Original author: Jia Liu

Low circulation, grand narratives, and high market value are becoming common characteristics of this round of speculation in the financial markets.

After less than half a year of listing on the Hong Kong Stock Exchange, the stock price of Zhi Pu once increased by 25 times. However, if one looks at its share structure, a more critical but easily overlooked number is revealed: at the initial stage of listing, only about 17.35 million shares of Zhi Pu were actually freely tradable in the market, accounting for less than 4% of the total share capital. For a company with a market value of one trillion Hong Kong dollars, the actual trading pool is only in the range of three to four hundred billion Hong Kong dollars.

This is a typical but not unique case; it can even be said to be a microcosm of this round of market gameplay.

Just over a week ago, SpaceX went public with a valuation of 1.77 trillion dollars, yet the publicly traded shares accounted for only 4.3%. To accommodate its listing, the Nasdaq directly abolished the 10% minimum public holding threshold that had been in effect for decades. SpaceX's market value peaked at over 2 trillion dollars, but the daily trading volume was only about 100 million dollars.

Cerebras, an American AI chip company, sold only about 15% of its outstanding shares during its IPO in May, and on the first day, its stock price soared to more than twice the issue price. Figma achieved total revenue of less than 10% share capital from issuance and old stock sales, with a first-day increase of 250%.

Low circulation, grand narratives, high market values. The structures that the cryptocurrency market has been playing with for several years are now being fully replicated in the traditional stock markets. The US stocks, Hong Kong stocks, and A-shares are all experiencing similar structures, with narratives extending from AI, chips, and large models to stablecoins.

The Era of Pricing Based on Financial Reports Has Ended

In February 2000, a hand puppet dog made from socks appeared in a Super Bowl advertisement. Pets.com purchased this 30-second ad spot for 1.2 million dollars. At that time, its annual revenue was less than 6 million dollars, with losses exceeding 60 million dollars. Nine months later, the company liquidated, and the sock puppet became the most iconic gravestone of the internet bubble.

The lessons from that generation of the market are almost inscribed in all investment textbooks: valuations without revenue support are bubbles; narratives cannot replace financial reports.

For over 20 years, this lesson has dominated the market. DCF, PE, PEG, discounted free cash flow—all methods of pricing based on financial data became orthodox. Warren Buffett was revered again after the 2008 financial crisis. "Buying without looking at financial reports" became synonymous with speculation.

However, when we look at the new technology sectors expected in 2025 to 2026 today, we find a fact: the most favored companies in these sectors are, in fact, losing money.

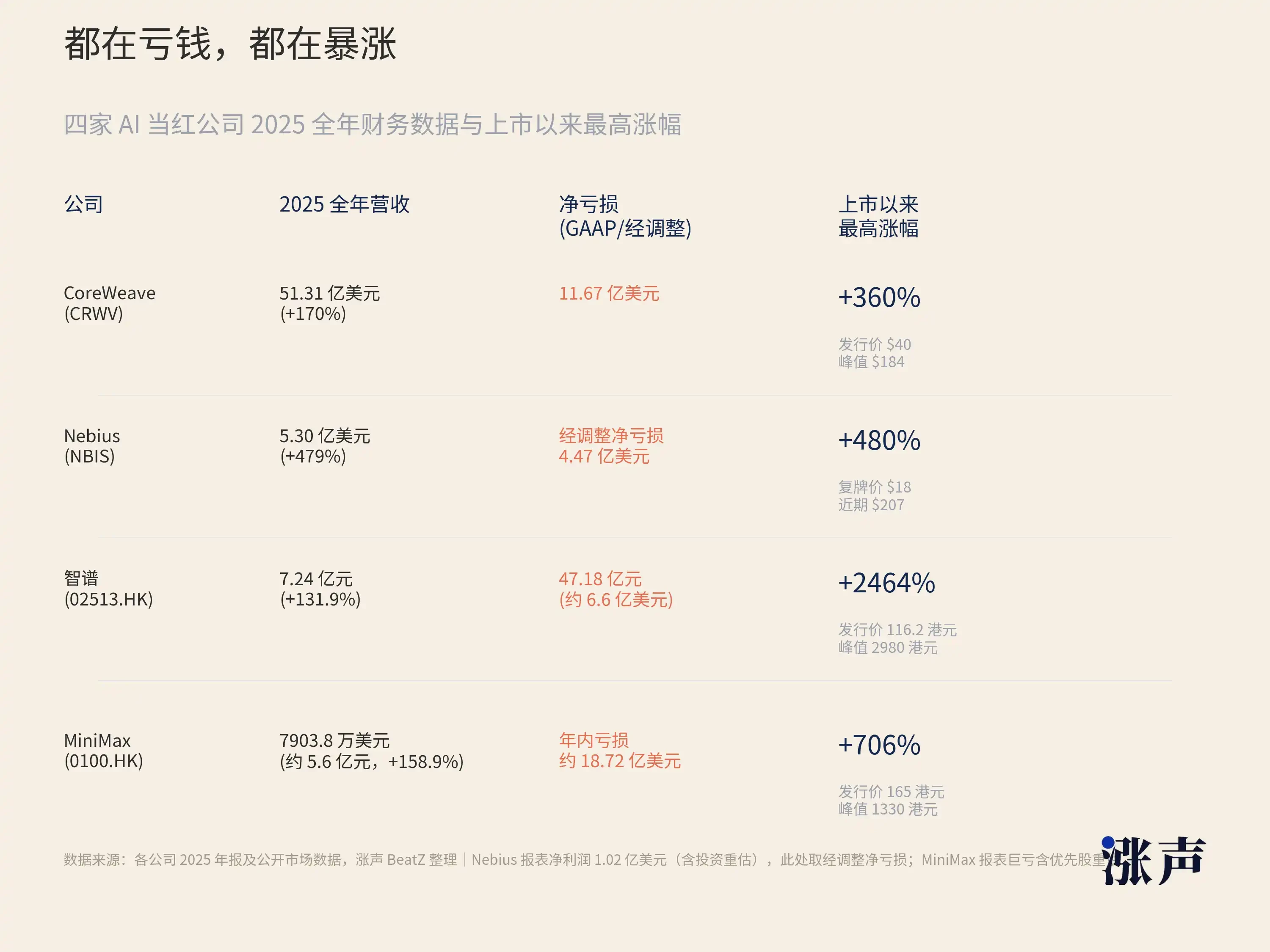

For example, CoreWeave, an AI computing infrastructure company invested by NVIDIA, had revenues of 16 million dollars in 2022, projected to grow to 5.1 billion dollars by 2025, a more than 300 times increase in three years. The revenue growth rate is astonishing, yet net losses expanded from 31 million dollars to 1.2 billion dollars. In Q1 2026, the company reported revenue of 2.1 billion dollars and a net loss of 740 million dollars, with a debt-to-equity ratio reaching 10.7. According to traditional banking credit standards, such a balance sheet is not healthy. Nevertheless, after its IPO, its stock price soared by 190% at one point.

Similarly, Nebius, previously part of Russian Yandex, pivoted to AI cloud services after a split. In Q1 2026, it reported a revenue of 399 million dollars, a year-on-year increase of 684%, but it still had a net loss of 100 million dollars after adjustments. Over the past 12 months, its stock price rose over 510%.

Shifting the focus back to the Chinese market.

Zhi Pu's total revenue for 2025 is 724 million yuan, roughly 100 million dollars, but its net loss is 3.182 billion yuan, 4.4 times its revenue. In other words, for every 1 yuan it earns, it spends far more than 1 yuan on computing power and R&D. Similarly, the Hong Kong-listed AI stock MiniMax, which IPO'd at the same time, saw its stock price rise by 109% on the first day, and its subsequent gains once exceeded 700%. Its total revenue for the year was 79.038 million dollars, approximately 560 million yuan, less than Zhi Pu.

Likewise, Hong Kong's GPU company Birran Technology and A-share domestic GPU company Muxi, alongside the sci-tech innovation board company Mohr Thread, saw first-day increases of 120%, 693%, and 425% respectively. These new shares with astonishing increases are similarly in a state of severe losses or non-profitability.

If we assess these companies using PE, many do not even meet the prerequisite for calculation since their profits are negative. Using PS, Zhi Pu has over 1200 times, while SpaceX about 95 times. Using DCF, with little change in the discount rate and terminal growth rate, the conclusion could shift from 100 billion to 10 billion, with model sensitivity becoming so high that it loses guiding significance. Aswath Damodaran, the author of the DCF textbook, assessed SpaceX's valuation at 1.2 trillion dollars, 30% lower than the IPO pricing. He himself admitted that slight parameter adjustments when handling this generation of IPOs lead to severe fluctuations in results.

Some might argue that in the early days of the internet, investors also did not look at PE; Amazon took twenty years to turn a profit, which is not something new. True, but a key difference between this round and the internet era is: the market is not even using alternative indicators to price; it is trading on pure narratives.

Investors in the internet era, although not looking at PE, still focused on user growth, GMV, and page views; essentially using a set of quantifiable intermediate indicators to anchor valuations. Today's AI companies also have metrics like ARR, but ARR does not explain Zhi Pu's 1200 times sales ratio. The frenzy around the supply chain has long since shed the gravitational pull of basic financial reports and priced all future expectations for the next three to five years into the present.

The old pricing framework is beginning to fail in the face of a new class of assets. The global financial markets and the investment logic of investors have also undergone significant changes.

Model weights, algorithm capabilities, developer ecosystems, and computing power scheduling capabilities are the true core assets of AI companies, but none can be recorded on a balance sheet. The programming ability of GLM-5.2 made Vercel's CEO say "almost shocked," but this statement will not show up in Zhi Pu's income statement. CoreWeave sits on a backlog of 100 billion dollars in orders, but that does not change the fact of its quarterly net loss. NVIDIA's GPUs are dubbed the oil of the AI era, but oil pricing has never been solely based on current production; it also considers reserves, demand curves, and geopolitics.

The core assumption of traditional pricing methods is: future cash flows can be extrapolated from historical financial data. This assumption works very well in industries like consumer goods, finance, and real estate.

However, the revenue curve of AI companies is not linearly extrapolated. It depends on the sudden changes in model capabilities, network effects within open-source ecosystems, and abrupt shifts in policies and industrial cycles. After the release of GLM-5.2, Zhi Pu's narrative status could change overnight; the open-source Llama rapidly expanded Meta's AI influence; the US-China chip restrictions transformed Birran and Muxi from marginal companies into leaders of "domestic alternatives." These variables are difficult to embed in any financial model in advance.

Meanwhile, the market's tolerance for narrative dominance is also rising, as over the past few years, those who believe in narratives have indeed made money.

In early 2023, those who bought NVIDIA without looking at financial reports made ten times their investment. In early 2026, those who bought Zhi Pu without looking at financial reports made 24 times. When a "wrong" method consistently produces "correct" results, the market corrects its methodology rather than the outcomes.

The Money Supporting High Market Value Is, in Fact, Not Much

A study conducted by Nasdaq reviewed data from 1980 to 2020: in the 1980s, the average public float of US IPOs was about 30% of total share capital. By 2020, this number had dropped to about 20%.

J.P. Morgan provided a more macro figure in a report from June 2026: newly issued IPO stocks, along with the shares of early investors allowed to be sold after lock-up, account for only about 1% of total market capitalization.

The circulation of IPOs is getting smaller. This has been an ongoing trend for almost thirty years.

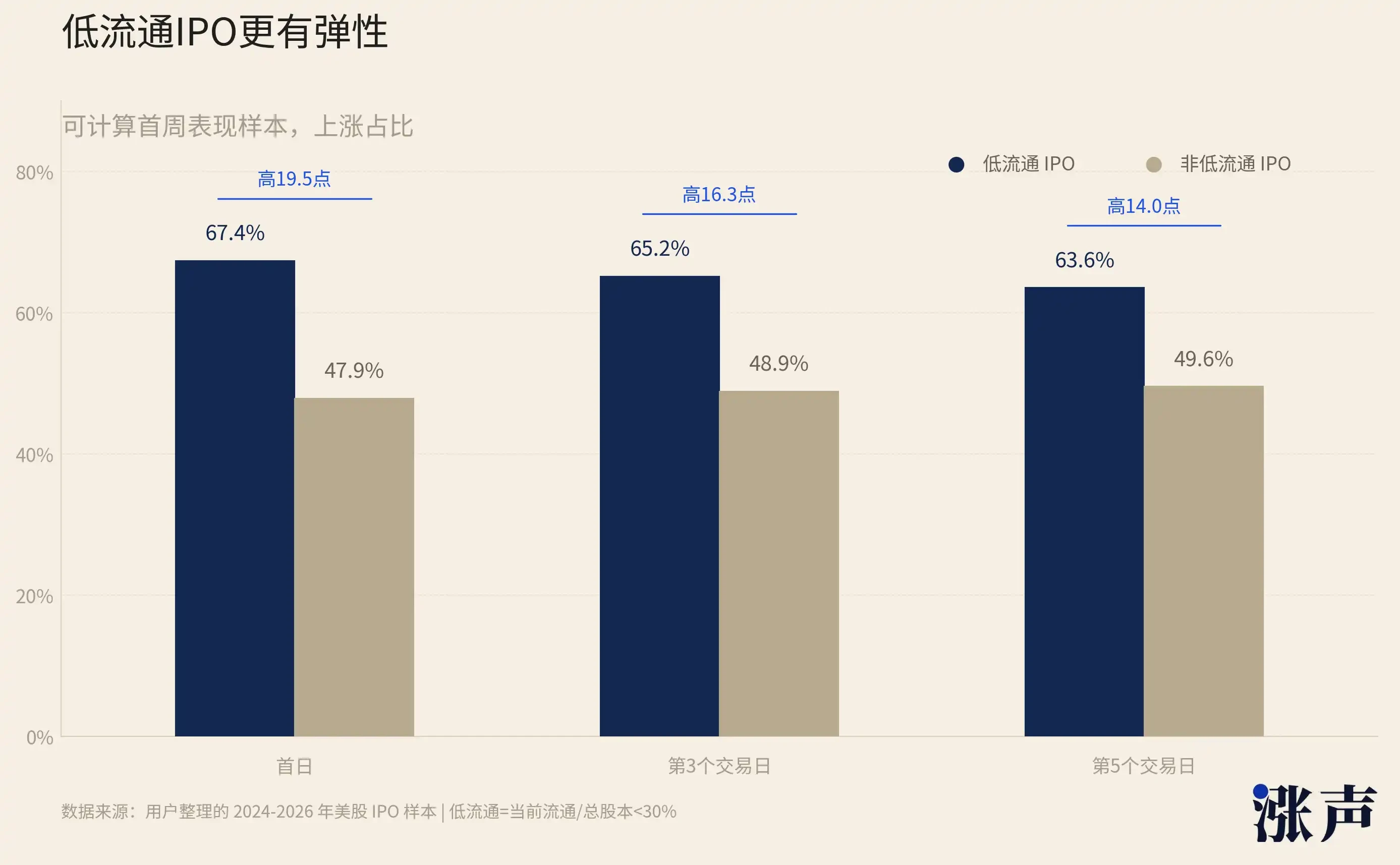

Nasdaq also found a clear inverse relationship between float and the first-day increase. In the years with smaller floats, the first-day increases were larger.

Our own analysis of the 2024-2026 US IPO sample shows the same characteristic. Defining low float as "current float / total share capital below 30%", in the samples that could calculate the performance of the first week, 67.4% of low float IPOs rose on the first day, 65.2% remained up on the third trading day, and 63.6% still rose on the fifth trading day.

The corresponding ratios for non-low float IPOs were only 47.9%, 48.9%, and 49.6%.

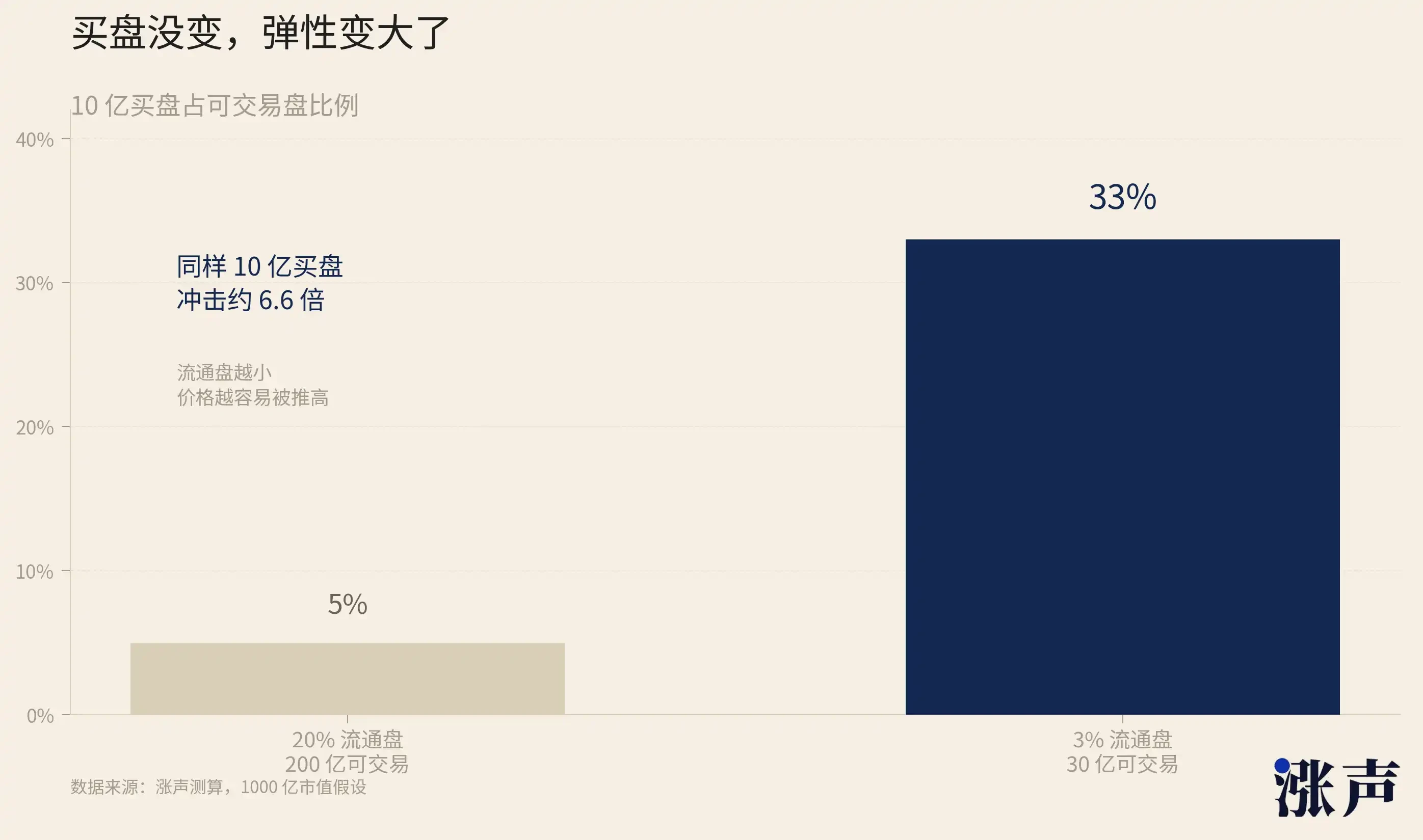

With fewer tradable chips, the same buying pressure leads to a greater impact, resulting in a stronger price elasticity.

The reasoning is straightforward. The same one billion in buy orders incurs a ripple in a 20 billion float but creates a tsunami in a 3 billion float. A float shrinking from 20% to 3% is not a linear change; it is a qualitative transformation in price elasticity.

Newly listed companies are increasingly inclined towards low circulation as this is the result of maximizing the interests of all parties.

Let's start with the founders. The smaller the float, the more secure the control. Elon Musk of SpaceX controls about 85% of the voting rights through Class B shares, and the public market's 4.3% float means external investors have almost no governance influence. He can simultaneously serve as CEO, CTO, and Chairman, merge xAI into SpaceX without shareholder approval, and completely hold the company's strategic direction in his hands. A smaller float weakens the voices of external shareholders, granting the founder greater flexibility.

Scarcity also directly increases market value figures. A company’s market value is not determined by all its shares but by the last transaction price multiplied by the total share capital. If only 3% of the chips are trading, and this 3% is pushed to a ridiculously high price, the entire company's market value is calculated based on this price.

The 97% of shares held by founders and early shareholders that are not traded have their book value inflated accordingly. This inflated market value can be used for financing, mergers, and attracting talent. SpaceX's listing at a valuation of 1.77 trillion dollars will appear in all job postings and negotiation tables.

This phenomenon is not limited to small-cap stocks.

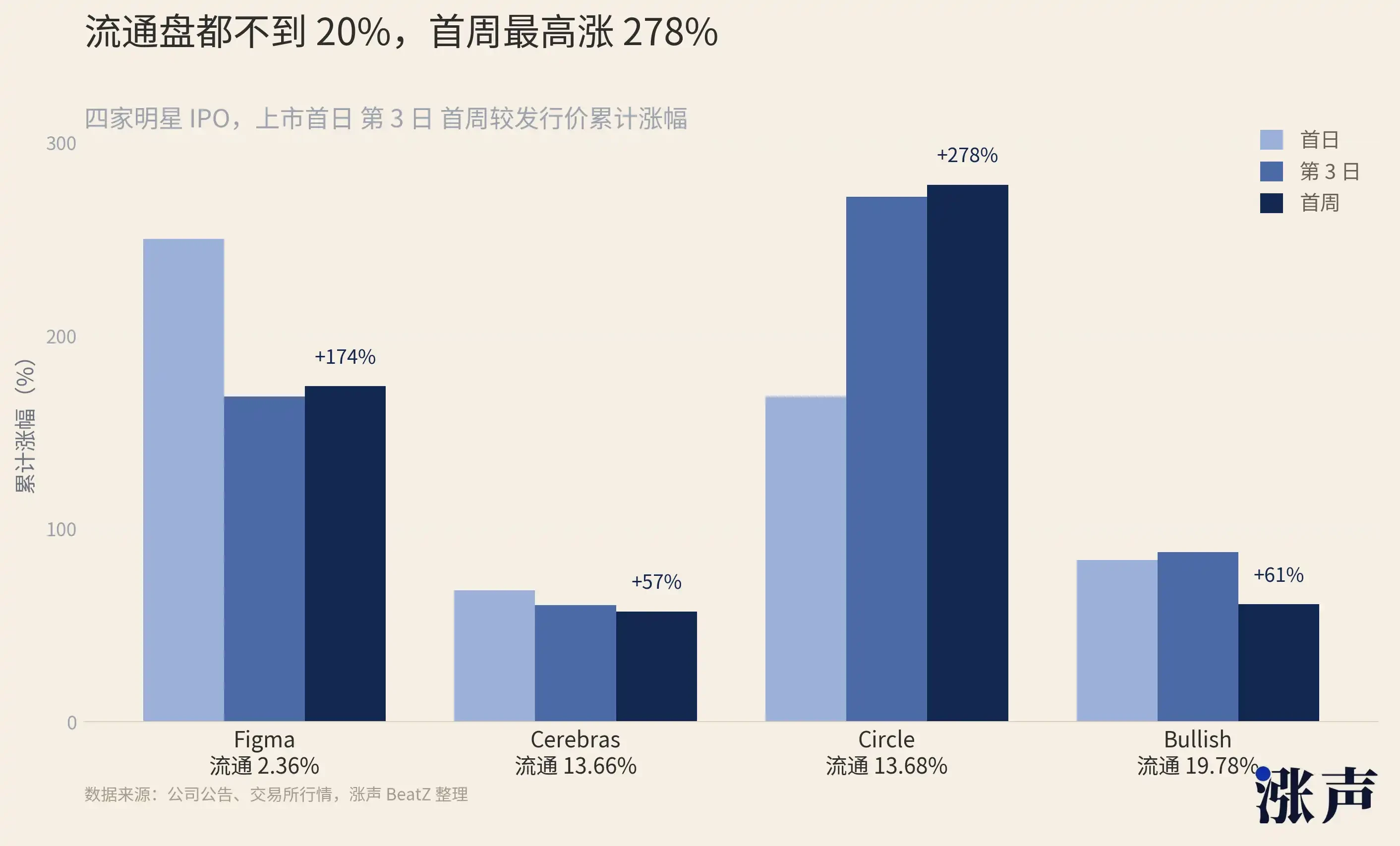

Figma (FIG) is a collaborative design software platform with only 2.36% of its shares circulated at listing, experiencing a 250% increase on the first day, 168.48% on the third day, and 173.7% in a week.

Circle (CRCL) is the stablecoin and blockchain financial infrastructure company behind USDC, with a circulation of 13.68% at listing, rising 168.48% on the first day, 271.77% on the third day, and 278.06% in a week.

Bullish (BLSH) is a digital asset trading platform and market infrastructure company, with a circulation of 19.78% at listing, rising 83.78% on the first day, 87.95% on the third day, and 60.84% in a week.

Cerebras (CBRS) is an AI computing infrastructure company with 13.66% circulated at listing, rising 68.15% on the first day, 60.35% on the third day, and 57.13% in a week.

Then we look at investment banks. The "first-day increase" of an IPO is the core indicator of underwriting success. Media headlines, client evaluations, and investment bank reputations are all linked to this figure. The smaller the float, the easier it is to achieve a larger first-day increase. Goldman Sachs designed a 4.3% float for SpaceX, which rose 19% on the first day; everyone called it a great IPO. If the float were 20%, the same scale of buying pressure spread over five times the chips might only cause a 4% rise, which would lead to a completely different media headline.

The incentive structure of investment banks is inherently biased towards low circulation—smaller floats lead to better first-day increases and enhance the banks' reputations.

Next are cornerstone investors. The cornerstone system in Hong Kong stocks is essentially a deal: "I help you lock the chips, you guarantee me allocation." The interest of cornerstone investors is to secure guaranteed IPO shares (without worrying about being scaled back or participating in a lottery), at the cost of being unable to sell for 6 months. However, this cost often turns into a reward—because cornerstone investors lock in most of the float, the remaining tradable shares are very few, making it easy for the stock price to be pushed up.

After the 6-month lock-up period, if the stock price has already risen several times due to low circulation, the returns for cornerstones far exceed normal IPOs. The cornerstone system ties "helping the company lock chips" with "making more money" together, aligning the interests of both parties completely.

Zhi Pu's eleven cornerstone investors (such as Gao Yi Asset, Taikang Life, Guangfa Fund, etc.) took 70% of the already limited circulating shares, resulting in a final circulating share of less than 4%. All locked for 6 months. While helping Zhi Pu lock its float, they were also creating scarcity premiums for themselves.

Thus, we can even see a systematic turning point from the Nasdaq trading platform, abolishing the 10% minimum public holding threshold.

This rule had existed for several decades. A listed company was required to have at least 10% of its shares publicly traded to ensure sufficient market liquidity and protect the interests of public investors. The S&P 500 is stricter, requiring a minimum public holding ratio for constituent stocks, and MSCI requires 15%. The Russell series requires 5%.

This precedent has far-reaching effects. If Nasdaq can abolish the 10% threshold for SpaceX, what obstacles could a company wishing to go public with a 3% float face? If the largest trading platform in the US deems low circulation acceptable, will other trading platforms follow suit? The cornerstone system of the Hong Kong Stock Exchange already allows locking a large part of IPO chips; if Nasdaq also loosens its rules, could there arise a global competition where trading platforms compete to be friendlier towards low circulation to attract the best IPO candidates?

Primary Investment, Secondary Hedging: Stock Markets Begin to Replicate Old Cryptocurrency Tactics

In the 1990s, after the options market matured, zero-cost collars became standard for the wealthy. You hold a stock, buy a put option to protect against downside (which costs money), while simultaneously selling a call option to recoup that cost (which brings in money). This balanced approach allows you to lock in a price range without spending money. Michael Dell used a variable prepaid forward to cash out part of his Dell shares at the end of the 1990s, triggering no tax and without reducing his holdings, but he received cash upfront.

But previously, this was used only by a few super-rich and founders; now, following SpaceX's listing, wealth management firms publicly promoted this scheme to thousands of employees, creating a scale never seen before. Wealth managers like Bernstein and Mercer now provide guidance to SpaceX employees on how to implement collars, indicating a level of dissemination unheard of in the past.

Bernstein's report includes a set of very sober data. It reviewed every US IPO raising over 50 million dollars in the past decade and found that, after the lock-up period ended, the median return was a drop of about 10%. One-tenth of IPOs fell by at least 62% within six months of unlocking. The conclusion is straightforward: if you are a SpaceX employee holding shares locked up, statistically, by the time you can sell, the price is highly likely to be lower than it is now. Therefore, you should lock in profits using derivatives before the lock-up ends.

Michael Burry, the one who made hundreds of millions betting against the US subprime market in 2008, publicly stated after SpaceX's listing that he had researched put options for shorting but found the prices too high to bear, ultimately not going long or short. Even the "big short" found the cost of shorting too high, indicating that too many people are trying the same trade, driving option prices to absurd levels.

In addition to these techniques, whether collars or pairs trading or lock-up arbitrage, there's a common prerequisite: the company is already publicly listed. The stock has a public market price, the options chain is out, and the shorting mechanism is established.

But if you have spent a few years in the cryptocurrency market, you may find these changes not new at all.

In 2024, Binance Research, the largest trading platform in the crypto market, issued a report titled "Low Float & High FDV: How Did We Get Here?". The report listed a group of tokens that had just launched, with the lowest circulation being only 6% of total supply, and the highest still not exceeding 20%.

In 2024, newly issued tokens had the lowest market value to fully diluted valuation ratio of the past three years. By releasing only a tiny fraction of chips at launch, valuations soared into the stratosphere. These projects rely on extremely low tradable chips to drive prices up at launch, seeming to reach market values that match those of Layer-1 and DeFi blue chips that have been around for years. But once the unlock happens, prices plummet down.

This is the lesson that the cryptocurrency market has imparted to everyone over the course of two years: low circulation can push prices up, but it cannot sustain them. Because locked-in shares will eventually unlock, and unlocking means supply; if the supply doesn’t correspond with demand, prices will drop. Binance Research has calculated that from 2024 to 2030, approximately 155 billion dollars in tokens are expected to unlock gradually. To maintain the current prices of these tokens, the market needs an additional injection of 80 billion dollars in buyer liquidity.

Data compiled by Memento Research indicates that in 2025, 118 major token issuance events (TGE) are expected, with 100 of them, or 84.7%, currently priced below their fully diluted valuations at launch. The median decline is 71%.

CryptoRank's year-end summary for 2025 states plainly: "The low float, high FDV token issuance model continues to impede the arrival of the altcoin season, as most of the upside has been taken by private placements and early investors, leaving very limited opportunities for the public market."

The pricing formation mechanism of low float tokens in the cryptocurrency market and low float IPOs in traditional finance is almost entirely the same: a small number of chips, a large amount of narrative, buying demand far exceeds tradable supply, and prices are pushed far beyond fundamental levels.

So, will the downturn in cryptocurrency altcoins reappear in the stock market?

Not necessarily. After all, the stock market has indices and passive funds providing continuous buying pressure, deeper institutional participation, and more diverse funding sources. These are structural supports not present in the cryptocurrency market. This allows low float IPOs in the stock market to potentially rise for several months.

Of course, the stock market cannot escape the eventual unlock day.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。