Author: David Christopher

Translated by: Everyday Blockchain

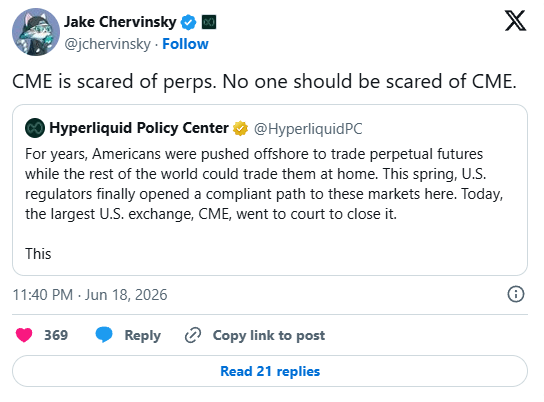

Yesterday, the largest derivatives trading platform in the United StatesCME sued the CFTC due to the recent approval by the Commodity Futures Trading Commission (CFTC) ofcompliant crypto perpetual futures.

CME believes thatKalshi's Bitcoin perpetual product should be classified as a "swap" instead of a "futures swap". Once the classification changes, the product may fall under a set of stricter and more institutionally inclined regulatory rules. The CFTC stated that this move is "not in accordance" and expressed anticipation of dismissing it.

For some time, we have been able to see that large trading platforms likeCME and ICE have increasingly been uneasy about the escalation of perpetual tension. This unease is reflected countless times as they push regulators to scrutinize the aforementioned super-liquid action - whether it’s weightlifting, evading sanctions, or any other issues they can find.

Because regulators have finally opened a pathway for U.S. users to anew compliant derivatives category of trading, and the efficiency advantages of such products are threatening the nearly monopolistic business models of these established institutions.

“CME does not dare touch perpetual contracts. No one should fear CME.” —— Jake Chervinsky, June 18, 2026

The "label" itself is the business model

CME's legal argument essentially embodies a "label".

If Kalshi's Bitcoin perpetual is classified asa futures contract, it can be listed on regulated futures trading platforms,and ordinary American users can access it. If it is classified asa swap, it may fall into a regulatory framework primarily designed for institutional derivatives, with stricter rules -harder to launch and harder to emerge, which would effectively make itmore difficult for most retail investors to access.

It sounds very technical, and somewhat similar to the classification dispute being played out in the prediction market space, but the actual outcome is quite simple:perpetual contracts will be open to retail investors, primarily only traded by institutional participants.

CME flies the flags of "safety" and "risk control" in its lawsuit, but as usual,the true motivation is economic interest. Perpetual contracts constantly threaten the portion of CME's business built around the "threat".

Standard futures contracts will intensify. In order to maintain the same contract positions, traders must switch to the next new contract before the contract expires.Every time the month changes, CME charges significant trading fees and tariffs, and this continuous rolling of trades also supports its additional services such as data market sales.

Butperpetual futures will not go down this path. Traders can hold the same positions indefinitely, only needing toregularly settle funding rates, rather than repeatedly rolling over.

Without rolling over, there is no repeated trading, and this ongoing panic disrupts the rhythm that CME's business has long relied on. The market has already recognized this threat. When regulators opened the door for compliant perpetuals in the U.S., investors began to truly factor in competitive pressures,and the stock prices of CME, Cboe, and ICE all saw declines.

Why perpetuals will continue to expand

Of course, none of this means that perpetual contracts are without risk. They may come with leverage, volatility, and funding rates that will be monitored over the long term. CME founder Terry Duffy has made it very clear:Many retail traders do not fully understand these risks, and the platforms offering perpetual products should clearly communicate these risks.

However,preventing the emergence of compliant perpetuals in the U.S. will not eliminate demand. It will only push U.S. usersback to offshore markets, where they will face less transparency in disclosures, more regulation, and less protection in case of issues.

Therefore, a more reasonable answer is not to block, but toestablish clear regulatory guidelines: set leverage limits, margin standards, and more transparent tariff rules.

The crypto market has become the starting point for this process because the market base here is already mature enough. This makesBitcoin perpetuals the easiest first stop for regulators to tackle. However, considering we have already seen demand inHIP-3, this model will soon extend beyond the crypto space andfurther reach into stocks, indices, and ETFs.

This is precisely why CME's lawsuit is so intriguing. Its demand is for "reclassification" rather than a "complete ban". If you truly believe a product can be completely killed off, you would go ahead and eliminate it; if you cannot do that, you would try to move it elsewhere and cut it off from its original path,slowing down the flow as much as possible.

This is the history that the crypto industry repeats over and over:A better technology emerges, attracting users due to its inherent advantages, and the old stakeholders label it as dangerous, thus regulatory battles unfold. And these debates often truly decide whether the old model can withstand; ultimately, it’s just a matter of how long the old model can hold up.

“Perpetualization” has already begun, and all old institutions can do now is at best drag their feet on this matter.

This article link: https://www.hellobtc.com/kp/du/06/6356.html

Source: https://www.bankless.com/read/why-cme-suing-cftc-perps

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。