Author: Token Dispatch and Thejaswini M A

Compiled by: Block unicorn

Introduction

Every industry has that moment when rivals suddenly realize they are fighting the wrong war.

In the financial sector, this moment quietly arrived in 2025, not through grand announcements, but through a series of seemingly unrelated corporate moves signaling a profound shift: the end of the standoff between traditional finance (TradFi) and decentralized finance (DeFi).

For years, these two financial ecosystems operated like parallel universes. Traditional finance (TradFi) existed in a world of T+2 settlements, bank operating hours, and regulatory compliance.

Decentralized finance (DeFi), on the other hand, thrived in a realm of instant settlements, 24/7 operations, and permissionless innovation. They spoke different languages, followed different principles, and were filled with mutual suspicion.

We all remember that acquisition frenzy:

Ripple → Hidden Road: $1.25 billion (April 2025)

Stripe → Bridge: $1.1 billion (February 2025)

Robinhood → Bitstamp: $200 million (June 2024)

But a fundamental change has occurred. Rigid boundaries are melting away, not because either side won the ideological battle, but because both finally understand what they lack.

Transformation

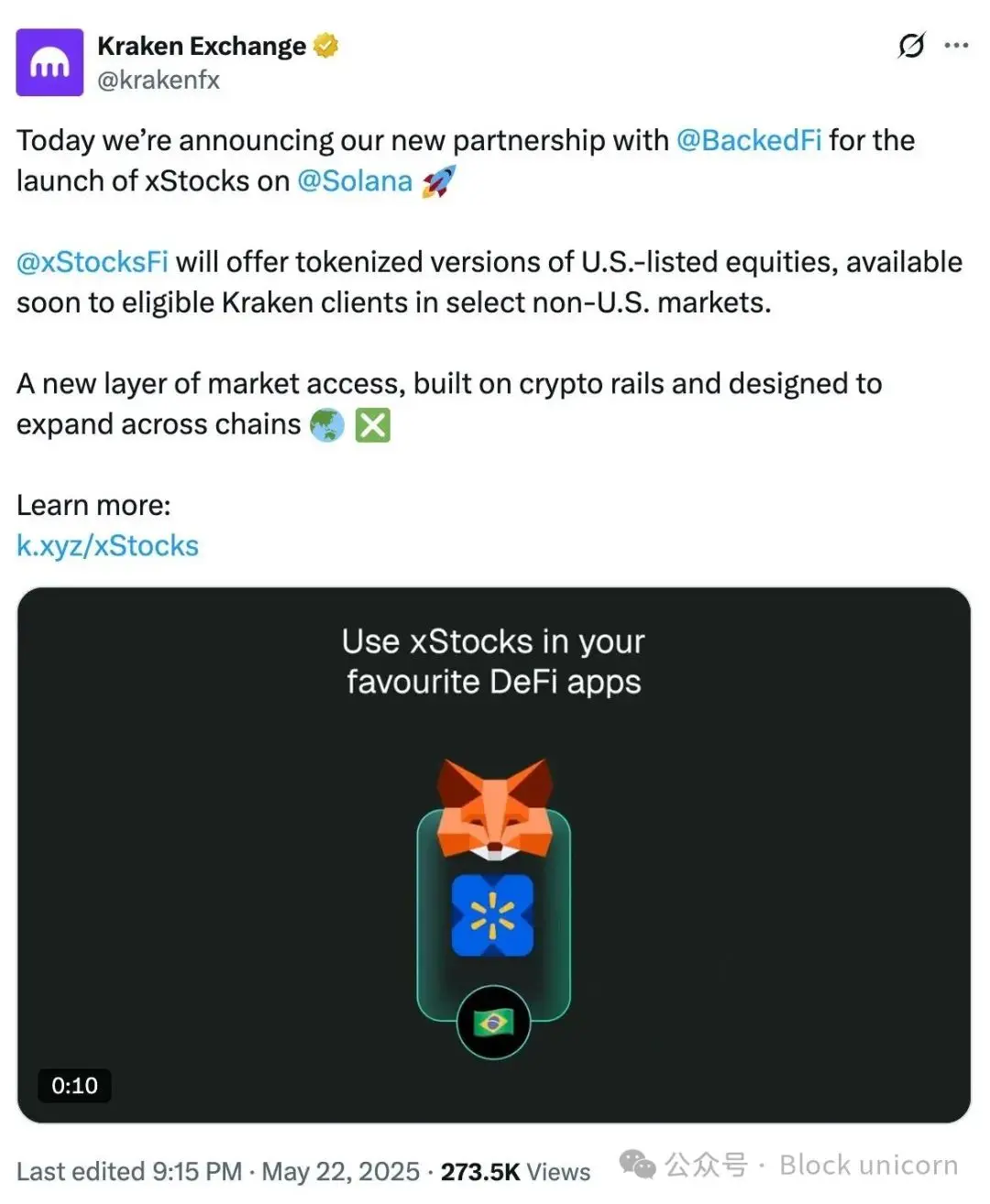

Kraken announced they would soon launch tokenized versions of Apple, Tesla, and Nvidia stocks—backed 1:1 by actual shares—and trade them 24/7 on the Solana blockchain.

Not crypto derivatives. Not synthetic exposure. Real stocks, just freed from the constraints of traditional market hours.

This announcement laid the groundwork.

Think about it. Apple generates revenue every second from App Store purchases in Tokyo, iCloud subscriptions in London, and iPhone sales in Sydney. Yet, the stock representing ownership in this global, 24/7 operating company can only be traded within a narrow time window while Manhattan is awake.

Kraken's xStocks—developed in partnership with Backed and issued as SPL tokens on Solana—do not solve this problem through clever financial engineering. They solve it by completely eliminating the problem. The same stocks, the same regulatory protections, the same underlying ownership. Just programmable.

The implications go far beyond extended trading hours. These tokenized stocks can serve as collateral in DeFi protocols, combine with other assets in automated strategies, and be transferred instantaneously across borders. Traditional brokerages require separate accounts, different compliance processes, and settlement delays. Blockchain infrastructure eliminates these friction points while preserving the core value proposition of equity ownership.

But the particularly important reason is: Kraken's target is not the crypto enthusiasts wanting to trade Tesla stock at 3 AM. Their target is institutional and retail investors outside the U.S., who face the expensive, slow, and restricted barriers of the U.S. stock market.

This is how the TradFi-DeFi bridge operates in practice. It is not cryptocurrencies trying to replace traditional assets, but blockchain infrastructure extending traditional assets beyond their conventional limits. This is just the beginning.

From fierce competition, we have now arrived at a point where banks are joining forces to create stablecoins:

This convergence is accelerating, surpassing the initiatives of individual companies.

This marks a strategic shift compared to the tentative, isolated experiments banks have conducted in the crypto space over the past few years. They are no longer competing alone in unfamiliar territory but are pooling resources to build shared infrastructure that challenges existing stablecoin leaders.

Infrastructure Revelation

Traditional finance has been grappling with a dirty secret: its infrastructure is crumbling under the pressure of global demand. Cross-border payments still take days. Settlement systems fail under market pressure. Transactions halt when they are needed most. Meanwhile, DeFi protocols have been handling billions of dollars in transactions, with settlement times measured in milliseconds, operating seamlessly across borders, and maintaining uptime.

The real revelation is not that DeFi is "better"—but that DeFi solves problems traditional finance didn't even realize could be solved.

When Kraken announced they would offer tokenized U.S. stocks for 24/7 trading on Solana, they were not trying to replace the stock market. They simply posed a straightforward question: why should Apple’s stock stop trading just because New York is asleep?

This question also drives R3's collaboration with the Solana Foundation to bring $10 billion in traditional assets from institutions like HSBC and Bank of America to the public blockchain.

They are not abandoning traditional finance. They are expanding it, transcending geographical and time zone limitations.

Liquidity Epiphany

DeFi's dirty secret is equally striking: despite being full of innovation, it is severely lacking in institutional capital. Retail traders and crypto natives can only provide limited liquidity.

Real funds remain trapped behind regulatory barriers. Breakthroughs occur when both sides stop trying to change each other and start building a translation layer. Stablecoins have become the Rosetta Stone.

When institutions discovered they could hold USDC without enduring the volatility of cryptocurrencies while still earning DeFi yields, everything changed.

When DeFi protocols realized they could access traditional liquidity pools through regulated custodians, the barriers began to crumble. It is expected that by 2025, stablecoin trading volume will exceed $30 trillion annually, driven not by speculation but by institutions using it as a bridge between new and old financial rails.

Composability Convergence

What is happening is a fundamental reshaping of financial services. Traditional finance has always been fragmented.

Your bank account does not talk to your brokerage account. Your insurance policy cannot interact with your portfolio. Your retirement fund operates independently of your daily spending. DeFi introduces something revolutionary: composability. The ability to seamlessly combine different financial primitives.

Providing liquidity, earning yields, using those yields as collateral, deploying borrowed funds into another strategy—all accomplished in a single transaction. Now, traditional institutions are starting to envy this composability.

Imagine a company's finance department automatically optimizing between traditional money market and DeFi yield strategies based on risk-adjusted returns.

Or a pension fund using tokenized stocks for 24/7 rebalancing while maintaining custody through regulated providers. These scenarios are no longer hypothetical. Today, companies that understand the future belongs to hybrid systems are building such infrastructure.

Ultimately, the convergence of TradFi and DeFi is driven by an inefficiency arbitrage that cannot be ignored. Traditional finance excels in scale, regulatory compliance, and institutional trust. But it is slow, expensive, and geographically constrained. DeFi excels in speed, automation, and global accessibility. But it lacks institutional adoption and regulatory clarity.

The companies that will win in this convergence are those that combine the strengths of both: institutional-grade compliance with blockchain efficiency, regulatory oversight with global accessibility, traditional scale with programmable automation.

When R3 moves $10 billion in traditional assets to Solana, they are not making an ideological statement.

They are pursuing an efficiency arbitrage that benefits everyone: institutions gain faster settlements and global accessibility, while blockchain networks gain the liquidity and legitimacy needed to scale.

Regulatory Reconciliation

The most significant shift is happening at the regulatory level. The adversarial relationship between regulators and cryptocurrencies is evolving into something more nuanced: cautious collaboration. The SEC's approval of a Bitcoin ETF is a signal that regulators are ready to work with crypto innovation rather than suppress it.

The "Financial Innovation and Technology Act of the 21st Century" (FIT 21) and proposed stablecoin legislation provide the clarity institutions need to operate in both worlds. But the change lies in how companies handle compliance.

The clearest signal of regulatory momentum comes from David Sacks, the White House crypto czar, who stated in a CNBC interview that the GENIUS Act's stablecoin legislation could unleash enormous institutional demand:

"We already have over $200 billion in stablecoins—just unregulated. I think if we provide legal clarity and a legal framework for this, we could create trillions of dollars in demand for our Treasury almost overnight, which is very fast."

Data supports Sacks' optimism. Tether alone holds nearly $120 billion in U.S. Treasuries, making it the 19th largest holder globally—surpassing Germany. The GENIUS Act passed a key procedural vote with bipartisan support of 66 to 32, requiring stablecoins to be fully backed by U.S. Treasuries or dollar equivalents.

They are no longer building crypto-native systems and hoping regulators will adapt; instead, they are designing blockchain platforms with institutional compliance from day one.

This regulatory thaw explains why major banks suddenly feel at ease with tokenization projects. They are embracing programmable infrastructure using blockchain technology—not just cryptocurrencies.

User Experience Revolution

Traditional finance has conditioned people to accept unnecessary restrictions imposed by blockchain technology. If blockchain transactions can be completed in seconds, why do international wire transfers take three business days?

When global demand operates 24/7, why should markets close?

Why does accessing different financial services require different accounts, different platforms, and different compliance processes? The convergence of traditional finance (TradFi) and decentralized finance (DeFi) is not just about institutional adoption or technological innovation—it is about building financial infrastructure that truly serves user needs, rather than being constrained by traditional limitations.

When Kraken offers tokenized stocks for 24/7 trading, they are not just adding a product feature. They are demonstrating how vast the possibilities can be when you no longer accept artificial constraints as a permanent reality.

What makes this convergence particularly powerful is that it creates a positive feedback loop.

As more traditional assets move onto blockchain rails, the value of these networks increases for everyone. As more institutions participate in DeFi protocols, these protocols become more stable and liquid.

These network effects explain why the convergence is accelerating rather than slowly evolving. Early actors are not only gaining a first-mover advantage—they are also helping to create the standards and infrastructure that others must adopt.

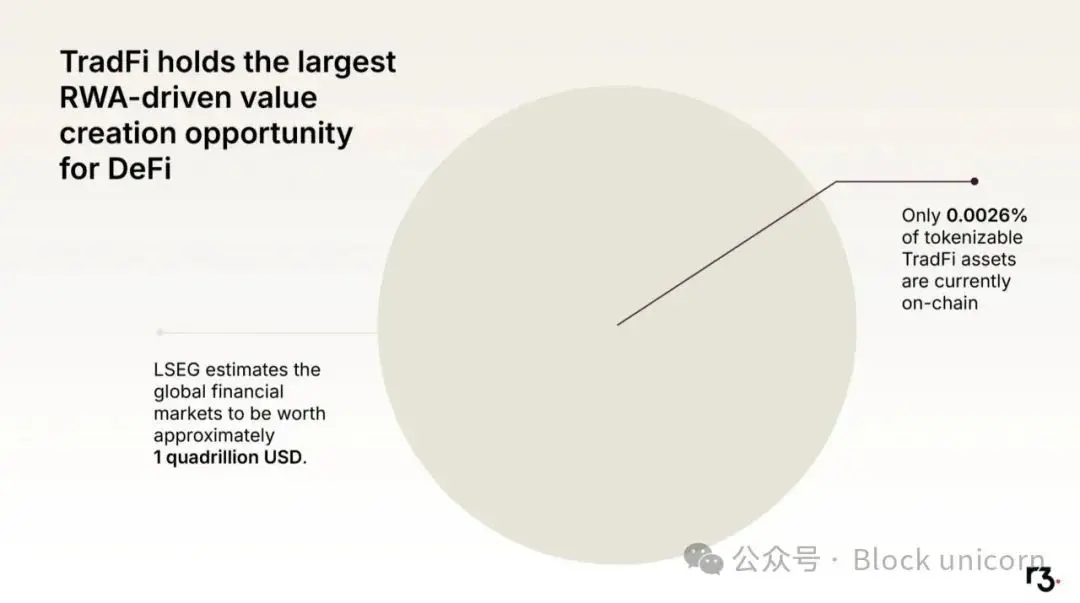

The tokenization of real-world assets is the most direct manifestation of this convergence. When Boston Consulting Group and Ripple predict that the tokenization market could reach $18.9 trillion by 2033, they are describing the infrastructure of a post-tribal financial system.

Perspective

The great financial reconciliation of 2025 represents not just a technological convergence. It is a victory of pragmatism over ideology.

For years, the debate between TradFi and DeFi has been like watching two groups argue about different issues.

Traditional finance focuses on scale, compliance, and stability. DeFi prioritizes innovation, accessibility, and efficiency. Both are correct in valuing what they do, but both are also incomplete. Breakthroughs occur when companies stop trying to prove the superiority of one approach and start building systems that combine the strengths of both.

Ripple's acquisition of Hidden Road was not to prove the superiority of cryptocurrencies—they did it because hybrid infrastructure creates more value than any single approach. This pragmatic convergence is exactly what the financial industry needs. Traditional finance, lacking innovation, is becoming increasingly outdated.

DeFi, without institutional adoption, remains a scarce resource in niche markets. But by smartly combining both, it is possible to create something that a single approach cannot achieve: efficient, accessible, compliant, and globally scalable financial infrastructure. The companies that will win this convergence are those that build the best bridges.

They understand that the future does not belong to TradFi or DeFi, but to those who can eliminate the friction between people's needs and the tools available to them.

This great financial reconciliation is about building a system that allows both sides to leverage their best advantages while rendering their limitations irrelevant. Based on the infrastructure being built today, this future is arriving faster than any ideologue from either side anticipated.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。