Author:Bu Shuqing

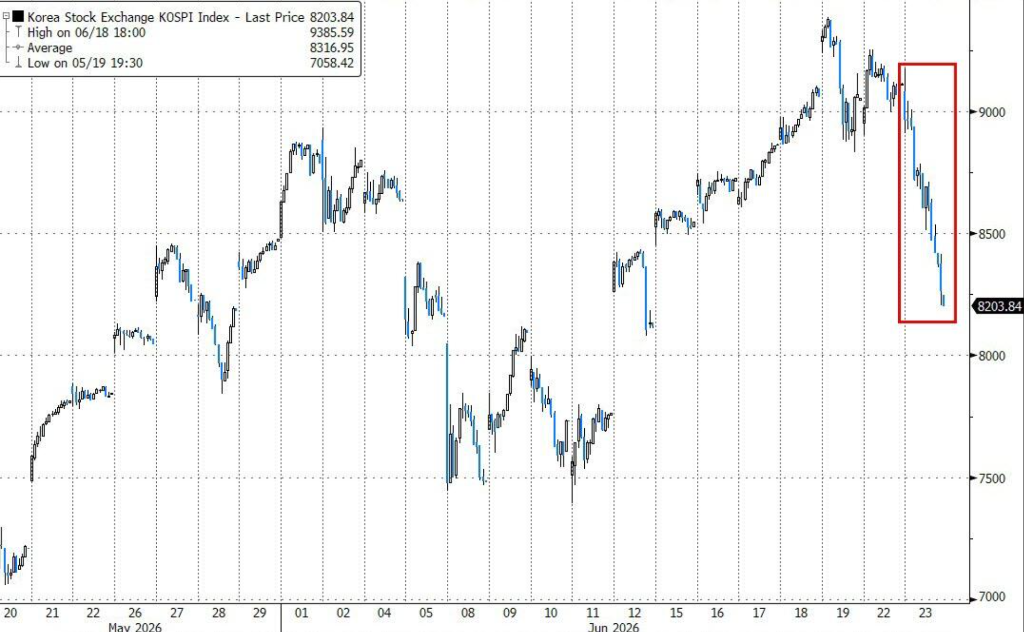

The South Korean stock market has rapidly collapsed from historical highs, with a risk that has long accumulated due to structural weaknesses being concentrated and released under multiple triggering factors.

The South Korea Composite Stock Price Index (KOSPI) fell 10% in a single day on Tuesday, with Samsung Electronics and SK Hynix both plunging over 12%, together contributing to 71% of the index's drop. The South Korean exchange initiated a 20-minute circuit breaker in the afternoon, but failed to stop the downward momentum, with foreign investors net selling KOSPI stocks exceeding $2.5 billion on that day.

Chris Cha, the head of Korea high-touch trading at Goldman Sachs, noted in a subsequent report that the root cause of the crash was not a deterioration in fundamentals but rather deep structural fragility in the market—when pension funds switched from buyers to sellers and retail leveraged funds faced forced liquidations, the marginal buying that supported the rally collapsed instantly.

The warning implications of this crash for market structure far exceed the magnitude of the single-day decline itself. The Goldman Sachs report clearly stated that the recent rally in the South Korean stock market increasingly relied on technical and liquidity-driven factors, rather than substantial new fundamental buying; once this fragile support is disturbed, an extremely large fluctuation at the index level becomes unavoidable.

Liquidity Structural Imbalance: Retail Investors Become the Final Buyers

The deep background of this crash is the ongoing narrowing of the buying structure in the South Korean stock market.

Chris Cha pointed out in the report that foreign capital had not been the main driver of the rally, and domestic institutional buying space was also increasingly limited; the market has in fact established retail funds as the most significant source of marginal demand. This structure can be maintained during stable market conditions, but can easily trigger a chain reaction when faced with external shocks.

Alexander Redman, chief equity strategist at CLSA Singapore, stated in a briefing that "the magnitude of this volatility is closely related to the degree of bubbling within the South Korean market, as it is now almost entirely driven by retail investors."

He candidly expressed that "seeing this level of volatility is truly unsettling."

According to the Korea Financial Investment Association data, the retail financing balance (which refers to margin debt incurred by borrowing money to buy stocks) reached a record high of 38.5 trillion won (approximately $25 billion) this month.

Kim Namho, a fund manager at Timefolio Investment Management in Seoul, stated, "The forced liquidations appeared to start around two or three o'clock in the afternoon, and selling orders accelerated the downward trend."

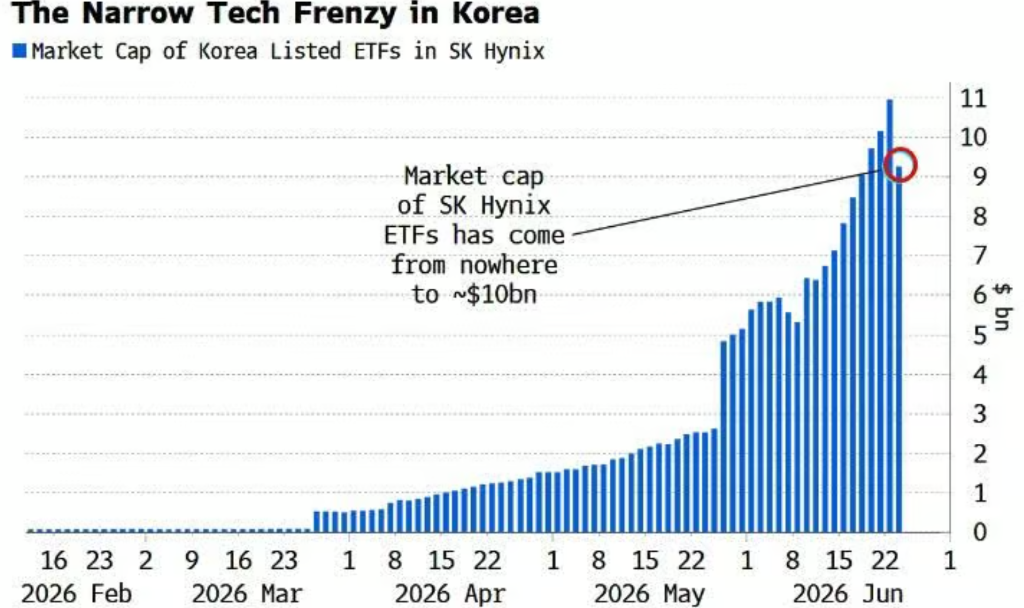

Regulatory Risks of Leveraged ETFs: Policy Signals Undermining Technical Buying

Another key thread in this crash is the regulatory shift regarding single-stock leveraged ETFs.

On that day, the highest financial regulator in South Korea publicly expressed regret over the failure to prevent the listing of single-stock leveraged ETFs linked to Samsung Electronics and SK Hynix, mentioning their negative side effects. This statement was made while the market was already in a fragile state, and its impact should not be underestimated.

According to the Goldman Sachs report, the asset management scale of 16 leveraged ETFs in the country has increased to $9.1 billion, while the combined scale of the CSOP 2x leveraged ETF tracking SK Hynix and Samsung has reached $21 billion. Notably, 92% of the asset management scale of domestic leveraged ETFs comes from retail investors.

Chris Cha pointed out that single-stock leveraged ETFs amplify price volatility in both directions through their rebalancing mechanism, particularly evident in large-cap stocks with high retail participation. Even if regulators do not take immediate action, the official expression of "regret" is sufficient for investors to reassess the sustainability of technical buying in the recent rally.

The Goldman Sachs report listed potential stabilizing measures that the Financial Services Commission (FSC) might take, including increasing the base margin requirement for retail participation in leveraged ETFs, strengthening qualification exam requirements, setting an upper limit on the asset management scale for individual ETFs, restricting the issuance of new products, and tightening the trading suspension mechanism when ETF prices deviate significantly from net asset value.

Pension Rebalancing: The Largest Stabilizer Turns into Mechanical Selling

In this crash, the role reversal of the National Pension Service (NPS), South Korea’s largest pension fund, is one of the core pressure sources emphasized in the Goldman Sachs report.

Previously, the significant rise in the stock market had pushed the domestic stock position above 30%, higher than the approximately 28.8% cap target, leading the NPS to proactively net sell about $1 billion in KOSPI over the past six trading days (including that day). Since June, the NPS's net selling scale has reached $1.5 billion, setting a record for the largest single-month net selling since April 2021.

Chris Cha noted that pension funds are typically viewed as a domestic anchor force stabilizing the market, but once the actual holding weight significantly exceeds the target, this group of investors will shift from passive support to a mechanical source of supply. Given that the market is already highly concentrated on a few large-cap tech stocks, and the technical indicators are clearly overstretched, the impact of this shift is particularly significant.

Ahead of Micron's Earnings Report, Chip Stocks Concentrate on Reducing Positions

The reason why the declines of Samsung Electronics and SK Hynix far exceeded the index is closely related to Micron Technology's impending earnings report, which is set to be announced Thursday morning Asia time.

The Goldman Sachs report pointed out that investors' expectations ahead of Micron's earnings report were already at extremely high levels, creating conditions for early position reduction.

When the market rally increasingly relies on tactical enthusiasm rather than substantial new buying, event risks often trigger a larger-scale profit-taking than can be explained by the fundamentals themselves.

Fundamentals Remain Unchanged, but Recent Pathways Become More Cautious

The Goldman Sachs report clearly distinguishes between structural risks and fundamental judgments.

Chris Cha stated that the semiconductor cycle is still on an upward trajectory, demand related to AI continues to support, earnings expectations at the index level are consistently improving, and KOSPI valuations are still considered relatively low. He maintains a constructive mid-term judgment on the South Korean stock market, but holds a more cautious attitude towards recent movements.

He pointed out that the next attractive entry opportunity will not arise merely because the market looks cheaper after a sharp decline, but will need to wait until forced selling significantly eases, Samsung and SK Hynix stabilize post-Micron's earnings report, and the market can build a more solid buying foundation over several trading days.

"Today's decline, rather than being a judgment on South Korea's fundamentals, is better seen as a reminder of how the recent rally has been 'financed'," Chris Cha wrote. "Even in a market where the mid-term logic still holds true, once the market structure is excessively stretched, it may still experience violent adjustments."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。