Original author: Jia Liu

The recent market heat is Zhizhu (02513.HK), the first AI stock in China.

If you bought 1 million worth of Zhizhu in January this year, by June 22, during the intraday peak, it was nearly 25 million, closing with over 20 million. This is also one of the companies that has rapidly surged from hundreds of billions in IPO valuation to a trillion Hong Kong dollar valuation in recent years.

There are three questions repeatedly asked in the market regarding this stock: Who made money from this wave? What led to such a rise? Who will take over next?

This article aims to answer these questions.

The Fastest Wealth Creation Wave in Hong Kong Stocks in Recent Years

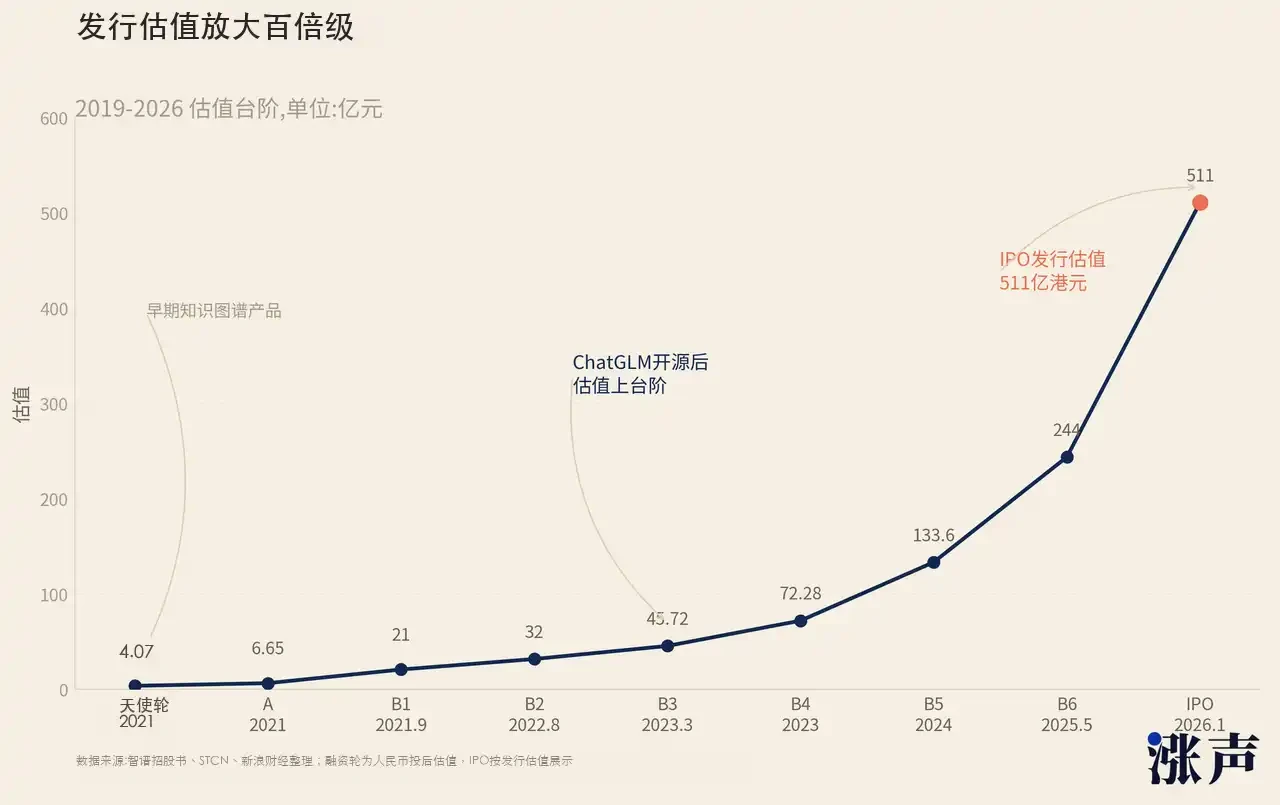

From the angel round to IPO, Zhizhu's valuation has increased by about 130 times. From IPO to the intraday peak on June 22, Zhizhu's stock price rose another 24.6 times.

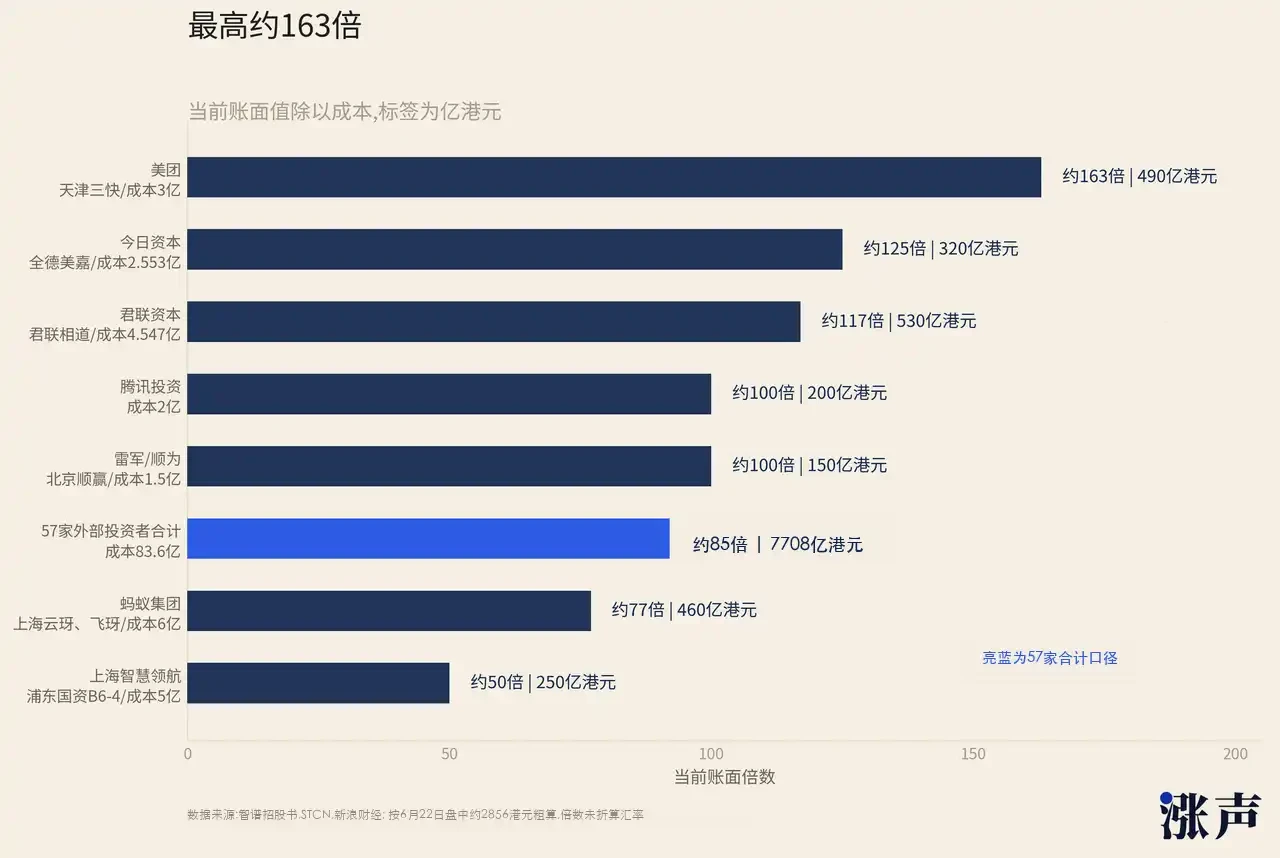

A total of 57 external investors have invested 8.36 billion RMB, which corresponds to about 77.08 billion HKD at the intraday peak on June 22. Overall returns are approximately 85 times. In the history of China's primary market, cases that achieve an average return of 85 times for all investors on a single project can be counted on one hand.

According to the prospectus, Zhizhu’s financing is categorized as "three rounds, fourteen times." The returns for the earliest investors have been particularly astonishing.

Zhuhai Huafa is one of the most extreme in terms of return multiples. According to the prospectus, it invested approximately 20.37 million RMB in the angel round, corresponding to a post-investment valuation of about 407 million RMB. At that time, Zhizhu was still a knowledge graph team spun off from Tsinghua KEG laboratory, and the concept of large models did not yet exist. Transforming over 20 million into several hundred billion Hong Kong dollars is one of the most extreme return cases in the history of China's AI primary market.

Investors from the A and B rounds saw similar results. According to rough calculations based on the intraday peak and market capitalization on June 22, the funds from the A round have already reached hundreds of times, while the B round is close to hundreds as well.

The figures from the following institutions are also astounding. Xu Xin's Today's Capital invested 255.3 million RMB in November 2023, acquiring 11.35 million shares, which roughly corresponds to around 30 billion HKD at the intraday peak on June 22, yielding over a hundred times return. Today's Capital manages around 3 billion USD, which means this investment in Zhizhu has already exceeded the value of their entire fund. Xu Xin has previously invested in NetEase, JD.com, and BOSS Zhipin, but in terms of absolute amounts, Zhizhu is likely her most profitable investment in her career.

Meituan’s example is also very direct. According to available data, Meituan invested approximately 300 million RMB, and now the return has exceeded 150 times. This means that the unrealized profit from a single industrial investment has already exceeded 5% of Meituan's own market value.

Lei Jun’s Shunwei Capital invested 150 million RMB through Beijing Shunying, and at the intraday peak on June 22, it corresponds to about 14.8 billion HKD, yielding about 90 times return. Shunwei manages nearly 50 billion RMB, and this investment in Zhizhu accounts for about a quarter of the total scale.

Legend Capital made the largest absolute profit. They followed up six times, investing a total of 454.7 million RMB, and calculated at the intraday peak on June 22, it corresponds to about 53.3 billion HKD, yielding about 107 times. Legend manages over 90 billion RMB, and the book value of this investment in Zhizhu is close to half of their total management scale. A well-established PE that has invested in iFlytek, CATL, and WuXi AppTec has ultimately achieved a historically high single project return on Zhizhu.

In addition to market institutions, Zhizhu also has a high density of state-owned shareholders. State capitals from Beijing, Tianjin, Shanghai, Hangzhou, Zhuhai, Chengdu, and Daxing are all involved. Zhongguancun Science City, Zhuhai Huafa, Haihe Fuxin Youda Fund, the Artificial Intelligence Fund, Hangzhou Urban Investment, and Daxing Industry Fund are all well-known local government investment platforms. The Social Security Fund Zhongguancun Independent Innovation Investment Fund also participated.

The influx of these funds is not just financial investment. After they come in, they drive the procurement of local government systems. When a local state-owned capital invests in Zhizhu, the local government gains a natural advantage when selecting large model suppliers. This is a very prominent feature of China's technology industry: the wealthiest buyers are the government, and a technology project that can obtain government investment and support has already succeeded halfway. Companies like Zhongji Xuchuang and Changxin Storage have already followed this model, where the founders bring technology back from overseas, and the government invests money to build factories and provide orders, allowing the company to scale quickly.

Employees are also big winners in this wealth creation wave. Zhizhu has a significant employee stock ownership, with two employee stock platforms collectively holding about 15% of the company's shares. At the IPO, the average shareholding value of 25 employees from the Zhizhen platform had already exceeded 100 million HKD. Calculated at the intraday peak on June 22, it has transformed into an average of several billion HKD per person. Another platform, Huihuili, after deducting the founder’s equity, had over 400 employees who, based on an approximate calculation at the June 22 high, also averaged in the billion range.

This density of wealth creation ranks among the top in the history of Chinese technology companies going public.

When Kuaishou went public in 2021, it also created many "paper billionaires," but Kuaishou had a larger market capitalization at listing, and its employee base was larger, causing the wealth to be distributed more evenly. Zhizhu, a company with fewer than 900 employees, has its core options concentrated in a very small number of early employees. After the IPO and an accumulated increase of 24.6 times, the numbers each person receives become extremely exaggerated.

Why Did Zhizhu Rise So Rapidly? The Capital Game Behind the Narrative Brilliance

It is a rare collective wealth creation: early VC, local state-owned capital, internet giants, competitors, the founding team, and core employees are all publicly repositioned in the same project. So why is it able to rise to this extent?

The first thing the market saw is that it indeed has a revenue-generating business.

Zhizhu's most solid revenue is not from C-end chat products or developer communities, but from localized deployment. Simply put, it involves installing the entire set of GLM large model into the client's own servers and intranet, with data remaining local. The primary payers are government agencies, state-owned banks, energy groups, and smart city projects. For the full year of 2025, localized deployment revenue is 534 million RMB, with over 100% year-on-year growth, accounting for 73.7% of total revenue, with a gross margin of 48.8%. For a large model company that is still in losses, this business at least proves it is not purely a storytelling venture.

The pricing of local deployment is roughly divided into several tiers. County-level government and small and medium enterprises use a lightweight version, at an annual fee of about several hundred thousand RMB; city-level governments and ordinary state-owned enterprises buy the standard universal version, packaged for three years at one or two million RMB; provincial departments, leading banks, smart cities, meteorological services, energy groups buy the flagship version, with annual fees reaching several hundred thousand RMB, plus maintenance and upgrade fees. A single project may not seem exorbitant, but China has dozens of provincial-level administrative regions, hundreds of prefecture-level cities, and thousands of districts, alongside vertical fields like finance, energy, and transportation.

As long as government and enterprise AI budgets continue to exist, Zhizhu's revenue ceiling is unlikely to be too low.

The shareholder structure is also endorsing this business. Names like Zhongguancun Science City, Zhuhai Huafa, Hangzhou Urban Investment, Chengdu High-tech Zone, and Pudong State-owned Capital entering the shareholder list is not just because they want to make money on stocks. After they invest, they often drive local demonstration projects, government system procurement, and industrial park cooperation. There has always been a similar path in China's technology industry: the government provides money, scenarios, and orders, and the company scales up quickly with the projects. In the past, chips, storage, and new energy vehicles have all followed similar paths, and Zhizhu has simply applied this logic to large models.

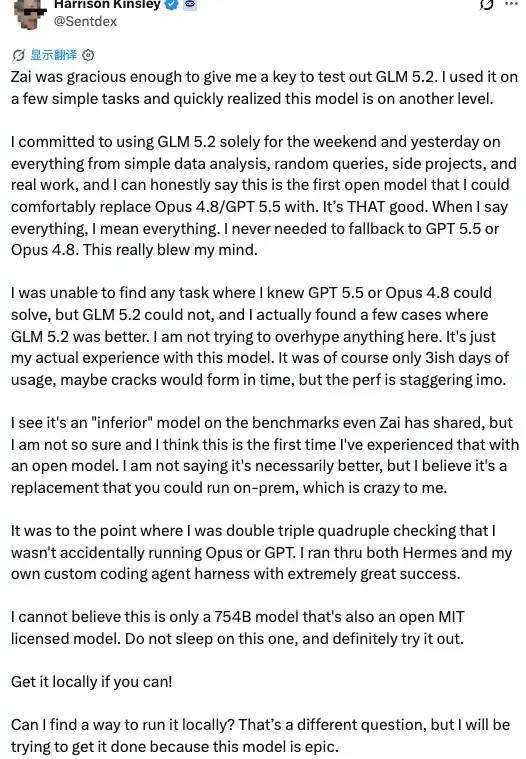

However, if it had only government and enterprise deployments, Zhizhu would not have risen like it has today. What truly ignited the second wave of enthusiasm was the rediscovery of GLM-5.2 in the English tech community.

In mid-June, Z.ai released GLM-5.2, focusing on coding and agents, supporting context of around 1 million tokens, with MIT open-source weights and API prices remaining unchanged. It did not immediately cause a significant stir on the Chinese internet, as domestic discussions about large models are often dominated by DeepSeek, Tongyi, and Hunyuan. But the English developer community reacted very quickly.

Vercel CEO Guillermo Rauch stated on X that he was "really impressed, almost shocked" by the programming capabilities of GLM-5.2. Former Meta, Google DeepMind, and Microsoft executives like Matt Velloso called it the first open-source model to reach a threshold for daily use. Developers found that they could shift much of their daily work to GLM-5.2 without needing to revert to GPT or Claude for many tasks.

This kind of dissemination is very important for Zhizhu. Chinese investors see Zhizhu as a Tsinghua-backed, state-owned, government enterprise deployment, and a rare AI stock in Hong Kong; the English tech community sees GLM-5.2 and questions whether it can replace parts of Claude and GPT. Can it be deployed locally? Is it open-source? Is the cost low enough?

When overseas developers, AI infrastructure companies, and English investors start discussing Zhizhu using this framework, it no longer remains just a Chinese local government and enterprise AI story, but rather becomes an asset that can be driven by global model layer reassessment logic.

The market is buying not just the projected revenue of over 500 million from localized deployments in 2025, but a possibility: If open-source models can really approach closed-source models, if Chinese model companies can reduce inference costs, if unlisted tech giants like OpenAI, Anthropic, and SpaceX continue to elevate the valuation anchors for model layers and hard tech assets, then Zhizhu, as one of the few already listed and directly purchasable model companies, will inherently gain a premium.

Of course, there is a significant question here. Whether the buzz from developers can ultimately translate into API revenue, localized deployment contracts, and high-margin cash flow has not yet been fully proven. However, during stock price increases, the market often first trades on possibilities before questioning profit statements. GLM-5.2 provided Zhizhu with a new narrative entry point and offered overseas capital a reason to buy.

Another direct and important reason is that the circulating chips are too few.

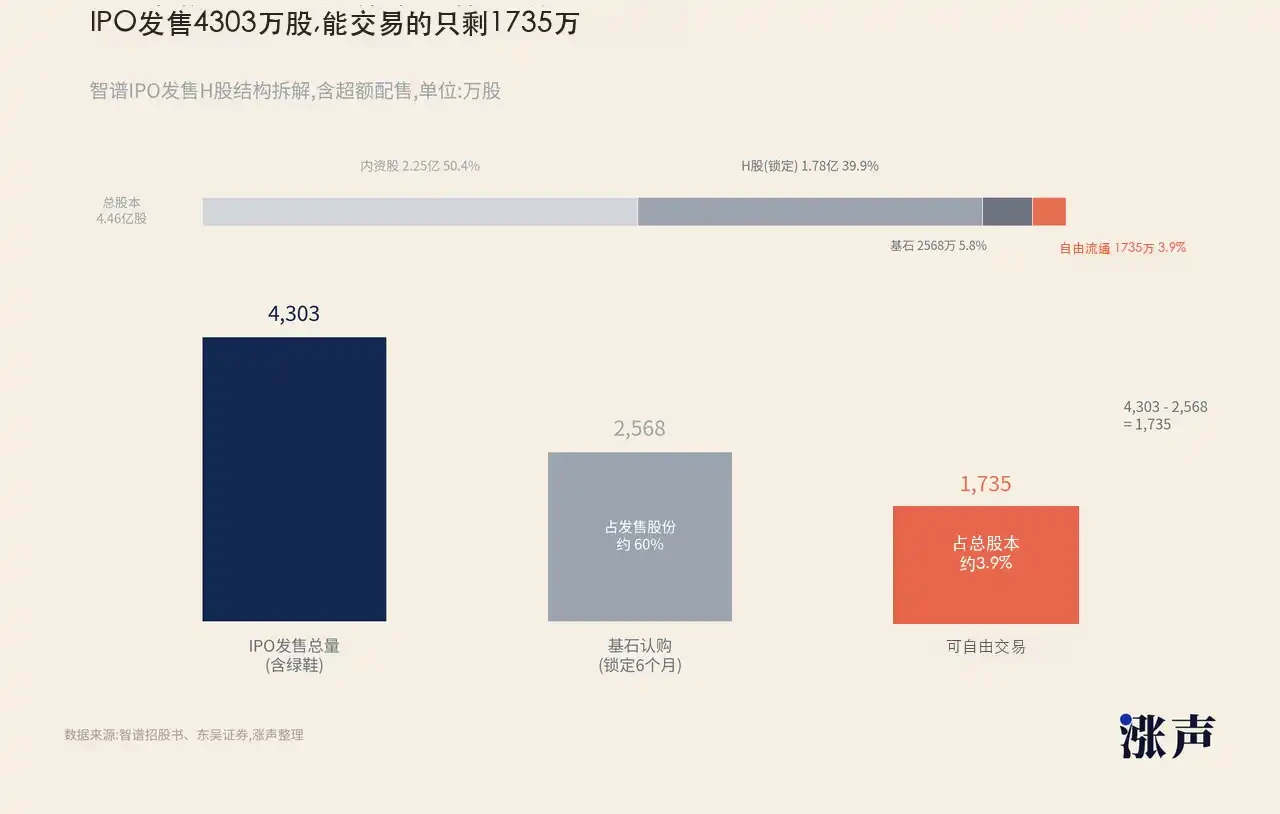

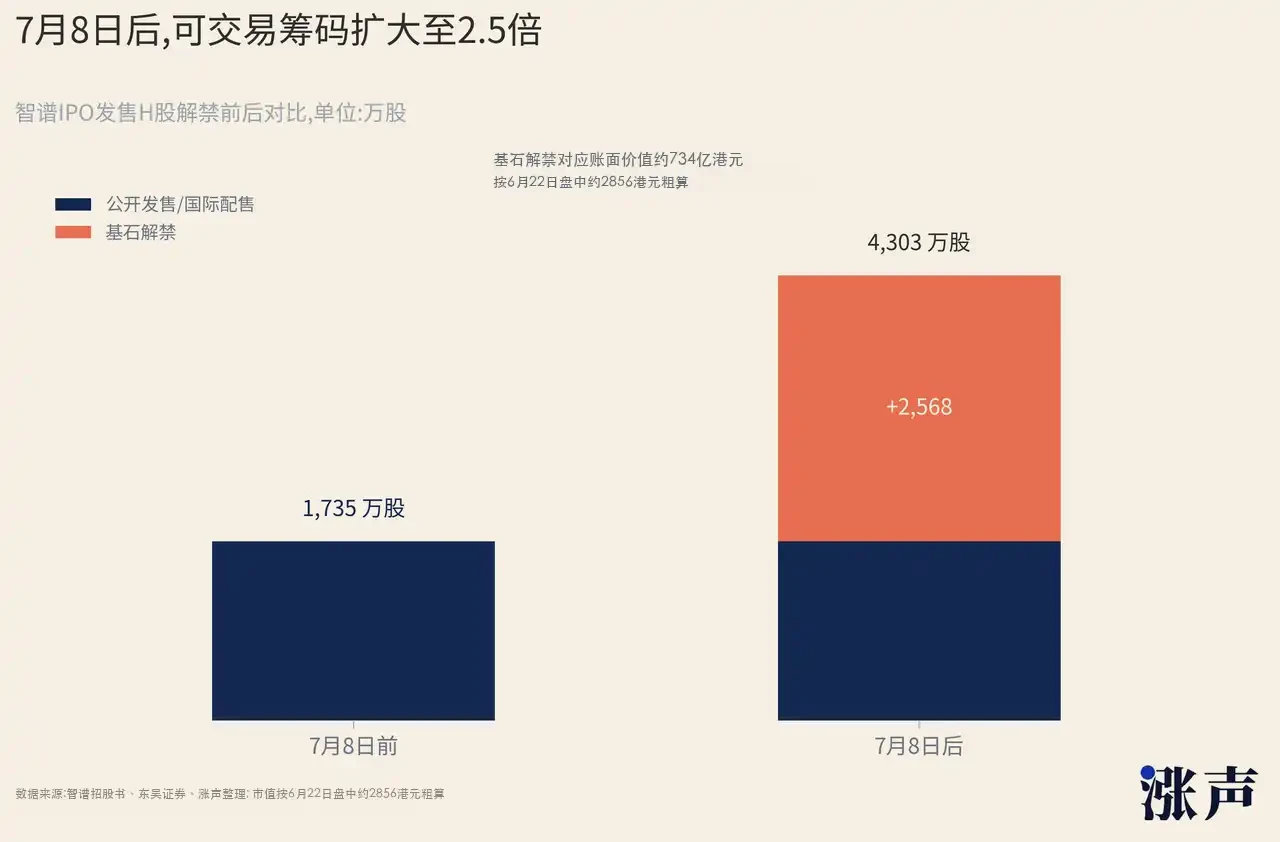

Many people who see the IPO share numbers in Dongwu Securities' research report may assume that Zhizhu has a circulating share capital of 221.31 million shares, accounting for about 49.6% of the total share capital, which isn't low. However, it is important to distinguish that "circulating shares" and "freely circulating shares" are not the same. Zhizhu is a shareholding company registered on the mainland and listed in Hong Kong; the circulating shares in the research report are closer to the H-share standard that has already been listed, but a significant part of these H shares was still locked during the initial listing period and could not be traded immediately. What truly determines the elasticity of the stock price is how many chips can be freely bought and sold in the market each day.

From the IPO structure, Zhizhu globally issued about 37.42 million H shares. Including the overallotment option, the total issuance scale is about 43.03 million shares, accounting for approximately 9.65% of the total share capital. This is less than one-tenth of the total share capital. More critically, a large portion of the IPO shares was taken up by cornerstone investors. Eleven cornerstone investors subscribed for a total of about 2.984 billion HKD, accounting for nearly 70% of the issued shares. Cornerstone investors typically face a six-month lock-up period, and the corresponding unlock date for this batch of Zhizhu is July 8, 2026.

This means that among the 43.03 million new shares issued in the IPO, about 25.68 million shares are locked by cornerstone investors. After July 8, the unlocking of cornerstone shares will expand the tradable portion from approximately 17.35 million shares to about 43.03 million shares, nearly 2.5 times the original. Based on the intraday peak on June 22, the 25.68 million shares correspond to a book value of approximately 73.4 billion HKD.

This is not a billion-dollar shock, but it is sufficient to change the supply-demand dynamics of the chips.

In addition to cornerstone investors, shares held by pre-listing shareholders, state-owned platforms, strategic investors, and employee stock platforms will gradually enter the sellable window in the future. They may not necessarily sell on July 8, but the market will not wait for the details to solidify before reacting. Once investors realize that these substantial unrealized gains will gradually transform into sellable chips, the stock price will begin to discount potential supply.

Such scenarios have been seen in the Hong Kong stock market before. After UBTECH's one-year listing unlocking, major shareholders quickly reduced their holdings, resulting in a significant stock price drop.

If cornerstone and early shareholders only make minor exploratory sales, the market might absorb it. However, if there are continuous large block sales at discounts, significant shareholders disclose reductions, and transaction volumes increase without a price rise, the scarcity premium will quickly evaporate.

Zhizhu currently needs to prove two things. First, whether the developer buzz brought by GLM-5.2 can translate into real revenue. Second, after July 8, whether the market can absorb the newly sellable chips, shifting the stock price from being driven by "low circulating shares" to being driven by "fundamentals."

If both of these things can be achieved, Zhizhu's high valuation at least still has room to continue its narrative.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。