Original author: Ye Zhen

Original source: Wall Street Journal

Meta's plan to sell excess computing power breaks the market's core belief in "absolute scarcity of computing power." This strategic shift has triggered a significant outflow of funds from chip stocks and marks a turning point in the market's tolerance for the uncontrolled capital expenditures of tech giants.

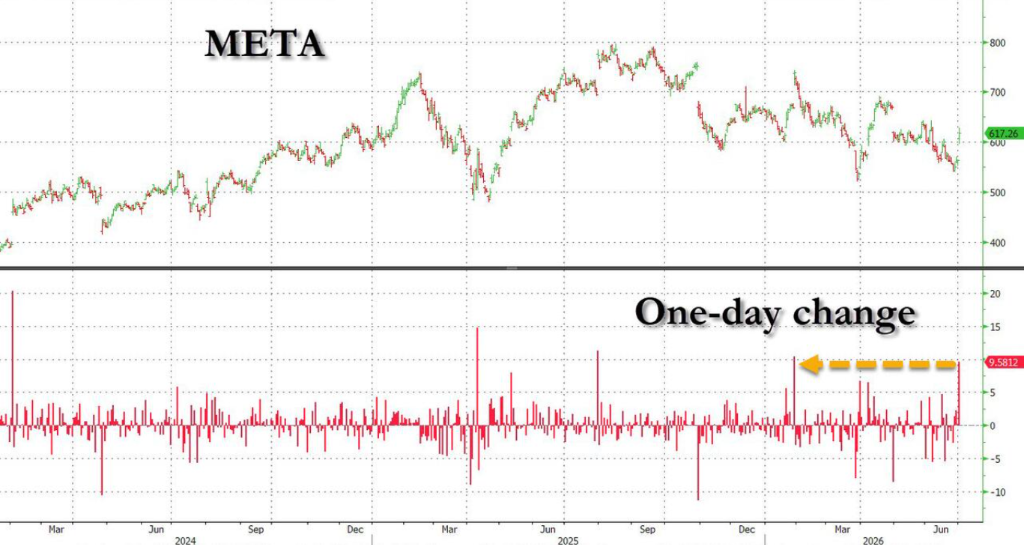

This news has caused extreme polarization in the secondary market. Meta, which actively signals a reduction in spending, saw its stock price surge by 10% in a single day, achieving its best performance of the year; meanwhile, traditional AI hardware beneficiaries—semiconductor giants, memory chip manufacturers, and emerging cloud service providers (Neocloud)—have suffered heavy losses, dragging the Nasdaq index into significant fluctuation.

Wall Street institutions generally interpret this as a major narrative shift in the AI investment cycle. The focus of capital is rapidly shifting from purely hardware infrastructure construction to the stability of corporate free cash flow and computing power utilization, with investors beginning to reward tech giants that demonstrate financial discipline with real money.

This change in underlying logic not only rewrites the power dynamics between hyperscale cloud providers and chip suppliers but also directly leads to the collapse of overcrowded momentum trading strategies, creating new uncertainties for the upcoming U.S. earnings season and market liquidity.

Meta's shift to sell "excess computing power" faces a turning point for large enterprises' capital expenditure

According to Bloomberg, Meta is forming a new business plan to sell its surplus computing capacity to external customers for revenue. Insiders reveal that potential options include allowing external access to various AI models hosted on Meta's existing AI infrastructure, a model similar to AWS's Bedrock service. Meta will be responsible for operating the data centers and chips powering its models like Muse Spark and charging developers for access.

Moreover, Meta is also considering directly selling "raw" computing power. Ironically, Meta had just signed contracts worth billions of dollars with emerging cloud service providers like CoreWeave and Nebius, and this move suggests that it will now directly compete with its own suppliers.

This internal initiative, named "Meta Compute," aims to build and manage the company's AI infrastructure. The team is co-led by Meta's infrastructure head Santosh Janardhan, AI division executive Daniel Gross from the Superintelligent Labs, and Meta's president Dina Powell McCormick.

In fact, this shift had been anticipated. Meta CEO Mark Zuckerberg hinted to investors during the May shareholder conference that selling excess computing capacity or API services "is absolutely within consideration." Another company that previously sold excess computing capacity, SpaceX, is also facing fierce competition in selling computing power recently.

The "scarcity of computing power" logic is challenged, and chip and momentum stocks face severe setbacks

Meta's actions directly challenge the core premise supporting the recent surge in chip stocks. Rich Privorotsky, head of Goldman Sachs' 1-Delta trading desk, warned that the market's core premise has always been computing power scarcity; once supply increases and rental prices decline, the scarcity narrative will be directly overturned, with hardware being the first to feel the pain.

Goldman Sachs warns that the AI market has become like a stretched rubber band, and the market's ongoing indifference to negative signals will eventually reach a breaking point. Once any major tech giant cuts AI spending, the valuation logic of the entire AI sector will face a comprehensive restructuring; meanwhile, the rise of low-cost AI models is challenging the current "high investment for growth" logic.

Impacted by Meta's news, the chip and storage sectors are first in line, with star stocks like Nvidia, Micron, and SanDisk facing tremendous sell-offs. Emerging cloud service providers are seen as the most obvious losers, with their stock prices recording some of the largest declines this year.

The sharp decline in the hardware sector has directly triggered a comprehensive collapse of momentum strategies. Goldman Sachs' high Beta momentum basket (currently mainly composed of chip and storage stocks) fell 9% in a single day after reaching historic highs. BTIG analyst Jonathan Krinsky pointed out that the long-short high Beta momentum index fell 10%, marking its worst single-day performance since 2020.

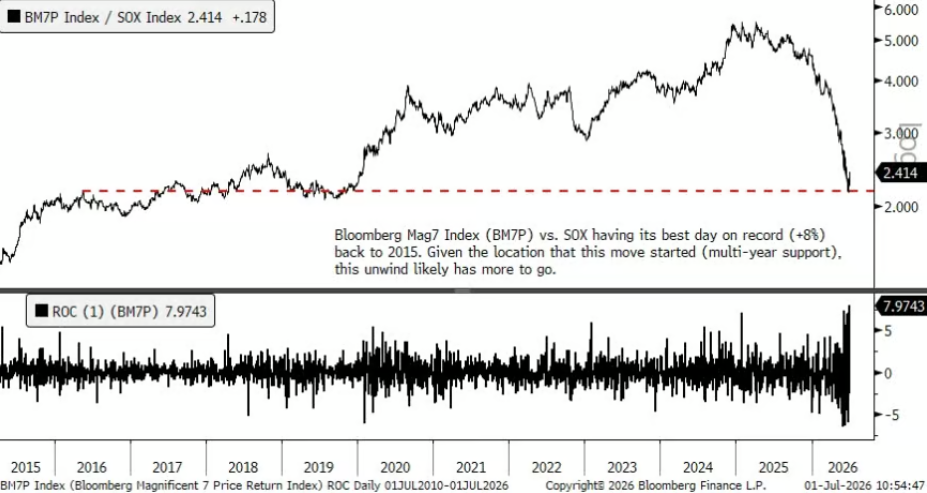

Additionally, the yield difference between the Bloomberg Mag7 index and the Philadelphia Semiconductor Index (SOX) reached the largest single-day extreme (+8%) since 2015, indicating that funds are crazily withdrawing from the semiconductor sector.

Market logic reshaping, investors rewarding "spending cuts"

In stark contrast to the dismal performance of hardware stocks, the market is giving a very high premium to signals of capital expenditure cuts. As Goldman Sachs previously predicted, the first hyperscale cloud provider to suggest a slowdown in spending will receive stock market returns.

Meta's surge of 10% confirms this judgment, indicating that investors believe, given the current valuation multiples, incremental revenue streams and financial discipline are more attractive than an endless arms race.

UBS trader Christina Dwyer noted that the relevant reports have shifted the market narrative towards stricter financial discipline, alleviating concerns over the continuous rise of capital expenditures. Capital expenditure expectations are no longer skewed solely upwards, with the market's focus turning to the stability of free cash flow.

Against the backdrop of capital rotation, the software sector has seen its second-largest single-day excess return relative to the semiconductor sector in a year.

Intensifying competition and liquidity concerns, upcoming earnings reports as key guidance

Meta's entry has made the supply and demand landscape for hyperscale cloud providers more complex. While the emergence of new competitors disrupts the existing landscape, alleviation of supply chain bottlenecks may also bring cost pressure relief.

UBS points out that the term "excess capacity" has raised market concerns about the underlying real demand for AI, and as we look forward to the upcoming Q2 and Q3 earnings seasons, the guidance provided by companies and their full-year capital expenditure plans will be key to determining whether the current valuation reassessment can be sustained.

It is worth noting that while the market experiences massive rotations, it is also facing severe liquidity risks. Goldman Sachs trading desk warns that although U.S. stock markets have recorded the highest daily average trading volume since 2026, market liquidity remains extremely poor. In June, the top-of-book liquidity of S&P E-mini futures plummeted by 33% month-on-month, from $12 million to only $8 million.

This means that the market is conducting record trades in a deeply shallow pool of funds. Each large order triggers more intense market fluctuations, execution costs are rising, and the risk of intra-day abnormal collapses remains high. Under the seasonal factors where momentum stocks typically perform poorly in July, chip stocks and the broader market may face even more severe shocks.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。