Original Author: Eric, Foresight News

In June 2026, Circle's seemingly bottoming rebound performance was abruptly halted. The circulation of USDC had fallen to 73.6 billion by June 25, US time, a decline of about 7 billion from its peak, while Circle's stock price once halved to around 63 dollars.

It appears that 7 billion is less than 10% of 80 billion. In contrast, USDT's circulation peaked at around 191 billion, and is still about 186.3 billion, only decreasing by 4.7 billion, with a reduction rate of less than 3%.

Although there is no evidence proving that the decline in USDC's circulation is directly related to Circle's stock price drop, their synchronicity, along with the coincidence of previous security incidents in the DeFi sector and the timing of Circle's stock price decline, surprisingly aligns with the view expressed by Compass Point analyst Ed Engel in January this year:

Circle is a barometer for DeFi activity.

Engel believed that Circle’s trading method resembles cyclical stocks, as from October 2025 to January 2026, the correlation coefficient between the USDC circulation curve and ETH price movements reached 0.66. The core reason lies in the fact that 75% of USDC circulates in cryptocurrency exchanges and DeFi protocols, while the portion truly used for daily consumption and cross-border payments is nowhere near as high as imagined.

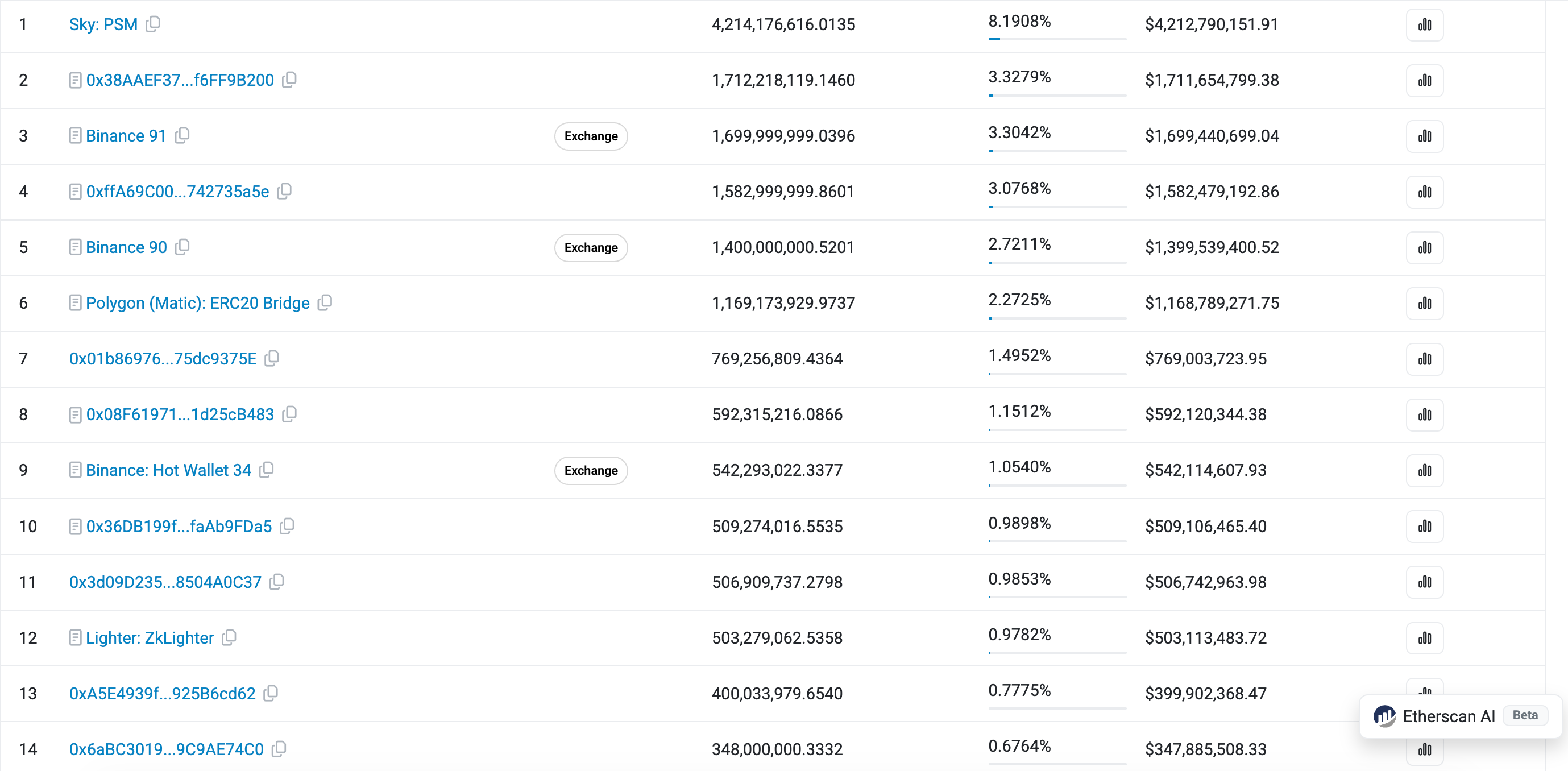

A glance at the Etherscan USDC holding address ranking shows a large number of contract holding addresses on the front page, with these USDC being held in DeFi, multi-signature wallets of exchanges, cross-chain bridges, and other protocols or addresses. Moreover, the top 100 holding addresses for USDC on Ethereum account for more than 50% of USDC, while 0.32% of the holding addresses take away 93.55% of the total amount. A significant amount of USDC is locked in protocols to earn yields higher than bank deposits.

This concentration of data is far from what a "digital dollar" for daily circulation should be. You might argue that USDT has a higher concentration on Ethereum, but in the Web3 industry, USDT is used to pay salaries, in foreign trade to settle payments, and gray and black industries leverage USDT to evade regulation, while third-world countries utilize USDT to protect deposits. These real use cases are quite common.

Although not as "glamorous" as USDC, these scenarios also build the foundation for USDT, allowing it to outperform the more compliant USDC in diminishing market conditions, despite being the stablecoin that should be most used in cryptocurrency trading pairs. Recent reports of the local USDT price in India having an 8% premium over the normal price further support this view.

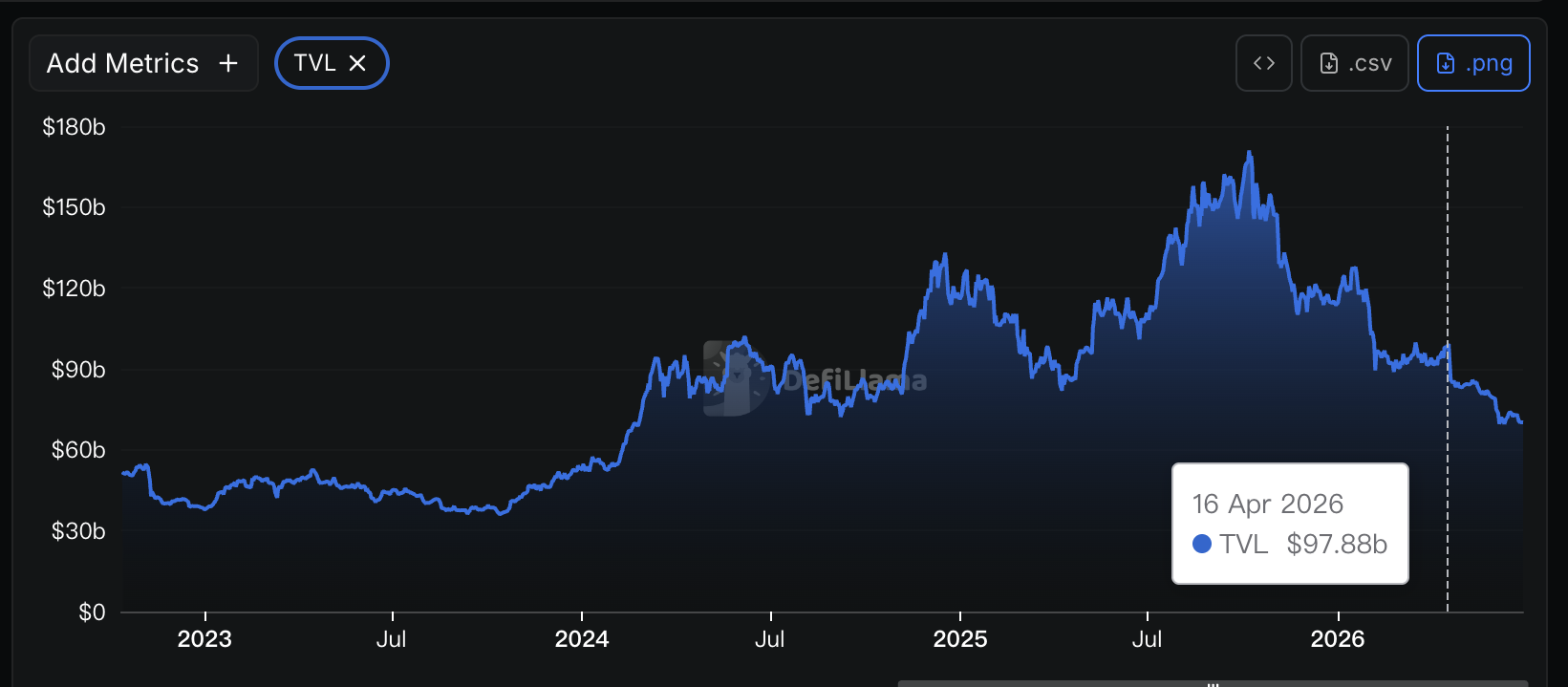

The overall TVL of DeFi has been declining since mid-April, coinciding with the Kelp DAO attack incident, while Circle's stock price started to decline from mid-May. Despite the initial time gap, the subsequent trends are quite similar.

Just last month, Circle and Coinbase jointly pushed USDC to become the settlement stablecoin on Hyperliquid, at the cost of each having to stake 500,000 HYPE and ceding 90% of the revenue generated by the USDC backing reserves on Hyperliquid. This situation, looking like a "triple-win" on the surface, actually reveals Circle's helplessness: the DeFi sector, as the main battleground, has started to shrink rapidly, and the Kelp DAO incident has severely undermined the credibility of DeFi, making it a bottleneck for USDC’s quantity to increase naturally; Circle has to "fend for itself."

If you observe closely, you will find that USDC is not only a settlement asset for Hyperliquid but also for platforms like Lighter. Beyond the cryptocurrency space, Circle is also tirelessly promoting USDC "to be used as dollars." According to Artemis data, the "organic transfer volume" of USDC (excluding wash trading, high-frequency trading, and exchange consolidated wallets) was 18.3 trillion in 2025, while USDT was 13.2 trillion.

It is an undeniable fact that USDC is widely used in institutional and compliant payment scenarios, but the amount of USDC needed in these scenarios is not as high as imagined. The flow of funds may not always occur in the form of USDC, but rather USDC serves as an "intermediate state," reducing the time and capital costs of flow between banks or financial institutions.

In other words, increasing USDC by 10 billion might require the actual increase of several trillion dollars in the real-world fund flow, but on-chain, it could just involve a few large DeFi protocols, meme coin trading platforms, or prediction markets. No matter how quickly USDC circulates in reality or how high its usage rate is, if USDC's issuance cannot increase, revenues and profits will not grow either.

Of course, all of this is not enough to "sentence Circle to death"; if in the future Circle can break free from its reliance on DeFi or prove that actual usage in daily life significantly boosts the issuance growth of USDC, then the investment logic surrounding Circle may be rewritten. However, in the short term, attention may still need to be focused on whether DeFi can overcome the "imbalance of returns and risks" and give the market more confidence.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。