Author: VWin Ventures

TLDR:

Stablecoins are the value mapping of their underlying fiat currency on the blockchain, serving as a trading medium that links fiat currency and crypto assets.

The core scenarios for stablecoins are divided into trading and payment, enabling permissionless trading settlements for financial assets and commodity trade on a globally flattened blockchain clearing and settlement network.

Trading scenario: The market is concentrated at the top, with future growth coming from new financial assets being tokenized on-chain. The competitive landscape for stablecoins is gradually evolving from on-chain/exchange trading scenarios to a market contest for traditional financial transactions on-chain.

Payment scenario: Payments represent the largest incremental market for stablecoins currently, especially in cross-border remittances and local acceptance, where there is real and substantial demand. Stablecoins are encroaching on the core interests of traditional clearing systems represented by SWIFT and card organizations. Licensed financial institutions provide compliant and stable trading venues for customers.

Leading stablecoin players USDT and USDC initially gained traction through early channel and traffic binding, with later competition focusing on liquidity and ecosystem networks. Tether expanded early on through a distributed network reliant on black and gray markets, while Circle leveraged its compliant identity to expand into mainstream financial channels.

Dollar stablecoins essentially carry a new round of financial sovereignty of the dollar's "de-geographical" output, establishing a dollar network that circulates globally without traditional banks and central banks, promoting free flow of funds and concentration of assets. The U.S. can remotely control the global on-chain dollar flow through regulatory policies and KYC reviews, forming a new digital colonial model.

The Underlying Logic of Stablecoins – Shadow Dollars on a Global New Clearing and Settlement Network

Stablecoins initially addressed the value stability issue in the digital asset world, but fundamentally, they meet the global demand for "de-banked dollars." This digital dollar can flow freely 24/7, unrestricted by banking and central bank systems, quickly occupying the "gray areas" that banks cannot reach.

The U.S. extends the dollar into areas that traditional regulation struggles to cover by tacitly allowing private institutions to issue stablecoins, forming a decentralized yet essentially controllable "dollar digital colonial system."

Stablecoins represent a business of monetizing liquidity through credit. Creating a stablecoin means becoming a private "global central bank," with extremely low costs of attracting deposits and marginal expansion costs, while mastering bidirectional exchange fees, capital accumulation interest, and various underwater profit models. In the entire crypto industry, stablecoins are akin to "casino chips" and "mining shovels," serving speculative arbitrage, leveraged trading, and other "gray" demands; stablecoins are one of the few core businesses in the crypto industry with real long-term value.

The Core Scenarios of Stablecoins – Permissionless Trading Settlements for Financial Assets and Commodity Trade

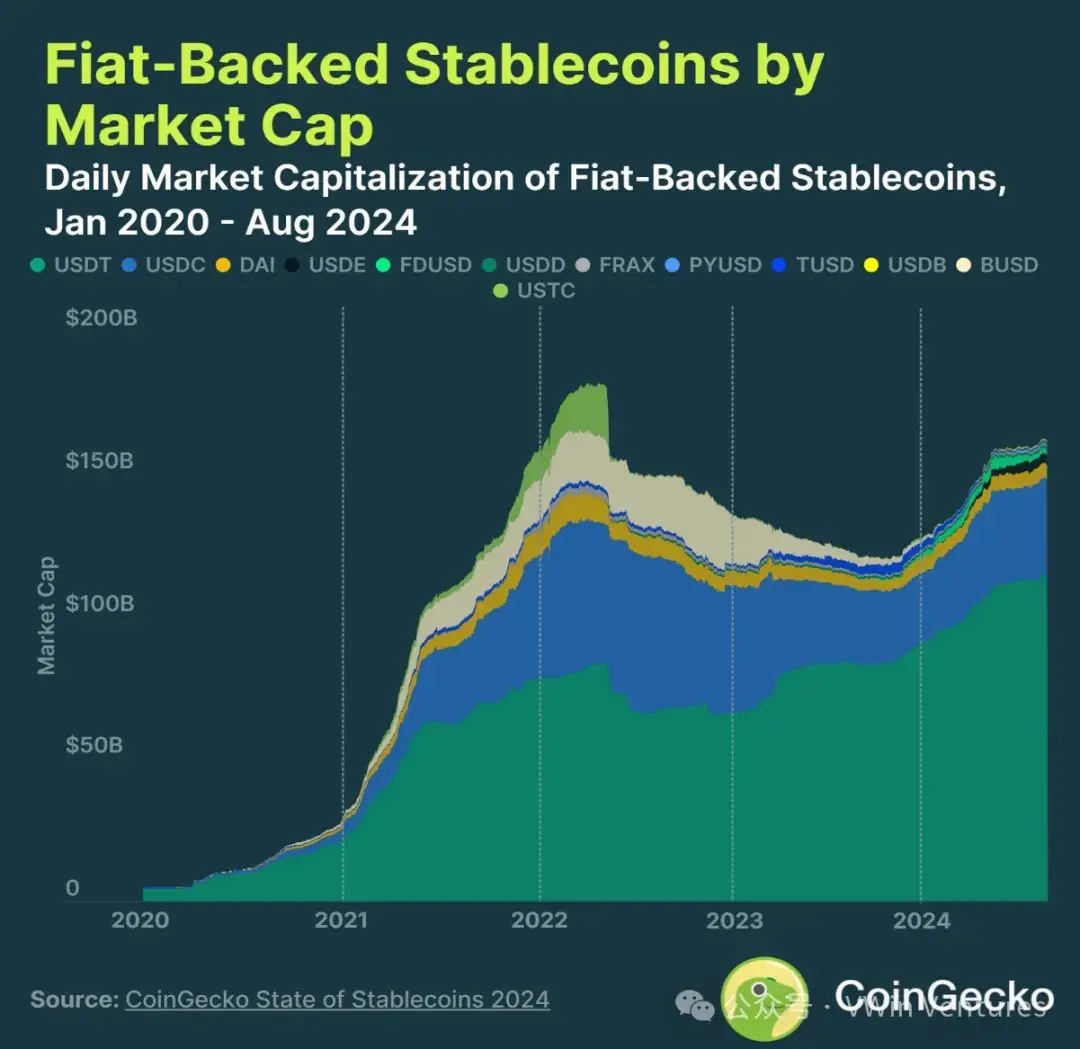

Currently, the total issuance of stablecoins exceeds $200 billion, primarily divided into two core scenarios: trading vs. payment.

Scenario 1: Trading Market (Dominated by Existing Supply, Strong Flywheel Effect)

In the trading scenario, stablecoins serve as safe-haven assets and trading mediums, currently trending towards concentration at the top, with USDT/USDC having a strong moat and evident network effects:

Existing market: Currently, there is a lack of high-quality assets on-chain to attract further liquidity, hindering the growth of stablecoins in trading scenarios, leading to fierce competition;

Incremental direction: Future growth points lie in tokenizing RWA (real-world assets), gradually evolving from standardized products (like bonds) to non-standard equity assets, creating new opportunities akin to a "Nasdaq on-chain";

New player opportunities: Capture new assets and new scenarios – for example, FDUSD is bound to Binance Exchange, leveraging specific vertical scenarios to build network barriers; or Ethena and Usual developing on-chain fixed-income financial products similar to Yu'ebao, seizing user financial demand through scenario-based entry points.

The future development of trading scenarios will gradually shift from purely trading tools to asset financialization and securities tokenization. Players will compete in resource integration and building scenario barriers.

Scenario 2: Payment Market (Current Largest Incremental Source for Stablecoins)

Compared to trading scenarios, the payment field holds greater potential for stablecoins, stemming from the conversion of existing traditional payment markets:

Cross-border payment demand: Especially in developing countries, where traditional financial systems are weak, stablecoins have a clear cost advantage and substantial demand, significantly impacting the monopoly of traditional banking systems.

Core competitive factors in payment scenarios: In stablecoin payment scenarios, credit endorsement and liquidity support are fundamental, with the core competition lying in building channel networks. Although the business models are relatively homogeneous, in the early blue ocean market, extending upstream and downstream can still capture asset-side or traffic-side dividends, forming bilateral network effects.

Path strategies:

Top-down: Circle obtains global compliance licenses, using official credit and first-mover advantages to promote traditional financial institutions' acceptance of USDC;

Bottom-up: Represented by USDT, it grows rapidly through local non-compliant financial institutions and OTC channels, quickly capturing market share, but with long-term compliance risks.

Compared to stablecoin issuers, channel distributors (such as payment companies, brokers, etc.) can also gain market expansion and customer acquisition benefits, focusing on downstream channel construction, creating regional distribution networks, capturing incremental market dividends, with early high gross margins, but market barriers are weaker than the network effects of issuers.

The Development Path of Leading Stablecoins – Growth Driven by Traffic, Success or Failure Dependent on Supply Chain

The core elements of competition for stablecoins are: 1. Credit endorsement; 2. Liquidity support; 3. Channel and customer acquisition capabilities. The competitive landscape for leading stablecoins has evolved from on-chain/exchange trading scenarios to market and channel contests in non-crypto scenarios like cross-border payment settlements.

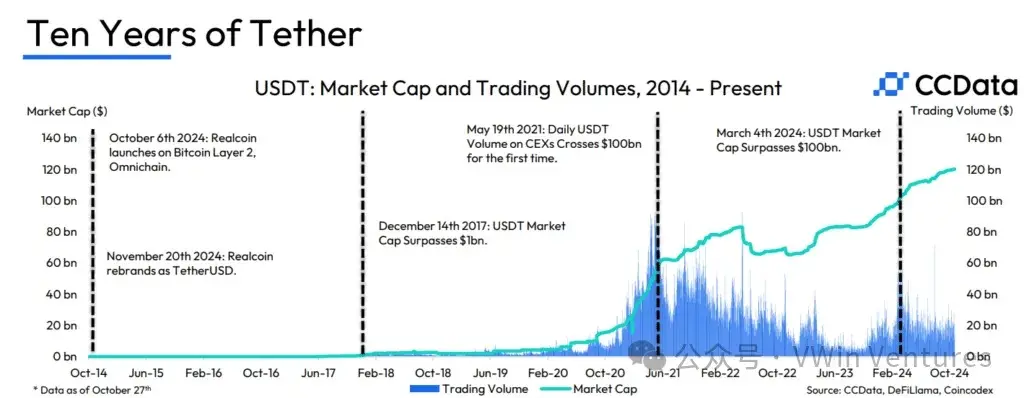

Tether (USDT issuer, with an issuance exceeding $140 billion and a market share of over 60%): Its development path mirrors the three stages of dollar development, naturally expanding through a distributed network reliant on black and gray markets in conjunction with the censorship-resistant Tron, forming a strong network effect.

Circle (USDC issuer, with an issuance exceeding $60 billion and a market share of over 25%):

Early binding with exchanges and public chains for cold starts (Coinbase & Base, Solana, Binance Launchpool);

Forming barriers through global compliance licenses, outlasting competitors (BUSD sanctioned by the U.S., MiCA expelling USDT in Europe), becoming the most credible compliant stablecoin in capital markets;

Continuously expanding compliant financial channels (exchanges, payment companies, banks) using compliance endorsement, capturing global incremental scenarios (payments, RWA, and new asset trading).

Circle officially submitted its IPO application to the U.S. SEC in April 2025, expected to become the first stablecoin target in the U.S. stock market; future major growth scenarios for stablecoins will come from cross-border trade and the on-chainization of global cross-border payments, with the compliant market being a larger incremental source. As a leading compliant stablecoin, USDC is favored by mainstream U.S. institutions and is expected to capture significant market share, with Circle likely to achieve substantial fundamental growth in the long term.

Future Challenges

Can Tether be compliant and "recruited"? To some extent, Tether has helped the dollar expand, becoming one of the top 20 U.S. Treasury investment institutions globally, while also having deep ties with Commerce Secretary Lutnick's former asset management company.

With the onset of a rate-cutting cycle, how to enhance diversified profitability as issuer interest income declines?

In a deregulated environment, more traditional financial giants (banks, payment companies, etc.) are entering the compliant competition track; how much longer will Circle's compliance lead enjoy dividends?

Payment Scenarios Become the Main Battlefield for Future Stablecoin Competition, with Cross-Border Payment On-Chainization Having Huge Growth Potential

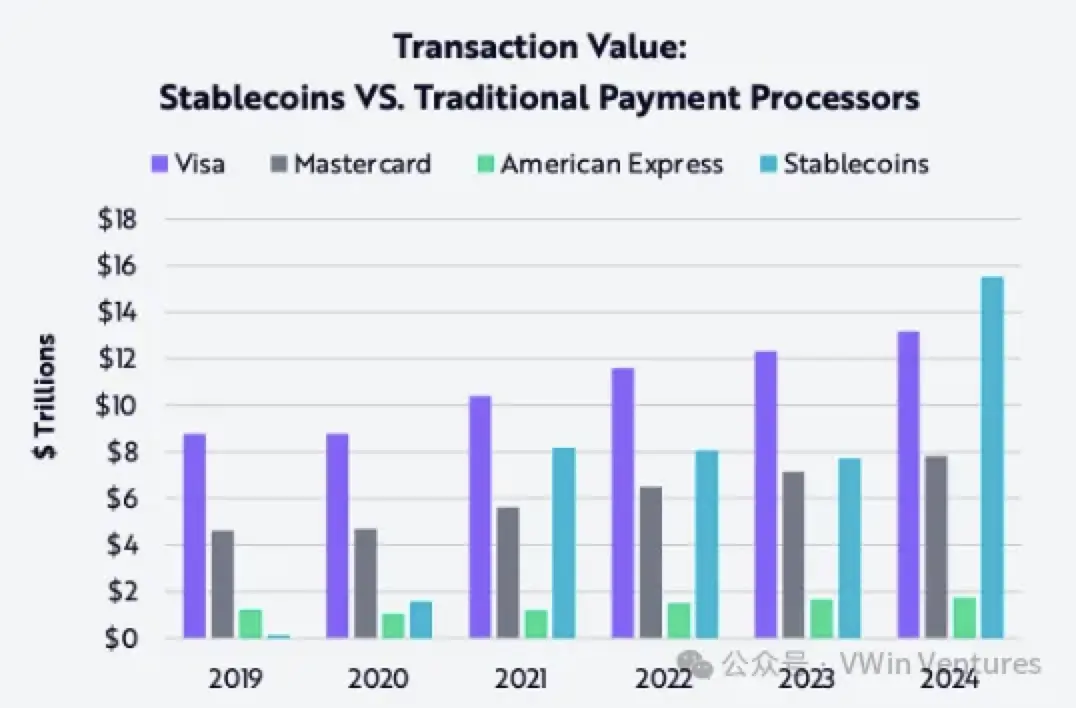

In 2024, the global transaction volume of stablecoins reached $15.6 trillion, surpassing the scale of traditional payment giants Visa and Mastercard during the same period, becoming one of the most important value transfer networks globally, with a conservative estimate that over half of this volume comes from cross-border payment scenarios.

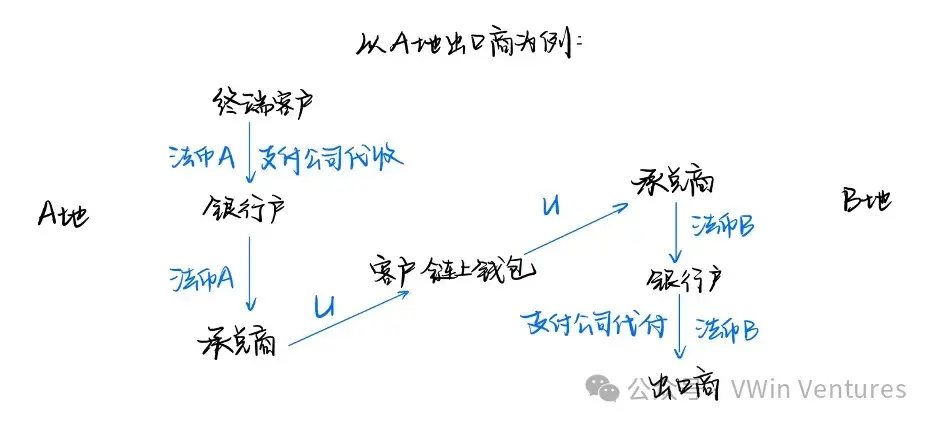

Traditional payment scenarios involve lengthy processes and many intermediaries, while stablecoins have clear advantages in cross-border payment segments. Stablecoin payments primarily have two core business scenarios:

Scenario One: To B Business

To B resembles a web2.5 business, adding a "fiat currency – stablecoin" process to the existing payment chain (which is also the main source of profit), achieving cost reduction and efficiency improvement compared to compliant systems, and regulatory arbitrage in sanctioned or restricted areas, addressing real needs.

To B business has a large scale, stable cash flow, and real business scenarios, including virtual service clients (e.g., voice chat, online gambling, etc.) and traditional trade clients:

Virtual service clients mostly have one-way off-ramp needs for stablecoins, where income is in crypto and expenditures (advertising, salaries, etc.) are in fiat. This scenario is highly homogeneous, gradually saturating, and heavily reliant on operational and sales capabilities.

Traditional trade clients generally require the full process of cross-border payments: local acquiring – local acceptance – cross-border transfer – currency exchange – payment on behalf; some also include needs for foreign exchange settlement and tax refunds. In smaller long-tail countries, there are higher gross margins, competing for stable capital flow channels, channel network construction, and localized operational capabilities. In contrast, the chain is longer, replacing and integrating more inefficient segments in traditional payment chains, offering greater value chain optimization and profit enhancement potential.

When To B business reaches a certain scale, there is compliance pressure, and licenses such as Hong Kong MSO/Singapore MPI become necessary compliance costs after scaling.

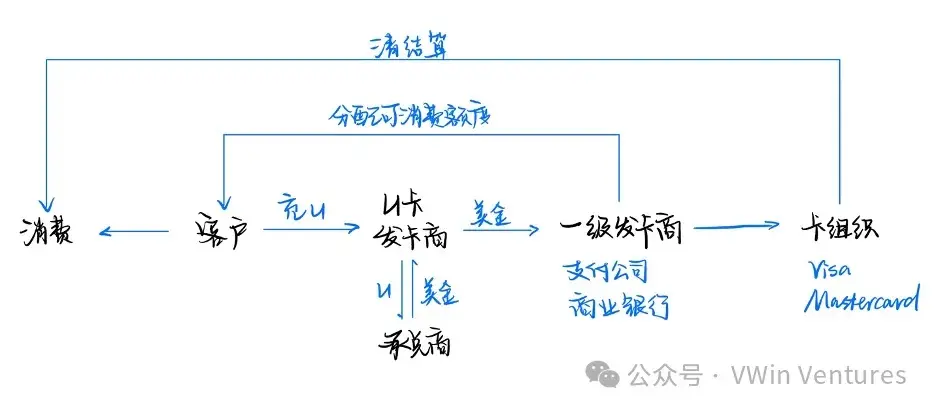

Scenario Two: To C Business

The typical model for To C business is U-card issuers, primarily serving underbanked end customers who are not adequately served by banks, with overall business currently having low gross margins. The business chain is:

C-end customers – Secondary issuers [accepting third-party acceptance] – Primary issuers (such as commercial banks, payment companies, etc.) – Card organizations (Visa, Mastercard)

Due to the high barriers to expanding upstream to primary issuers, purely crypto cards represent a business with risks exceeding returns, but they can serve as customer acquisition tools, expanding asset management and other businesses as a means of attracting traffic, making them a natural choice for major exchanges' business expansion.

Whether for B-end or C-end users conducting currency exchange, compliance and security have always been the biggest pain points in the market. As the market moves towards institutionalization and mainstreaming, licensed financial institutions have become the most compliant and secure trading channels, such as compliant exchanges in Hong Kong and listed brokers like Victory Securities, providing customers with safe and reliable trading options.

Future Development Trends of Stablecoins: The Compliance Battle

Stablecoin payments are currently in a relatively gray area, and compliant stablecoin settlement scenarios have enormous potential for growth. As the upstream of payment scenarios, stablecoins can significantly enhance business barriers by binding to core large channels.

The path to compliance development in the current stablecoin market is challenging due to significant conflicts of interest within the traditional financial system and high compliance thresholds. However, in the long run, the compliance route holds greater strategic value:

In the context of geopolitical conflicts and financial sanctions, trading companies need compliant, secure, auditable, and mutually beneficial solutions;

Mainstream institutions are entering the market (Fidelity, Wyoming State, World Liberty Finance, etc.), competing for the conversion of traditional payment markets and the tokenization of quality assets;

Local protectionism and the emergence of regional leading players, such as compliant stablecoins in Europe and Hong Kong. New players include local banks, payment companies, and internet companies, with licenses serving as a stepping stone, while the core competition lies in seizing and building core channel resources and exchange networks;

Under the trend of de-dollarization in international trade, there are opportunities to promote offshore RMB in scenarios like the Belt and Road Initiative.

Strategic Competition: Do Stablecoins Help Achieve Financial Hegemony for the Dollar?

From a higher global strategic competition perspective, dollar stablecoins carry the "de-geographical" output of a new round of financial sovereignty for the dollar. Stablecoins map the dollar onto a globally permissionless clearing network on the blockchain, facilitating smoother capital and liquidity flows globally on the funding side, while exacerbating the "global Matthew effect" and concentration of assets on the asset side.

Stablecoins significantly lower the barriers to the global flow of dollars, bypassing banks and central bank systems to directly reach global users. In the past, dollar hegemony relied on central banks for trade settlements; currently, in many markets, especially developing countries, the public spontaneously uses stablecoins as a means of pricing, payment, and value storage. Stablecoins enable the free flow of dollars across borders, facilitating the attraction of global funds to dollar assets such as U.S. Treasuries and U.S. stocks, while benefiting the U.S. in asset harvesting through dollar tides.

Central banks in developing countries are thus placed in a passive position. Dollar hegemony continues to extend through stablecoins along two legs: compliance and gray areas:

Gray Expansion: Represented by USDT, which relies on regulatory arbitrage demands, is widely used in speculative, gambling, and regulatory evasion scenarios in gray areas, rapidly expanding user bases and market penetration in regions with foreign exchange controls such as Southeast Asia, Latin America, and Africa.

Compliance Expansion: Represented by USDC, which has U.S. regulatory support, gradually incorporating mainstream financial institutions to build an on-chain compliant dollar clearing and settlement network. While it holds significant long-term value, its current growth is relatively slow due to certain conflicts of interest with traditional payment systems, making its development path more reliant on official regulation and institutional endorsement.

The U.S. regulatory strategy reflects a tacit approval of the wild growth in gray areas (USDT) while actively supporting the development of compliant scenarios (USDC). Together, they construct a strategic moat for the dollar on-chain, achieving a siphoning effect on global financial liquidity.

As a strategic projection tool for dollar hegemony, stablecoins essentially serve as a "programmable financial sanctions" weapon, with the U.S. controlling this seemingly decentralized network clearing system. The U.S. can precisely target objectives through regulatory compliance and smart contract asset freezes (e.g., freezing USDC related to Tornado Cash addresses).

For policymakers in developing countries or other regions, avoiding becoming a "digital dollar colony" is crucial:

If a credible local on-chain financial system is not established, they will long remain passive users of the dollar stablecoin system.

In the new era, "clearing equals hegemony": controlling on-chain clearing flows is akin to controlling global water sources — seemingly free, but with valves. Consider launching national or regional on-chain financial infrastructure (such as local stablecoins or CBDCs) to reduce excessive reliance on the dollar on-chain system.

Conclusion: Stablecoins as Strategic Weapons of Dollar Hegemony in the New Era and Historical Opportunities for Reshaping Global Financial Order

The promotion and popularization of stablecoins rely on genuine trading demand and clearing efficiency, constructing a structural and sustainable capital flow network globally.

Currently, stablecoins have relatively solidified their position in crypto trading scenarios, with leading players monopolizing market share, and incremental growth coming from new financial assets being tokenized; while payment scenarios, especially cross-border payments, represent the main incremental blue ocean and structural breakthrough.

The on-chain payment and clearing network built around stablecoins is encroaching on the traditional banking and SWIFT-dominated cross-border payment systems, giving rise to a massive payment and exchange market worth trillions of dollars, providing global financial institutions, payment companies, and even national-level financial infrastructures with a historic opportunity to redefine their roles.

The rise and widespread adoption of stablecoins essentially continue the penetration of dollar hegemony in the financial system, upgrading it to a more covert, broader, more strategic, and precise version on-chain. The competition in the stablecoin era is no longer a game at the level of financial instruments but a strategic contest for global currency sovereignty and discourse power in the global financial order.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。