Original Author: Zhao Ying

Original Source: Wall Street Journal

The South Korean stock market is experiencing a rare structural rupture in funding: foreign capital is net selling at a record pace, while retail investors are buying with an equivalent amount of funds. The hedging of these two forces is shaping the unique ecology of the most volatile market in Asia against the backdrop of a fundamental rise driven by the AI wave.

According to the Wind Trading Desk, the latest South Korea stock strategy report released by JPMorgan Chase on June 25 states that foreign capital has net flowed out approximately $95 billion from the South Korean stock market this year, likely breaking the annual foreign capital outflow record for any single Asian market. Meanwhile, retail investors (including local ETF purchases) have accumulated a net buying scale of about $80 billion this year, becoming the main support for the market.

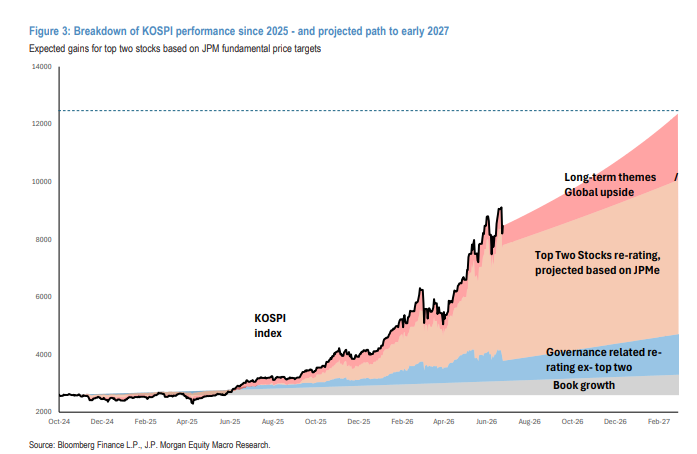

JPMorgan maintains a bullish stance on the South Korean stock market, raising the KOSPI target scenarios for the next 12 months to 12,500 / 15,000 / 8,000 points for the baseline / optimistic / pessimistic scenarios, respectively, and recommends that investors increase positions during any pullbacks to maintain maximum exposure.

The aforementioned funding game pattern will not reverse in the short term, but the upward trend in fundamentals driven by AI, the national wealth effect brought about by corporate profit growth, and the potential for valuation recovery through corporate governance reforms still constitute the core bullish logic for the South Korean stock market. South Korea remains JPMorgan's most favored market in Asia.

Foreign Capital Forced to Sell: Scale Constraints Trigger Involuntary Selling

The outflow of foreign capital from South Korea is classified as "involuntary" (non-discretionary), rather than actively bearish. The core reason is that the market capitalization of the two storage chip giants, represented by Samsung Electronics and SK Hynix, has sharply inflated, reaching the holding limits for emerging market (EM) long-term funds. This scale constraint affects about 10% of foreign holdings in both stocks, forcing fund managers to continuously reduce positions as share prices rise.

Data shows that over 90% of the total foreign capital outflow this year comes from the aforementioned two storage stocks. This structural characteristic means that as long as the storage stocks continue to outperform the regional benchmark, the benchmark constraints for EM funds will not disappear, and the pressure of foreign capital outflow will persist.

It is worth noting that despite the continuous net selling by foreign capital, the proportion of foreign holdings in South Korean stocks has actually increased significantly since the beginning of the year—the reason being that the rise in share prices far exceeds the scale of selling. Currently, the two major storage stocks account for more than two-thirds of foreign holdings in South Korea. In contrast, global funds (non-EM specific) are significantly underweight in Korea; many large real fund accounts reflect insufficient exposure to South Korea and have a demand for positioning.

Leverage ETF Expansion: Structural Increase in Volatility

The abnormal surge in the volatility of the South Korean market is closely related to the explosive growth of leveraged ETFs both domestically and abroad. The scale (AUM) of leveraged ETFs targeting South Korean assets has increased to $50 billion, with most of the increase coming from the market's own rise.

These ETFs primarily achieve exposure through index futures and some spot and options, driving a substantial rise in individual stock futures outstanding contracts. At the same time, the demand for "crash protection" from ETFs has also pushed up implied volatility—the ratio of VKOSPI to VIX is currently close to 5 times, while the historical normal level is about 1 time. The scale of the Gamma imbalance related to leveraged ETFs has now exceeded $1 billion, significantly amplifying both upward and downward market volatility.

Moreover, the South Korean exchange and clearinghouse have raised capital requirements in response to higher trading volumes, leading to increased financing costs for large-cap stocks, and some brokers are also facing difficulties in managing concentrated exposures. Given the widespread adoption of such tools both domestically and abroad, the scale of leveraged ETFs will not materially shrink in the short term, and high volatility will become a normative feature of the South Korean market structure.

Retail Investors Taking Over: Space Remains, Leverage Risk Manageable

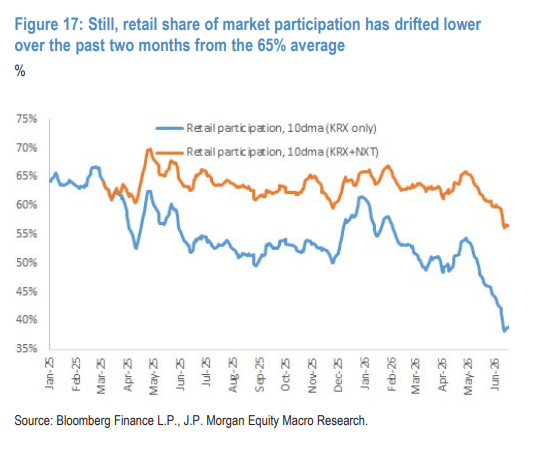

In the context of continuous outflow of foreign capital and institutional investors (pensions) reducing positions at highs for rebalancing, retail investors have become the main buyers in the South Korean stock market. Data shows that if trading through the NXT platform and ETF purchases are included, the net buying scale by retail investors this year has reached about $80 billion.

There is still room for retail buying, for three reasons: first, although the financing balance and leverage levels in options trading have risen, they remain relatively low compared to the overall market capitalization and customer deposits; second, South Korean retail investors have just begun to bring overseas stock holdings back to the domestic market, providing a large area for repatriation; third, as income grows and the wealth effect from stocks continues to ferment, residents' willingness to invest in stocks is expected to further increase, especially against the backdrop of limited real estate investments.

However, the proportion of retail investors in market transactions has declined from an average of 65% over the past two months, while pension participation has increased. Nevertheless, pensions still overall are net sellers to maintain targeted portfolio weights.

AI Narrative Disturbance: Cyclical Volatility Does Not Change Upward Trend

The fundamentals of the South Korean market are highly tied to the AI cycle, which is currently still on a strong upward trajectory. Analysts maintain a constructive judgment on the storage cycle of "high levels sustained longer" and believe that the earnings of South Korean tech stocks have higher elasticity compared to similar global stocks.

However, the periodic disturbances of the AI narrative are unavoidable. JPMorgan listed five major factors that have recently caused market volatility: first, there are signs at the user level of optimization reducing token consumption, raising concerns about token pricing; second, GLM 5.2 from China's Zhipu AI received a positive market response, reigniting competition concerns; third, recent export control policies have brought policy uncertainty; fourth, ongoing pressures from the supply of stocks and bonds; fifth, the reopening of the Strait of Hormuz may alleviate pressures in related markets and sectors.

As long as the growth rate of capital expenditure in large-scale cloud computing continues to exceed that of semiconductor equipment, the supply-demand imbalance will continue, thus supporting the profit margins of storage chip manufacturers.

The AI earnings of South Korean storage chip companies have grown large enough to have a substantial macro impact. It is estimated that over the next three years, the direct taxes (including corporate income tax) paid by the two major storage companies to the government could easily exceed $350 billion, and when including individual income tax from employee bonuses, the scale would be even larger.

For reference, South Korea's total foreign exchange reserves are currently about $427 billion, and the total government debt is approximately $1 trillion. This wealth effect will provide ample resources for the South Korean government for long-term physical and financial investments, social infrastructure construction, and strategic planning for the AI era.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。