Original author: Glassnode

Original translation: AididiaoJP, Foresight News

The price of Bitcoin has fallen below $60,000, with institutional funds continuing to flow out and defensive positions in the options market suppressing market sentiment. However, beneath the surface, long-term holders and patient buyers are gradually absorbing selling pressure, suggesting that the bottoming process may have quietly begun.

Key Points

- Long-term holders are returning to accumulation mode, experienced investors are once again absorbing chips during the market pullback.

- Widespread accumulation is seen across multiple wallet groups, showing that investors are gradually gaining confidence in the weakening price.

- The quantity of Bitcoin currently at a loss has exceeded that in profit, reflecting general pressure on investors, with chips shifting towards more resolute holders.

- The U.S. spot Bitcoin ETF continues to experience net outflows, and the trend of de-risking by institutions persists.

- Coinbase's order book is notably skewed towards buy orders, with institutions patiently providing liquidity and rebuilding support below the market.

- Leverage traders have significantly increased long exposure, potentially triggering a violent rebound or a new round of long liquidations.

- Market-maker gamma positions are increasingly favorable, with hedging funds likely to suppress volatility and promote price stability.

- Options traders are paying premiums for downside protection, with a clearly defensive market sentiment and a surge in hedging demand.

- Implied volatility is rising, indicating Bitcoin is entering a bottoming phase, although a final panic-driven spike in volatility cannot be ruled out.

Macroeconomic Insights

The Federal Reserve maintained interest rates in June for the fourth consecutive meeting, but the real market impact is not the decision itself, but the tone. Newly appointed Fed Chair Kevin Warsh has exhibited a distinctly hawkish stance. Due to stubborn inflation above target and tariffs that continue to push consumer prices higher, the market has largely abandoned expectations for interest rate cuts this year. The earliest possible easing may not be until 2027. Treasury yields have risen back to near 2026 highs, the U.S. dollar has strengthened, and while the job market is still adding positions, concentration is showing signs of narrowing. Financial conditions are not loose, and there are currently no catalysts to improve this situation in the near term.

Bitcoin has become the primary bearer of this repricing. After strong performance in the first quarter, June saw the most severe institutional retreat since the introduction of the spot ETF: the ongoing wave of redemptions is more a rational profit-taking rather than a panic sell-off—many institutional positions were built at prices significantly lower than current levels. The selling pressure is orderly yet continual, leading Bitcoin's price to drop back to levels that reset short-term expectations. As we enter the third quarter, the key question is whether the macro environment can stabilize to restore risk appetite, or if sticky inflation and a strong dollar will continue to weigh on liquidity-sensitive assets.

On-Chain Insights

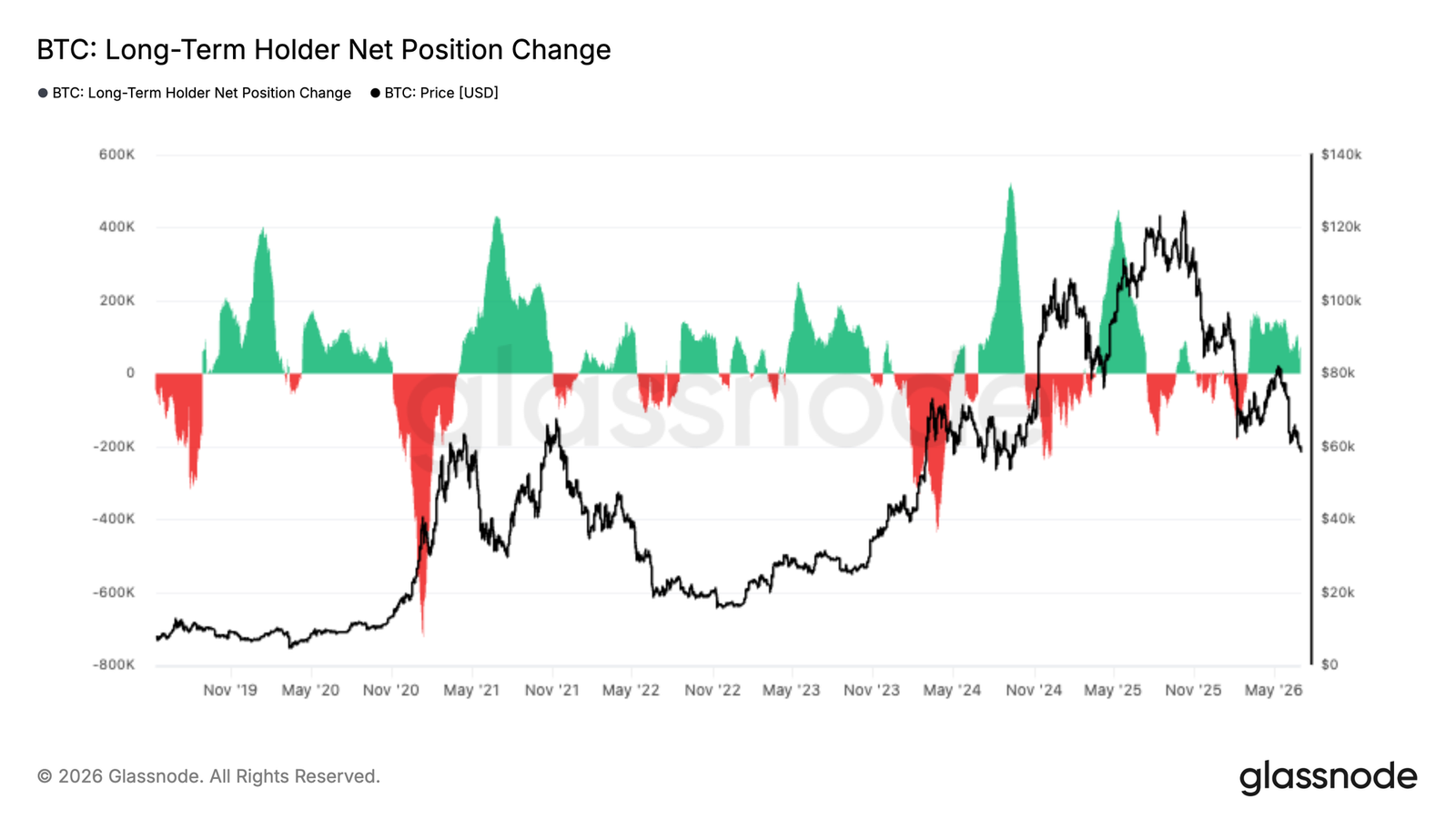

Long-Term Holders Return to Accumulation

Long-term holders have begun to rebuild their positions after a prolonged period of distribution, with net position changes firmly turning positive. Although the accumulation speed seems mild compared to the large-scale buying during the previous bull market expansion, this marks a significant behavioral shift—Bitcoin's most confident investor group is starting to absorb chips again.

This change occurs as Bitcoin retraces to around $60,000, indicating that experienced holders view the recent pullback as an opportunity rather than a reason to reduce holdings. Historically, a continuous shift from net distribution to net accumulation often occurs during weak market periods, with long-term investors gradually increasing their positions while short-term participants de-risk. While it is still too early to declare a full accumulation phase, the ongoing return to long-term buying has released positive signals: belief is being gradually rebuilt beneath the surface.

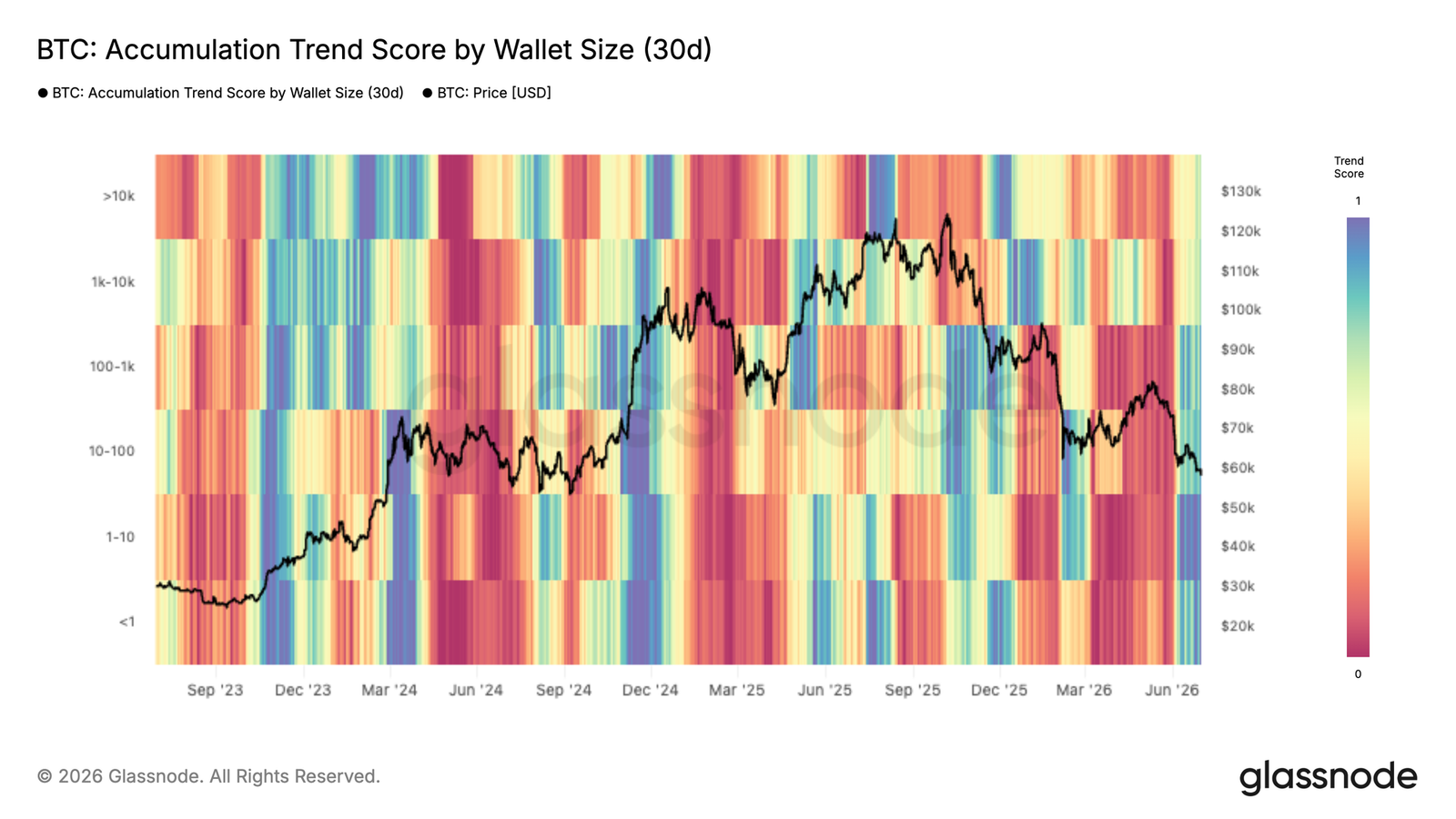

Widespread Accumulation Emerging

The accumulation trend score for Bitcoin has significantly improved over the past month, with buying behavior becoming increasingly widespread among investor groups. Following several months of sustained distribution during market declines, most wallet groups have shifted towards accumulation, indicating that the recent pullback is beginning to attract new demand.

The strongest accumulation currently comes from small holders (less than 1 BTC) and entities holding 100-1000 BTC, both of which have trend scores nearing their highest levels. Meanwhile, larger groups, including wallets holding 1000-10000 BTC, have also turned to net buying, though not at the intensity seen earlier in the cycle. This simultaneous improvement among multiple investor groups indicates that confidence is being rebuilt after the pullback, with market participants increasingly willing to absorb selling pressure at current price levels. Historically, widespread accumulation among different wallet sizes often lays a constructive foundation for long-term market recovery, although continuous buying is needed to confirm this.

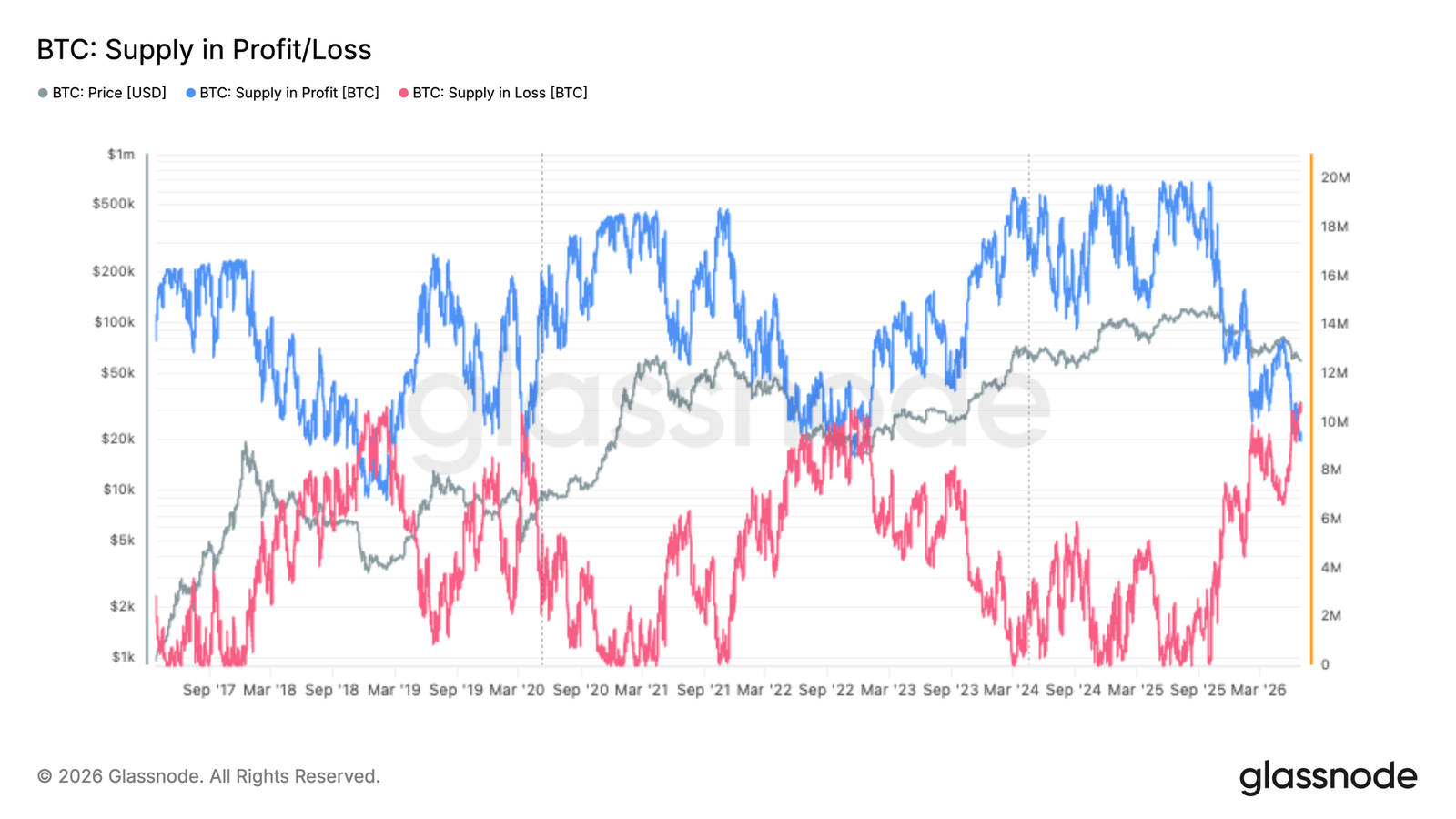

Most Bitcoin at a Loss

Recent sell-offs have pushed the market into an important psychological and structural milestone: the quantity of Bitcoin currently at a loss has exceeded that in profit. According to the latest data, approximately 10.83 million Bitcoins are underwater, compared to about 9.22 million that are in profit. This marks one of the most significant deteriorations in investor profitability since the start of this bull market, reflecting the degree of recent repricing.

Historically, when the amount of lost chips exceeds that of profitable chips, it is often accompanied by high financial pressure and a broad capitulation of new entrants. While this may suppress sentiment in the short term, it also creates favorable conditions for stronger hands to absorb weaker hands' chips. Combined with the renewed accumulation from long-term holders and other groups, the sharp decline in profitability indicates that the market is entering a phase where chips are migrating towards high-conviction investors.

Off-Chain Insights

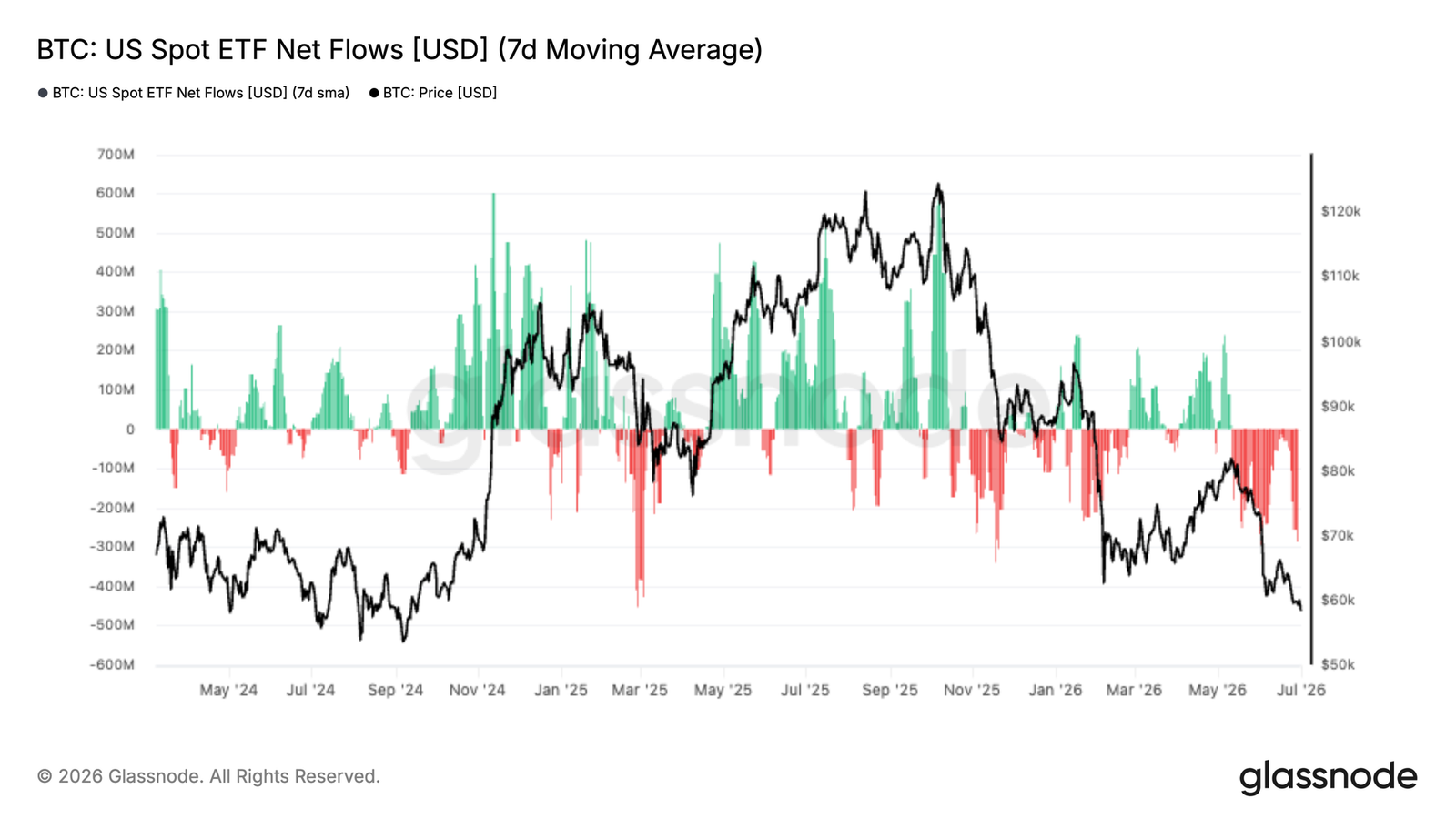

Accelerating ETF Outflows

Institutional demand continues to deteriorate, with the seven-day moving average net outflow of the U.S. spot ETF deepening into negative territory. After a brief warming in May, funds reversed again, and with Bitcoin falling towards $60,000, continuous outflows have become the norm. The persistence of redemptions indicates that institutions are still maintaining a defensive stance, opting to reduce holdings rather than enter to absorb weakness.

This sharply contrasts with the strong ETF demand that previously drove the market upward. While on-chain data shows long-term holders and multiple groups are re-accumulating, ETF investors have not exhibited the same level of conviction. This divergence underscores that the current market is supported by patient on-chain capital, while institutions more sensitive to price are continuing to withdraw liquidity. Stabilization of ETF fund flows will be an important signal to confirm the recovery of broader investor confidence.

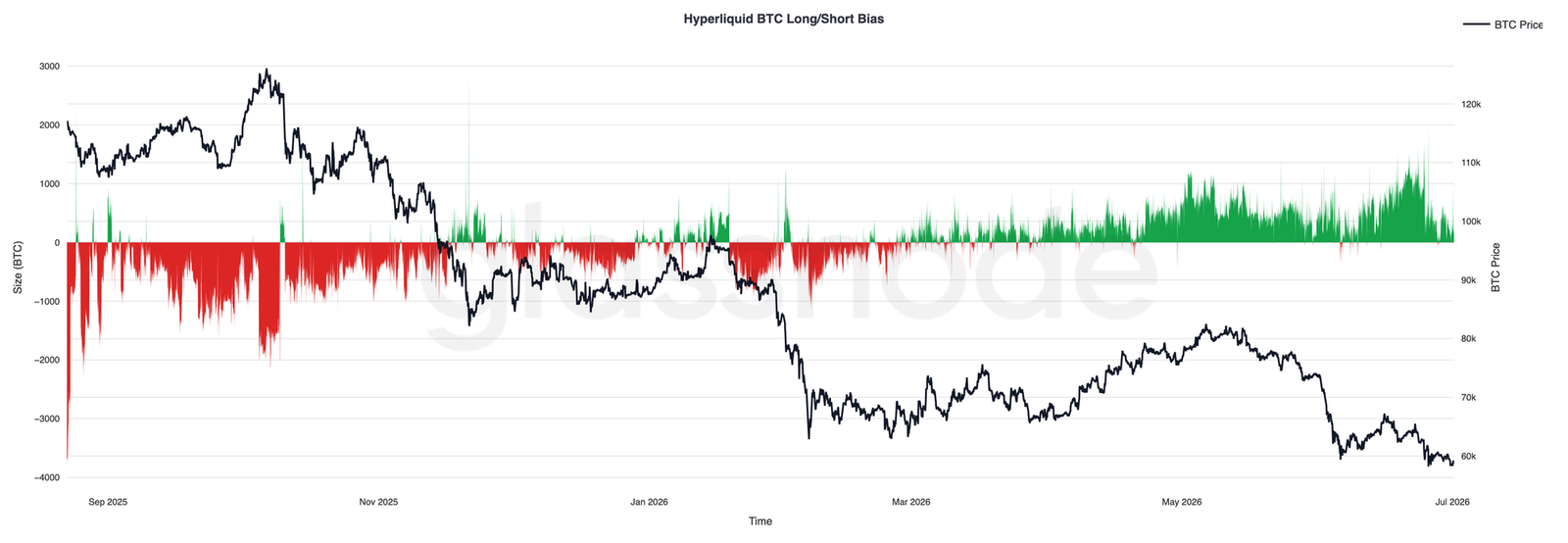

Hyperliquid Leverage Traders Turning Very Bullish

Positions on Hyperliquid have generally shifted to long, even as Bitcoin prices continue to decline, with net long exposure steadily increasing. Leverage traders have not reduced their positions during weakness; on the contrary, they continue to increase bullish positions, pushing long preferences to the highest levels in the observation period.

This creates an increasingly asymmetric market structure. If buyers regain control, a large number of long positions may fuel a violent rebound. However, as long as prices remain in a clear downtrend, the accumulation of leveraged longs makes the market susceptible to further downward shocks after support fails. If such a scenario occurs, forced liquidations of excessively expanded longs will amplify volatility and accelerate declines. Current data shows that derivatives traders are preparing for a reversal, but this conviction remains to be validated by price action.

Options Market Maker Positions Favorable for Suppressing Volatility

Deribit GEX strike price heatmap shows that the options market near current prices is being dominated by positive gamma positions. Significant positive gamma concentration forms near the $60,000 low. When market makers are in a positive gamma state, they typically buy during weakness and sell during strength to hedge, and this dynamic naturally suppresses volatility and encourages prices to stabilize near high open interest strike prices.

This suggests that despite recent sell-offs, the options market is no longer preparing for accelerated downward movements. On the contrary, the flow of market maker hedging funds is increasingly becoming a source of liquidity, helping to absorb directional volatility and reduce the likelihood of chaotic price movements. This does not necessarily signify an impending reversal but indicates that the market is transitioning from a state of high instability during the downturn. Unless significant macro catalysts force prices away from these gamma-dense areas, options positions point towards a period of consolidation and reduced realized volatility, rather than a new round of panic selling.

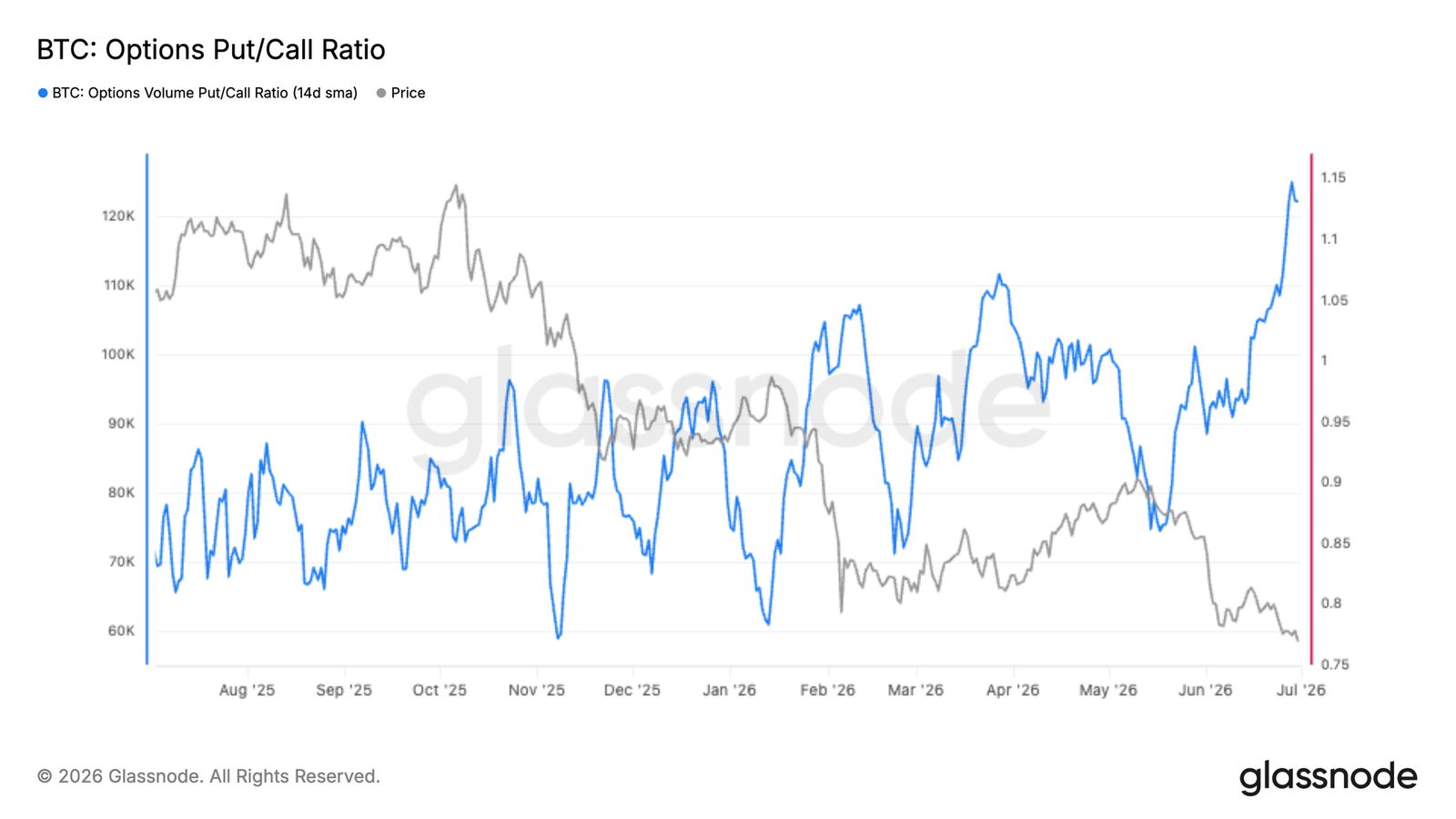

Options Traders Paying Premiums for Downside Protection

The options market has shifted to defense, with the 14-day put/call volume ratio soaring above 1.0, reaching the highest level in the past year. This indicates that put options activity has eclipsed call buying, reflecting that traders are prioritizing downside protection rather than upward participation after Bitcoin falls towards $60,000.

Historically, high put/call ratios occur during periods of great uncertainty, with investors either hedging spot exposure or expressing bearish views. While this reinforces the cautious tone of ETF fund flows and recent price actions, excessive hedging demand could also become a contrarian signal. When a large number of participants have defensively positioned, the market's vulnerability to incremental selling pressure tends to decrease. However, for now, the options market still shows that risk management, rather than recovery speculation, remains the dominant priority.

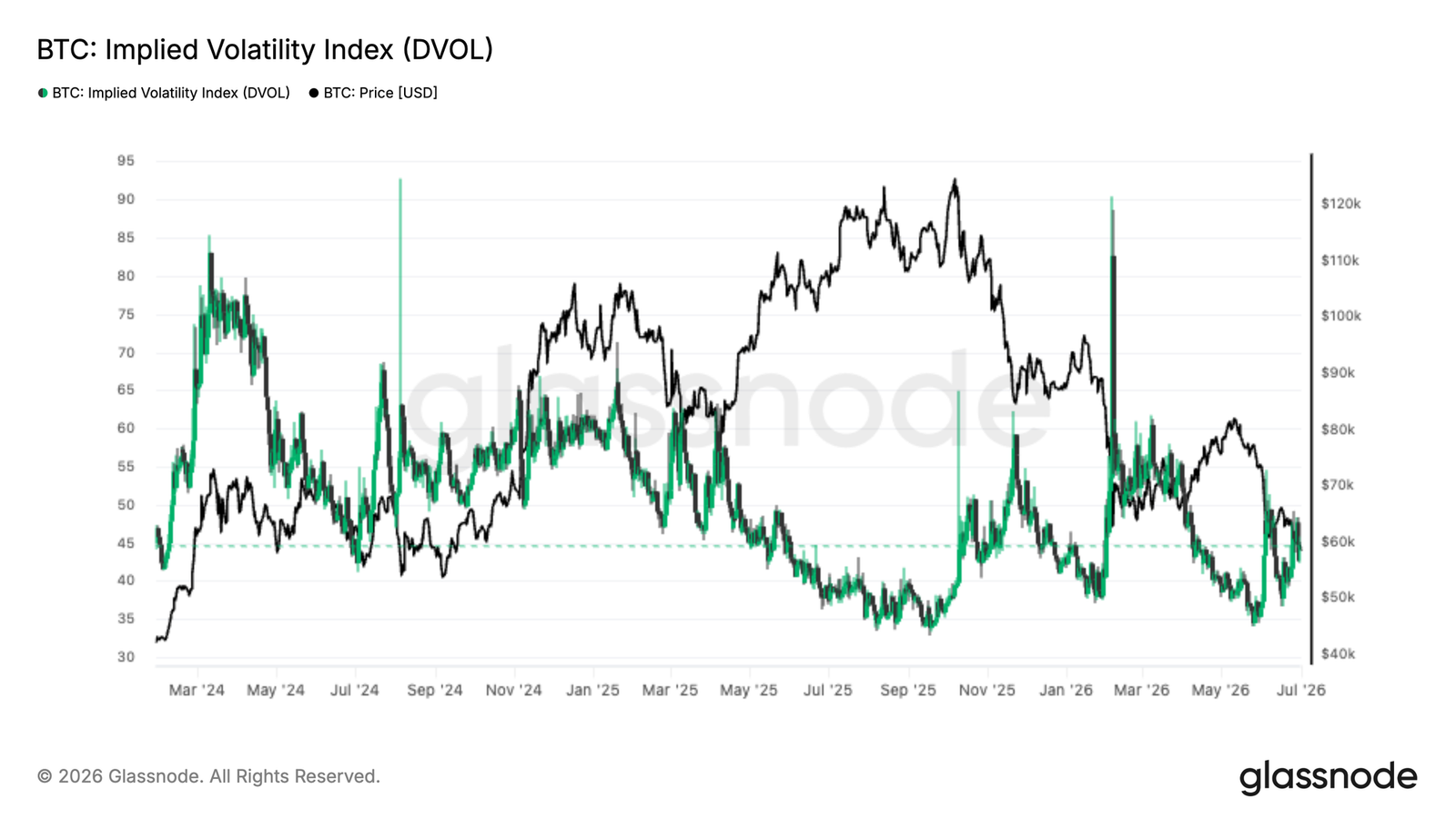

Implied Volatility Resurgence

The Bitcoin implied volatility index (DVOL) has begun to rise from historical lows following recent sell-offs, but it remains far below the panic extremes typical of significant market dislocations. This suggests that options traders are beginning to price in larger future price volatility, with uncertainty rising, yet expectations have not reached the fear levels historically accompanying durable lows.

Structurally, this feels more like the early stages of a bottom rather than an end. Volatility begins to reprice as the market seeks a bottom, but prior cycle lows often come with one last spike in volatility, triggered by forced selling, liquidations, or macro shocks. If such a peak occurs, it is likely accompanied by indiscriminate selling and high pressure in the derivatives market. Until that happens, the gradual rise in implied volatility indicates that traders are preparing for larger moves, although the final washout needed to establish a durable bottom has yet to occur.

Conclusion

Bitcoin is still in a clear pullback phase, but beneath the weak price performance, some significant structural changes are starting to manifest. Long-term holders are accumulating again, buying activity is expanding among multiple wallet groups, and the Bitcoin spot order books (Binance and Coinbase) are increasingly skewed towards buy orders. These changes are typically associated with patient capital entering the market when weak hands exit.

At the same time, caution is still required. Institutional funds are continually flowing out of the U.S. spot ETF, options traders are actively hedging downside risks, and leveraged long positions have reached high levels, making the market susceptible to another round of liquidation-driven selling. Implied volatility also suggests that the market may still need to experience one final washout to establish a low.

Overall, the data indicates that Bitcoin is transitioning from a distribution phase to an accumulation phase, but confirmation is still needed. While the foundation for a long-term recovery is gradually forming, the market may first need to undergo a final test of belief before a sustainable upward trend can emerge.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。