Original Author: Long Yue

Original Source: Wall Street Journal

The customer first pays a deposit of $22 billion, signs an irrevocable long-term contract, and accepts a pricing framework that is far more favorable to Micron than at any historical period—this is the core term of Micron's latest long-term strategic customer agreements (Strategic Customer Agreements, SCA).

According to Wind Transaction Desk news, on June 25, Barclays, Morgan Stanley, and JPMorgan collectively viewed it as a "game-changing" agreement. JPMorgan semiconductor analyst Harlan Sur characterized this batch of SCAs as a "fundamental shift" in Micron's business model—from a cyclical commodity supplier to a long-term supplier protected by multi-year contracts, with significant downside hedging for revenue and profits.

The value of these contracts lies in: first, they cover a substantial amount, with the signed agreements corresponding to about 20% of DRAM and about one-third of NAND; second, they bind price and volume, with 14 agreements calculated based on minimum commitment volume and minimum price corresponding to about $100 billion in cumulative minimum revenue; third, customers are required to provide a total of $22 billion in deposits and financial commitments. Fourth, the gross margin corresponding to the price floor is "far higher than historical peaks" (historical peak around 62%), essentially locking in a higher profit bottom line for Micron.

16 Contracts Covering 20% of DRAM and One-third of NAND

Micron disclosed that it has signed 16 SCAs, with customers spanning three major markets: data centers, consumer electronics, and automotive.

In terms of customer distribution, there are 4 large customers (market speculation generally includes hyperscale cloud providers and major consumer electronics OEMs), 3 medium-sized customers, and the remaining 9 are smaller clients in the automotive sector.

Agreement duration: contracts for data centers and consumer electronics are for 5 years, covering 2026 to 2030; automotive contracts are for 3 years.

Scope of coverage: these 16 agreements together cover about 20% of Micron's DRAM shipments and about one-third of NAND shipments.

According to Barclays’ research report, management indicated that once all planned SCAs are signed, it is expected that over 50% of the company's revenue will come from these agreements. Among them, contracts with fixed prices or price ranges are expected to account for about 40% of company revenue.

$22 Billion Deposit Increases Default Cost: Customers Pay First, Micron Temporarily Holds, Returned at Maturity

Under the 16 signed agreements, Micron will receive a total of about $22 billion in cash deposits and other financial commitments—of which $18 billion is unrestricted cash and $4 billion is letters of credit.

This money is held by Micron, stays on the balance sheet during the contract period, and will be returned to the customers at maturity, with the return timing being "back-end weighted," meaning that large amounts will be returned only in the later part of the agreements.

This money should not simply be viewed as pre-revenue. Its real function is to increase the cost for customers to back out.

Regarding the binding nature of the contracts, Morgan Stanley's report directly cited management's statement during the conference call: "These contracts are non-cancellable." If customers fail to take delivery at the agreed volume and price, Micron can take action on the deposit. For Micron, this effectively amounts to providing a margin for a portion of demand over the coming years; for customers, this is a cost of commitment to supply certainty.

This also explains why customers are willing to accept price ranges and deposit arrangements. Driven by AI servers, data center SSDs, HBM, and high-end terminal demand, when storage supply is tight, locking in volume itself has value.

Pricing Structure: There is an Upper Limit, but the Bottom Price Locks in Gross Margins "Far Above Historical Peaks"

The pricing framework of the SCA is divided into three categories: fixed prices, prices with upper and lower limits, or prices that refer to market prices but fluctuate within a nearby range.

Upper price limit: For existing products, the upper price limit refers to the market price in the second quarter of 2026. This clause has been interpreted by some market participants as Micron "actively locking in the room for price increases," which has caused some controversy.

However, the lower price limit is the real highlight: The gross margin corresponding to the bottom price is "far higher than any profit peak in historical cycles." Micron's past gross margin peak was around 62%, while the current gross margin has reached 84.9%—this means even triggering the bottom price clause, Micron’s profit level still exceeds the historical best periods.

However, the SCA is not a contract where "prices always move up." Some existing products have set price ceilings, with ceilings anchored to the market price in the second quarter of 2026. In other words, Micron traded off some future price increase flexibility for greater revenue certainty and a profit margin bottom line.

Analyst Joseph Moore commented that: "The contract price ceiling being equal to the second quarter price" indeed raised some concerns about "the company's locking in a ceiling," but he also noted that the gross margin is nearing 90% and is expected to remain in that range for a considerable time—seeking some protection in negotiations is reasonable, while the duration of the contract is the core dimension in evaluating its value.

$100 Billion Revenue Bottom Line is Just "The Minimum"

Among the 16 agreements, 14 have explicitly defined price terms.

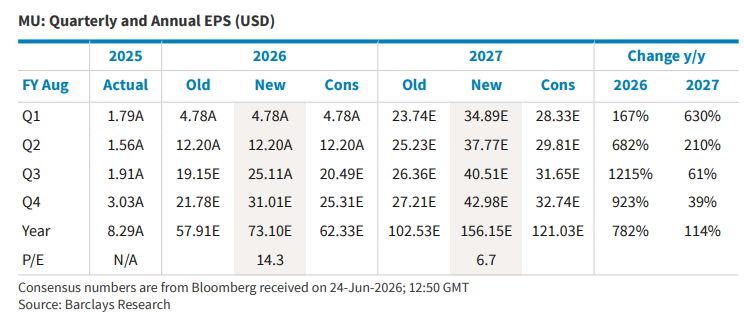

According to Barclays and JPMorgan's research reports, the minimum committed revenue (RPO, which is the remaining performance obligation calculated based on minimum commitment volume and price) of these 14 agreements totals about $100 billion.

Management has clearly stated that actual revenue is expected to "far exceed" this bottom line—because the $100 billion is only the guaranteed minimum based on the bottom price; if the market price exceeds the bottom price, revenue will naturally increase.

For new products, the agreements also reserve additional pricing upside space.

Long-term Agreements Still Require Capacity Expansion; Capital Expenditure has Not Disappeared

Locking in demand does not equal automatic delivery.

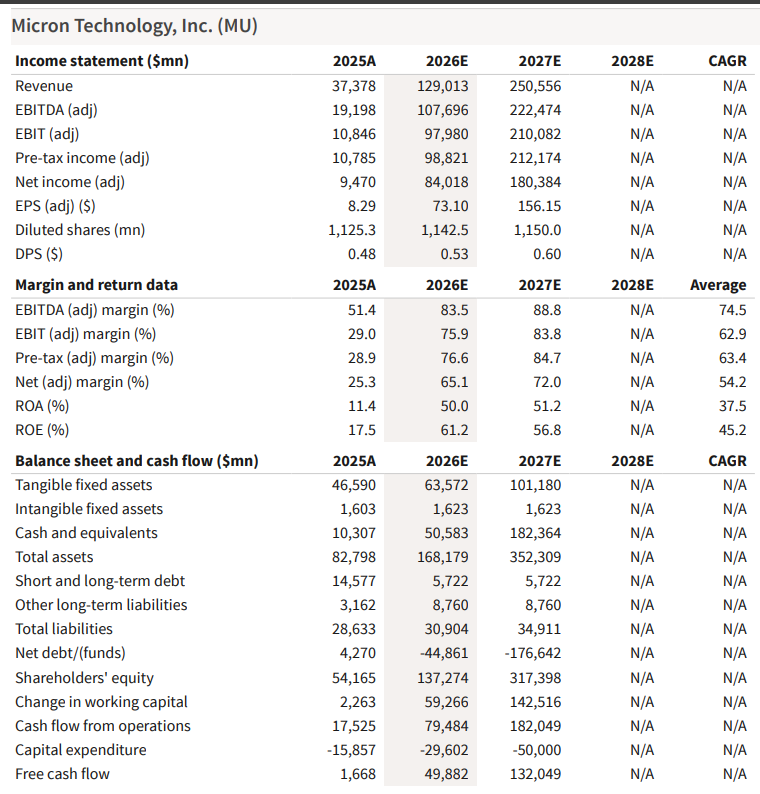

Micron has raised its FY26 net capital expenditure guidance to about $27 billion, from around $25 billion previously. FY27 quarterly capital expenditures are expected to exceed FQ4 levels, with more than half of the year-over-year increase coming from capital expenditures for construction, aimed at preparing cleanroom capacity.

This indicates that the SCA brings not a light asset model, but a more definitive reason for capacity expansion.

Customers are willing to commit money, and Micron must also invest money. Long-term agreements provide more rationale for expansion, but if future demand or prices deviate, capacity investments will still become a cyclical variable.

Three Major Institutions Upgrade Target Prices, Behind which the Market is Reassessing "How Long Peak Profits Can Last"

All three institutions have raised their target prices for Micron, but the logical focus is not merely on the better-than-expected May quarterly financial report.

Barclays (analyst Tom O'Malley): Target price raised from $117.5 to $200, based on 12 times CY27 earnings per share of $166.74. The research report states that SCA details "exceeded expectations" and believes these agreements "have substantial positive significance for protecting downside risks," while supply-demand imbalance will not ease in the short term, still having upside potential.

Morgan Stanley (analyst Joseph Moore): Target price raised from $105 to $120, based on 30 times through-cycle profitability (earnings per share of $40). The research report raised the through-cycle profitability estimate from $35 to $40, reasoning that the earnings run rate is approaching $200 per share.

JPMorgan (analyst Harlan Sur): Target price raised significantly from $55 (target for December 2026) to $154 (target for December 2027), based on 10 times (10-year median P/E ratio) FY28 earnings per share of $15. The research report characterizes SCA expansion as a "step-change," believing it fundamentally alters Micron's business model attributes.

Behind these model changes, the key variable is the sustainability of profits.

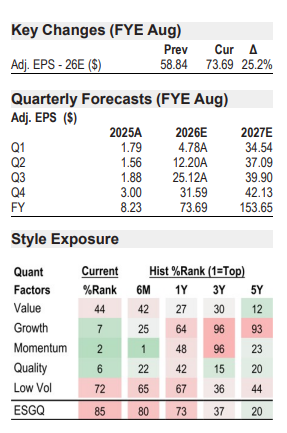

Micron's revenue for the May quarter reached $41.456 billion, a sequential increase of 73.7%; the August quarter revenue guidance midpoint is $50 billion, with non-GAAP EPS guidance midpoint at $3.1. The quarterly figures are already very high, but the SCA presents another question to the market: If prices no longer rise rapidly, can Micron maintain high gross margins and high free cash flow?

The framework currently provides the answer: some revenue has stronger protection, but not all revenue. Price ceilings, future capacity expansions, and the sustainability of AI demand remain boundary conditions.

Deposits and Cash Flow Open Up Expectations for Capital Returns, But Timing is Limited

The SCA also brings a change to the balance sheet: the deposits will enter Micron's hands, although ultimately they must be returned to the customers, but in the short term, this will increase cash size.

As of the May quarter, Micron had about $26 billion in cash and investments; operating cash flow for the quarter was $25.4 billion, and adjusted free cash flow was $18.3 billion. The August quarter is also expected to receive about $10 billion in customer cash deposits.

The path for capital returns is also beginning to clarify. The restrictions associated with the U.S. CHIPS and Science Act have constrained Micron's near-term buyback space; after December 9, 2026, as the restriction window passes, the company's guidance points toward gradually returning 100% of excess cash to shareholders, with buybacks being the primary method.

This portion is not a direct contribution to SCA's revenue, but it is another facet of how SCA changes market narratives: if profits stay high and cash accumulates quickly, Micron will no longer just be "earning cyclical revenue," but may also enter a more stable cash return framework.

The Financial Report Itself: Gross Margin Hits Historical High, Next Quarter Guidance Again Exceeds Expectations

Aside from the SCA, Micron's financial report data for the May quarter (FY3Q26) is also strong:

- Revenue of $41.456 billion, sequential growth of 73.7%, significantly exceeding the market expectation of $35.6 billion

- DRAM revenue of $31.3 billion (sequential growth +67%), NAND revenue of $9.9 billion (sequential growth +99%)

- Average price of DRAM increased by about 60% over the previous quarter, average price of NAND increased by about 80% mid-range over the previous quarter

- Gross margin of 84.9%, hitting a historical high, above the market expectation of about 81.8%-81.9%

- EPS of $2.511-$2.512, significantly exceeding the market expectation of about $2.049

Guidance for the August quarter (FY4Q26):

- Revenue guidance of $50 billion (midpoint), above market expectation of about $43.1-43.6 billion

- Gross margin guidance of about 86%, continuing to be above market expectations

- EPS guidance of $3.10 (midpoint), above market expectation of about $2.531-2.572

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。