Author: Stani Kulechov

Translation: Deep Tide TechFlow

Deep Tide Introduction: Securities financing is one of Wall Street's largest yet least known markets, with the average daily exposure in the U.S. repo market alone reaching $12.6 trillion. Aave V4's centralized radiating architecture perfectly takes on the on-chain migration demands of this trillion-dollar market. From securities-backed lending to repos to securities lending, every link in the chain is using protocols to compress the rent of traditional intermediaries.

Securities financing is one of the largest markets outside of Wall Street that almost no one is paying attention to, and it has already started to go on-chain. Securities-backed lending is a multi-trillion-dollar business. In the U.S. repo market alone, the average daily exposure is approximately $12.6 trillion, with margin lending reaching a record $1.3 trillion and securities-backed loans in wealth management adding over $400 billion on top. The separately calculated securities lending market has about $4.6 trillion in assets being lent, generating a record $15 billion in revenue in 2025. Today, almost none of these activities have touched blockchain, which presents opportunities.

The best way to bring it on-chain is to get the market structure right. Between borrowers and lenders is a plethora of custodians, lending agents, tri-party collateral managers, prime brokers, and clearinghouses. Each layer takes a fee, adds settlement delays, and obscures information. Collateral is trapped in bilateral relationships, with the re-collateralization chain extending out of sight, and when problems arise, it can take days for anyone to see why. Each layer creates work, friction, and cost.

Improving this market structure is precisely what Aave V4 aims to do, and the on-chain tracks have already reached scale. The stablecoin market has surpassed $322 billion, Aave has locked in about $23 billion in liquidity, GHO has been launched as Aave's native dollar, and Aave Horizon's total deposits have exceeded $500 million, powering loans supported by RWA. The cash endpoints, liquidity, and collateral pipelines now exist.

Why V4?

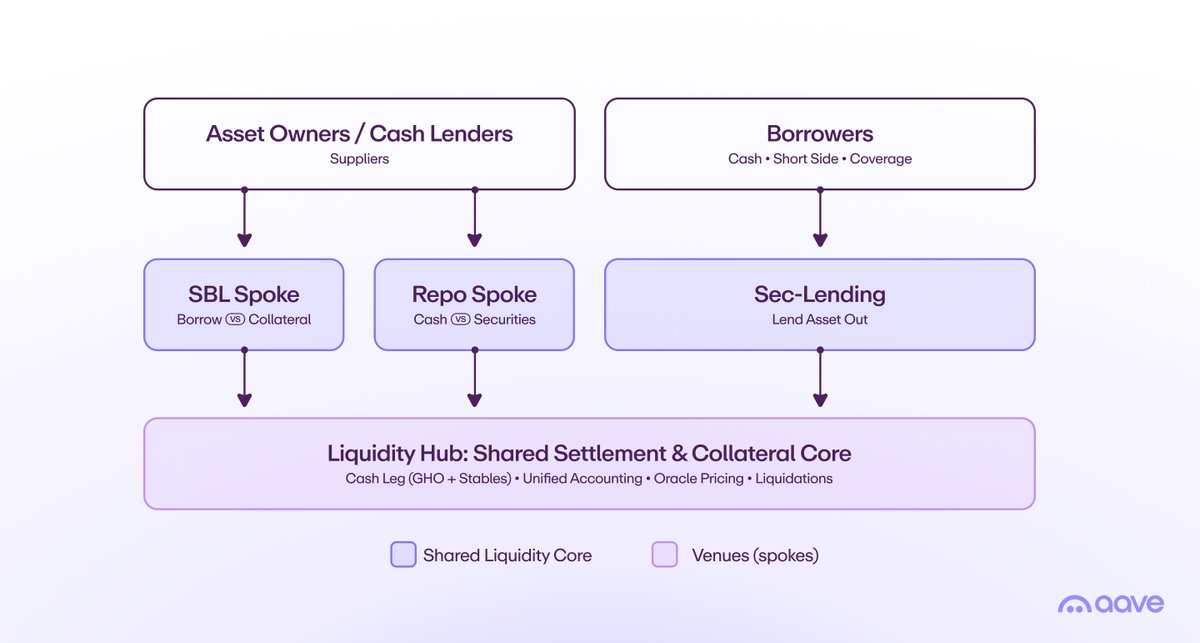

V4 divides the system into a liquidity center and spokes. The center is a deep funding pool, while the spokes are modular venues (i.e., markets) inserted within, each with its own risk parameters, asset ranges, and rules. This single design choice almost perfectly maps the organizational structure desired in the securities financing market: shared liquidity at the bottom and segregated compliant venues at the top.

Three processes run throughout, and together they make up the market.

Securities-Backed Lending

Tokenized securities are deposited as collateral in a spoke, using a conservative, asset-specific discount rate, allowing owners to borrow GHO or stablecoins without needing to sell. Positions remain transparent, discount rates are clear, and liquidation operates automatically rather than through a back office. Owners retain the potential for appreciation and release liquidity, freeing up bank balance sheets. In the U.S. wealth management sector alone, this already represents a $400 billion ledger that remains under-served. As real-world asset tokenization moves towards $16 trillion by 2030, every asset becomes collateral that can be borrowed instantly. Horizon's institutional RWA deposits have already surpassed $500 million, indicating clear demand. For end users, liquidity arrives within minutes, with collateral being tokenized assets rather than through bilateral credit negotiations that take days, with interest rates transparent and set by deep shared pools.

Repos

This is the giant. Repos are short-term collateralized cash lending, mainly backed by government bonds, with the average daily exposure in the U.S. market alone approximately $12.6 trillion. On-chain, repos mean using tokenized securities as collateral to borrow stablecoin cash at a low-risk center, which is precisely what V4 intends to do. Atomic settlement addresses eliminating settlement failures, while terms are programmable and can run 7×24 rather than relying on bank calendars, making approximately $5 trillion of opaque non-central clearing bilateral repos transparent and continuously margin-traded. The market that needs clean settlement and real-time collateral visibility the most is precisely where V4 serves best.

Securities Lending

Tokenized securities themselves become borrowable assets at the center. Borrowing needs from the short sellers and settlement cover parties pay interest rates that directly flow back to the supplying owners of the assets, with the matching, pricing, and collateral management functions of lending agents collapsing into protocols. This is where the fee pool resides, generating $15 billion in revenue in 2025, corresponding to tens of trillions of available supply. Today, lending agents take approximately 20% to 30% of the revenue, siphoning off billions annually before owners see a dime. Routing the same process through protocols compresses this take to nearly zero, and the price difference instead goes to the owners.

A Market Structure Proposal

There are two layout options, both sharing the same spokes. They only differ in how underlying liquidity is organized.

Option A: Single Shared Liquidity Center

A single liquidity center acts as the core for settlement and collateral. It holds the cash side, maintains unified accounting for every position, and prices collateral through oracles, with maximum depth existing in one place and shared by everything above it.

Surrounding it are dedicated spokes, each with its own rulebook but the same underlying liquidity. The SBL spoke accepts tokenized securities as collateral, allowing owners to withdraw stablecoins or GHO based on conservative asset class discount rates. The SBL spoke can be divided into multiple spokes based on risk. The repo spoke handles short-term cash borrowing with high-quality securities collateral, with atomic settlement and continuous margining. The securities lending spoke lists tokenized securities as borrowable assets, with borrowing fees flowing back to their owners.

The advantage of this layout is depth, as a single pool means the deepest liquidity and simplest accounting. The limitation is that risk exists in one place, so isolation must be designed at the spoke level rather than structurally.

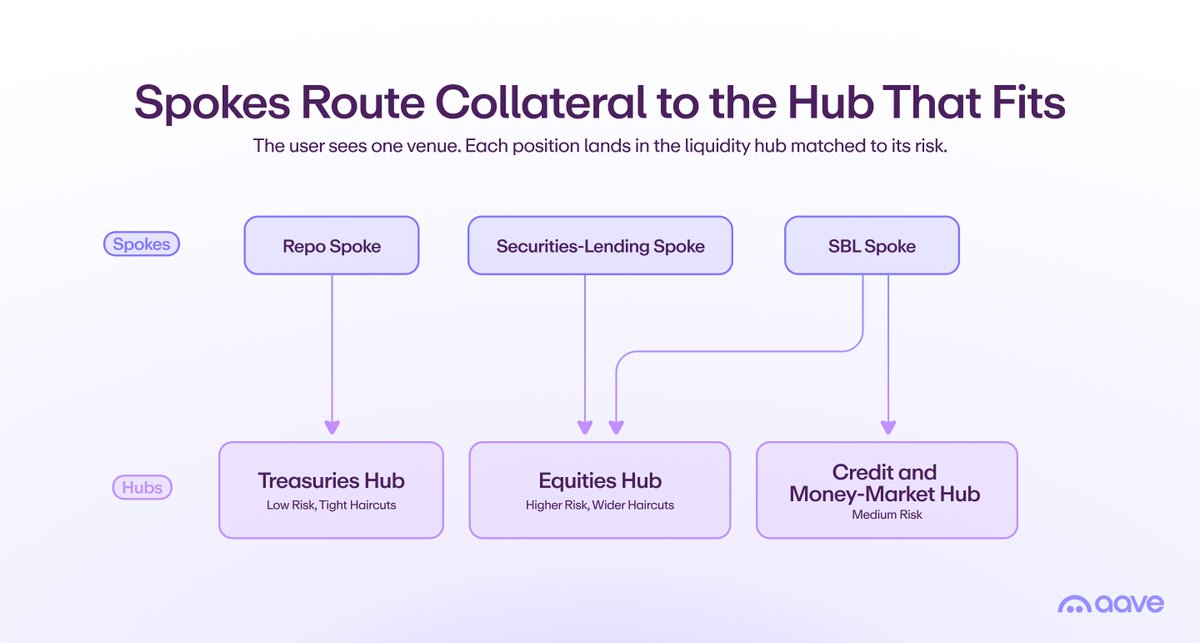

Option B: Multiple Centers by Asset Class and Risk

Another approach is to operate multiple liquidity centers, each limited to a specific asset class and risk tier, allowing spokes to connect across multiple centers. The low-risk government bond center adopts tight discount rates, with most repos naturally falling here, while the medium-risk credit and money market center caters to other needs, and the high-risk equity center uses wider discount rates with stricter clearing thresholds. Each center prices for its own risk and isolates accordingly.

Spokes automatically route across these centers. The repo spoke sends government bond collateral to the government bond center, while the SBL spoke sends a basket of equities to the equity center, with the same user seeing a single venue, while the protocol puts each position into a pool matched by parameters.

This brings three benefits. Risk isolation becomes structural rather than configurable, so equity shocks can be controlled without affecting the government bond pool supporting the repos. Pricing is more accurate, as each center sets rates and discount rates for a specific risk tier rather than mixing multiple. Regulatory separation is easier, as one center can be limited under a single framework while spokes still aggregate experiences from all frameworks. The cost is that each center has shallower depth, but because spokes pull from multiple centers, total liquidity and combinability are preserved. Credit limits between specific centers and spokes can increase liquidity flows while maintaining risk exposure caps.

The actual path is a spectrum rather than a binary choice. Start from constancy to gain depth and simplicity, then as collateral types expand and isolations warrant fragmentation, upgrade to centers divided by class and risk. Regardless of the path, the same spokes can persist.

Roles in Both Models

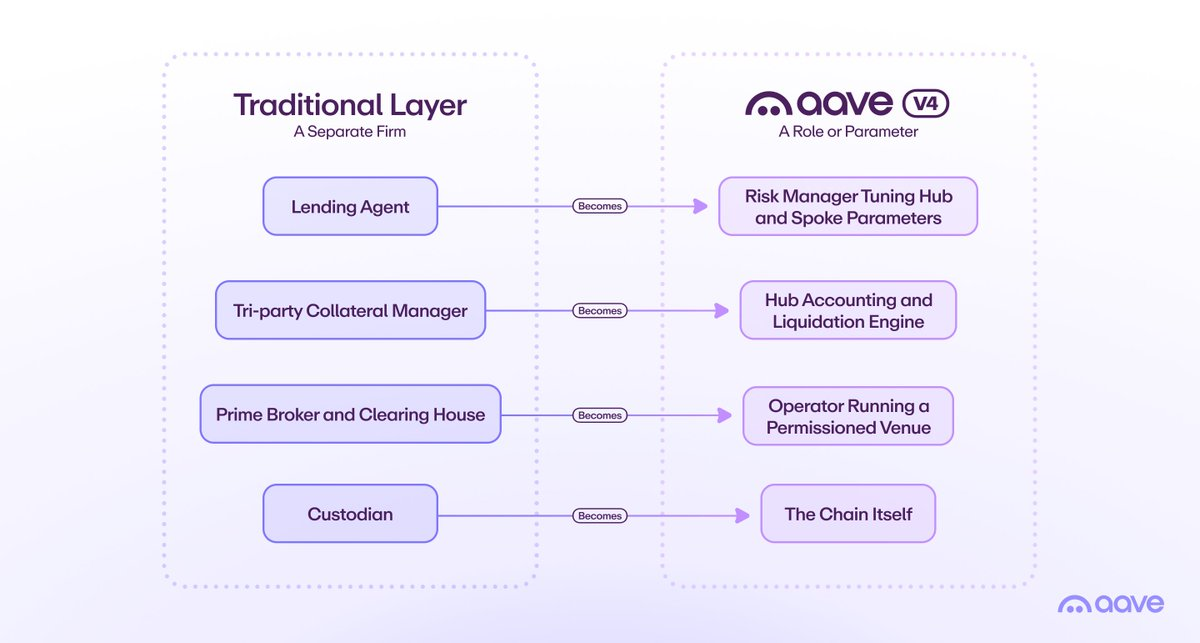

Functions that were once spread across different firms transition into protocol roles, so work remains while rent disappears. Lending agents become risk managers adjusting center and spoke parameters, tri-party collateral managers become the accounting and settlement engine for the center (the protocol itself), and prime brokers and clearinghouses become operators of the venues that run the licenses. Custodians' ledgers become the chain itself.

Structural Changes

Functions that previously existed across different companies shift into protocol roles, so the work remains and the rent disappears. Collateral that used to be trapped in bilateral agreements now gets put to work, as the same asset can provide exposure support for every center it qualifies for, eliminating pre-funded inventory stagnating at each counterparty, along with the loss of floating income. Licensed spokes or jurisdiction-limited centers enforce KYC, jurisdiction, and eligible asset rules at the margins while still drawing from shared liquidity, ensuring that regulators have compliant venues without disrupting the order book relied upon by the rest of the market.

Settlement happens at a completely different pace. The traditional securities market in the U.S. still settles the day after trading, while most of Europe is on a two-day settlement cycle, and the industry has recently only moved to a one-day settlement, a step that has cost participants around $30 billion to implement. V4 offers atomic settlement, available around the clock, with no failures and a marginal cost close to zero, transforming the days-long reconciliation of traditional finance into a single state read on-chain.

What It Unlocks

For asset owners, borrowers, and cash lenders, the gains are tangible. The reachable market size amounts to trillions; the average daily exposure in the U.S. repo market is approximately $12.6 trillion, margin at $1.3 trillion, and securities lending at $4.6 trillion, all based on collateral expected to be tokenized to $16 trillion by 2030.

Gains are retained rather than siphoned off, as the 20% to 30% of securities lending revenue taken by agents today flows back to asset owners. Settlement no longer fails, as atomic 7×24 securities transactions replace T+1 and T+2 cycles and the intraday failures plague bilateral repos. Capital works harder, as pooling liquidity at the center ends idle pre-funded inventories, allowing the same collateral to flow across venues. Risks become visible and manageable, with positions, discount rates, and re-collateralization being transparent in real time, while category centers control shocks at their origins. Acquisition takes just minutes, allowing owners to borrow against tokenized holdings on demand, with interest rates transparent and set by the market rather than negotiated bilaterally over days.

Conclusion

Securities financing has been waiting for a settlement and collateral layer that can operate without stacking intermediaries. Securities-backed lending, repos, and securities lending are three facets of the same balance sheet, where you use holdings to borrow cash, obtain short-term financing, or lend out to earn returns, all moving on a pipeline that siphons off billions and takes days to settle.

V4 carries all three on one framework, whether as a single deep center or as a category and risk-divided center network with spokes routing across, with liquidity, stablecoin cash endpoints, and institutional pipelines already online. The pipeline finally gets an upgrade, directing the value toward the asset owners, relying on the market measured in trillions. This is the market Aave can capture.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。