TL;DR

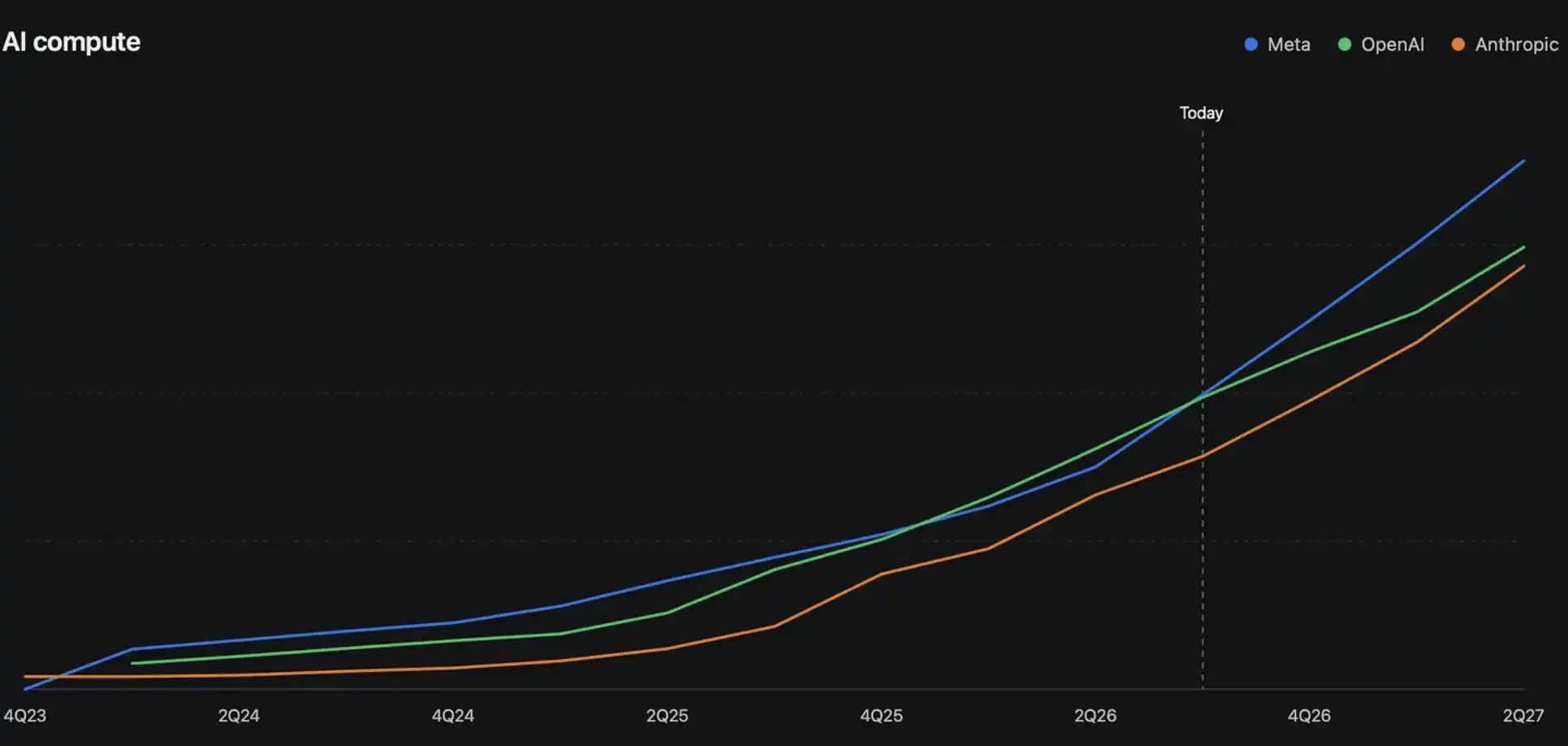

- SemiAnalysis bets that Meta may surpass Google in the next 6 months, becoming the strongest contender after OpenAI and Anthropic.

- This judgment is based on the $14.3 billion Scale AI deal, RL data production, and multi-GW computational power expansion.

- Muse Spark 1.1 still has not caught up with leading models; whether Meta can catch up with Google depends on the performance of next-generation models.

SemiAnalysis presents an aggressive judgment in its latest report: the Meta superintelligence lab is not yet a winner in leading models, but if talent, reinforcement learning data, and computational power expansion are realized simultaneously, it has the opportunity to surpass Google and become the most competitive contender after OpenAI and Anthropic within the next 6 months.

This is not to say that Meta has already caught up. Meta launched Muse Spark in April, and on July 9, Axios reported that Muse Spark 1.1 has opened its API to developers, priced at $1.25 per million input tokens and $4.25 per output token. Axios noted that this is not the "breakthrough" model Meta was expecting; the larger model codenamed Watermelon is still being trained.

SemiAnalysis bets on another point: after the setback with Llama 4, Zuckerberg is restructuring the AI organization more aggressively, channeling money, talent, internal engineering resources, and data center capacity into the superintelligence lab. The core divergence in the report is whether Google can still hold its position as the AI third pole.

Current models are not strong; the report bets on a 6-month catch-up speed

After the introduction of Muse Spark, the Meta superintelligence lab has not recreated the sense of leading in open source that characterized the Llama 3 and Llama 3.1 periods. According to SemiAnalysis's tests and judgments, Muse Spark and its subsequent versions still struggle to be considered leading in most benchmark tests and general intelligence scenarios.

This is also where this report needs to be limited. Muse Spark 1.1 is roughly comparable to Opus 4.6 or GLM 5.2, with details such as internal token usage not yet migrating, belonging to the author's tests and model judgments, not official Meta statements. At least from public information, Meta has not yet put forward a model that can directly challenge OpenAI and Anthropic.

However, SemiAnalysis focuses on the slope. After Llama 4's failure, the Meta superintelligence team has completed a significant adjustment, and the short-term organizational chaos is being absorbed. The report judges that if the next round of model training and reinforcement learning data production starts to reflect in products, Meta's position may be more advanced than the current rankings suggest.

$14.3 billion Scale AI deal fills the most scarce personnel for leading models

Meta's most noticeable move is the $14.3 billion investment in Scale AI. Multiple media outlets including Fortune, Forbes, and Reuters have previously reported that Meta has introduced Scale AI founder Alexandr Wang through this deal and has him join or lead teams related to superintelligence.

In the competition for leading models, this deal is not just about acquiring a data labeling company but more like a high-intensity talent acquisition. Scale's security, evaluation, and alignment team SEAL is viewed by SemiAnalysis as an important source for Meta to enhance its evaluation, alignment, and post-training capabilities.

Reuters has also mentioned that Meta is offering some AI engineers multi-hundred-million-dollar compensation packages. This figure indicates that Meta has prioritized superintelligence at the company level, rather than ordinary AI product iterations. For a large tech company, the real challenge is not securing the budget, but aligning research, product, infrastructure, and management around a single goal.

SemiAnalysis cites Alexandr Wang’s recent statements in a podcast, saying that true leading laboratories often first believe that superintelligence is close, with subsequent business decisions following this judgment. The report interprets Meta's recent moves as a shift towards the AGI priorities seen with OpenAI and Anthropic.

3,000 engineers shifting to RL, Meta wants to turn internal work into training data

Beyond personnel, reinforcement learning tasks and real work data are the second line.

Today, model capability enhancement relies not only on pre-training corpora. More crucially, can models complete tasks in environments closer to real work: understanding context, utilizing tools, executing tests, fixing errors, and iterating based on results? Code library fixes, product analysis, and internal tool usage will be closer to the true difficulty of white-collar work than standard exam questions.

SemiAnalysis states that Meta has reassigned approximately 3,000 engineers to become full-time RL task creators. This figure still needs to be understood according to the report's standards, but if executed properly, Meta's advantage will become clear: it is not simply outsourcing to purchase artificial data, but transforming its engineering organization into a production line for training tasks.

This type of data is particularly important for agents. Many reinforcement learning tasks appear difficult, but the prompts have overly detailed steps that do not align with real work habits. Screen recordings, daily workflows, tool usage records, and internal evaluation systems may better suit training models that can automate white-collar work.

This is also one of the reasons the report is optimistic about Meta catching up to Google. Google has DeepMind, Gemini, TPU, and cloud business, but Meta is concentrating internal organization, data, and engineering capabilities on the same model objectives.

Multi-GW computational power expansion positions Meta at the leading table

Computational power is the third line. SemiAnalysis stated in a July 2 article that Meta signed contracts for over 5GW of capacity in the first half of this year, accumulating nearly 10GW of transactions since 2024, and judging that the bulk of new capacity will still flow to the Meta superintelligence lab.

For ordinary investors, the focus is not on specific data center designs, but rather on the direction of capital expenditure. Meta’s expansion of computational power is not for regular cloud services but is aimed at preparing larger-scale clusters for internal model training, post-training, and agent cyclic preparation. The heavier training and reinforcement learning become, the faster computational power deployment will impact model iteration speed.

The report also mentions infrastructure plans for inter-regional connectivity and rapid data center deployment. These details still belong to SemiAnalysis's model projections, but the direction is clear: Meta is trading infrastructure for time.

The debate surrounding Google does not concern whether there’s computational power, but how that power is allocated. SemiAnalysis predicts that a significant portion of the new data center capacity serving Google will be directed towards IaaS and third-party API businesses, and that the concentration of resources available for leading training at DeepMind may be lower than the outside world imagines. Even if Google expands more AI infrastructure through external financing or capital markets, new capacity may be partially consumed by cloud clients.

Thus, the report provides a more controversial judgment: the competition for the third spot in AI is no longer about Google firmly holding its place, but may turn into a reshuffling among Meta, Google, and other high-computational-power players.

The biggest problem remains that Meta has not produced a leading model

The most impactful part of this report is also the riskiest: it is betting on the next 6 months, not on results that have already happened.

Meta has already secured the $14.3 billion Scale AI deal, Alexandr Wang's participation, multi-hundred-million-dollar compensation packages, multi-GW computational power expansions, and a shift of internal engineering resources towards RL tasks. But these are still conditions for catching up, not victories of the model itself.

Muse Spark 1.1 currently cannot prove that Meta has entered the position occupied by OpenAI and Anthropic. Larger models like Watermelon are still in training, and actual capabilities, costs, availability, and developer feedback have yet to be tested by the market.

Google has not exited the table either. DeepMind, TPU, Gemini, and cloud business remain hard advantages. The real divergence lies in the fact that Google’s resources must serve search, cloud, API clients, and internal models simultaneously, while Meta is channeling more resources into the superintelligence lab.

If Meta’s next-generation model does not show significant improvement, the $14.3 billion spent on talent acquisition and large-scale computational power investment will become heavier capital expenditure pressure. If new models and agent products are realized, only then will the third position in AI truly be at risk.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。