Original author: Dong Jing

Original source: Wall Street Insights

Morgan Stanley's latest interpretation of Kioxia's annual report reveals a "super cycle" brewing in the storage industry.

On June 25, according to news from Chase Trading Desk, the core conclusion of Morgan Stanley's latest research report points to one signal: the super cycle in the storage industry is accelerating realization, consumer electronics giants are panic buying, and upstream manufacturers are crazily stockpiling raw materials. Kioxia's annual report data is the clearest annotation of this cycle.

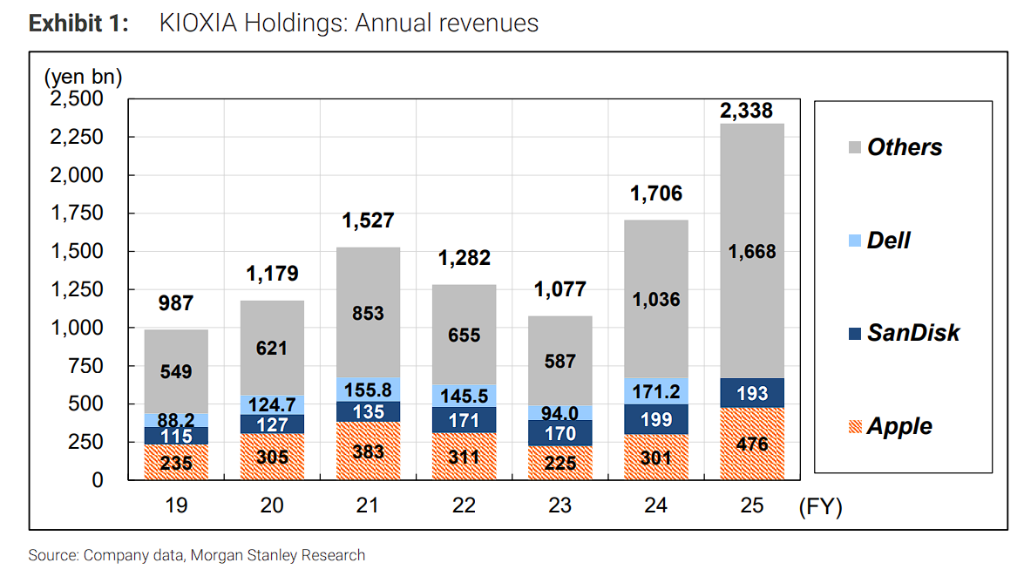

The report states that Apple's revenue contribution skyrocketed by 58% year-on-year to 476 billion yen, far exceeding Kioxia's overall growth rate, which not only indicates that consumer storage prices have risen significantly, but also suggests that major customers are "stockpiling in advance" before price increases.

Meanwhile, as of the end of March 2026, Kioxia's raw materials inventory surged, mainly for early procurement of DRAM needed for SSDs, confirming the tight supply expectations upstream in the industry chain. In addition, the company's capital expenditures are shifting from factory construction to investments in front-end equipment such as BiCS-8.

Morgan Stanley maintains Kioxia's "Overweight" rating with a target price of 110,000 yen, noting that AI-driven demand and strong free cash flow will provide solid support for the stock price.

Apple's orders surge 58%, consumer giants initiate "stockpiling in advance" mode

The most notable highlight of the annual report data is the drastic differentiation in orders from major customers.

For the fiscal year ending March 2026, annual revenue from Apple reached 476 billion yen, a year-on-year increase of 58%. This growth rate not only significantly outpaces the company's overall revenue growth rate (+37%) but also exceeds the overall growth rates for SSDs and storage businesses (+40%).

Morgan Stanley believes that this data supports two important judgments:

- First, storage price increases in the March 2026 quarter have spread to the consumer end. Previously, the market focused on storage demand driven by data center customers, but the rapid growth of Apple orders indicates that the consumer electronics sector has also experienced substantial price increases, and Kioxia has implemented significant price increases for consumer clients.

- Second, Apple is likely engaging in advance stockpiling. Against the backdrop of continuous expectations for rising storage prices, Apple may have conducted advance procurement of components (pull-in procurement) to secure lower costs or ensure supply security. This behavior itself directly reflects the "stockpiling in advance" logic of the entire industry chain.

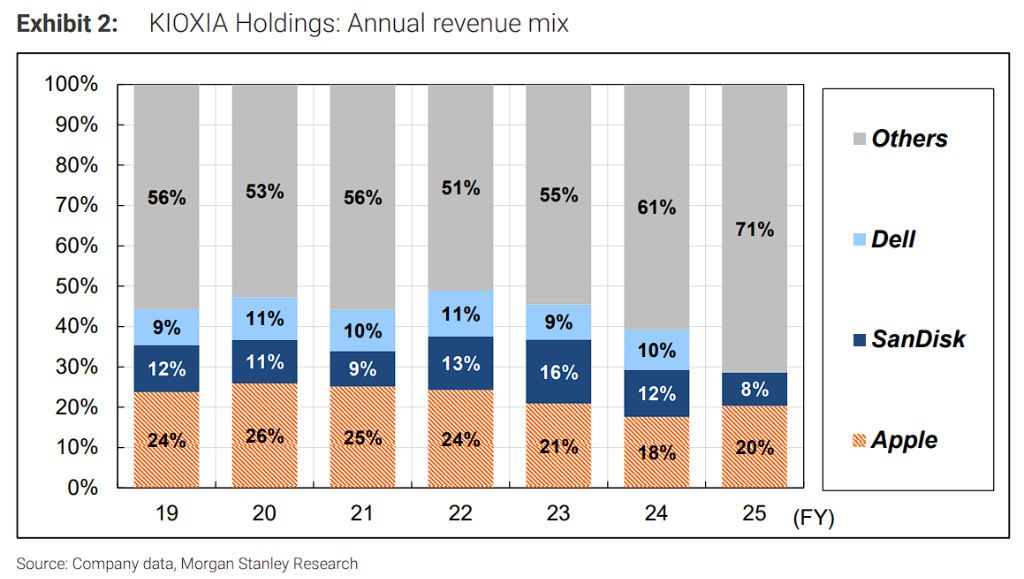

Historically, Apple's share of Kioxia's revenue has risen from about 18% in the fiscal year ending March 2024 to about 20% in the current fiscal year, with absolute amounts increasing dramatically from around 301 billion yen to 476 billion yen.

It is noteworthy that two major clients previously disclosed in the annual report for the fiscal year ending March 2025—SanDisk and Dell—are no longer separately listed in this annual report due to their revenue contributions falling below the 10% threshold. SanDisk's revenue has been disclosed in the quarterly report as 193.4 billion yen (year-on-year -3%).

Raw materials inventory surges: the entire industry chain is stockpiling in advance for the next price increase

Morgan Stanley believes that Kioxia's annual report inventory data reveals another key signal.

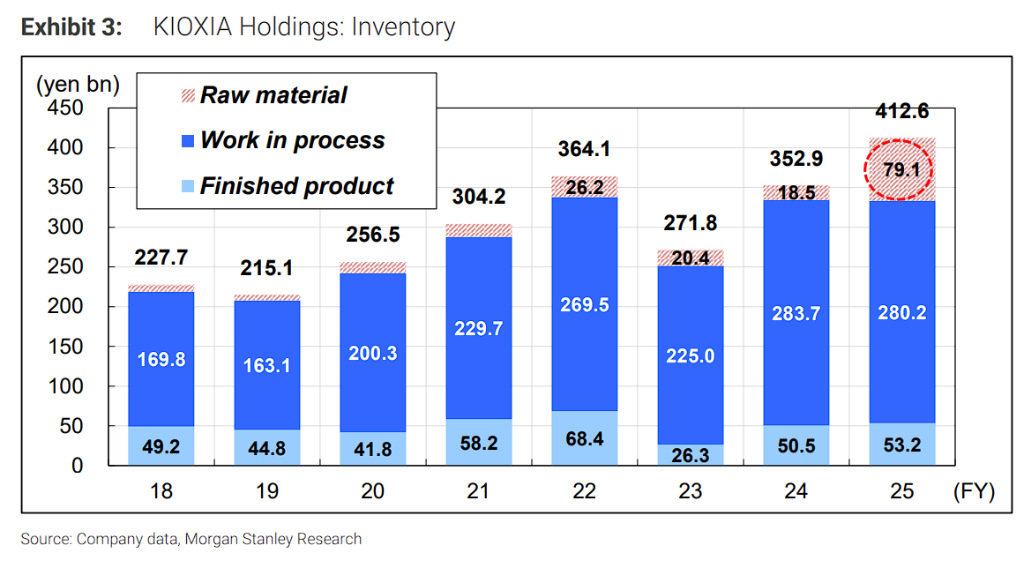

As of the end of March 2026, Kioxia's finished goods and work-in-progress inventories remained basically flat compared to the previous year, but raw materials inventory saw a significant increase.

Morgan Stanley assesses that this change likely stems from the advance procurement of DRAM for SSDs. DRAM is an important raw material for SSD production, and locking in the supply of raw materials in an upward price cycle is a rational choice for manufacturers.

This change in inventory structure corresponds with Apple's advance stockpiling behavior—from end-brand manufacturers to storage manufacturers, the entire industry chain is strategically positioning itself in advance, betting on continuous increases in storage prices.

In terms of total inventory, Kioxia's total inventory reached 412.6 billion yen at the end of the fiscal year ending March 2026, further increasing from 352.9 billion yen in the fiscal year ending March 2025, with raw materials inventory showing the most significant growth.

Capital expenditure structure shifts: from "building factories" to "installing equipment," BiCS-8 mass production accelerates

The report indicates that Kioxia's capital expenditure structure has undergone a significant transformation this fiscal year, reflecting the company's shift from the capacity construction phase to the stage of equipment investment and mass production ramp-up.

FY3/25 (last fiscal year): Within tangible fixed assets, the transfer amount for construction and building works was 109.9 billion yen, while the transfer amount for machinery and equipment was 192.7 billion yen, indicating the company made large-scale investments in factory and infrastructure projects like the Kitakami factory.

FY3/26 (current fiscal year): The transfer amount for construction and buildings plummeted to 6.2 billion yen, while the transfer amount for machinery and equipment surged to 259.8 billion yen. Morgan Stanley believes this indicates that the focus of capital expenditure has clearly shifted to the front-end wafer manufacturing equipment for BiCS-8 at the Yokkaichi and Kitakami factories.

Looking ahead to FY3/27 (next fiscal year), Kioxia plans capital expenditures to reach 450 billion yen, an increase of 166 billion yen year-on-year. Morgan Stanley assesses that while there may be cleanroom construction investments within existing factories, the main direction will still focus on investments in front-end equipment for BiCS-8 and BiCS-10.

This clear capital expenditure path indicates that Kioxia is fully advancing the construction of mass production capabilities for the next-generation NAND flash technology to prepare for the upcoming demand peak.

Morgan Stanley maintains an "Overweight" rating on Kioxia, setting a target price of 110,000 yen, about 19% upside potential relative to the current stock price (as of June 23, 2026, closing price of around 92,290 yen), and has listed Kioxia as a Top Pick in the Japanese semiconductor sector.

Morgan Stanley uses An expected free cash flow (FCF) yield of about 10% for FY3/28 as a valuation anchor, believing this level can provide ample support for the stock price. The implied price-to-earnings ratio based on the FY3/28 EPS forecast is 11 times.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。