Buying back STRC is superior to increasing Bitcoin holdings.

Author: Khing Oei

Translated by: Chopper, Foresight News

Recently, MSTR and STRC markets have experienced significant volatility. Let’s set aside short-term fluctuations and return to the underlying logic: Bitcoin reserve companies are essentially entities holding a single leveraged asset, and their business model is closer to that of banks rather than software technology companies.

From a valuation logic perspective, the market will never price a bank solely based on total assets. A bank's loan assets are prioritized for repayment to deposit customers and bondholders, while common shareholders only enjoy residual rights. Therefore, the core valuation metric for banks is the price-to-book ratio, which is the value of shareholders' equity after deducting priority debt from total assets. This is also the primary reference index for analysts at investment banks and brokerage firms.

The price-to-book ratio for Bitcoin reserve companies is mNAV: it equals the company's market value divided by the net asset value of equity, where net asset value of equity refers to Bitcoin reserves minus debts and preferred stock that are prioritized over common stock. As of yesterday's close, the mNAV value of Strategy was 1.10 times. (Translator's note: The closing data mentioned in this article all refers to data from June 24.) The underlying fundamentals per share are the net Bitcoin value per share—meaning the actual number of Bitcoins held per share after the settlement of priority claims. This corresponds to the book value per share when valued in Bitcoin. The industry's focus—per share Bitcoin growth rate—represents the return on that book value. For a fund management company, this is almost equivalent to a profit metric.

This set of metrics is not something I invented; it simply applies the traditional financial analysis framework of banks to the balance sheet of Bitcoin:

- Value of equity units market value = Price-to-book ratio

- Net Bitcoin holdings per share = Book value per share

- Growth rate of Bitcoin holdings per share = Return on book assets

This is a universal valuation logic applicable to all leveraged financial institutions, perfectly suited for such Bitcoin reserve companies.

Yesterday, MSTR's stock price was $94.13, which is lower than the total net value per Bitcoin of $143.76 per share, resulting in a rough net value multiple of only 0.65 times. Looking solely at this criterion, the stock price is discounted nearly one-third compared to the value of Bitcoin assets, and raising capital by issuing more shares to buy Bitcoin seems to dilute asset value. However, after deducting about 40% of Bitcoin equity occupied by debt and preferred stock, the current stock price is relative to the actual Bitcoin assets held by common stock at 1.1 times. These two calculations yield completely contradictory conclusions, and the bank-style valuation framework is the correct metric, also determining how the company should use newly added funds.

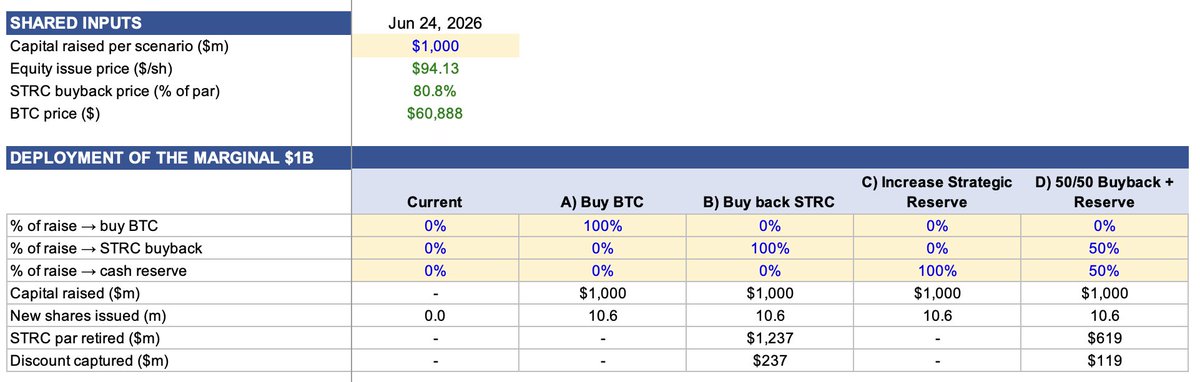

Newly added $1 billion in funds, four paths for usage calculation

Assuming $1 billion in equity is raised at the current stock price, the funds can be allocated in four ways: 1) increase Bitcoin holdings; 2) buy back STRC; 3) expand cash reserves; 4) half buy back STRC and half supplement cash reserves. The issuance price is $94.13; yesterday's closing price for STRC was $80.84, a discount of 19% from par value, with an actual annualized yield of 14.2%. For every $1 invested in buybacks, $1.24 of STRC's par value can be canceled, while avoiding a permanent dividend of 11.5%.

Impact of the four plans on the balance sheet

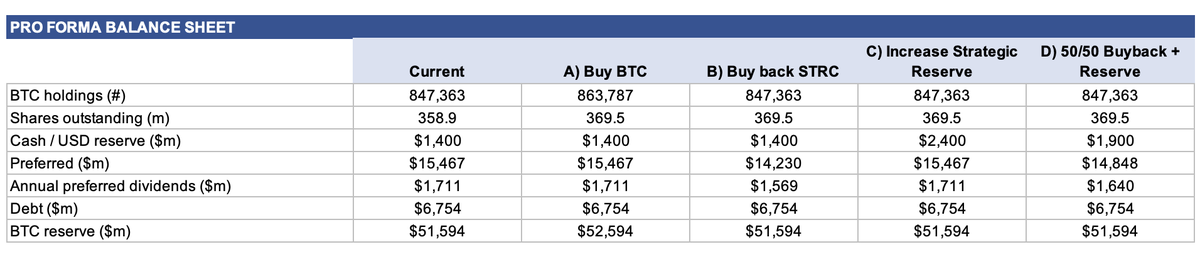

Among the four plans, three will not increase Bitcoin holdings, only adjust the upper priority debt structure:

Buy back STRC: At a discount of 19%, $1 billion can cancel $1.24 billion in par value STRC, reducing annual preferred stock dividends from $1.711 billion to $1.569 billion;

Expand cash reserves: Cash reserves increase from $1.4 billion to $2.4 billion, with dividend payments unchanged;

Fifty-fifty split plan: Cash rises to $1.9 billion, dividend payments decrease to $1.640 billion, canceling $619 million in par value STRC;

Increase Bitcoin holdings: The only option that increases Bitcoin reserves, total holdings rise from 847,363 coins to 863,787 coins, but is also the weakest choice for core metric improvement.

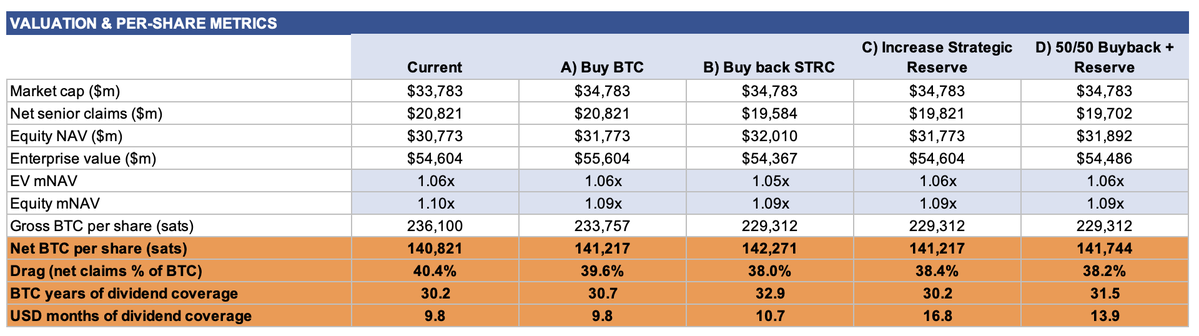

Calculating based on total Bitcoin value per share, all four plans result in dilution. Even if you use the entire $1 billion to purchase Bitcoin, the per share value drops from 236,100 Satoshis to 233,757 Satoshis; in the case of issuing shares without buying any Bitcoin, the per share value drops even further to 229,312 Satoshis. Based on this, you would conclude that the company should do nothing.

However, regarding the net Bitcoin value per share, each option would lead to an increase in value:

- Buy back STRC: Net Bitcoin per share rises to 142,271 Satoshis (+1.0%), debt ratio drops from 40.4% to 38.0%, the effect on restoring the balance sheet is strongest;

- Fifty-fifty split plan: Net Bitcoin per share becomes 141,744 Satoshis, debt ratio 38.2%, significantly enhancing cash debt coverage capability;

- Simply expanding cash reserves or increasing Bitcoin holdings: both yield 141,217 Satoshis, with minimal increase.

Increasing Bitcoin holdings shows the poorest results, and the logic is clear. The issuance price of your stock is 1.1 times the net asset value, while the asset purchase price is 1 time the net asset value. This only slightly increases the net Bitcoin per share yet dilutes the total Bitcoin holding metric that the market focuses on heavily. In contrast, buying back STRC at a discount immediately creates value.

Currently, the most concerning indicator for the market is the number of months cash covers dividends. Strategy’s current cash reserve is $1.4 billion, with annual STRC dividend total at $1.711 billion, cash can only cover 9.8 months of dividends:

- Increasing Bitcoin holdings: Coverage remains at 9.8 months;

- Buying back STRC: Increases to 10.7 months;

- Simply expanding cash reserves: Increases significantly to 16.8 months;

- Fifty-fifty split plan: Increases to 13.9 months.

This is another core indicator in banking: liquidity coverage ratio. In a loose funding cycle, the market pays no attention, but in times of tight financing, it becomes critical for a company’s survival. The fact that STRC broke below par value is a direct signal of tightened market financing channels.

The company's own financial report data also supports this conclusion

The above analysis is not a personal subjective judgment; Strategy’s Q1 financial report provided the same breakeven threshold: According to the company’s internal framework, only when mNAV is above 1.22 times can selling MSTR to increase Bitcoin holdings add to the net Bitcoin per share; at the current 1 times multiple, this action would directly deplete 48 basis points. The company's current EV (enterprise value) stands at 1.06 times, mNAV at 1.10 times, both below its internal breakeven line.

The two core assumptions of the company’s original conventional expansion route have now all failed. If STRC could issue at par value normally and cash reserves could cover 1.5 years of dividends. Nowadays, STRC’s market price is only $81 and cannot be issued at par, while cash reserves cover less than 10 months.

What should Strategy do

In the current valuation range, issue equity and inject new funds into channels that can significantly optimize core financial metrics. Expanding cash reserves and buying back STRC at a discount are two operations that can both increase net Bitcoin per share, reduce debt burden, and restore market concerns over liquidity coverage capacity; the fifty-fifty split plan can simultaneously achieve all these goals.

Continuing to increase Bitcoin holdings now can only optimize the surface indicators that the public is concerned about, while ignoring the core balance sheet risks of the company facing $15 billion in priority debt and tightening financing channels.

Investors only looking at the total Bitcoin holding indicator will overlook the positive feedback logic. Buying back STRC will directly bolster token buying, signaling liquidity safety to the market. After the market's panic subsides, the price of STRC will recover towards the $100 par value; price increase corresponds to yield decrease, the current 14.2% high yield will continue to narrow. A complete positive cycle is thus formed: restoring the balance sheet → STRC price rebound → dividend yield decline → previously closed par issuance channels reopening.

The discount on STRC does not have to be passively waiting for repair; the current deep discount is the lowest cost capital the company can obtain and is also the key to restarting other financing channels.

Judging Bitcoin reserve companies should follow the bank valuation standards: price-to-book ratio, book value per share, and debt repayment ability under pressure.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。