The weak trend in the second quarter was exacerbated by the deterioration of three major demand channels: spot ETFs, Strategy, and stablecoin supply.

Written by: Tanay Ved, Coin Metrics

Translated by: Luffy, Foresight News

TL;DR:

- Bitcoin gave back all of its gains from April, declining nearly 11% in the second quarter amidst a shift in interest rate expectations, outflows from ETFs, and capital rotation into AI stocks.

- All three major liquidity channels—ETFs, Strategy companies, and stablecoins—saw a weakening in the second quarter, with the spot Bitcoin ETF experiencing a net outflow of $4.08 billion.

- The total amount of long liquidations for BTC and ETH reached $8.35 billion, leading to significant deleveraging in the second quarter, but the market became more stable entering Q3.

Market Overview

The crypto market entered the second quarter of 2026 with good momentum. After a difficult Q1, Bitcoin rebounded to around $82,000 in April, aided by a brief easing of geopolitical tensions and improved institutional demand, alongside a recovery in the stock market. However, this recovery did not last.

This reversal was driven by three forces: Brent crude oil prices spiking to $126.41 due to geopolitical negotiations, a shift in Federal Reserve interest rate outlook to a hawkish stance, and capital rotating into AI sectors.

By mid-May, cryptocurrencies largely tracked the stock market, with both BTC and ETH rising about 20% from early April lows. A divergence occurred by the end of May, as cryptocurrencies retraced while the stock market remained robust. Ultimately, the S&P 500 and Nasdaq 100 indices rose approximately 16% and 28% respectively during the quarter, while BTC fell about 10%, ETH fell about 20%, and SOL fell approximately 13%.

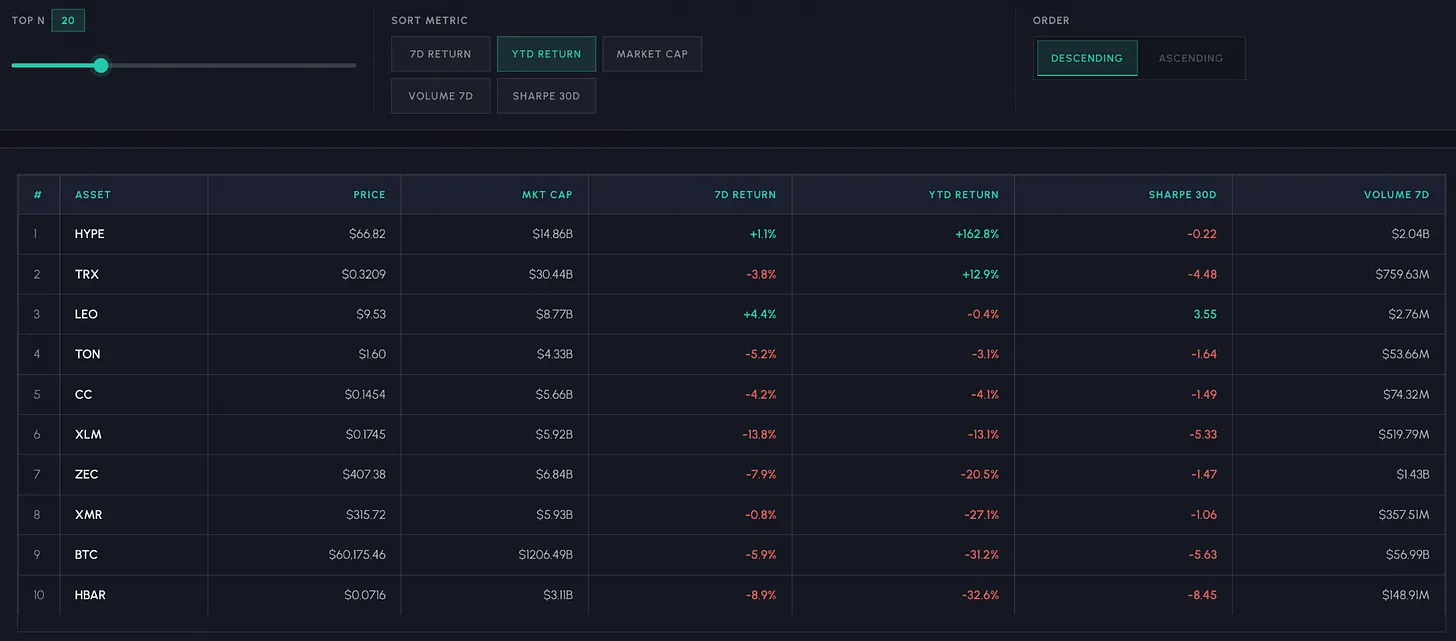

Bitcoin is currently trading around $60,000, down about 52% from its historical high of $126,000 set at the end of 2025. Altcoins have shown similar performance, with fewer rising coins. Year-to-date, among the top 20 cryptocurrencies by market capitalization, Hyperliquid (HYPE) remains the only standout (up 142%), driven by strong demand for trading perpetual contracts in stocks and commodities on-chain.

Capital Flows

The weak trend in the second quarter was exacerbated by the deterioration of three major demand channels: spot ETFs, crypto asset treasuries like Strategy companies, and stablecoin supply.

Spot Bitcoin ETF: April started strong for spot Bitcoin ETFs, with inflows dominating. The single-day peak inflow occurred on April 20, reaching $474 million, after which the flow of funds reversed. Outflows dominated the remaining time of the quarter, with 53 days of outflows compared to only 30 days of inflows. June was the month that caused major losses, with a net outflow of $3.84 billion for the tracked ETF issuers, which accounted for most of the quarterly total net outflow of $4.08 billion.

Crypto Asset Treasuries (Strategy Companies): In this quarter, the rate of Bitcoin accumulation by Strategy companies significantly slowed. Their priority stock (STRC), aimed to stabilize around $100, fell to a historical low of $74, while the market net asset value ratio (mNAV) compressed close to 1.0, impacting the funding channels behind their accumulation. The unexpected sale of 32 BTC in early June shocked the market and disrupted the sentiment of "never selling." In response, Strategy companies established a new digital credit capital framework, raising the STRC dividend to 12%, authorizing a sale of up to $1.25 billion in BTC, and setting up a $2.55 billion dollar reserve to cover approximately 17 months of debt.

Stablecoins: In the second quarter, the total market cap of stablecoins shrank by about $4.2 billion, leading to a reduction in funds supporting on-chain activity and liquidity. USDT modestly grew by $1.8 billion, while USDC shrank by $3.4 billion. Ethena's USDe fell by $1.4 billion as risk-off sentiment diminished market interest in yield-generating stablecoin strategies.

With all three major demand channels weakening simultaneously, the liquidity environment in the third quarter is noticeably tighter than in early second quarter. Whether this demand will flow back into crypto assets or continue to surge into AI stocks remains a dynamic to watch.

Exchange Activity and Derivatives

Total spot trading volume on exchanges fell by 28% to $2.32 trillion, continuing a downward trend that began in January. Futures trading volume fared slightly better at $12.32 trillion, down 11.6% quarter-on-quarter, but the spot/futures ratio compressed from 0.23 to 0.19, indicating that the increase is more related to derivatives positions rather than an increase in spot demand.

Hyperliquid particularly stood out, with its futures trading volume market share growing to about 4.5%, as on-chain perpetual contracts continue to capture market share from centralized exchanges.

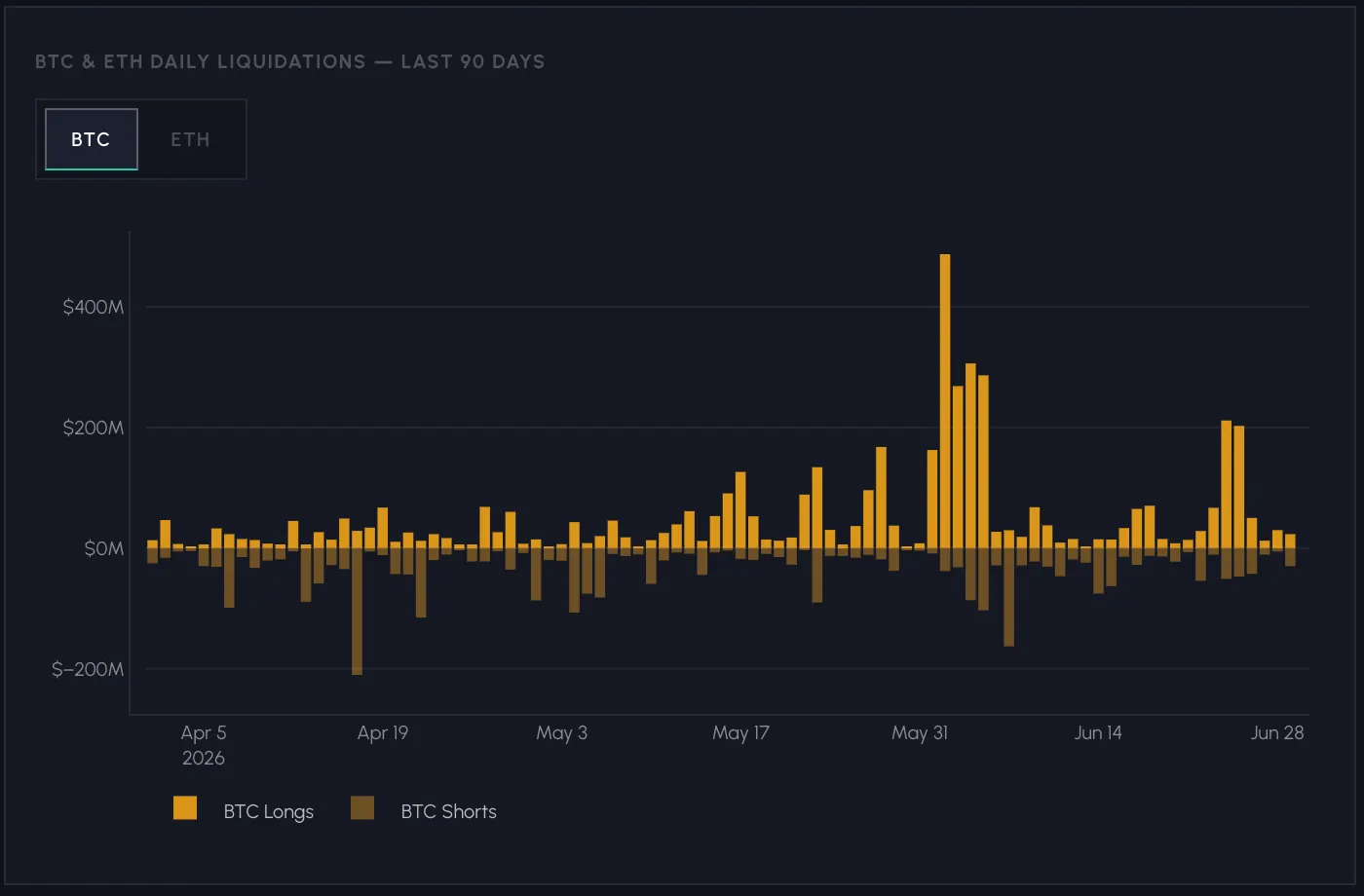

Open interest peaked before the sell-off in May, with BTC reaching $49.2 billion and ETH reaching $27.2 billion. Currently, these figures have dropped to $33.5 billion (BTC) and $16.2 billion (ETH), down 32% and 40% from their peaks, respectively. During the second quarter, the total amount of long liquidations for BTC and ETH reached $8.35 billion, with over half occurring between May 25 and June 7 as over-leveraged long positions were liquidated. The market entered the third quarter in a more deleveraged state.

During the second quarter, funding rates fluctuated drastically, swinging from deep negative values (annualized -16%) in mid-April to strong positives (annualized +10%) in May as long positions increased. The subsequent sell-off pulled rates back to neutral levels, oscillating around zero at the end of the quarter, reflecting cautious market sentiment.

Liquidity also deteriorated simultaneously. Bitcoin's 2% order book depth fell from a peak of about $70 million in early May to around $35-40 million by the end of June, indicating reduced market liquidity and weakened ability to absorb sell-off pressures.

Future Themes to Watch

Beyond the price trends of the second quarter, some structural developments also hint at the market's future direction, from new asset classes emerging on-chain to the infrastructure supporting them.

- Tokenized Stocks: Coinbase announced the launch of 1:1 pegged, fully rights-bearing tokenized stocks.

- Rise of RWA Perpetual Contracts: On-chain trading and price discovery have expanded beyond cryptocurrencies to stocks, indices, and commodities through Hyperliquid's HIP-3 perpetual contracts and centralized exchanges offering 24/7 RWA perpetual contracts.

- SpaceX IPO Priced On-Chain: The $1.7 trillion SpaceX IPO has been priced on the crypto rail before its public listing, providing early signals for price discovery of private companies.

- Treasuries and Lending Markets: On-chain treasuries are becoming a core layer for institutional capital, aggregating deposits into selected lending strategies like Morpho and Aave. As traditional asset management firms like Bitwise enter the treasury management space, the related infrastructure is maturing rapidly.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。