Author: Ethan (@ethanzhang_web3), Planet Daily

On the morning of September 12, Beijing time, the U.S. federal funds rate market released a highly clear signal: the probability of the Federal Reserve cutting interest rates by 25 basis points at this month's meeting has risen to 93.9%. After five consecutive meetings of "holding steady," the market has finally welcomed a directional shift in monetary policy. Meanwhile, another gamble related to the future direction of the Fed over the next two years is quietly advancing: who will succeed Powell as the next Fed Chair?

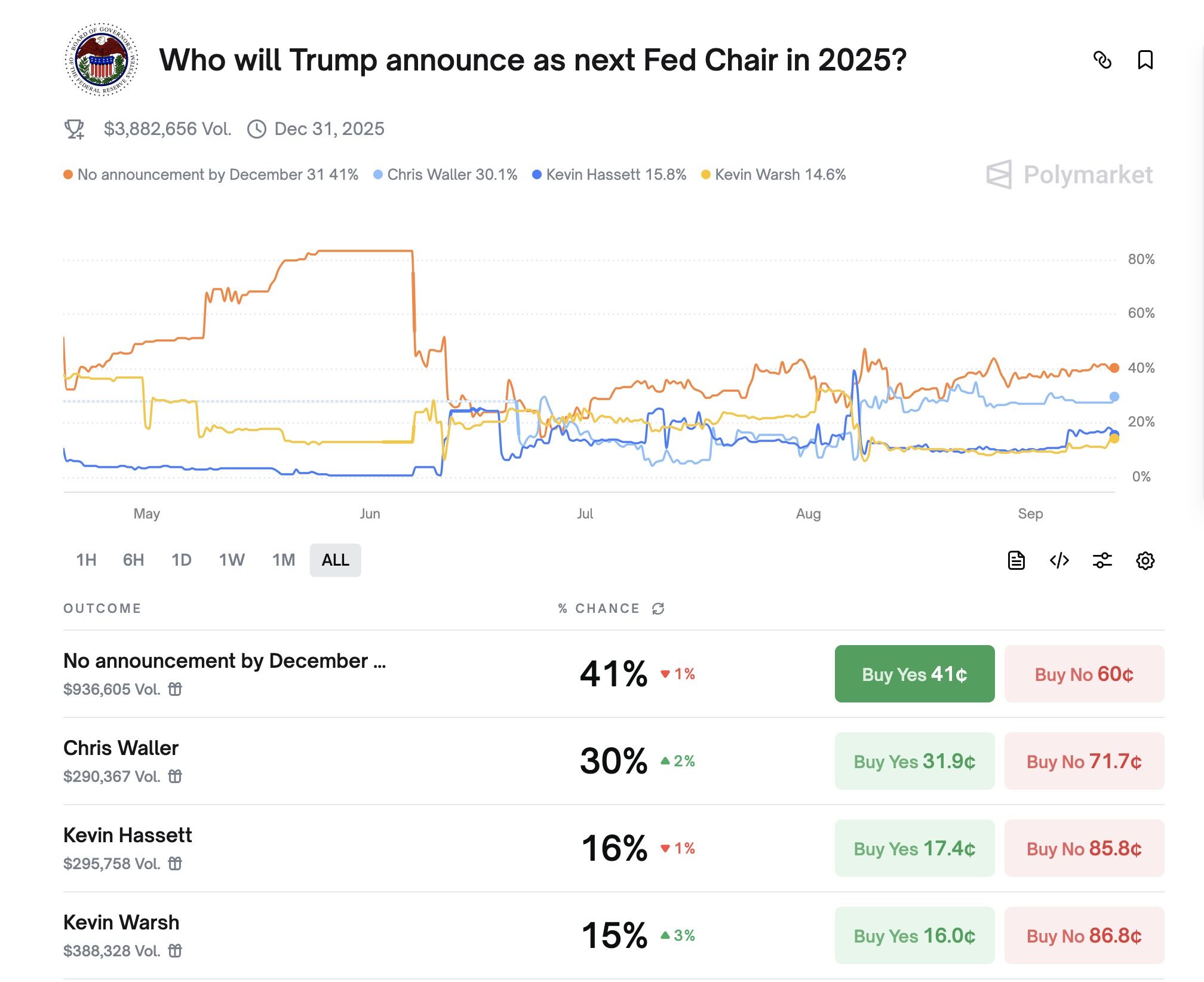

As of the same day on the decentralized prediction platform Polymarket, current Fed Governor Christopher Waller is leading with a 30% probability, ahead of the other two "Kevin faction" competitors—Hassett (16%) and Waller (15%). However, the market also retains a more dramatic possibility: the probability that "Trump will not announce a successor before the end of the year" remains the highest at 41%.

This series of data indicates that the market is simultaneously betting on two directions: one is the consensus path of interest rate cuts, and the other is the still uncertain battle for the monetary helm. In between these two, Waller's name repeatedly appears in various trading perspectives and policy games.

Why has the market begun to "believe in Waller"?

A story of a "non-typical Fed Governor": How a small-town professor was pushed to the forefront?

Waller's background and experience seem out of place within the Fed system. He is not from an Ivy League school and has not held key positions at Goldman Sachs or Morgan Stanley; he was born in a small town in Nebraska with a population of fewer than 8,000. Starting from Bemidji State University, he earned a bachelor's degree in economics. In 1985, he obtained a Ph.D. in economics from Washington State University and began a long academic career, teaching and researching at Indiana University, the University of Kentucky, and the University of Notre Dame for a total of 24 years.

Afterward, he spent another 24 years in academia researching monetary theory, focusing mainly on central bank independence, term structures, and market coordination mechanisms. It wasn't until 2009 that he left the campus to join the St. Louis Fed as the research director. In 2019, he was nominated by Trump to the Federal Reserve Board, a nomination process filled with controversy and a challenging confirmation process, but ultimately, on December 3, 2020, the Senate confirmed his appointment by a narrow margin of 48:47. At 61, Waller entered the highest decision-making body of the Fed, older than most governors, but this turned out to be an advantage; he had fewer burdens, owed no favors to Wall Street, and having spent time at the St. Louis Fed, he understood that the Fed is not a monolith—diverse opinions are not only tolerated but sometimes encouraged.

This path has allowed him to possess professional judgment while retaining the freedom to express himself without being categorized as a spokesperson for any particular faction. From Trump's perspective, such a figure might be easier to "use"; from the market's viewpoint, such a candidate signifies "less uncertainty."

However, in a power transition game intertwined with bureaucracy and political will, Waller is not the kind of candidate who is naturally favored by the market. His career trajectory is relatively academic and technical, not known for public rhetoric, nor does he frequently appear on financial television.

Yet, this very individual has gradually become a frequently mentioned "consensus candidate" in various market tools and political commentary. The reason lies in his threefold compatibility:

First, a flexible monetary policy style, but not speculative.

Waller is neither a typical "inflation hawk" nor a proponent of easy money. He advocates that policy should move with economic conditions: supporting preemptive rate cuts in 2019; favoring rapid rate hikes to curb inflation in 2022; and in 2025, amid economic slowdown and falling inflation, he became one of the first Fed governors to vote for rate cuts. This "non-ideological" policy style stands out as rare in the current highly politicized Fed landscape.

Second, clear political relationships and an extremely clean technical image.

Waller was nominated to the Fed Board by Trump in 2020 and is one of the few monetary policy officials within the Republican system who can achieve "technical neutrality" and "political compatibility." He is neither seen as "Trump's confidant" nor rejected by the party establishment, and this unique middle positioning grants him broader political maneuverability amid fierce partisan competition.

Unlike Hassett, who has a clear stance and strong party alignment, and Waller, who has close ties to Wall Street, Waller exhibits a more pure technocratic quality. He is more easily viewed as "a trustworthy professional," and in the context of highly polarized American politics, this depoliticized, capability-based image makes him a stable and easily accepted candidate for appointment.

Third, his attitude towards crypto technology shows a degree of "tolerance" within the system.

Waller is not a so-called "crypto believer," but he is one of the most vocal figures within the Fed system on topics such as stablecoins, AI payments, and tokenization. He does not advocate for government-led innovation and opposes CBDCs, but supports private stablecoins as tools for improving payment efficiency, suggesting that "the government should build the infrastructure like building highways, leaving the rest to the market."

In the space between traditional finance and digital assets, compared to the other two candidates, he may be the only Fed official clearly signaling "public-private collaboration."

Instinct and sense of timing: he knows when to speak and when to remain silent.

In July of this year, the Fed held its summer FOMC meeting. Although the market generally expected to "maintain interest rates," a rare scene unfolded: Waller and Michelle Bowman cast dissenting votes, advocating for an immediate 25 basis point rate cut.

Such "minority dissent" is not common within the Fed. The last occurrence of a similar situation was in 1993.

Two weeks before the vote, Waller had already released his stance at a central bank seminar at New York University. His public remarks clearly advocated that "current economic data supports a moderate rate cut." On the surface, this was a technical "advance communication"; but in terms of timing, it was a release of a political signal. At that time, Trump had been expressing mixed feelings towards Powell, previously attacking him on Truth Social, demanding "immediate rate cuts." Waller's vote and speech did not completely align with the president but also did not provide cover for Powell. He skillfully positioned himself between "policy adjustment" and "technical independence."

In a highly politicized Fed environment, a governor who knows how to gauge the situation and choose the right moment to express himself appears more leader-like.

Trump criticizes Powell for "poor and incompetent" management of the Fed building.

How should the crypto market react if he takes office?

The crypto market's interest in "who will steer the Fed" is not merely peripheral gossip but a triple reflection of policy expectations, market sentiment, and regulatory pathways. If Waller indeed ascends to the chair, we need to seriously consider how three types of roles will reprice the future.

First, for stablecoin issuers and compliant pathways, it represents a large-scale opening of the "regulatory dialogue window."

Waller has repeatedly stated in speeches that he opposes central bank digital currencies (CBDCs), claiming they "do not solve the market failures of the existing payment system," and instead emphasizes the advantages of private stablecoins (such as USDC, DAI, PayPal USD, etc.) in improving payment efficiency and cross-border settlements. He stresses that regulation should come from "Congressional legislation rather than agency expansion of power," calling for "these new technologies should not be stigmatized."

This means that if he becomes chair, projects like Circle, MakerDAO, and Ethena are likely to enter a "period of institutional clarity," no longer constantly caught in the gray area between the SEC and CFTC. More importantly, Waller's idea of "market-led, government-built" may prompt the Treasury, FDIC, and other supporting agencies to collaboratively develop a regulatory framework for stablecoins, promoting policies of "licensing, reserve standardization, and information disclosure standardization."

Second, for main chain assets like BTC and ETH, it serves as a "sentiment boost + regulatory easing" medium-term umbrella.

Although Waller has not publicly praised Bitcoin or Ethereum, he stated in 2024: "The Fed should not take sides in the market." This succinct statement implies that the Fed will not actively "suppress non-dollar systems," as long as they do not infringe upon payment sovereignty and systemic risk thresholds.

This will provide BTC and ETH with a "relatively mild regulatory cycle" window. Even if the SEC may still question their securities status, if the Fed does not aggressively push for CBDCs, does not block crypto payments, and does not intervene in on-chain activities, then market speculation and risk appetite will naturally improve.

In simple terms, in the "Waller era," Bitcoin may not receive "official endorsement," but it will benefit from a natural easing of regulatory pressure.

Third, for developers and DeFi native innovators, it represents a rare window of "dialogue with the central bank."

Waller has mentioned "AI payments," "smart contracts," and "distributed ledger technology" on multiple occasions this year, stating: "We do not necessarily have to adopt these technologies, but we must understand them." This stance is in stark contrast to many regulators who avoid or belittle crypto technology.

This opens an extremely important space for developers: they are not required to be accepted, but at least they are no longer excluded.

From Libra to USDC, from EigenLayer to Visa Crypto, generations of developers have found their communication with central bank regulators stuck in a "parallel universe" awkwardness. If Waller takes office, the Fed may become the first central bank leader "willing to engage in dialogue with DeFi natives."

In other words, crypto developers may welcome a starting moment for "policy negotiation rights" and "financial discourse rights."

Conclusion: Predictive trading prices the future, chair candidates price the direction

Whether "Waller will be the new chair" is still inconclusive. However, the market has begun to trade on "how he would price the future if he becomes chair." Moreover, the prediction market's 31% bet on him continues to rise, far exceeding that of his competitors.

At this juncture, it is certain that the expectations for interest rate cuts are moving towards realization; the crypto industry is seeking policy breakthroughs; and U.S. dollar assets are in a global "increased issuance of U.S. debt - high interest rates - risk appetite recovery" triangular game. Waller, as a politically acceptable, policy-predictable, and market-imaginable "successor," naturally becomes the focus of bets.

But perhaps there is another topic worth paying attention to: if he ultimately does not become the Fed chair, how will the market readjust these expectations? And if he truly takes office—the ranking competition for the "next generation dollar system" may just be beginning.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。