On July 11, Robinhood Chain's early top Meme launch platform NOXA suspended new token issuance. Two days later, the original website was temporarily inaccessible; the static entry point enabled on July 14 only retained functions for browsing historical projects, existing trading, and collecting creator fees. On July 15, NOXA further announced that it would no longer collect follow-up trading fees and would transfer all trading income to creators. As of the time of writing, its new issuance has not yet resumed.

NOXA's exit speed almost matched its rise speed. After the mainnet launch of Robinhood Chain, the platform quickly gathered creators, traders, and fee income through CASHCAT. The official attention and dissemination from Robinhood further reduced the cold start costs for early native projects. NOXA created a total of over 60,000 tokens, accumulating fees close to $12 million; however, after halting new issuance, the project supply quickly turned to Pons.family, Flap, and other entry points.

CoinW Research Institute believes that the Robinhood Chain launch platform has entered a high supply, low conversion stage. Data from Dune indicates that on July 16, the entire chain added 42,709 tokens, with Pons.family and Flap accounting for a total of 50.30%; as of the time of writing, there are only 18 tokens with a market value exceeding $1 million, most of which come from NOXA and Virtuals. The issuance entry has shifted towards Pons and Flap, while high market value projects remain concentrated on platforms that formed wealth effects in the previous stage. No new absolute leader has emerged after NOXA's exit, and subsequent rankings will largely depend on effective graduation rates, million-dollar token output, and market value retention.

1. NOXA's First-Mover Advantage Did Not Form a Stable Barrier

NOXA experienced only a short market cycle from leading to halting issuance. The platform's rise relied on first-entry access, representative projects, amplified by official Robinhood support and buyer attention; once new projects stopped entering, this growth loop was interrupted.

1.1 How CASHCAT Helped NOXA Establish Its First Round of Advantage

Robinhood Chain opened its public mainnet on July 1. The network uses the Arbitrum Platform, supporting a latency of about 100 milliseconds and compatible with EVM development tools. Uniswap v2, v3, v4, and UniswapX were synchronously accessed upon the mainnet launch, allowing developers to directly deploy token contracts, establish public liquidity, and quickly enter trading paths with wallets and aggregators.

NOXA linked token creation directly to Uniswap v3's unilateral liquidity. New projects entered public pricing from the first transaction, enabling creators to earn trading fees from within the pool, while manual pool creation and subsequent migration steps were correspondingly reduced. At a time when other launch platforms had not yet formed stable products, this process first met the new coin issuance demands of the Robinhood Chain.

NOXA's first-round advantage did not solely stem from its product mechanism. CASHCAT connected Robinhood's early brand narrative, on-chain community, and short-term trading demand; the official attention and dissemination from Robinhood further amplified project exposure, community trust, and inclusion of trading tools. Price and transaction growth subsequently drew attention back to NOXA: creators sought to reach existing buyer networks and leaderboard traffic, while traders gradually viewed NOXA as an important entry point for discovering new coins on Robinhood Chain. Representative projects, official support, and platform traffic thus formed an inter-reinforcing cold start loop.

1.2 Halting Issuance Cuts Off New Project Supply, Existing Assets Remain Operational

NOXA attributed the suspension of new issue to rampant duplication by bots and low-quality tokens flooding the market. After the original domain was interrupted, the team migrated the historical interface to the ENS entry, allowing browsing and trading of existing projects, and creators could continue to receive fees. The fee adjustments on July 15 further confirmed the platform's contraction direction: NOXA stopped collecting follow-up trading fees and transferred all revenue to creators, equivalent to retaining historical contracts and trading channels while giving up continuous monetization from the platform side. For existing projects, tokens and liquidity pools remained operational; for NOXA, the growth loop composed of new projects, platform income, and leaderboard updates has now been interrupted.

This indicates that the traffic loop of launch platforms relies on continuous supply. Platforms must not only continually introduce projects but also maintain rankings, connect trading tools, and consistently output content to the market. Once new projects stop entering, creators lose access to existing buyer networks, and traders will turn to platforms that are still updating.

1.3 NOXA Exposes Three Shortcomings of Early Launch Platforms

First, representative projects can quickly amplify platform traffic but will also increase the platform's dependency on the行情 of a single asset. CASHCAT helped NOXA establish market recognition, but when the representative projects declined, the platform halted issuance, and market sentiment weakened simultaneously, the transaction volume and user attention would also decline in sync.

Second, continuous operation itself has become a core competitive capability. If a platform halts its core operations during the most active market periods, creators' expectations for fee collection, contract maintenance, and product continuity will all be affected. Platforms with leader potential need to prove they can filter low-quality projects during supply peak periods while maintaining contracts, front-end, and project services.

Third, official support is an important variable for cold starts, but it cannot replace the independent growth of the platform. NOXA's early explosion indicates that Robinhood's official attention, brand collaboration, and channel dissemination can significantly enhance the exposure efficiency of native projects. Subsequently, platforms need to improve issuance and liquidity products, as well as strive for content distribution, event cooperation, and infrastructure access; more importantly, they must convert phase-based support into continuous project supply, real buyers, and repeatable market distribution capabilities.

2. Single-Day Addition of 42,709 Tokens, Only 18 Tokens Exceeding One Million in Market Value

2.1 In a Single Day, Over 40,000 Tokens, Which Platforms Concentrate the Million-Dollar Tokens?

Dune data shows that on July 16, Robinhood Chain added 42,709 tokens in a single day. Pons.family created 11,547 tokens, accounting for 27.04%; Flap created 9,935 tokens, accounting for 23.26%; the two together accounted for 21,482 tokens, or 50.30%, while other platforms accounted for a total creation of 21,227 tokens, or 49.70%. Pons and Flap remain the two main issuance entry points, together slightly exceeding half of the entire chain. However, as of this report's update, there are only 18 tokens with a market value exceeding one million dollars.

Table 1: Major Launch Platforms for Robinhood Chain - Token Issuance Scale and Million-Dollar Token Output

Platform or Scope | Issuance Volume | Number of Tokens Exceeding One Million in Market Value | Issuance Share | Market Value Results and Judgments |

11,547 tokens | 1 token | 27.04% | Only $PONS entered the leaderboard, market value output concentrated on a single project | |

Flap | 9,935 tokens | 0 tokens | 23.26% | Second in issuance volume, but no project has entered the million-dollar leaderboard yet |

NOXA | Stopped new issuance | 10 tokens | — | 55.56% of the entire chain, leading in number of million-dollar tokens |

Virtuals | The dashboard didn't separate the daily amount | 5 tokens | — | 27.78% of the entire chain, second in number of million-dollar tokens |

Bullmarkets | The dashboard didn't separate the daily amount | 1 token | — | 5.56% of the entire chain |

Bowfun | The dashboard didn't separate the daily amount | 1 token | — | 5.56% of the entire chain |

Entire Chain | 42,709 tokens | 18 tokens | 100% | Million-dollar tokens are still highly concentrated on a few platforms |

Table 1 shows that the issuance share and market value results have formed two distinct rankings. Pons and Flap together contributed 50.30% of the newly issued tokens on July 16, but the latest million-dollar leaderboard is still mostly composed of NOXA and Virtuals projects; Pons currently primarily relies on its namesake token to form a high market value sample, while Flap has zero projects in the million-dollar category. The issuance entry is shifting towards Pons and Flap, but projects exceeding one million dollars remain primarily concentrated on platforms such as NOXA and Virtuals.

2.2 Pons, First in Issuance, but bot volume inflation Exists

Pons' public page shows approximately 21,454 tokens still in the curve stage, 110 graduated tokens, and a total of about 21,564 tokens created. Based on this, Pons' original graduation rate is about 0.51%. However, among the 110 graduated tokens, only $PONS is included in this time's million-dollar leaderboard, accounting for about 0.91% of graduated projects and 0.0046% of all created projects.

Meanwhile, on-chain data confirms that there seems to be bot-driven volume inflation in the Pons ecosystem. Here, "volume inflation" mainly refers to automated accounts repeatedly executing operations to create tokens, buy tokens, authorize transaction routing, sell tokens, and collect fees, causing the reported token creation numbers and on-chain transaction counts to rapidly increase within a short time frame.

Here are two verifiable addresses:

Address One: 0x7DE5b9C86D2B47607A2962043bB165f7BEFeB06b

Address Two: 0x7D22d3Dd32F00848A54eBE00c00a9082A18D4E66

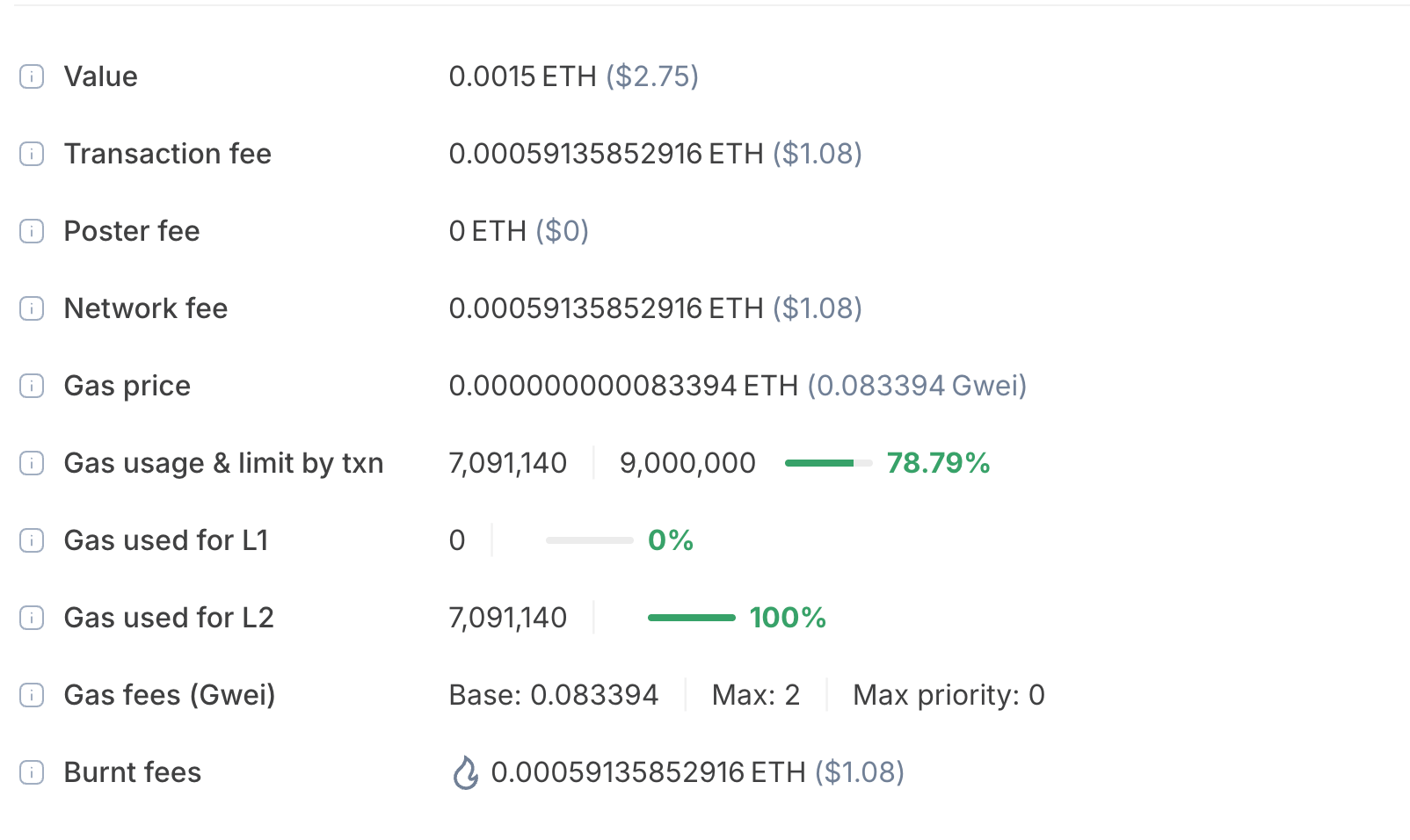

For example, in a significant amount operation on July 17, VLAD (contract address: 0x91e2ce85c223CD55b0Cf76Ca668a0e61ed696C6b) was created by the Pons issuance contract. At 00:23:51, 00:24:58, and 00:26:06, the two addresses consecutively purchased VLAD with the identical amount of 0.033333333 ETH in the same second. Each address invested approximately 0.1 ETH, totaling about 0.2 ETH for both addresses.

At 00:31:09, both addresses again sold all VLAD during the same second. Address One sold approximately 5,694,114.656 VLAD, converting to 0.101688749 WETH, and after routing fees, actually received 0.100671862 ETH; Address Two sold approximately 5,707,289.584 VLAD, converting to 0.106254208 WETH, and actually received 0.105191665 ETH.

Moreover, on July 17, addresses One and Two successfully called the Pons issuance contract 896 times and 886 times, respectively, creating a total of 1,782 tokens, each creation transaction set at a fixed amount of 0.0015 ETH.

A large number of standardized creation records and the two addresses concurrently purchasing and liquidating in the same second do not align with the characteristics of independent user manual operations, indicating that the related operations were executed by bots or automated scripts in bulk. Such actions inflate Pons' issuance and transaction numbers while dragging many tokens lacking subsequent operations into graduation rates. Hence, it can be concluded that there are apparent bot-driven volume inflations in Pons' issuance data.

2.3 Flap's Graduation Rate and Market Value Conversion Still Need Verification

Flap set a single-day issuance record of around 22,000 tokens on July 14. On July 16, its creation volume dropped to 9,935 tokens, accounting for 23.26% of the day’s total issuance across the entire chain, still making it the second-largest launch platform after Pons.

Dune statistics show that there are only 18 tokens with a market value exceeding one million dollars on the Robinhood Chain, with major positions still held by NOXA and Virtuals platforms. Although Flap quickly expanded its issuance scale, there are zero million-dollar projects. This indicates that its current advantages mainly focus on creation entry and project distribution, and whether it can further convert issuance scale into high market value projects still needs observation concerning the market values, liquidity, and natural retention of graduated tokens.

2.4 Comprehensive Judgment: Sustained Market Value Output Determines Platform Ranking

Pons' advantages are in issuance scale, its namesake representative token, and strong on-chain attention; its drawback is an original graduation rate of only about 0.51%, with bot-driven batch operations visible in the on-chain sample, causing some issuance numbers and transaction counts to diverge from real user demand. Currently, the projects entering the million-dollar leaderboard from Pons are mostly the platform's namesake tokens, with market value output concentrated on a single project. Flap has a more complete external distribution and protocol reuse but has zero million-dollar projects. Meanwhile, NOXA and Virtuals still occupy the majority of high market value project listings, indicating that the user base and wealth effects formed by historical representative projects have not been replaced by the new issuance scale. Therefore, after NOXA's exit, Robinhood Chain has yet to witness the emergence of a leading new head, and subsequent attention should focus on effective graduation rates, token market value, and retention rate.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。