The current central bank gold purchases have become the "only support," with Goldman Sachs and other investment banks intensively lowering their target prices. The battle to defend the psychological barrier of $4000 has begun, and the one-sided rise feast has come to an end.

Written by: Li Jia

Source: Wall Street Observer

Gold, one of the most crowded long trades globally this year, is experiencing a severe reversal.

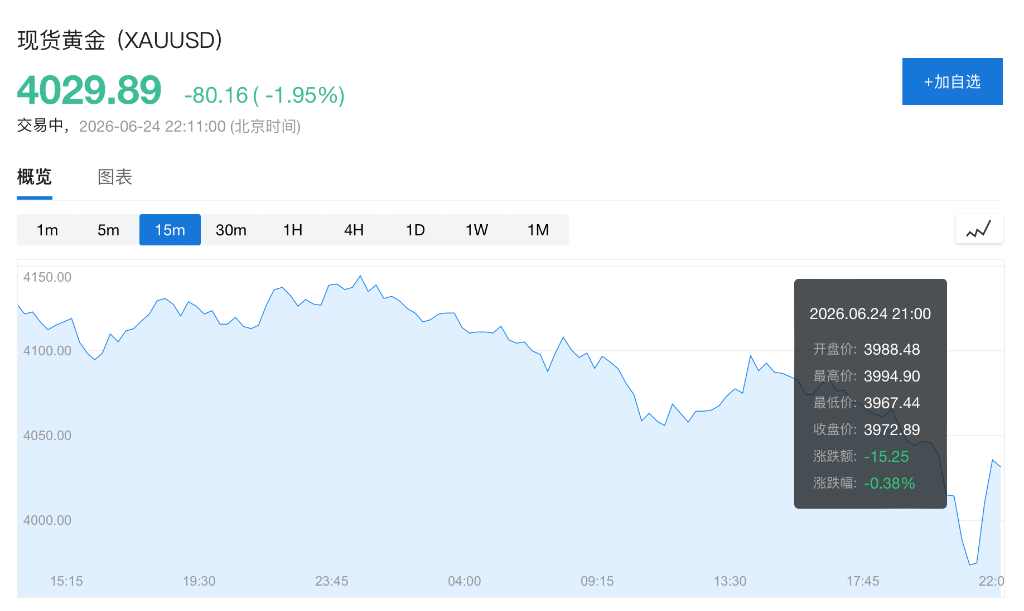

On June 24, spot gold fell below $4000 per ounce during trading, marking the first time since November last year that it has breached this critical integer level. Since reaching a historic peak near $5600 per ounce at the end of January this year, gold prices have retraced approximately 29%, officially entering a technical bear market range.

Over the past three years, gold has recorded double-digit annual gains consecutively, with prices doubling. Multiple factors, including central bank gold purchases, global interest rate cut expectations, concerns about dollar credit, and geopolitical conflicts, have resonated, making gold one of the most sought-after assets worldwide. However, as expectations for Federal Reserve policy make a sharp turnaround, the dollar index continues to strengthen, and risk aversion demand noticeably cools, the core logic that previously supported gold's upward movement is facing substantial challenges.

Recently, several Wall Street institutions have intensively lowered their gold price targets, with Goldman Sachs, Deutsche Bank, Citigroup, and Morgan Stanley shifting to a cautious stance. The market begins to reassess a key question: has the super bull market in gold that lasted three years reached its end?

Reassessment of Interest Rate Expectations Becomes the Biggest Bearish Factor for Gold

The core reason for the current gold adjustment stems from the market's repricing of the path of U.S. interest rates.

Previously, the U.S.-Iran conflict once propelled international oil prices to rise sharply, raising market concerns that energy prices would translate into inflation, thereby forcing the Federal Reserve to maintain higher interest rates. Although recent oil prices have fallen with the advancement of ceasefire negotiations, the market's vigilance regarding inflation has not fully dissipated.

More importantly, newly appointed Federal Reserve Chairman Waller sent clear hawkish signals in his first monetary policy meeting. The market began to factor in the possibility of further interest rate hikes before the end of the year, while U.S. Treasury yields remained elevated, and the dollar index rebounded in tandem.

For gold, which does not generate interest income, a high interest rate environment means increased holding costs, leading funds to prefer allocations toward yield-bearing assets like Treasury bonds. ING analysts believe that the primary driver of gold's recent decline is indeed the significant reassessment of interest rate expectations.

Continuous Outflows from Gold ETFs and Strong Wait-and-See Sentiment in Physical Consumption

In addition to macro pressures, signals from the financial sector are also becoming cautious. Data from Deutsche Bank shows that gold ETFs continue to record net outflows, reflecting a significant decline in interest from traditional asset allocation investors in gold.

Meanwhile, there is also no improvement on the physical consumption side. Although mainstream domestic jewelry brands have cumulatively pulled back over 460 yuan per gram from their peaks at the beginning of the year, the offline market has not seen the anticipated buying frenzy at lower prices.

Under the influence of the "buy highs, not lows" sentiment, most consumers choose to hold cash and wait for further adjustment space. Several gold retailers have reported that even promotional measures like weight discounts and fee reductions have not boosted store foot traffic or actual transactions, with overall trading sentiment remaining weak.

Investment Banks Intensively Downgrade Gold Price Expectations, Central Bank Gold Purchases Become the Only "Pillar"

As international gold prices continue to decline, several Wall Street investment banks have recently cut their price forecasts extensively, indicating institutional caution toward gold's short-term outlook.

Goldman Sachs has significantly lowered its year-end gold price target by $500 to $4900 per ounce; Deutsche Bank has reduced its target prices for the third and fourth quarters to $4300 and $4800, respectively, with some forecasts dropping by over 20%. BMO Capital Markets has also lowered its average gold price expectation for the second half of the year by 5% and explicitly pointed out that the direction of U.S. monetary policy remains the biggest uncertainty risk facing gold.

Amid the current intertwining of many bearish factors, central bank gold demand has become the most solid "ballast" in the gold market.

According to the latest data, global central banks' net gold purchases reached their highest level in over a year in the first quarter, with many central banks continuing to increase their holdings, and surveys indicate that the purchasing momentum from official sectors is likely to remain strong in the coming years. Deutsche Bank's latest report bluntly states that central bank demand has become the "only still solid pillar" of the current gold market.

This means that despite the withdrawal of speculative funds, ETF reductions, and the slowdown in consumer demand putting pressure on gold prices, official reserve demand has temporarily prevented gold from experiencing a more profound collapse.

The Battle to Defend the $4000 Threshold Begins

For the market, $4000 per ounce is not just an integer threshold, but also an important psychological defense line.

If gold prices can stabilize at this level, it means that the market has largely digested the bearish factors such as rising interest rate expectations, a stronger dollar, and cooling geopolitical risks, and may hope to enter a phase of consolidation.

However, if the $4000 level is breached and continues to decline, it could trigger programmatic trading and further leveraged fund liquidations, leading to a new round of selling pressure.

From a longer-term perspective, the core driving forces behind the three-year gold bull market—global central bank gold purchases, expanding fiscal deficits, and the diversification of the monetary system—have not completely disappeared. Yet in the short term, the market's dominant logic has shifted from "rate cut trading" to "high rate trading."

For gold, this may not mean the complete end of the long-term bull market, but at the very least, it signifies that the era of nearly one-sided rising gold prices has come to an end.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。