Author: Rita

Tide Guide

Morgan Stanley updated its research report on SanDisk on June 22, raising its target price from $1100 to $1750 and maintaining an overweight rating. The reasoning is straightforward: AI inference demand is rewriting the rules of the NAND market, and cloud data center customers are insensitive to pricing, which gives SanDisk pricing power. Additionally, the new business model agreements lock in profit margins, making the company's future profits fairly predictable.

Changing Demand Structure, AI Inference Reshapes NAND Market

After a 64% quarter-on-quarter growth in Q4, SanDisk's Q1 cloud business growth rate further expanded to 233%. This is due to a change in demand structure. Cloud vendors are paying premiums for AI inference KV Cache (key-value cache) and context window storage. Morgan Stanley's calculations show that the proportion of cloud business in SanDisk's Q1 sales has reached a high level, almost entirely driven by TLC (Triple-Level Cell), with customers demanding storage density and performance. These customers do not play by the consumer end's logic but sign long-term contracts with fixed prices, effectively supporting profit margins.

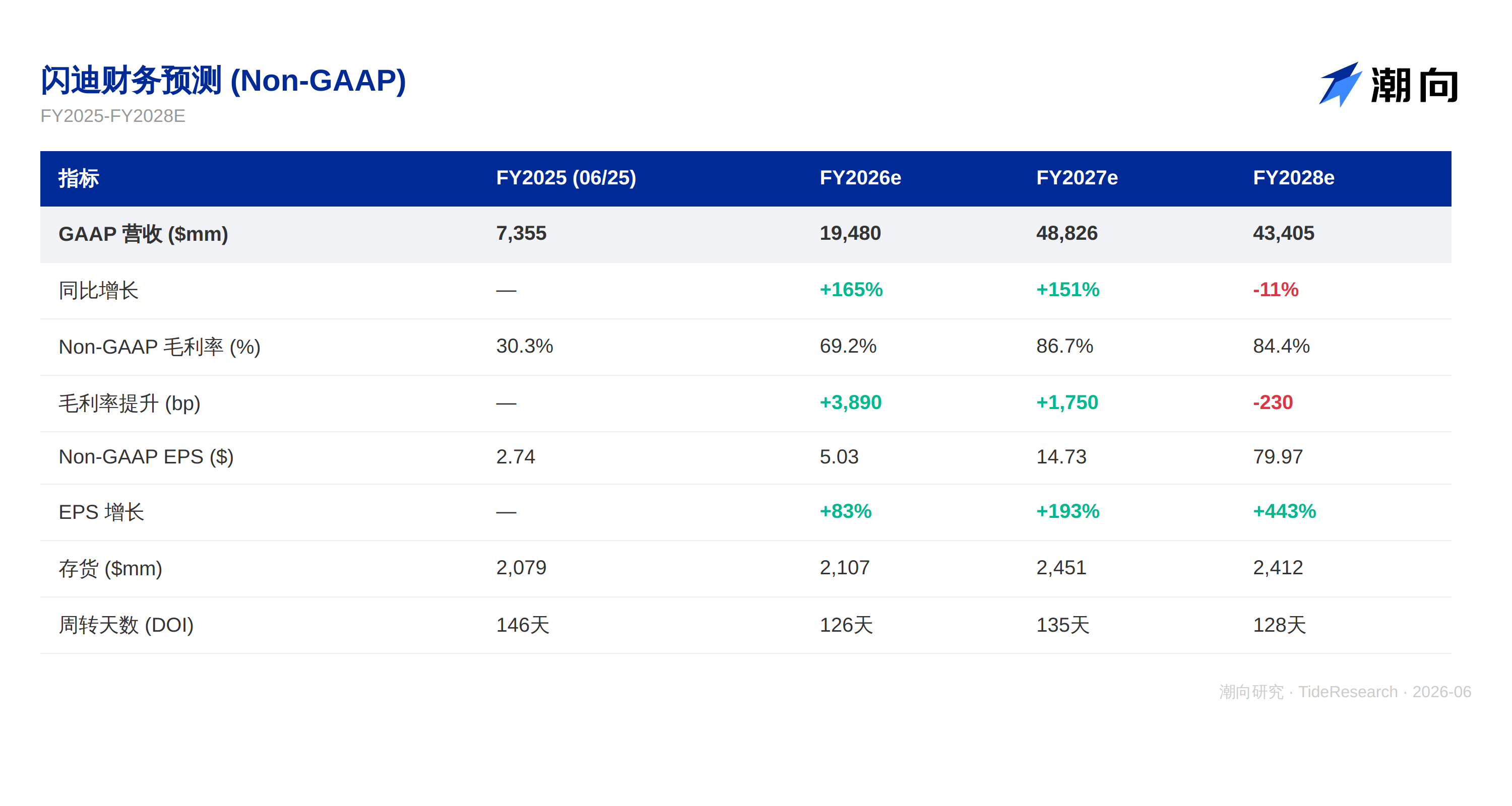

The NBM (New Business Model) agreements launched by SanDisk have already secured over a third of FY27 bit shipments. These agreements typically span 3 to 5 years and include fixed prices or upper and lower limit structures. A key point: even at the base price, these contracts can maintain around 80% gross margins. By comparison, historical data shows SanDisk's gross margin was only 30.3% in FY25, increasing to 69.2% in FY26e, and soaring to 86.7% in FY27e, indicating that this improvement is sustainable. Morgan Stanley believes the company could eventually bring 70% to 80% of its shipments under NBM coverage, and once this ratio is achieved, the company’s profitability would have a cushion. Moreover, with 80% margins even at base prices, it means that high profits can be maintained even in a price war.

Supply Pricing Power and Profit Resilience

The current tight state of NAND supply may persist for a long time. Throughout the industry cycles, overcapacity has repeatedly triggered price collapses, and this time the expansion of AI data centers is accelerating, with storage demand far from saturated. By locking in long-term contracts during this window, SanDisk can hedge a significant portion of cyclical risks. Morgan Stanley expects the ASP (average selling price) to continue rising until calendar year 2026, possibly extending into mid-2027. SanDisk derives 40% to 50% of its revenue from North America, with data centers becoming the largest end market. In the context of tight supply and high customer loyalty, pricing power is firmly in the hands of suppliers.

The company's target is a bit growth rate of 15% to 19%, primarily relying on technological transitions (density improvements and process enhancements) rather than capacity expansion. From FY25 to FY27, revenue is expected to grow from $7.355 billion to $48.826 billion, an increase of about 6.6 times, while EPS is projected to rise from $2.74 to $14.73. The key behind these numbers is the quality of growth, not speed. Growth comes from high-margin cloud business, not from the low-price, low-margin consumer market. The company has just announced a $6 billion stock repurchase plan, with management believing the current stock price is among the lowest valuations in the semiconductor sector. From a valuation perspective, Morgan Stanley's three scenarios are based on FY27 full-year EPS: in the base scenario, a 28x PE corresponds to $1750, a bull market at 31x PE corresponds to $2635, and a bear market at 25x PE corresponds to $1100.

Coexistence of Catalysts and Risks

There are several directions worth noting for the upside catalysts. The penetration of data center eSSD (enterprise solid-state drives) may exceed expectations, edge AI applications will drive growth in NAND content volume, and investments in advanced technologies like HBF (high bandwidth flash) may also begin to yield returns. Downside risks include industry growth falling short of expectations, competitors increasing capital expenditures, SanDisk losing market share in the data center sector, and Chinese memory manufacturers like YMTC (Yangtze Memory Technologies Co., Ltd.) continuing to gain market share.

Morgan Stanley's bullish case for SanDisk is built on three pillars: the structural demand changes brought by AI inference, the gross margin protection afforded by NBM agreements, and the ongoing tight supply of NAND. The target price has been raised from $1100 to $1750, corresponding to about 28x PE for FY27; predictions will be adjusted with earnings reports and customer feedback, but the logical framework is more valuable than the specific numbers.

Disclaimer

This article is a compilation and interpretation of research reports from third-party brokerage firms by Tide Research. The ratings, target prices, earnings forecasts, and related judgments cited in this article represent the views of the brokerage firm's analysts, solely reflecting their institution's stance, and do not represent the views of Tide Research, nor do they constitute any investment advice.

Please pay attention to three points when reading: 1. The target price is the analyst's expectation for the next approximately 12 months, a prediction rather than a promise, and will be adjusted repeatedly with performance and market conditions. 2. Sell-side research reports are inherently optimistic, and some covered companies have investment banking relationships with the brokerage. 3. The value of the research report lies in the main logical direction and its underlying assumptions, rather than any specific target price. Focus on the logic, not just the price.

The market carries risks, and decisions should be made independently. This article should not be used as a basis for buying or selling any securities.

Data source: Morgan Stanley Research Report (Joseph Moore, June 22, 2026) · Company Financial Reports

Tide Research · June 2026

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。