Author: Claude, Deep Tide TechFlow

Deep Tide Introduction: On June 22, SK Hynix's market value reached 208 trillion won during trading, surpassing Samsung Electronics for the first time in 26 years. Hanwha Investment & Securities raised its target price from 1.63 million won directly to 4.3 million won, the highest price among South Korean brokerages, with the core logic being that long-term supply agreements (LTA) and HBM demand have fundamentally changed the profit volatility of memory chips. The stock has seen a cumulative increase of over 340% this year, briefly exceeding 3 million won in pre-market trading, but fell over 5% in official trading.

On June 22, SK Hynix's stock price rose to a historic high of 2.95 million won, with a market value reaching 208.1 trillion won, surpassing Samsung Electronics’ 207.3 trillion won. This marks the first time Samsung has lost its position as the highest market value in the South Korean stock market since November 2000.

According to The Korea Herald, as of 3:15 PM that afternoon, SK Hynix closed at 2.91 million won, up 5.32%, while Samsung Electronics dipped 0.28% to 353,000 won. SK Hynix has a cumulative increase of 341.9% this year, compared to a 197.7% increase for Samsung Electronics during the same period. Both companies are in the semiconductor sector, but the market is voting with its feet: in the AI era, companies directly benefiting from infrastructure development are receiving a higher valuation premium than integrated giants.

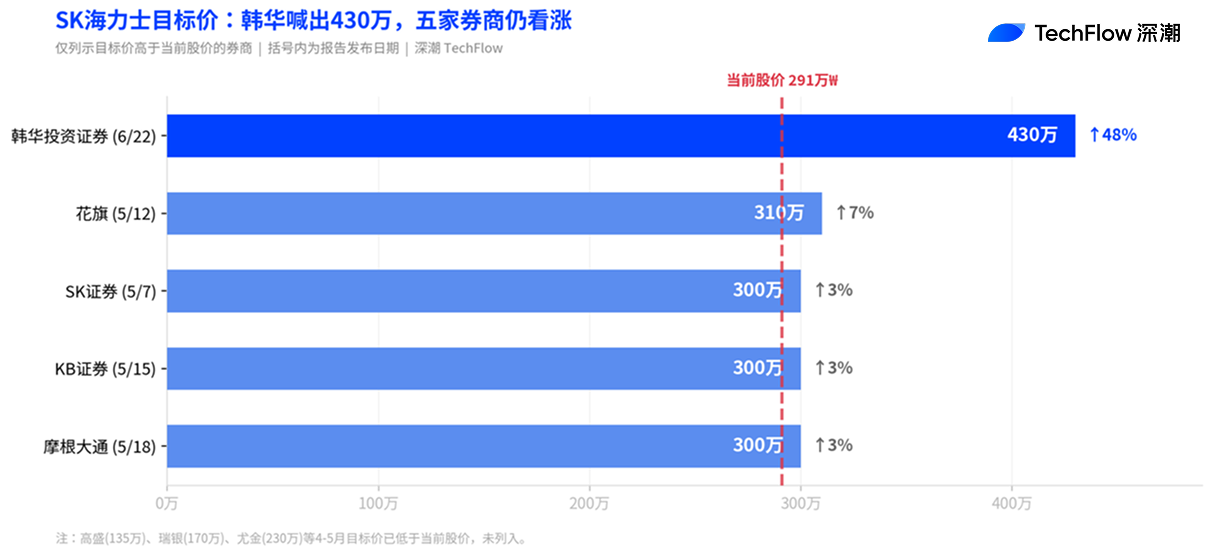

Hanwha Investment & Securities sets a target price of 4.3 million, doubling the previous value

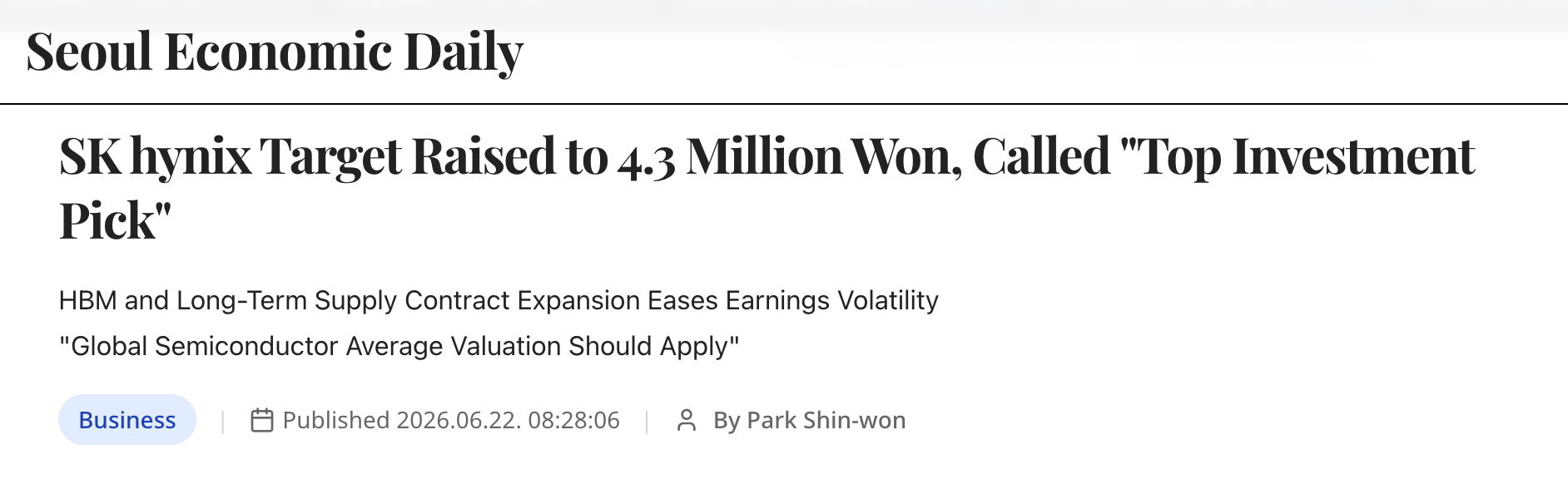

Park Jun-young, an analyst at Hanwha Investment & Securities, raised the target price for SK Hynix from 1.63 million won to 4.3 million won on June 22, nearly 1.6 times higher, making it the highest target price set by any South Korean brokerage currently.

Park's core argument is that SK Hynix is no longer a company with severe profit fluctuations, but is transforming into a company capable of continuously generating high levels of profit. He pointed out that South Korean memory chip manufacturers have long endured valuation discounts, but with the expansion of long-term supply agreements (LTA) and a surge in HBM demand, profit visibility has fundamentally improved.

According to the Seoul Economic Daily, Hanwha used a 10 times price-earnings ratio (PER) to calculate the target price, which is the lowest among global semiconductor companies. SK Hynix currently has a 12-month forward PER of about 6.6 times, lower than that of fellow memory manufacturer Micron. Hanwha predicts that even if the memory market weakens, SK Hynix's operating profit margin will remain at at least 30% or more, while in past downturns this figure had dropped below 10% or even resulted in losses.

Hanwha also listed the ADR listing as a catalyst. Park Jun-young stated that the ADR listing within the year would allow SK Hynix to directly benchmark valuations against similar companies like Micron in the US stock market, "SK Hynix is currently the optimal investment target in both fundamental and momentum dimensions."

Multiple brokerages collectively raised target prices, the valuation framework of the storage industry is being rewritten

Hanwha is not alone. In the past two months, South Korean and international brokerages have undergone a round of intense target price revisions for SK Hynix.

SK Securities raised its target price to 3 million won on May 7, using a 10 times PER framework, which was the highest price among Korean brokerages at the time. KB Securities raised its target price to 3 million won on May 15, predicting an operating profit margin of 78.1% in 2026, stating that storage semiconductors are becoming a "scarce strategic asset that determines the overall performance of AI systems." Citigroup raised its target price from 1.7 million won to 3.1 million won on May 12, citing higher-than-expected HBM price growth in the second half of the year. JPMorgan raised its target price to 3 million won on May 18 and simultaneously revised its earnings per share expectations for 2026 to 2028 upwards by 9% to 20%.

Nomura Securities published a report on May 15, bluntly stating "this time is really different," believing that the valuation logic of the storage industry is undergoing a paradigm shift, and that risk premiums should align closer to TSMC rather than continuing to apply traditional cyclical stock frameworks.

These revisions are supported by a common logic: LTA has changed the pricing mechanism of the storage industry. According to Hanwha's analysis, the current long-term supply agreements signed include price drop protection clauses and legal guarantees for contract performance, allowing manufacturers to maintain a certain profit margin even during market downturns. This is in stark contrast to the past model where DRAM spot prices fluctuated wildly, and manufacturers passively bore the cycles.

Q1 Performance: Revenue exceeds 50 trillion for the first time, operating profit margin 72%

The target price revision is supported by hard data. SK Hynix's revenue for the first quarter of the 2026 fiscal year was 52.58 trillion won, a year-on-year increase of 198%, breaking the 50 trillion mark for the first time. Operating profit was 37.61 trillion won, a year-on-year increase of 405%. The operating profit margin was 72%, surpassing Nvidia's 65%, setting a new record for the semiconductor manufacturing industry.

HBM is the core driving force. SK Hynix currently holds about 70% to 80% of the global HBM market share and is the main supplier for Nvidia's AI accelerators. According to a Goldman Sachs report in April, the forecast for the global DRAM supply-demand gap in 2026 has expanded from 3.3% to 4.9%, the most severe in 15 years. The top three memory manufacturers have nearly sold out their production capacity this year, and the construction cycle for wafer fabs is four to five years, meaning there is almost no new capacity added this year.

UBS indicated when revising SK Hynix's earnings forecast in April that AI-driven HBM demand continues to erode DDR capacity, combined with server replacement cycles and synchronous explosive demand for storage SSDs, the global DRAM supply-demand gap is expected to extend to the fourth quarter of 2027, labeling it a "super cycle for storage that hasn't occurred in nearly thirty years."

Pre-market surge past 3 million won, but formal trading fell over 5%

In pre-market trading on June 23, SK Hynix briefly hit 3.002 million won on the Nextrade NXT platform, breaking the 3 million mark. However, after the formal trading opened, the stock price fell back, reporting 2.75 million won by 11 AM, down 5.79% from the previous day’s close.

The direct reason for the decline was a general weakness in large global tech stocks, although the memory sector in the US stock market performed well overnight (Micron up 6.9%, SanDisk up 4.1%). The KOSPI has increased 7.53% this month, but the growth has been highly concentrated in Samsung and Hynix stocks. Excluding these two stocks, the KOSPI 200 index actually dropped 2.48% during the same period, showing extreme market polarization.

According to The Korea Herald, some brokerages have issued warnings: with Samsung Electronics' profit size and growth rate predictions both exceeding those of SK Hynix, a market cap reversal could be a sign of short-term overheating.

However, data from high-return investors tracked by Meilai Asset Securities (top 1% of returns over the past month) shows that the most net bought stock on the morning of the 23rd is still SK Hynix. These investors view the pullback as an opportunity to increase their positions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。