that truly need this property and are worth the cost.

The vast majority do not need it, and that’s perfectly normal. In the following discussion, please keep in mind this test: does this need to exist on a computer owned by no one? Because it basically determines everything that follows.

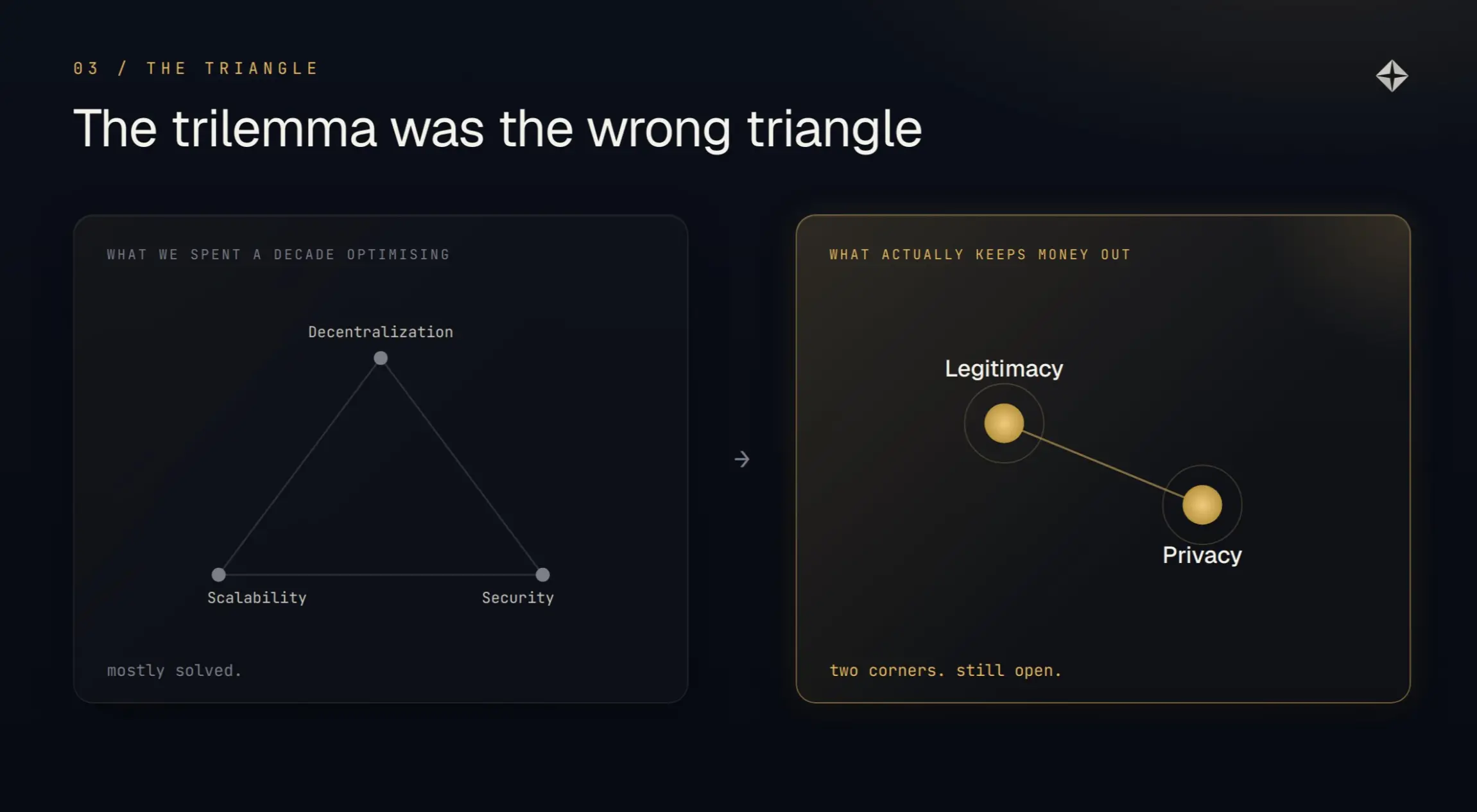

The "trilemma" is a misdrawn triangle

The entire industry has spent a decade grappling with the trade-offs among decentralization, scalability, and security. It has basically won this battle but discovered that the real constraints are not contained within that triangle.

For years, all discussions have revolved around the "trilemma": decentralization, scalability, and security—you can only have two at a time, never all three. The Ethereum era was a long debate centered on this. Block size, sharding, Rollup, Layer 2—these topics have consumed the field for many years.

Then, quietly, we essentially solved it. Now, block space is cheap, throughput is high, and Rollup works well. The scalability issues that defined the decade have essentially become a thing of the past at the application level.

Then, the real core issue surfaced. Once scale is no longer a bottleneck, a disconcerting fact becomes clear: the constraints that truly keep funds outside this machine are not in that triangle at all. We spent a decade optimizing wrong corners of the triangle.

To find the correct angle, one must set aside the question of "how does the machine perform" and ask a more direct and honest question: who does this serve, and who is still unable to use it to this day?

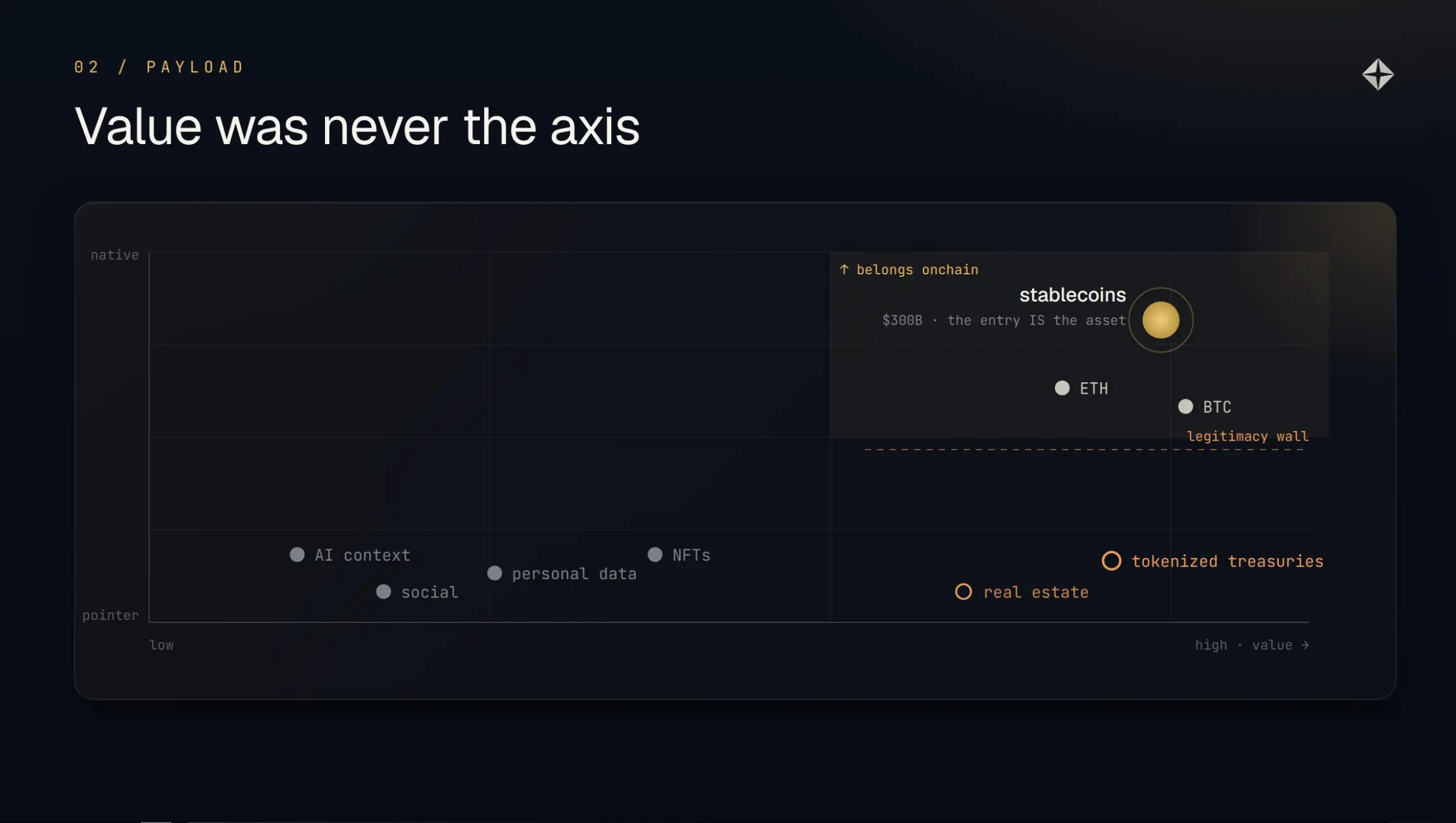

Why only funds can truly flow

Funds are the only thing for which "the record on the ledger itself is the asset." Everything else you put on the chain is merely a pointer to something elsewhere.

Following its characteristics down the line, what is the purpose of blockchain? The answer almost reveals itself.

The first is access. Anyone, from anywhere, can log into this shared computer and change its state. There are no business hours, nor do you need to ask a privileged entity (a bank, broker, or exchange) to help you update the ledger. For funds, this is immensely valuable. Transferring value becomes as straightforward as editing a file.

The second is trust. Why did we initially entrust money to those privileged entities? Because we believed that our money was safe there. The blockchain answers the same question through a different mechanism: not trusting an institution, but trusting numbers; here, "numbers" has two meanings, both mathematical and quantitative. As long as there are enough honest participants incentivized by the economy, each in their different roles, and then using mathematics to verify the entire system. Now, your money is as safe as the network itself, not as safe as a certain entity.

But there is a third point that almost no one mentions. Funds are the only thing for which the ledger record itself is the asset. A dollar on the chain is just a number, and that number is the dollar itself, nothing more.

This is why finance can take root here while almost all other attempts have failed. This type of purely ledger-based asset is precisely what the ledger was built for. The market has confirmed this: stablecoins now have a volume of $300 billion, settling about $33 trillion annually, and this growth is no longer driven by retail speculation.

What should be on-chain and what shouldn't

The crypto industry found its killer application, and then only served a very narrow layer of the market. For the institutions above, the risk is too high, while for average people below, it is utterly meaningless. It only caters to those who are "somewhat well-off," with hardly anyone else.

Since funds are the natural payload, the next question is: which things related to money are truly worthy of the threshold of "needing a computer owned by no one"? The failures at both ends perfectly sandwich the answer in the middle.

At the bottom are those cheap items. You could argue that anything has value and thus counts as "finance." But you are always weighing two things: how much an item itself is worth and how much it costs to run it on the most expensive computer in history.

Social media, personal data, tokenized AI context. These are things that Web2 does exceptionally well, and essentially for free. Moving them onto the chain only raises costs, without reducing anything. The individual value is too low to justify the machine's reasonableness. Most things that people forced onto the chain in the last cycle failed this test, and the same will happen in the future.

At the top are those massive funds that cannot come in. This is the real tragedy. Frankly, when you look at who is actively using cryptocurrencies, that group is incredibly small; let’s call them "the somewhat well-off." They have enough money not to worry about survival every day, but not so much as to manage a large corporate capital. Besides a few crypto-native funds, that's about it.

The capital that should have come (family offices, sovereign funds, large institutions, corporate treasuries) look at this machine and turn away. Not because they don’t understand, but because its operational model does not make sense to them.

Their list of objections is long, and to be fair, most of them are valid: uncertainty in law and regulation, custody risks, endless hacking threats, smart contract risks, MEV, inability to securely self-custody at scale, and counterparty risks at every level. When all these are tallied up alongside the marginal profits, the answer often turns out to be simply not worth it.

In the eyes of many, the crypto space is merely a high-volatility, zero-sum arena, where everyone fights to seize the same batch of dollars. Honestly, they are often not wrong.

So the crypto industry is stuck in a tight band: too bizarre for the capital above, yet too trivial for the applications below.

But take another look at that list of objections. Most of them are operational issues, and operational issues can often be solved with straightforward methods: auditing, insurance, regulated custodians, time. Strip these away, and two unfixable points remain. Because they are not implementation flaws but design attributes.

Public chains are permissionless, which places them in a legal gray area. At the same time, public chains are transparent, which exposes you completely.

Legitimacy and privacy. This is the real triangle that the old version missed, and it only has two corners. Whether we can cross these two corners is the entire outcome of this game, and it ultimately boils down to these two defects.

Defect One: Legitimacy

For the past decade, the most honest answer to the question of "Is this thing legal?" has been "sort of." For anyone managing real money, this is a non-starter answer. And now, for the first time, that answer is beginning to change.

The first defect directly stems from the very advantage it stands on. Anyone can do anything, which is precisely what makes this machine valuable, and also what turns it into a regulatory minefield.

Permissionless is a double-edged sword: that ability to transfer funds without needing anyone's consent also allows others to do things that label the whole industry as a "fraud paradise." For a serious allocator, regardless of how good the underlying technology is, this is a veto.

This defect cannot be fixed with better cryptography; it requires policy to resolve it. In July 2025, the "GENIUS Act" officially became law, providing a real federal framework for stablecoins as core financial payload for the first time. Market structure legislation followed closely behind. It hasn’t become law yet, but the direction is clear, and the environment has become much friendlier for entrepreneurs and allocators than it was two years ago.

The past conundrum that intertwined governance, decentralization, and legal risk has receded to this extent: conducting a compliant on-chain business is now just an ordinary business decision.

Thus, the corner of legitimacy is gradually or more or less closing itself off. The other defect, however, is where the entire industry has truly gone awry over the past decade.

Defect Two: Transparency is a tax

On-chain transparency is not an advantage; it is a tax. Every position you hold is public, and the network charges you for "being seen" through MEV, through front-running.

This is something everyone has become accustomed to, but absolutely should not take for granted. On a public chain, your entire financial life is being broadcast. Every position, every transaction, every transfer can be seen in real-time by anyone holding a block explorer. "This is transparency, it's an advantage," we have heard that too long, long enough that we no longer notice it is actually a leak.

And it is a quantifiable, ongoing tax. The moment your order enters the public mempool, anyone can see it, then engage in reverse trading, front-running, or wait to liquidate you.

This is not just talk. By mid-2025, the cumulative MEV extracted on Ethereum had already exceeded approximately $1.8 billion. This value was directly extracted from ordinary users' transactions, simply because these transactions were visible before settlement.

Look at who is already spending money to avoid it. Seasoned trading desks and funds long ago stopped broadcasting into the public mempool. They are using private relays and order flow auctions to conceal their actions before execution.

Smart money has been gradually buying privacy piece by piece because smart money knows transparency is costing it money. The rest are simply accepting to pay this tax.

For retail, the situation is even worse: an ordinary trader in a trading venue, every time they open a position that the whole world can see, their profits are leaking away.

Transparency is sold as an "even playing field," but the actual effect is quite the opposite.

Now, let’s turn our gaze to the capital we truly want. No family office, sovereign fund, or large institution would place its balance sheet onto a machine that a competitor can read in real-time.

Of course they wouldn’t. Allowing the entire world to watch your treasury operations in real-time makes no sense. They need a slice of privacy within this shared computer.

Honestly, everyone needs it. You would never accept a bank putting your statements online, so there is no reason to accept it here.

This is why payments and serious trading cannot fully be moved on-chain, and why equating privacy with "anonymous trading" is actually a bit laughable.

The biggest irony of the cryptographic world

Encrypted communication has been mainstream for thirty years. Encrypted funds, however, have not. In a system built entirely on cryptography, this should be somewhat embarrassing.

Taking a step back, this absurdity becomes hard to ignore. Blockchain is built with cryptographic primitives. Hashes, signatures, commitments, from start to finish, it’s all cryptography.

Yet, the one thing it hasn’t done is encrypt users' actual activities. We have built an entire cathedral of cryptography, yet the front door—your financial privacy—stands wide open.

We solved this problem for communication decades ago. No one finds encrypted communication strange or suspicious; it is the default setting, and the world continues to run just fine.

To move the same thing to funds, the foundational elements have always been there; these cryptographic primitives have been quietly improving for the past decade.

What has really been lacking is performance: how to make it fast enough, cheap enough, to reach production levels. This is both a math problem and a hardware problem. The hardware has caught up; dedicated acceleration hardware has brought the costs of these proofs down to levels feasible for actual throughput.

The problem has never been "is this feasible," but rather "is it worth paying that cost." Now, for the first time, the answer has become "worth it."

A question worth responding to

"But isn't transparency key? Proof of reserves, no hidden leverage, verifiable solvency." If privacy means hiding everything, this statement holds true. But privacy doesn’t have to be like that.

The strongest argument against on-chain privacy deserves a solid reply. Transparency is burdensome. It’s how you verify whether a stablecoin truly has enough reserves supporting it, how you confirm whether a protocol is solvent, and how you root it out before hidden leverage blows up.

It is also a tool for law enforcement to trace stolen funds and for regulators to combat money laundering. Making everything opaque would strip away half the value of auditability and hand criminals a useful tool.

This is a serious concern, but it quietly builds on a false dichotomy: as though you only have the options of "completely public" or "completely hidden."

Privacy and compliance have never been enemies

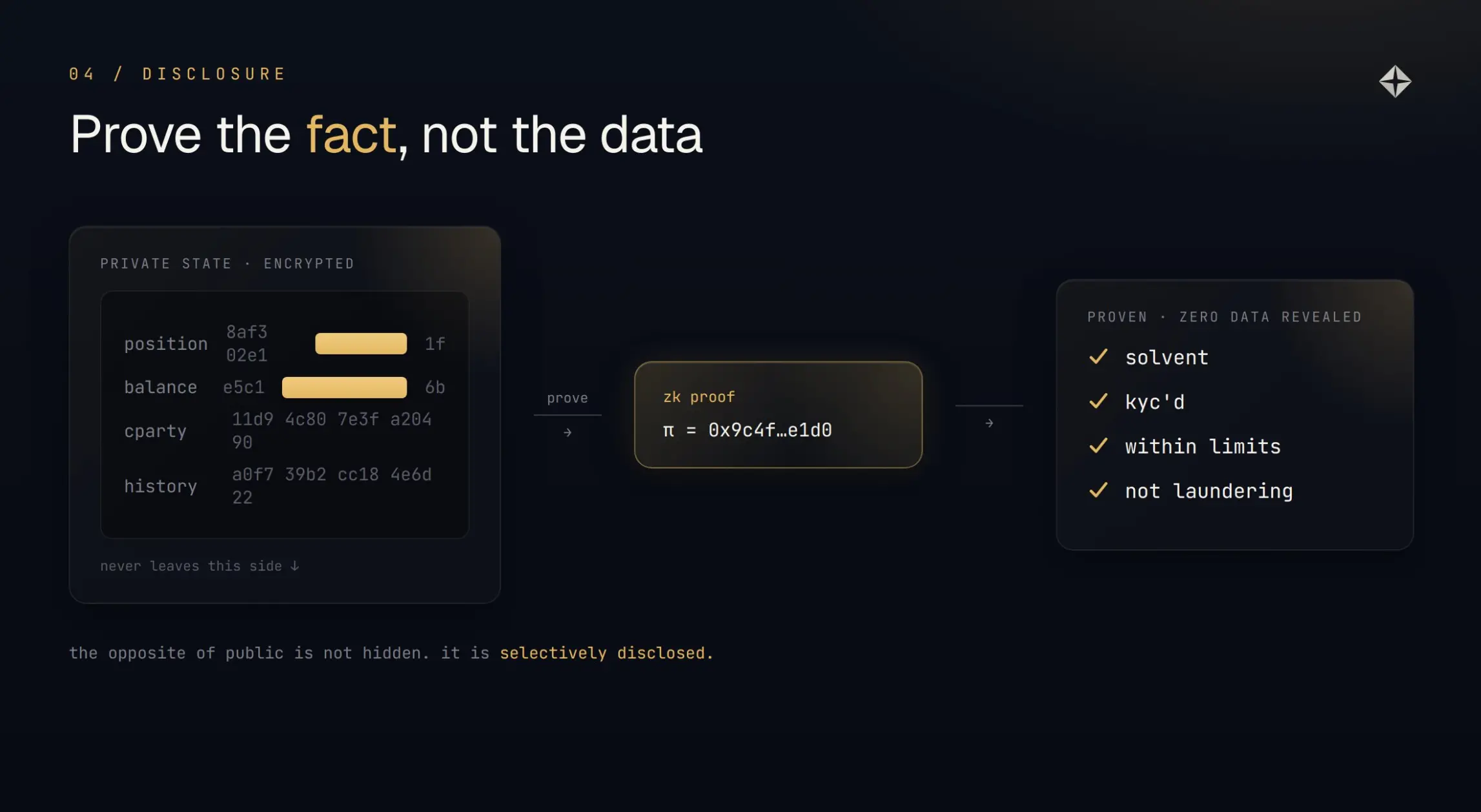

You can prove your solvency without disclosing any position, passing KYC, and staying within limits. Prove that fact rather than laying the data bare.

This is the true argument, let’s be clear: the opposite of openness is not hiding. Modern cryptography allows you to prove a statement is true without having to disclose what makes it true.

You can prove reserves exceed liabilities without disclosing reserve details. Prove that an address has passed KYC without revealing who it is. Prove that a position is within risk limits without showing the position. Prove that a transaction is clean and not laundering without having to disclose the sender's entire history.

This directly resolves the objections. Auditors still get their assurance. Regulators still get their compliance checks. Law enforcement still has legitimate paths for disclosure. What disappears is the real-time broadcasting of everyone’s financial lives, along with every lurking predator, indiscriminately to the world. You retain every benefit that transparency was supposed to bring, and that tax gets dropped.

Privacy and compliance have never been in opposition. They appear to be opposed only because the privacy tools we had in the past were too blunt, such as mixers that hide from everyone (including the police).

Compliance privacy with provable disclosures is precisely the comprehensive solution that has been missing from this entire debate. It enables regulated entities and private individuals to use the same chain, with everyone only revealing what they must, leaving nothing more exposed.

A pure upgrade

Today’s public chains are essentially like a Google Sheet: charging you rent while laying everything about you bare for strangers to see. The version that can keep your secrets is a pure upgrade and is precisely what will ultimately bring the next trillion in funding on-chain.

Let's face what most current crypto products really offer. Strip away the consensus mechanism, and a public chain is just a shared Google Sheet that records everyone's transactions, only it is slower, more expensive, and can be read by every competitor and predator on the planet.

Compared to a true Google Sheet, the only real additional value it offers is decentralized consensus: ensuring no one can secretly change a row. That guarantee is real and valuable. But today, it is the only value added.

Every exchange and DeFi protocol built on mainstream public chains is ultimately leasing this characteristic.

With provable compliance privacy, it is no longer a worse spreadsheet. It becomes something that has no counterpart in the old world: a shared machine that can confirm transactions are true without leaking transaction details.

We have already accepted this model elsewhere: an encrypted email can confirm it was delivered without having to broadcast the content to the entire street. There is no reason for funds to be the only exception.

In almost every dimension that serious capital cares about, "default privacy + provable compliance" is a pure upgrade to the status quo. The same consensus, the same settlement, only without that leak.

The common rebuttal here is that the current crypto crowd seems to not want these things; they are trading here, and the current products obviously suit them well.

Indeed, that is the key. Early adopters will only be those who this current version can already serve. They are not the missing market. The missing market (those institutions, those treasuries, those ordinary people who would never publicize their bank statements) sits on the other side of these two defects.

Shut down these two defects, and you get the bridge that can ultimately cross the chasm, completely flipping a multi-trillion-scale financial system onto the track it has been quietly built for from the very beginning.

This most powerful cryptographic system in history will finally learn how to keep a secret. This will change everything.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。