Introduction

In the past few years, DeFi's yields have primarily come from on-chain mechanisms. Lending protocol yields stem from user borrowing demands, DEX yields come from trading fees, derivatives protocols generate yields from funding rates and liquidations, and liquidity mining yields are derived from token subsidies. The advantage of this system lies in its transparency, openness, and composability, but the downsides are also significant: yields are highly dependent on market conditions, leverage, and trading activity. Once the market enters a low volatility, low leverage, and low trading volume environment, on-chain yields can quickly compress.

Now, the yield structure of DeFi is undergoing a deeper shift. Protocols are beginning to allocate reserve assets, stablecoin liabilities, and idle user funds into tokenized Treasuries, money market funds, CLOs, private credit, on-chain credit vaults, and institutional-grade yield products. DeFi is no longer just seeking yields from within the on-chain ecosystem; it is incorporating cash flows, credit spreads, and interest rate curves from TradFi onto the chain, then distributing them to users through stablecoins, vaults, sTokens, or yield-generating assets.

I. The DeFi Yield System Enters a Reconstruction Cycle

If the first phase of DeFi addressed the question of "whether a financial market can spontaneously form on-chain," the industry now faces a more pragmatic issue: when trading, leverage, and token incentives can no longer sustain high yields, what exactly should the next phase of DeFi growth rely on?

1.1 Intrinsic Yields Are No Longer Sufficient to Sustain DeFi's Next Growth Phase

The first wave of DeFi growth relied on on-chain native yields. Lending protocols like Aave, Compound, and MakerDAO, DEXs such as Uniswap and Curve, as well as derivatives protocols like dYdX and GMX, together proved one fact: as long as there is trading, borrowing, leverage, and liquidity demand on-chain, protocols can continuously create yields through transaction fees, borrowing interests, funding rates, etc., without depending on the traditional financial system. However, as the market matures, this model that relies entirely on on-chain activities for yields is beginning to show increasingly evident limitations.

First, on-chain yields have a clear pro-cyclical characteristic. During bull markets, leverage demand increases, borrowing scales expand, and trading activity elevates, allowing protocol revenues to grow quickly; but when entering bear markets, trading volumes shrink, funding rates decline, and borrowing demand weakens, leading to a simultaneous reduction in protocol yields. Therefore, on-chain yields struggle to form long-term stable cash flows.

Secondly, the yields in DeFi often come from the cyclic use of the same pool of funds. Users collateralize ETH to borrow stablecoins, then participate in leverage strategies, LP strategies, or yield vaults, with different protocols nested within each other, leading to a continuous increase in TVL, but without a real increase in underlying assets. This capital cycle can amplify yields during market uptrends and exacerbate liquidation risks and liquidity shocks during downturns.

Finally, token incentives are difficult to sustain over the long term. Early DeFi relied on liquidity mining to achieve a cold start, but subsidized yields are not equivalent to real yields. When token prices rise, high APY can quickly attract funds; conversely, when token prices fall, high yields quickly convert into sell pressure, leading protocols to consistently raise subsidy costs to maintain liquidity. For stablecoins, savings products, and institutional funds, this yield model dependent on incentives is hard to meet long-term allocation needs.

As the industry enters a mature phase, relying solely on on-chain intrinsic yields is becoming increasingly insufficient to support DeFi's continuous growth; searching for new sources of yields is gradually becoming the direction for the entire industry's development.

1.2 TradFi Yields Enter the Chain, DeFi Begins to Seek a Second Growth Curve

Against this backdrop, TradFi yields are starting to become an important supplementary source for DeFi. Traditional financial assets like U.S. Treasuries, money market funds (MMF), structured credit products, and private credit may not be new concepts, but through asset tokenization, compliant custodianship, and on-chain distribution mechanisms, they are beginning to enter the DeFi ecosystem in the form of on-chain assets.

For protocols, the source of yields is shifting from dependence on on-chain trading activities to acquiring real cash flows off-chain; for users, stablecoins are also beginning to evolve from being merely transactional media to entrances for on-chain money market funds, savings accounts, and yield asset management products.

It is important to emphasize that the migration of yield sources does not mean that risks disappear, but rather signifies a change in the structure of risks. Traditional DeFi has focused more on smart contract, oracle, and liquidation risks; with the introduction of TradFi yields, custodial risks, credit risks, interest rate risks, redemption liquidity, maturity mismatches, and legal rights have begun to emerge as new core risk sources.

Therefore, the essence of DeFi introducing TradFi yields is not about acquiring "risk-free yields," but rather completing a restructuring of yield sources and risk pricing systems. Those who can efficiently allocate real-world assets, manage risks, and continuously distribute stable yields will gain an advantage in the next stage of DeFi competition.

II. The Divergence from DeFi Native Yields to Asset Management Yields

In the face of the gradual capping of on-chain intrinsic yields and the ongoing influx of TradFi yields, different protocols have evolved divergent yield models based on their positioning and governance philosophy. Some remain committed to the native DeFi lending logic, some are beginning to build a complete on-chain asset management system, while others directly use U.S. Treasuries and other RWAs as underlying reserves.

2.1 Aave: Committed to DeFi Native Yields

As one of the largest decentralized lending protocols currently, Aave's business model has always revolved around lending interest differentials. Users deposit assets like ETH, BTC, and stablecoins into the protocol to earn deposit yields, while borrowers pay interest on loans, with the protocol obtaining some interest differential income through the Reserve Factor, forming a continuous cash flow for the protocol.

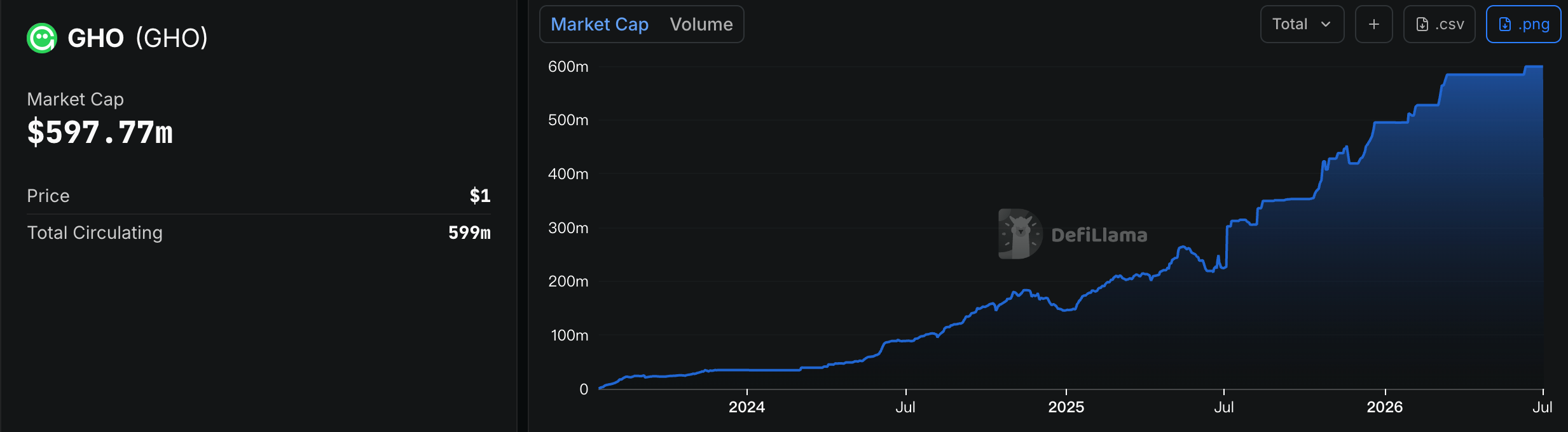

The launch of GHO further完善 of Aave's yield loop. GHO is an over-collateralized stablecoin introduced by Aave in 2023. Unlike stablecoins issued by centralized institutions such as USDT and USDC, GHO is not issued based on fiat reserves but is minted by users through collateralizing qualifying assets and borrowing. GHO is essentially still an on-chain loan. Users only mint GHO when there's borrowing demand and continuously pay loan interest; once the loan is repaid, GHO is simultaneously destroyed. Hence, the circulation of GHO directly reflects on-chain funding demand, while protocol revenues come from the continuous interest payments made by users. According to DeFiLlama data, as of July 2, 2026, GHO had a total circulation of approximately $598 million.

https://defillama.com/stablecoin/gho

To further reward long-term holders, Aave has also launched sGHO (Savings GHO), which currently offers an annualized yield of 4.5%. After users deposit GHO into sGHO, they can share in the protocol's revenues distributed as determined by governance. From a yield structure perspective, Aave's logic is very clear: borrowing demand creates yields, the protocol acquires those yields, and then governance decides on yield distribution.

2.2 Sky: Transitioning from a Stablecoin Protocol to an On-Chain Asset Management Platform

Following a brand upgrade launched by MakerDAO in 2024, it proposed a new positioning: upgrading the protocol from a single stablecoin system to a complete on-chain asset management platform. In this system, USDS is no longer just a stablecoin but represents the entire protocol's liability side; sUSDS has become the primary entrance for users to share protocol yields; modules like Spark, Grove, PSM, and Legacy RWA together form the protocol's asset allocation system. The protocol no longer relies solely on a single lending market to create yields; instead, it allocates funds to different types of yield-generating assets according to governance strategies and continually allocates yields to sUSDS holders through the Sky Savings Rate (SSR).

Compared to Aave, Sky's biggest difference is that its yield sources have started to diversify. On one hand, lending protocols like Spark can still contribute continuous on-chain borrowing yields; on the other hand, the protocol is gradually increasing the proportion of allocations to U.S. Treasuries, money market funds, and other real-world assets, transitioning yield sources from solely on-chain financial activities to off-chain real cash flows. At the same time, PSM (Peg Stability Module) continues to manage stablecoin exchanges and liquidity, forming a complete asset-liability management system interlinking liabilities, asset allocations, and yield distribution.

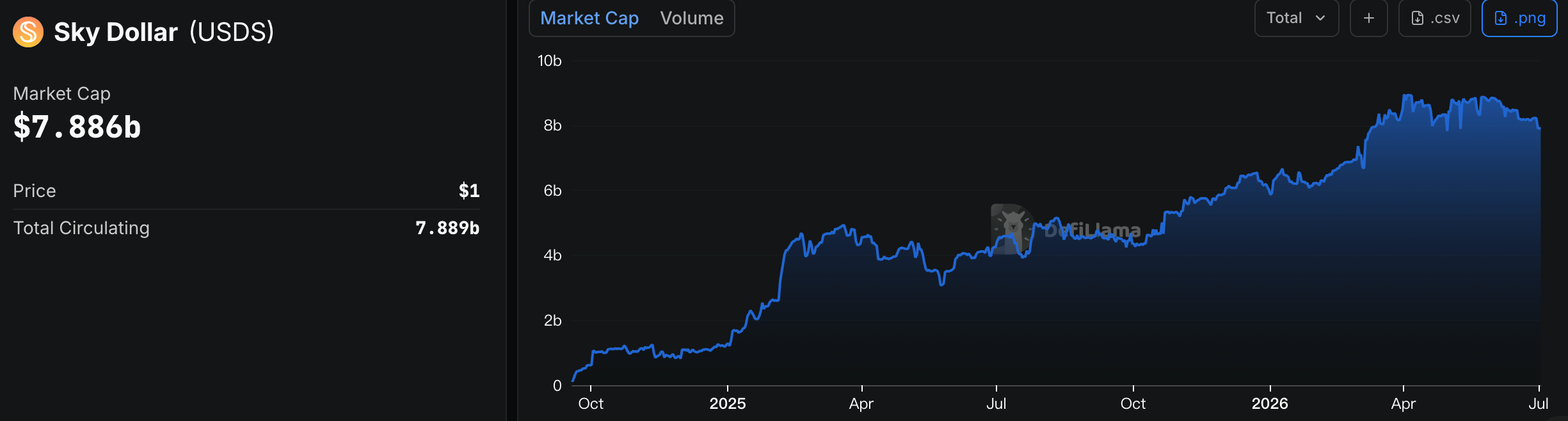

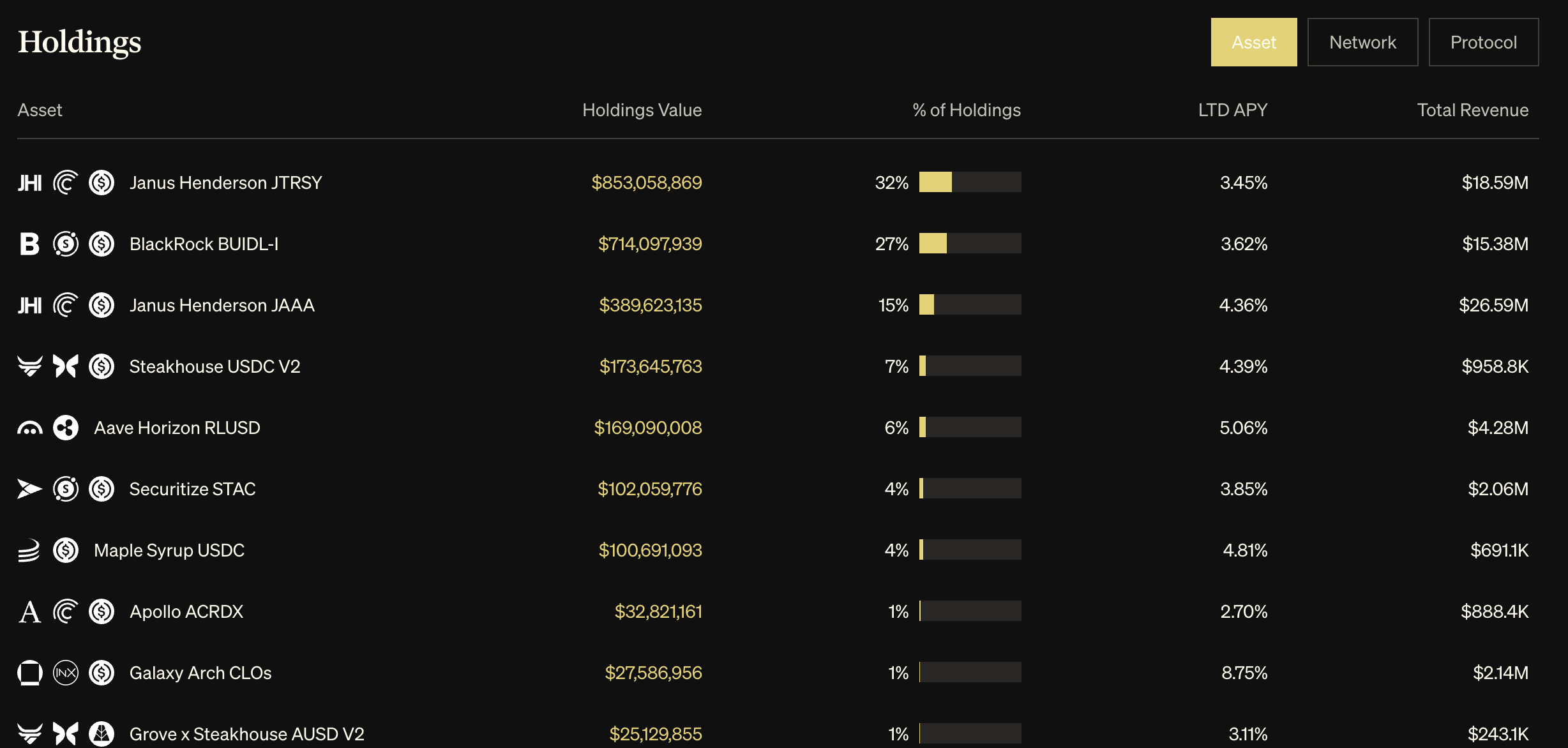

As of early July 2026, sUSDS has become one of the largest yield-generating stablecoins in the DeFi market, with sky’s official data indicating a total USDS supply of about $7.88 billion as of July 2, 2026, with an sUSDS APY of 3.75%. Meanwhile, core modules such as Spark and Grove manage billions of dollars in assets, continuously creating stable cash flows for the protocol, making Sky one of the most capable protocols in asset allocation currently in DeFi. As of now, the total value of Grove's holdings is approximately $2.645 billion, including about $1.567 billion in short-term U.S. treasury bonds, about $492 million in investment-grade public credit, and about $32.82 million in private credit. The three categories total around $2.092 billion, accounting for approximately 79.1% of Grove's total holdings.

Source: https://defillama.com/stablecoin/sky-dollar

Source: https://data.grove.finance

This shows that Sky has established a multi-layered, multi-source asset portfolio and continuously allocates funds through a unified asset-liability management system. This model is increasingly approaching the operational logic of traditional asset management institutions, with all asset allocations, yield distribution, and governance decisions occurring on-chain.

2.3 Ethena: Building a Dual Yield Engine Parallel to TradFi

In contrast to Aave's commitment to DeFi native yields and Sky's restructured asset-liability management system, Ethena has created a multi-yield system that can dynamically switch according to market conditions. Ethena's initial innovation comes from USDe. USDe does not rely on on-chain lending; rather, it builds a delta-neutral strategy by holding spot assets and establishing corresponding perpetual contract short positions. The most prominent feature of this model is that its yields do not come from lending interest but from the trading structures of the crypto market itself. However, funding yields show significant cyclicality. When the market enters a fluctuating or bear market phase, funding rates decline or even turn negative, similarly causing protocol yields to fluctuate.

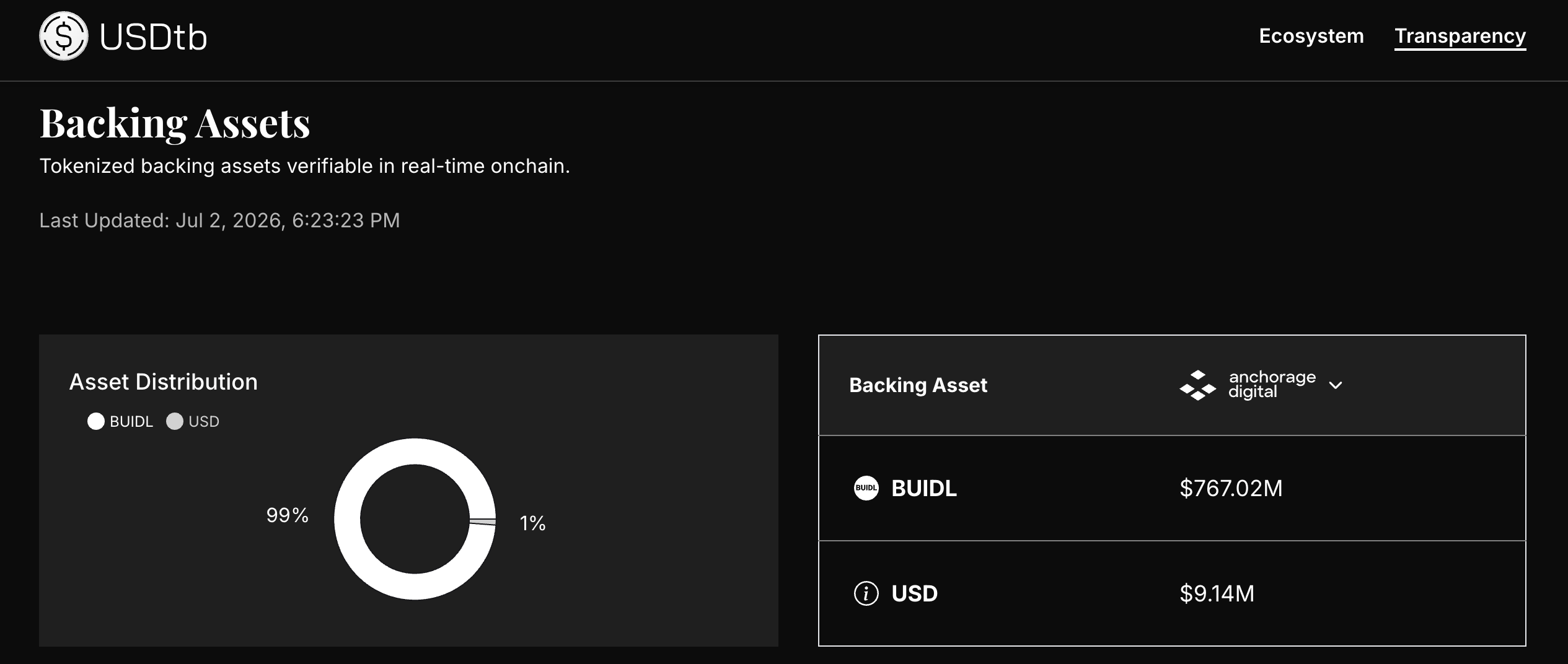

In this context, Ethena introduced USDtb. Unlike USDe, USDtb does not rely on derivatives strategies to generate yields, but rather allocates underlying reserves to BlackRock's BUIDL fund and other U.S. Treasury assets, with yields directly sourced from the interest generated by U.S. Treasuries and other real-world assets. The emergence of USDtb signifies another developmental direction: DeFi is no longer just about on-chain financial protocols but is beginning to serve as a distribution channel for real-world assets on-chain. According to DeFiLlama data, as of July 2, 2026, USDtb had a circulation of about $775 million, of which approximately 98.97% was in BUIDL reserves.

Source: https://usdtb.money/transparency

By simultaneously laying out funding yields and U.S. Treasury yields, Ethena establishes two distinct yield engines: on one hand, during periods of market activity, the protocol can take full advantage of high-yield opportunities arising from the derivatives market; on the other hand, when funding yields decline, it can rely on real-world assets to provide more stable cash flow, thus smoothing overall yield fluctuations and enhancing the protocol's stability across different market cycles. Therefore, what Ethena represents is not a specific yield model, but rather a more flexible idea of yield allocation: protocols can integrate both on-chain and off-chain yield sources simultaneously and continuously optimize asset allocations based on market conditions, achieving a dynamic balance of yield sources.

These three models correspond to different asset allocation philosophies and yield sources: native yields, balance sheet expansion, and yield structure restructuring. But they collectively indicate one thing: the competitive focus of DeFi has shifted from mere protocol design to the competition of asset management capabilities and yield organization abilities.

III. The Shift in Yield Structure Fuels a Paradigm Shift in the DeFi Industry

The current changes in DeFi's yield structure are not simply reflected in a single protocol or product, but the entire industry is undergoing a systemic evolution. From yield sources to asset allocations, from protocol positioning to competitive logic, DeFi is gradually moving away from the early development model reliant on on-chain intrinsic yields to evolving into a more mature asset management system.

3.1 Yield Sources Are Shifting from Singular to Diverse

In the early stages of DeFi, yields were almost entirely derived from on-chain financial activities. Lending interests, trading fees, funding rates, and liquidity incentives collectively constituted the main sources of protocol income. This model boasts advantages such as high capital efficiency and full on-chain operation, but it also implies that yields are highly dependent on market activity levels. When markets enter a downturn, borrowing demands decrease, trading volumes shrink, and funding rates fall, leading to a corresponding reduction in protocol revenues.

In recent years, with the rapid development of RWA, DeFi's yield sources have begun to diversify. In addition to traditional lending yields, real-world assets like U.S. Treasuries, money market funds (MMF), investment-grade credit bonds, and private credit have started to become new sources of yields. At the same time, yield strategies from funding rates, staking rewards, basis trading, etc., have continuously enriched the yield structure of protocols.

The increase in yield sources not only enhances the protocols' ability to withstand market cycle fluctuations but also makes it possible for DeFi to allocate yield-generating assets across different markets for the first time. For users, yields are no longer derived solely from the crypto market but are beginning to share cash flows generated from real-world assets; for protocols, the new focus is how to continuously acquire high-quality yields from different markets.

3.2 Protocols Are Shifting from Product-Driven to Asset-Driven

Behind the changing yield sources lies a deeper shift in the operational modes of protocols. Early DeFi protocols, once they launched lending, DEX, or stablecoin functions, could naturally obtain revenues as long as market trading was active. Therefore, competition among protocols centered more on product features, user experience, and liquidity, while the importance of asset management capabilities was relatively limited.

As yield sources gradually expand to off-chain assets, more and more protocols are beginning to actively manage assets rather than passively awaiting yield generation. Protocols need to continuously adjust asset allocation ratios according to market conditions, dynamically balancing between on-chain borrowing, RWAs, stablecoin reserves, credit assets, and liquidity to achieve the optimal combination of yield, risk, and liquidity.

This change allows DeFi protocols to begin resembling asset management institutions. Asset allocation is no longer just a risk management tool, but has become a core capability for generating yields. In the future, differences between protocols will stem more from their asset acquisition capabilities, allocation capacities, and ability to continuously generate cash flows, rather than just their functional designs.

3.3 DeFi Is Becoming an On-Chain Distribution Platform for TradFi Yields

In addition to changes in yield sources and asset allocation strategies, DeFi's role within the entire financial system is also undergoing a transformation. In the past, DeFi primarily served as on-chain financial infrastructure, providing lending, trading, derivatives, and other financial services, with revenues mainly coming from internal fund circulation within protocols. As more and more real-world assets enter the chain, DeFi starts to assume new responsibilities — becoming an important channel for distributing TradFi yields to global users.

In this process, protocols are no longer just yield creators but more like yield organizers and distributors. One end connects to real-world yield sources like U.S. Treasuries, money market funds, and credit assets, while the other end connects global on-chain users, completing yield calculations, asset management, and yield distribution through smart contracts. Traditional financial markets generate cash flows; DeFi is responsible for bringing these yields onto the chain in an open, transparent, and composable manner.

This change signifies that the relationship between DeFi and TradFi is shifting from competition towards integration. In the future, they are more likely to form a collaborative relationship: TradFi provides stable and sustainable underlying yield assets, while DeFi offers a global, programmable distribution network, jointly constructing a new generation of on-chain financial systems.

3.4 The Next Phase of Competition Will Focus on Yield Organization Capabilities

As yield sources, asset allocation strategies, and protocol roles change, the competitive logic of DeFi also transforms.

In the past, a protocol's success depended more on metrics like TVL, APY, trading volumes, and product functionalities. High yields, high liquidity, and rapid user growth often became core competitive advantages for protocols. However, as the industry matures, these metrics are becoming increasingly difficult to form long-term barriers.

In the future, the more important competitive advantage will stem from yield organization capability. This ability involves not only acquiring quality assets, designing yield products, and continuously generating cash flows, but also establishing stable collaborative networks, comprehensive risk management systems, and efficient yield distribution mechanisms. The focus of competition between protocols will shift from merely comparing yields to measuring yield stability, sustainability, and risk-adjusted overall returns.

From this perspective, DeFi is experiencing a paradigm shift from "financial product competition" to "asset management competition." Those who can continuously acquire high-quality assets, properly allocate different yield sources, and establish reliable yield distribution systems are more likely to become core platforms for the next stage of industry development.

IV. The Risk Pricing System Reconstruction Behind Yield Migration

Increasingly, DeFi protocols are incorporating real-world assets like U.S. Treasuries, money market funds, and private credit into their yield systems. However, the migration of yield sources has not eliminated risks; instead, it has altered the origins, transmission paths, and pricing mechanisms of risks. In the past, DeFi focused more on smart contracts, oracles, and liquidation mechanisms; today, protocols are beginning to face traditional financial issues related to asset quality, credit risk, liquidity management, and compliance operations that have long existed. As the yield structure changes, the entire industry's risk pricing system is also undergoing a profound reconstruction.

4.1 Risks Are Shifting from the Code Layer to the Asset Layer

Early DeFi risks primarily stemmed from the technology itself. Smart contract vulnerabilities, oracle anomalies, cross-chain bridge attacks, volatile collateral prices, and liquidation mechanism failures almost constituted the main sources of risks for the industry. Therefore, whether or not a protocol is trustworthy largely depends on whether the code has been adequately audited, how robust the liquidation mechanisms are, and whether the protocol has withstood the test of market cycles.

As more protocols begin to incorporate real-world assets, risks are gradually shifting from the code layer to the asset layer. For protocols allocating assets such as U.S. Treasuries, money market funds, and private credit, smart contracts remain important, but the true determinants of yield stability have become the underlying assets themselves. The existence of assets, the sustainability of yields, the ability of issuers and custodians to fulfill obligations, and the accuracy of asset valuation all become important factors affecting the safety of protocols.

This change indicates that the object of risk management in DeFi has gradually expanded from on-chain infrastructure to the entire asset lifecycle; protocols not only need to ensure code safety, but also continuously manage asset quality, partner institutions, and underlying investment portfolios.

4.2 Credit Risk Has Reemerged as a Core Variable of DeFi

If asset-layer risks are a direct result of the migration of yields, credit risk represents the fundamental change following the entry of TradFi yields into DeFi.

Traditional DeFi mostly adopts over-collateralization mechanisms. Whether it's ETH, BTC, or mainstream stablecoins, their risks often stem more from price volatility than from credit defaults. Therefore, protocols mainly rely on collateral rates and liquidation mechanisms to manage risks, requiring little to no judgment on the borrower's credit quality. However, when yields begin to derive from U.S. Treasuries, money market funds, investment-grade bonds, private credit, or other real-world assets, credit once again becomes a significant component of the entire yield system. For instance, Treasury yields correspond to sovereign credit; money market funds rely on the operational capabilities of fund managers and custodial institutions; private credit calls for constant assessment of borrowers’ repayment capabilities and default probabilities. For protocols, the higher the yield, the more likely they are to take on higher credit risks instead of just market volatility risks.

Thus, in the future, DeFi protocols need to establish a comprehensive credit assessment system rather than merely a risk control system. From asset screening, partner selection, to investment portfolio management, credit analysis will gradually become an important component of a protocol’s asset management capabilities.

4.3 Liquidity Management Will Become More Important Than Yield Rates

Yield rates have always been the most关注的指标 in DeFi, but for long-term funds, what truly determines asset allocation willingness is often not the APY but rather liquidity.

Traditional DeFi products generally allow instant redemptions because the underlying assets themselves possess high liquidity. However, when protocols start allocating real-world assets like U.S. Treasuries and private credit, the underlying assets naturally include term structures and redemption cycles, meaning protocols must seek a new balance between yield rates and liquidity. To meet users' demands for on-demand redemptions, protocols typically need to maintain a certain percentage of cash reserves or highly liquid assets, establishing liquidity buffers. When a market sees significant redemptions, these liquidity reserves can reduce the risks of forced asset sales and mitigate the impact of yield fluctuations on user experiences.

Therefore, for future yield-generating stablecoins, the importance of liquidity management may even surpass that of yield rates themselves. Those who can achieve more efficient fund allocation and liquidity management while maintaining stable yields are more likely to gain recognition from long-term institutional funds.

4.4 DeFi Is Establishing a New Risk Pricing System

The shifts in yield sources, changes in asset allocation methods, and increasing demands for liquidity management are collectively pushing DeFi to establish a new risk pricing system.

In the past, protocol risks mainly revolved around the on-chain ecosystem. Risk assessments focused more on code security, protocol mechanisms, and market volatility; in the future, risk models will need to include multiple dimensions such as asset credit, custodial arrangements, legal structures, liquidity management, regulatory environments, and partnerships. This signifies that DeFi and TradFi are forming a closer collaborative relationship: TradFi provides underlying assets and stable yields, while DeFi offers globalized, programmable asset management and yield distribution capabilities. For protocols, introducing TradFi yields does not simply mean adding a new asset class but requires re-establishing a comprehensive management framework covering assets, risks, liquidity, and governance.

Therefore, the real competition in the next phase of DeFi isn’t merely about providing higher yields but establishing a long-term balance between yields, risks, liquidity, and transparency. Those who can continuously acquire quality assets, accurately identify risks, reasonably allocate funds, and establish trustworthy yield distribution systems are more likely to become core platforms for on-chain asset management in the next stage.

V. Future Competition in DeFi Will Center Around Asset Management Capabilities

Looking back at DeFi's development journey, one can see that every significant evolution in the industry essentially corresponds to an upgrade in value creation methods. During the liquidity mining era, the core of competition was who could attract more funds to enter the protocol; following the rapid development of lending and derivatives, competition gradually shifted towards capital efficiency and protocol income; as more real-world assets begin to enter the chain, the focus of DeFi competition is also experiencing new changes.

5.1 Asset Management Capabilities Will Become the New Competitive Barrier

In the past, most DeFi protocols focused more on the liability side, that is, how to attract more users to deposit assets, expand stablecoin issuance, or increase protocol TVL. However, as yield sources gradually diversify, simply having capital scales is no longer sufficient to form long-term competitive advantages.

In the future, what will be more important is the asset management capabilities. Here, asset management does not merely involve allocating U.S. Treasuries or RWAs, but also establishing systematic management capabilities around the entire asset lifecycle, covering multiple aspects such as quality asset acquisition, yield source selection, credit risk assessment, liquidity management, asset portfolio optimization, and ongoing yield distributions.

From this perspective, outstanding DeFi protocols in the future will increasingly resemble digital asset management institutions with global asset allocation capabilities. The focus of protocol competition will gradually shift from product design capabilities to asset management abilities.

5.2 Yield Competition Will Gradually Shift to Comprehensive Capability Competition

In the past few years, the DeFi market has been accustomed to judging whether a protocol is attractive based solely on its APY. However, with more institutional funds entering the chain, relying solely on yield rates has become challenging to establish a long-term competitive advantage. For long-term funds, determining whether a yield product is worth allocating hinges less on the yield itself and more on whether the yields are stable, assets are transparent, liquidity is sufficient, and risks are manageable.

In the future, competition among protocols will not only center on yield rates but will instead focus on comprehensive capabilities. This comprehensive capability includes at least four aspects:

First, Asset Acquisition Capability. Whether a protocol can continuously access quality U.S. Treasuries, money market funds, credit assets, and other real-world yield sources will directly determine the quality of the yields.

Second, Yield Organization Capability. Different assets have varying yield cycles, risk characteristics, and liquidity requirements; protocols need to continually optimize asset allocation to achieve more stable cash flows.

Third, Risk Management Capability. Protocols need to set up a complete management system covering credit risks, liquidity risks, custodial risks, and governance risks, rather than relying solely on smart contract safety.

Fourth, Yield Distribution Capability. How to continuously distribute protocol yields to users in a transparent, composable, and efficient manner will also become an important component of future product competition.

It is foreseeable that the truly leading protocols in the future may not necessarily have the highest APY, but they are likely to possess the most stable and sustainable yield systems.

Conclusion

When examining the development of DeFi over the past few years in the context of a longer historical cycle, it becomes apparent that the entire industry is completing a role transformation. Early DeFi addressed the question of "how to facilitate financial transactions on-chain"; subsequently, the industry began to explore "how to create yields on-chain"; and now, more protocols are responding to a more crucial question—how to continuously manage assets and transparently distribute the yields generated from the real world to global users in an open, programmable manner. Overall, DeFi is evolving from yield protocols into an asset hub connecting on-chain funds with TradFi cash flows.

In this sense, the endpoint of the migration of DeFi yield structures is not merely about shifting U.S. Treasuries onto the chain or adding a yield rate label for stablecoins. It is about redefining the relationship between asset management, yield creation, and risk management within an open financial system. In the future, the truly leading protocols may not necessarily hold the highest yields but will definitely build more mature asset management capabilities, more robust risk control systems, and more transparent yield distribution mechanisms. This perhaps also marks an important starting point for DeFi's journey from "on-chain financial protocols" towards a "global open asset management platform."

About Us

Hotcoin Research, as the core investment research institution of Hotcoin Exchange, is dedicated to transforming professional analysis into your practical tools. Through "Weekly Insights" and "In-depth Research Reports," we analyze market contexts for you; leveraging our exclusive column "Hotcoin Selection" (AI + expert dual screening), we pinpoint potential assets and lower error costs. Each week, our researchers also engage with you through live broadcasts to interpret hot topics and predict trends. We believe that warm companionship and professional guidance can help more investors navigate cycles and capture the value opportunities of Web3.

Risk Warning

The cryptocurrency market is highly volatile, and investing inherently carries risks. We strongly advise investors to understand these risks thoroughly and to invest within a strict risk management framework to ensure fund safety.

Website: https://www.hotcoin.com/zh_CN/learn/index/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。