Original Title: Make revenue great again

Author: JoelJohn, Decentralised.co

Translation by: Riley, ChainCatcher

This article is organized from the piece "Make revenue great again" by JoelJohn, a columnist for Decentralised.co. As the crypto market shifts from frenzied speculation to rational returns, this article focuses on the core contradiction of token economics—should tokens be supported by real revenue? Do teams have an obligation to enhance token utility through buybacks? The article conducts an in-depth analysis from multiple dimensions, including market cycles, business models, and technological evolution, revealing the challenges and opportunities in the current crypto ecosystem.

ChainCatcher has compiled and organized this without altering the original meaning.

When people start to revisit the fundamentals, you know how bad the market conditions are. This article raises a core question: should crypto projects generate operational revenue through tokens? If the answer is yes, do teams have an obligation to initiate a token buyback mechanism? Like many complex issues, there is no standard answer—perhaps the future direction of the industry can only be reached through honest dialogue among all parties.

Life is just a game of capitalism.

This article is inspired by a series of conversations with Ganesh from Covalent, discussing the cyclicality of revenue, the evolution of business models, and whether protocol treasuries should prioritize token buybacks as a strategic focus. It serves as a supplement to Tuesday's article “Death to Stagnation in the Crypto World”.

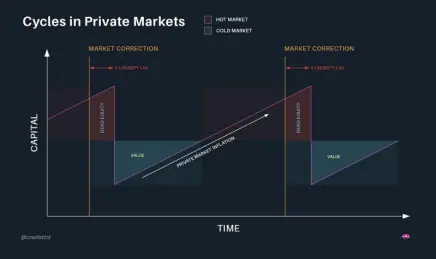

The private capital market (such as venture capital) always oscillates between liquidity excess and scarcity. When asset liquidity increases and external capital flows in, the market's euphoric sentiment drives up prices. Observing the market performance of newly listed stocks or newly issued tokens confirms this rule—liquidity expansion directly boosts asset valuations while stimulating investors to increase their risk appetite, giving rise to a new batch of startups. When underlying assets (like ETH, SOL) continue to appreciate, profit-seeking capital migrates to earlier-stage projects, attempting to surpass benchmark returns by betting on innovative targets; this migration of capital itself constitutes the underlying driving force of industry innovation.

This is a mechanism, not a loophole.

Source: https://x.com/credistick/status/1897688251667714300

The liquidity cycle in the crypto market is closely related to Bitcoin halving. Historically, a market rebound occurs within six months after a Bitcoin halving. In 2024, ETF inflows and Michael Saylor's (CEO of MicroStrategy) purchases have become a "demand black hole" for Bitcoin. Saylor alone spent 22.1 billion dollars on Bitcoin last year. However, the surge in Bitcoin's price has not driven up the prices of long-tail small-cap tokens.

We are in an era where liquidity providers are tight on funds, attention is dispersed across thousands of assets, and founders who have built token ecosystems over the years struggle to find meaning in their efforts. When the returns from issuing meme coins are higher, who will bother to develop valuable applications? In the previous cycle, L2 tokens gained valuation premiums due to exchange listings and VC endorsements. But as more players enter the market, this premium is being eroded.

As a result, the valuations of L2-held tokens are declining, limiting their ability to subsidize small products through grants or token revenues. Overvaluation forces founders to confront an eternal economic question—where does revenue come from?

Transaction is paramount

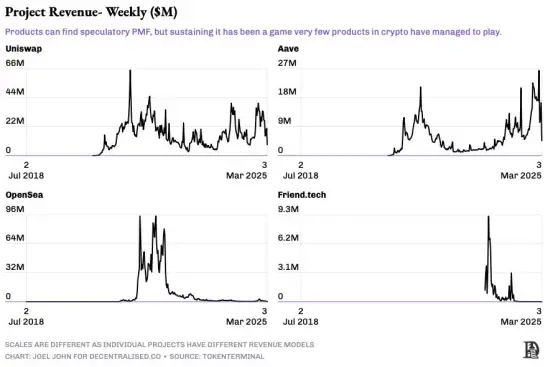

The above image clearly illustrates the typical revenue models in the crypto industry. For most products, the ideal state is like Aave and Uniswap. Benefiting from the "Lindy effect" (the longer something has existed, the greater the likelihood it will continue to exist), these two products have consistently generated revenue over the years. Uniswap can even generate revenue through front-end fees, reflecting the solidification of user habits—now, Uniswap has become the "Google" of decentralized exchanges.

In contrast, the revenues of FriendTech and OpenSea are merely quarterly. The NFT craze lasts about two quarters, while Social-Fi speculation only lasts two months. If the revenue scale is large enough and aligns with product goals, speculative revenue still makes sense. Many meme coin trading platforms have joined the "100 million+ fee club," which is the best outcome founders can expect through tokens or acquisitions, but for most, such success is often out of reach.

They are not developing consumer applications but focusing on infrastructure—where the revenue logic is entirely different.

From 2018 to 2021, VCs heavily invested in developer tools, hoping developers would bring in massive user bases. However, by 2024, the ecosystem has undergone two major shifts:

- Smart contracts have infinite scalability and require no human intervention: the team sizes of Uniswap or OpenSea do not need to expand with transaction volume.

- ****Advancements in LLM and AI have reduced reliance on crypto developer tools: this sector is facing a **revaluation.

The API subscription model of Web2 relies on a large online user base, while Web3 remains a niche market, with few applications reaching a million users. The advantage of Web3 lies in the high user revenue contribution rate: crypto users invest funds more frequently due to the characteristics of blockchain. In the next 18 months, most projects will need to adjust their business models to directly derive revenue from user transaction fees.

This idea is not new. Stripe initially charged per API call, and Shopify adopted a subscription model, later both shifted to revenue sharing. For Web3 infrastructure providers, this means capturing the market through low-price strategies—even offering services for free until a certain transaction volume is reached, then negotiating a revenue-sharing ratio. This is an idealized assumption.

Taking Polymarket's actual operations as an example: the core function of the UMA protocol token is dispute arbitration, and the number of disputes is positively correlated with token demand. If a transaction sharing mechanism is introduced, 0.10% of each dispute deposit could serve as a protocol fee. Based on a $1 billion betting scale for the presidential election, UMA could earn $1 million in direct revenue. Ideally, UMA could use this revenue to buy back and burn tokens, but this has its pros and cons.

MetaMask is another case. Its built-in exchange function has processed about $36 billion in transaction volume, generating over $300 million in revenue from just this feature. A similar logic applies to staking service providers like Luganode—fees are tied to the scale of staked assets.

But if the demand for API calls continues to weaken, why would developers choose a particular infrastructure provider? If revenue sharing is required, why choose a specific oracle? The answer lies in network effects. An infrastructure provider with multi-chain compatibility, millisecond-level data parsing accuracy, and indexing response speeds leading by three standard deviations will gain preferential selection when new projects launch—these technical parameters directly determine the migration costs for developers.

Burning to the ground

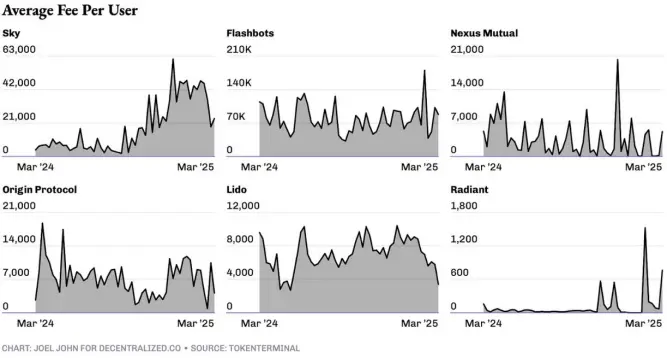

Linking token value to protocol revenue is not a new trend. Recently, several teams have announced buybacks or token burns based on revenue proportions, including Sky, Ronin, Jito, Kaito, and Gearbox.

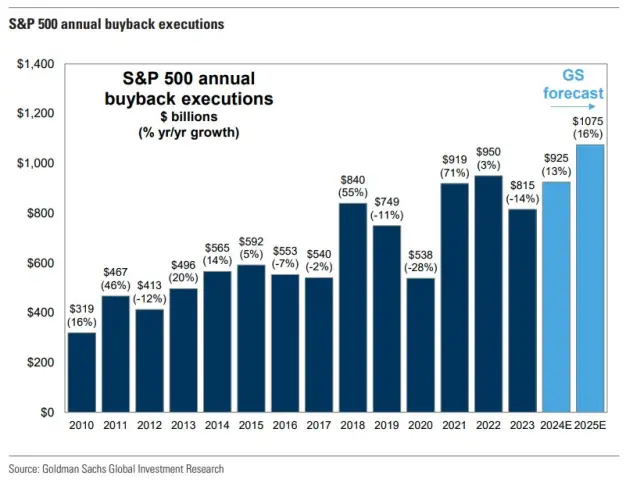

Token buybacks emulate stock buybacks in the US market, essentially returning value to shareholders (in this case, token holders) without violating securities laws. In 2024, the scale of stock buybacks in the US reached $790 billion, far exceeding the $170 billion in 2000. Before 1982, stock buybacks were considered illegal. In the past decade alone, Apple has spent $800 billion on stock buybacks. Regardless of whether this trend can continue, the market has clearly differentiated: tokens with cash flow willing to invest in their own value versus those with neither.

For early protocols or dApps, using revenue to buy back tokens may not be the best use of their funds. One viable solution is to allocate enough funds to offset the dilution caused by token issuance. The founder of Kaito recently explained their buyback strategy: this centralized company generates cash flow through enterprise clients and uses part of the funds to buy back tokens through market makers, with the buyback volume being twice that of newly issued tokens, thus achieving deflation.

Ronin, on the other hand, employs a different strategy: the blockchain adjusts fees based on transaction volume per block. During peak times, a portion of the network fees is directed to the treasury to control the asset supply rather than directly buying back tokens. In both cases, the founders have designed mechanisms to bind value to economic activity.

In the future, we will analyze the impact of such operations on token prices and on-chain behavior. However, what is currently evident is that as valuations are suppressed and VC funding in the crypto space decreases, more teams will compete for marginal capital inflows.

Since the essence of blockchain is a capital track, most teams will shift towards a revenue-sharing model based on transaction volume. If a project is already tokenized, the team can implement a "buyback-burn" mechanism. Well-executed projects will excel in the liquidity market, but this requires taking on the risk of buybacks during valuation bubbles. The truth can only be seen in hindsight.

Of course, one day, discussions about price, revenue, and income will once again become outdated—people will start pouring money into Doge and snatching up Bored Ape NFTs. But for now, founders concerned about survival have begun dialogues around revenue and destruction.

Creating value for shareholders, Joel John.

Disclaimer:

- This article does not constitute investment advice.

- Relevant personnel hold CXT tokens.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。