Author: Lyn Alden, Broken Money

Translator: AIMan, Golden Finance

Over the past year or so, the Bitcoin ecosystem has largely been driven by the rise of Bitcoin treasury companies.

Although Strategy (MSTR) was the first to adopt this trend back in 2020, the subsequent adoption by other companies has been slow. However, after experiencing another round of bear and bull market cycles, along with significant updates from the Financial Accounting Standards Board (FASB) in 2023 regarding the accounting treatment of Bitcoin on balance sheets, 2024 and 2025 are witnessing a new wave of companies adopting Bitcoin as a treasury asset.

This article explores this trend and analyzes its pros and cons for the entire Bitcoin ecosystem. Additionally, it discusses the nature of Bitcoin as a medium of exchange rather than a store of value. In my view, this aspect is often misunderstood from an economic perspective.

1. Why are Bitcoin stocks and bonds on the rise?

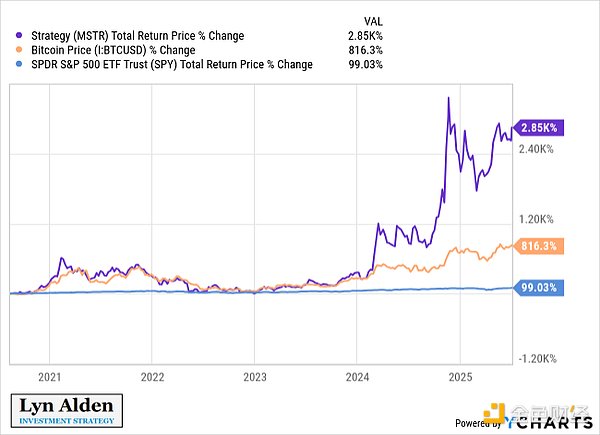

Back in August 2024, when this trend was still relatively unknown, I wrote an article titled "A New Perspective on Bitcoin Treasury Strategy," discussing the practicality of Bitcoin as a corporate treasury asset. At that time, only a few companies were using Bitcoin on a large scale, but since then, a wave of new and old companies have adopted this strategy. Companies that adopted Bitcoin on a large scale back then, such as Strategy and Metaplanet, have seen significant increases in price and market capitalization.

That article explained why publicly traded companies should consider implementing this strategy. But what about investors? Why is this strategy so popular among them? From an investor's perspective, why not just buy Bitcoin directly? There are several main reasons.

Reason 1: Authorized Capital

The capital managed by capital management companies amounts to trillions of dollars, some of which have strict regulations.

For example, some equity fund portfolio managers can only purchase stocks. They cannot buy bonds, ETFs, commodities, or other products. They can only buy stocks. Similarly, some bond fund portfolio managers can only purchase bonds. Of course, there are also more specific regulations, such as some fund managers can only buy healthcare stocks or non-investment-grade bonds.

Some of these fund managers are bullish on Bitcoin. In many cases, they also hold some Bitcoin themselves. However, they cannot express this view by putting Bitcoin into stock or bond funds, as it would violate their duties. However, if someone creates a stock with Bitcoin on the balance sheet or issues convertible bonds for a stock with Bitcoin on the balance sheet, they can purchase it. Portfolio managers can now express their bullish view on Bitcoin within their own funds for themselves and their investors. This is a previously undeveloped market that is increasingly gaining attention in the U.S., Japan, the U.K., South Korea, and other countries/regions.

I will use myself as a specific micro case to illustrate how Bitcoin treasury companies help achieve this goal. Since 2018, I have been operating a real-money model portfolio for my free public newsletter, allowing readers to transparently track my holdings.

At the beginning of 2020, I strongly recommended Bitcoin as an investment in my research service, and I also bought some myself. Additionally, I wanted to increase my Bitcoin exposure in my newsletter portfolio, but the brokerage I was using at the time did not provide a way to purchase Bitcoin-related securities. At that time, I couldn't even buy the Grayscale Bitcoin Trust (GBTC) for my model portfolio because it was traded over-the-counter rather than on major exchanges.

Fortunately, Strategy (then known as MicroStrategy) added Bitcoin to its balance sheet in August 2020. MicroStrategy was then traded on NASDAQ, and my model portfolio broker could buy it. Therefore, considering the various restrictions on that specific portfolio, I was happy to buy MSTR in the growth stock sector to express my bullish view on Bitcoin. Since then, my portfolio has maintained a long position in MSTR, which has been a wise decision for nearly five years:

Eventually, the broker added GBTC as a purchasable security, and of course, they also added it when the major spot Bitcoin ETFs were listed, but I continued to hold MSTR in that portfolio (for the second reason that will be described below).

In short, many funds can only hold stocks or bonds related to Bitcoin due to authorization regulations and cannot hold ETFs or similar securities. Bitcoin treasury companies give them the authority to invest in Bitcoin.

This is a complement to Bitcoin rather than primarily competing with it, as Bitcoin is an asset that individuals can hold in their own custody.

Reason 2: Companies Have Ideal Leverage

The fundamental strategy for publicly traded companies adopting Bitcoin as a treasury asset is to hold some Bitcoin instead of cash equivalents. Those who first proposed this concept often have high confidence in the idea. Therefore, the current trend is not only to buy Bitcoin but also to use leverage to buy Bitcoin.

In fact, publicly traded companies have better leverage capabilities than hedge funds and most other types of capital. Specifically, they have the ability to issue corporate bonds.

Hedge funds and some other capital pools typically use margin loans. They borrow money to purchase more assets, but if the asset value drops too low relative to the borrowed amount, they risk a margin call. If asset prices fall too quickly, a margin call may force hedge funds to sell assets, even if they firmly believe those assets will rebound to new highs. Liquidating quality assets at a low point is undoubtedly a disaster.

In contrast, companies can issue bonds, typically with maturities of several years. If they hold Bitcoin and the BTC price drops, they do not have to sell prematurely. This makes them more capable of withstanding market volatility than entities relying on margin loans. Although there are still some bearish scenarios that may force companies to liquidate, these scenarios require a longer bear market duration, making them less likely to occur.

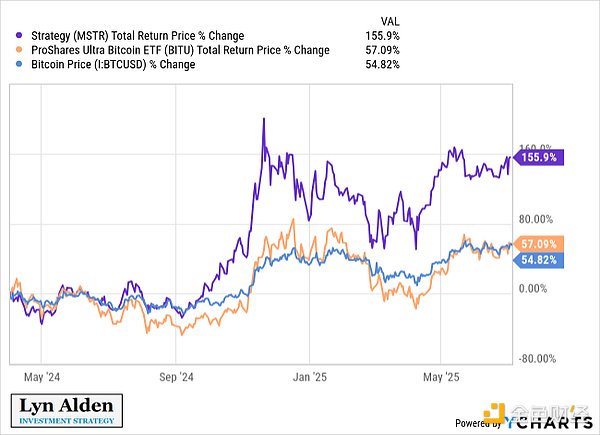

This longer-term corporate leverage is also typically more long-term than leveraged ETFs. Since leveraged ETFs do not use long-term debt, their leverage resets daily, making volatility generally unfavorable for them. Fidelity has a great article that details these numbers with examples.

This article includes a practical chart showing how a 2x leveraged ETF performs when the underlying asset's returns fluctuate between +10% and -10%. Over time, this leveraged product will gradually depreciate relative to its leveraged corresponding index:

In fact, although Bitcoin prices have risen during this period, the performance of the 2x leveraged Bitcoin ETF BITU has not truly outperformed Bitcoin since its inception. You might think that the performance of the 2x leveraged version would significantly exceed that of Bitcoin, but it actually just increased volatility without delivering higher returns. The following chart traces back to the inception of BITU:

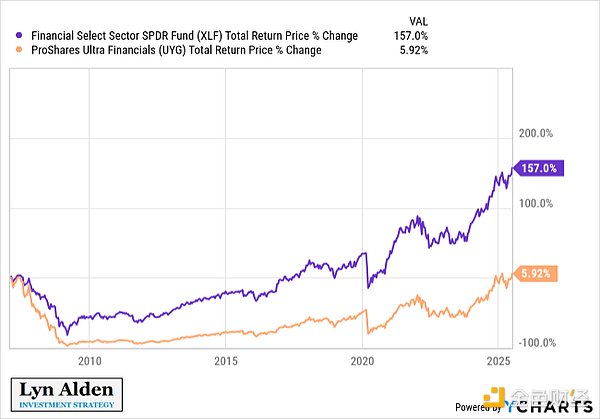

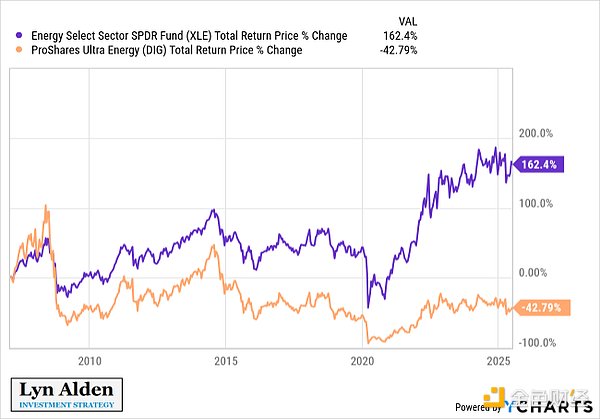

The same reasoning applies if you look back at the long-term history of more volatile stock sectors, such as the 2x leveraged versions of the financial or energy sectors, where their performance during volatile periods lags far behind:

So, unless you are a short-term trader, daily leverage is quite poor. Volatility harms this leverage.

However, linking long-term debt to assets typically does not lead to the same issues. Pairing an appreciating asset with long-term debt is a powerful combination. Therefore, for those who are firmly bullish on Bitcoin and wish to utilize reasonably safe leverage to gain returns, Bitcoin treasury companies are a useful security.

Not everyone should use leverage, but those who do naturally want to operate in the most optimal way. Currently, there is a wide variety of Bitcoin treasury companies, differing in risk profiles, sizes, industries, jurisdictions, and so on. This is a genuine market demand that is being met over time.

Similarly, some securities issued by these companies, such as convertible bonds or preferred stocks, can provide lower volatility Bitcoin price exposure. Some investors may want higher volatility, while others may prefer lower volatility, and the variety of available securities can provide investors with the specific type of exposure they need.

2. Are Bitcoin treasury companies beneficial or harmful to Bitcoin?

Now that we understand the reasons for their existence and the ecological niche they fill for investors, the next question is: Are Bitcoin treasury companies beneficial to the entire Bitcoin network? Does their very existence undermine the value of Bitcoin as a free currency?

To determine whether Bitcoin treasury companies are good or bad for Bitcoin, we must first understand how decentralized currency theoretically becomes popular (if it indeed becomes popular). What steps need to be taken? What is the general order?

Thus, this section will contain two steps. The first step will provide an economic analysis of how a new form of currency can become popular, specifically analyzing what its path to success looks like. The second step will analyze whether Bitcoin treasury companies will promote or hinder this development path.

Step 1: What kind of new currency can successfully become popular?

What would it look like if it appeared to be a global, digital, sound, open-source, programmable currency, and it was monetized from absolute zero?

Ludwig Wittgenstein once asked a friend, "Please tell me, why do people think it is more natural for the sun to revolve around the earth than for the earth to rotate?" The friend replied, "Well, obviously, because it looks like the sun is revolving around the earth." Wittgenstein responded, "Then what would it look like if the earth really rotated?"

As the four-year bull market for Bitcoin begins, we must be prepared to welcome sudden, uninformed attention from the world. Many newcomers will come with an open mind—just as we once did—but there will also be many disruptors emerging from behind the scenes, insisting that what we see with our own eyes is not actually happening because, according to their theories, it is simply impossible.

Bitcoin cannot serve as a store of value because it has no intrinsic value. It cannot serve as a unit of account because it is too volatile. It cannot serve as a medium of exchange because it is not widely used for pricing goods and services. These three attributes constitute the three main properties of money. Therefore, Bitcoin cannot be money. But Bitcoin has no other basis of value, so it is worthless. Proof complete (QED, Quod Erat Demonstrandum).

I call this argument "semantics, therefore it is right." How could it be falsified? Fundamentally, it is a statement about the material world; about what will happen in real life, or in this case, what will not happen. However, it seems to rely entirely on the meanings of words. In discussing the dollarization of Ecuador—a guiding process where an "official" currency is spontaneously replaced by a simpler, superior currency—Larry White remarked about those who, by definition, deny that such a thing could happen, saying they "just stare at the blackboard and do not look at what is happening outside the window." This is a strange way to understand novel phenomena, and generally, I would not recommend this approach. Reality does not care how you describe it.

——Allen Farrington, 2020, "Wittgenstein's Money"

Bitcoin was launched in early 2009. During 2009 to 2010, some enthusiasts mined, collected, tested, speculated, or researched ways to contribute to or improve it in some way. They liked the idea of Bitcoin.

In 2010, Satoshi Nakamoto himself described how the network initially guided some tiny initial values on the Bitcoin Talk forum:

As a thought experiment, imagine a base metal that is scarce like gold (note: referring to metals other than precious metals like gold, silver, platinum, etc.), but with the following characteristics:

– It is a dull gray color

– It is not a good conductor of electricity

– It is not particularly strong, nor is it malleable or easy to forge

– It is not suitable for any practical or decorative purpose

And it has one special, magical property:

It can be transmitted through communication channels

If it somehow, for whatever reason, gains any value, then anyone wanting to transfer wealth over a distance can buy some, transmit it, and then let the receiver sell it.

——Satoshi Nakamoto, 2010, Re: Bitcoin does not violate Mises' regression theorem

A year later, in 2011, Wences Casares, the founder of Xapo, also used it for this purpose. Here is an excerpt from Episode 56 of "Masters of Scale":

Wences Casares: We take a bus trip for a week every year, starting from Buenos Aires, traveling around the world. We have a lot of fun. We just gather together, drink mate, and run many, many miles.

Reid Hoffman (co-founder of LinkedIn): This is Wences Casares, a serial entrepreneur from Argentina, who is taking us on an annual trip with a group of close friends. I want you to imagine this beloved bus. It looks like a school bus that crashed into an RV and then lived in the post-apocalyptic world of "Mad Max" after being retired. Before one of their epic trips, Wences learned that the bus was broken. The repair was not difficult, but the cost was very high. Especially since Wences was living in California at the time, and the bus was in Argentina.

Casares: We had to send money to fix the bus, but Argentina had shut down all payment methods like Western Union, PayPal, etc. You could wire money to the central bank, but the process was cumbersome and expensive.

Hoffman: It seemed that their next trip would have to wait until the Argentine financial system returned to normal. But that could take months or even years. Then a friend made a suggestion.

Casares: "Have you looked into Bitcoin?"

Hoffman: Bitcoin. It was 2011, just two years after this network currency was launched. Wences was caught off guard.

Casares: I should have been a tech person and a finance person, but I had never heard of these things before. I asked, "What is that?" He said, "Oh, well, it's a new currency that you can send money anywhere without a third party." I was very skeptical at the time, even a bit cynical.

Hoffman: But the bus could not fix itself. The Argentine financial system could not be repaired in the short term either. So Wences decided to give Bitcoin a try. A mysterious journey began.

Casares: I saw an old man on Craigslist willing to sell me $2,000 worth of Bitcoin, and he arranged to meet me at a café in Palo Alto. We met a guy who looked like Gandalf, and I gave him $2,000 in cash.

Hoffman: Wences was not entirely convinced by what Gandalf did next.

Casares: He had me download an app, scan a QR code, and then sent me what was supposedly $2,000 worth of Bitcoin. I went back to the office, convinced I had been scammed. Then I sent my friend $200—that was the part I was supposed to send. That evening after work, my friend said, "Hey, Wences, I got the Bitcoin and then sold it for pesos, so everything is good." I thought, "What just happened?"

Hoffman: Wences' view of Bitcoin changed.

Casares: I was in a dilemma—this lasted for six months—I was very cynical at first. But after six months, I said, you know, I want to spend the rest of my life helping it succeed because I believe a world where Bitcoin serves billions of people is more important than a world where the internet succeeds.

Shortly thereafter, Casares convinced many large investors to buy Bitcoin. His Wikipedia page currently describes this as follows:

According to Quartz, Casares is widely referred to as "Patient Zero," an entrepreneur who persuaded Bill Gates, Reid Hoffman (co-founder of LinkedIn), Chamath Palihapitiya (founder of Social Capital), Bill Miller (chairman of Legg Mason Capital Management), Mike Novogratz, Peter Briger (co-CEO of Fortress), and other tech veterans from Silicon Valley and Wall Street to invest in Bitcoin.

And that's not all. I personally know several people active in institutional finance who bought Bitcoin early on, directly because Casares explained the value of Bitcoin to them or because of his talks on Bitcoin.

After achieving some initial success, Bitcoin faced the challenge that the network spawned millions of competitors. Countless altcoins emerged, all with similar functionalities, primarily being able to be purchased, transferred, and sold by the receiver. The stablecoins launched in 2014 allowed for the use of tokens backed by dollars instead of freely floating units for the above operations, helping to eliminate volatility.

In fact, the rise of competitors was the biggest reason I did not buy Bitcoin in the early 2010s. I was not against the concept (quite the opposite), but I thought the industry was 1) rife with speculative bubbles, and 2) easily replicable to the point of being drowned out. In other words, while Bitcoin's supply might be limited, the idea was infinite.

But by the late 2010s, I noticed something: Bitcoin's network effect was successfully becoming a portable capital. It was breaking through that ceiling. Just like a communication protocol (whether verbal language, written text, or digital standards), money as a concept greatly benefits from network effects. The more people use it, the better it is for others to use it; this is a self-reinforcing phenomenon. And this is where the willingness to hold it truly matters. This is also why the network effect must grow to break through this niche and crowded phase.

In this context, we can categorize money into two types:

- The first type of money is "situational money," which refers to money that can solve specific problems but has not yet gained widespread attention in other respects. An asset that can be purchased with local currency, transferred across high-friction points (capital controls, payment platform shutdowns, etc.), and allows the receiver to sell/exchange it for local currency is a form of situational money. It has value, but achieving success in this regard does not necessarily lead to broader success.

- The second type of money is "universal money," which refers to money that is widely accepted within a specific region or industry. Importantly, the receiver does not immediately sell or exchange the money upon receipt; they hold it as a cash balance and may use it again elsewhere.

For something to be used as universal money, users must already possess it, and receivers must have the willingness to hold it. Notably, people generally want more of what they already have. After all, if potential receivers want to hold it, they are likely to have already purchased some. Therefore, if a new type of universal money emerges, most people may initially view it as an investment because they believe its purchasing power may appreciate, and then they would also be willing to accept more of this currency as a means of payment. By that time, they would not need to be persuaded to accept it as a means of payment; they already like the asset, so whether they buy more of this asset or people directly hand it to them as payment is almost the same thing.

Bitcoin's simple and secure design (proof of work, fixed supply, limited script complexity, moderate node requirements, and decentralization left by the disappearance of its founder) and first-mover advantage (guiding network effects) give it the best liquidity and robustness, leading many to want to buy and hold it. So far, Bitcoin's tremendous success lies in this: it is a robust and portable store of value that allows users to choose to consume or exchange.

A sound, liquid, homogeneous, and portable store of value lies between situational money and universal money. Unlike situational money, people increasingly see it as worth holding long-term rather than selling/exchanging immediately upon receipt. But unlike universal money, it has not yet been widely accepted in most areas because those who take the time to analyze it are still a minority. This is a necessary step to connect these two types of money, and I believe it is a very long process.

The reason it takes a long time to go through this phase is due to volatility, and because of the enormous scale of existing network effects, people's spending and liabilities are measured against it.

If a new currency network with independent units (i.e., not pegged to existing currencies as its credit track, but rather a system completely parallel to central banks) is to develop from zero to a massive scale, it needs to experience upward volatility. Any appreciating asset with upward volatility will attract speculators and leverage, which will inevitably lead to a period of downward volatility. In other words, it will look like this:

In its application phase, Bitcoin's value skyrocketed from being worthless to several trillion dollars, but it is a rather flawed form of short-term currency. If you receive some Bitcoin and want to pay your rent at the end of the month (and your budget is very tight, meaning you have no extra cash), neither you nor your landlord can afford the possibility of Bitcoin dropping 20% in value within a month. The landlord has expenditures in the existing fiat currency network effect; she needs to know exactly how much rent she is receiving from her tenant. As a tenant, you need to ensure that you can pay your rent at the end of the month without being caught off guard by a rapid devaluation of that money. The same goes for other living costs.

Therefore, during this era, Bitcoin is primarily viewed as an investment. Hardcore enthusiasts are more likely to want to use it. Those facing specific payment issues (capital controls, payment platform shutdowns, etc.) are also more likely to want to use it, although they increasingly have similar liquidity options, such as stablecoins. If you primarily use stablecoins like a checking account for days, weeks, or months, then the centralized nature of stablecoins becomes irrelevant.

There are some well-meaning Bitcoin supporters trying to persuade Bitcoin holders to spend more Bitcoin. I do not think this is a sustainable practice. Bitcoin will not become popular like charities. For Bitcoin consumption to become sustainably popular on a large scale (i.e., for the annual volume of exchange medium transactions globally to not only reach tens of billions of dollars but rather trillions), it must solve problems that other solutions have not yet addressed for consumers and/or recipients. And in the current application phase, this is not necessarily the case, especially with capital gains tax applied to every transaction and options like stablecoins available to meet short-term spending needs, as volatility needs to be reduced. The best advice I can give these supporters is that while educating people is a good thing (keep it up!), it is important to manage expectations throughout the process and understand the economic path dependence involved.

This is where the importance of optionality comes in, and from my observation, this theme is widely misunderstood or underestimated.

Having a reliable, liquid, homogeneous, and portable store of value that is in the process of becoming mainstream can provide holders with advantages or choices that other assets do not possess. Most importantly, they can take this store of value anywhere in the world without relying on central counterparties and credit. It also allows them to make cross-border payments, including payments to off-platform recipients, without experiencing significant friction, even if they stay put. They may not be able to pay with it everywhere at all times, but if needed, they can find ways to exchange it for local currency in most environments, and in some cases, they can even pay directly with it.

From this perspective, Bitcoin has achieved incredible success. To understand why, we must first grasp how shocking the unsold nature of most currencies is.

Imagine you are going to a random country. What currency or other portable, liquid, homogeneous, and untraceable asset can you bring to ensure you have enough purchasing power without relying on the global credit chain? In other words, if all your credit cards are disabled, how do you ensure you can still transact in the face of some troubles and friction?

The best current answer is often physical dollars. If you carry dollars, although you may find it difficult to spend directly at many types of merchants, it is easy to find merchants willing to exchange dollars for local currency at reasonable rates and with ample liquidity.

The second, third, and fourth best answers might be gold coins, silver coins, and euros. Again, in most countries, it is not difficult to find brokers willing to accept gold, silver, or euros and exchange them at reasonable local prices.

After that, the ranking starts to drop rapidly: the renminbi, yen, pound, and a few other currencies enter the top ten. The exchange friction for these currencies is often greater. Currently, I believe Bitcoin should rank in the top ten, probably between 5 and 10, especially if you are going to an urban center. Most cities offer a wealth of exchange options, and if needed, you can seek them out. Considering Bitcoin has only been around for 16 years, that is already impressive.

Further down is the long tail effect of over 160 other fiat currencies. I often use the Egyptian pound and Norwegian krone as examples because I go to Egypt every year and visit Norway every few years, and I always have some of their banknotes on me. These currencies perform poorly outside their home countries, and the vast majority of currencies do as well.

Q: If you don't spend Bitcoin, would you consider it a currency?

A: Yes. Currency gives you liquidity choices. Holding it is using it. Bitcoin is not yet a universally accepted currency, so it serves in the early stages as enthusiasts' currency, situational currency, and/or portable capital.

Q: When will it become a medium of exchange?

A: It may not happen unless it scales up an order of magnitude and reduces volatility. Only a small portion of people understand it and hold it as a store of value. Its proportion in global assets is very small (about 0.2%). It can rise over 100% in a year and fall over 50%. Moreover, since universal money refers to currency that you are happy to hold after receiving it (rather than quickly selling/exchanging it like situational currency), the large-scale use of a store of value often precedes the large-scale use of a medium of exchange.

The market for mediums of exchange is highly competitive. Stablecoins pegged to existing fiat currencies are most likely to achieve scalable growth in the coming years. The downside of stablecoins is that they depreciate when someone wants to hold them for more than a few months and may be subject to scrutiny/seizure by issuers or institutions influential to issuers, whereas no central authority has such power over Bitcoin.

Q: Is Bitcoin's volatility too high to be used as currency?

A: Yes and no. Volatility is not an inherent property of Bitcoin; if its various characteristics are unstable and frequently changing, that is not an inherent property of Bitcoin. Bitcoin's characteristics are quite durable and robust. Volatility is something that other countries impose on Bitcoin as they explore and adopt it.

As the network is starting from zero and entering a vast global capital ocean, it needs upward volatility to develop. Sustained upward volatility brings excitement and leverage, followed by painful corrections and deleveraging events. For this reason, it is often viewed as a long-term investment at this stage. Unlike other investments, it also gives investors monetary capabilities through liquidity, portability, and divisibility, meaning it is a type of currency asset.

If its scale becomes larger and its holdings more widespread, its volatility will decrease, whether upward or downward.

Q: If Bitcoin is priced in dollars, how can it be its own asset? Isn't it just a derivative of the dollar?

Bitcoin is an asset that can be priced in any currency. It can be priced in any currency and also priced in goods and services. Its code itself has no content related to the dollar. It is typically priced in other currencies at foreign exchange markets and traded peer-to-peer in other currencies.

The dollar is the most liquid currency in the world today. Smaller, less liquid assets are almost always priced in larger, more liquid assets, not the other way around. People use larger, more liquid currency networks as units of account and as the pricing unit for most liabilities, so that is their reference point.

Long ago, the dollar was defined by a certain amount of gold. Eventually, the dollar network became larger and more widespread than gold, and the situation reversed: now gold is primarily priced in dollars. In the long run, Bitcoin may replace the dollar in this way, but it is far from that level at present. What Bitcoin is priced in during this process does not matter; it is an untraceable asset that can be priced in any currency that is the largest and most liquid. If one day it becomes the largest and most liquid currency, then other things will naturally be priced in it.

While people can freely price it in whatever currency they want psychologically, it is unrealistic to expect most people to price in Bitcoin in the short term. Critics describing this as a flaw in Bitcoin are also misguided; for an emerging decentralized currency asset, there is no alternative but to price it in existing currencies while its scale is still small and growing.

Step Two: How Companies Integrate

As early as 2014, Pierre Rochard wrote a prescient article titled "Speculative Attacks."

A speculative attack in the foreign exchange market refers to borrowing a weak currency to buy more strong currency or other quality assets. This is also one of the reasons why central banks raise interest rates to strengthen their currency's exchange rate; it helps curb the rapid borrowing of the domestic currency relative to other currencies. If this practice does not work well, some countries will turn to direct capital controls to prevent entities from arbitraging their poorly managed currency (and these capital controls themselves have economic costs, as who would want to do business in a country tightening capital controls if there are better options?).

Wikipedia provides a useful definition:

In economics, a speculative attack refers to previously inactive speculators rapidly selling untrustworthy assets and correspondingly acquiring some valuable assets (currencies, gold).

——Wikipedia, July 2025, "Speculative Attack"

Well, Rochard described in the article that due to Bitcoin's appreciation characteristics, various entities would eventually borrow currency to buy more Bitcoin. At that time, Bitcoin's price was slightly above $600, with a market cap just over $8 billion.

Initially, borrowing money to buy Bitcoin was a marginal behavior. But now, with the Bitcoin network being highly liquid and its market cap exceeding $2 trillion, it has entered mainstream capital markets on a large scale, with billions of dollars in corporate bonds circulating specifically for the purpose of purchasing more Bitcoin.

Today, eleven years later, this situation still occurs from time to time. Is this good or bad for the Bitcoin network?

From what I see, there are mainly two types of critics who believe this is detrimental to the Bitcoin network.

The first type of critic is part of the Bitcoin user base itself. Many of them belong to the cypherpunk camp or the self-sovereignty camp. In their view, handing Bitcoin over to custodians seems dangerous or at least contrary to the network's purpose. I have seen some of them refer to supporters of Bitcoin treasury companies as "suitcoiners," and I think that term is great. The entire Bitcoin camp prefers that people hold their own private keys. Some of them go further to say that rehypothecation by major custodians could depress prices or otherwise undermine Bitcoin's ability to succeed as a free currency. While I appreciate the values of this camp (I essentially belong to this camp myself), some of them seem to hold a utopian dream that everyone should be as interested in fully controlling their funds as they are.

The second type of critic is usually someone who has held a negative view of Bitcoin in the past. They question whether Bitcoin can succeed after years of ups and downs. As Bitcoin continues to rise to new highs after experiencing multiple cycles over the years, some of them have changed their tune, claiming, "The price of Bitcoin may be going up, but it has been captured." I place less importance on this camp compared to the first, mainly viewing it as a response. It is similar to the perpetual bears in the stock market, who, when their bearish arguments fail after a decade, turn around and say, "The market is up just because the Fed printed too much money." My response is, "Well, yes, that’s why you shouldn’t be bearish."

What I want to point out to both camps is that just because some large capital pools choose to hold Bitcoin does not mean that "free-range" Bitcoin is harmed in any way. It can still be self-custodied and transferred peer-to-peer as usual. Moreover, the fact that many other types of entities hold Bitcoin makes the network larger and less volatile, thereby enhancing its utility as a peer-to-peer currency. It may also provide political cover, helping the asset normalize relative to policymakers who want to harm it. If Bitcoin reaches this scale, it is inevitable that large amounts of capital will purchase Bitcoin.

One of the skills of perpetual bears (regardless of which asset is being discussed) is to adjust the narrative as necessary, so that no matter what happens, they are correct and the asset fails. For Bitcoin, this means creating a narrative that there is no viable path to success and no reasonable definition of success. If it remains at the retail level? Then its price appreciation and ability to positively impact the world will be diminished—see, it is failing! If it is adopted by large entities and governments and continues to grow on a large scale? Then it will be captured and lose its way!

But if it is to grow, be widely accepted, and change the world to some extent, how can that path not ultimately go through companies and governments? I am inexplicably reminded of the scene in "The Notebook" where Gosling keeps asking McAdams what she wants. The bulls are Gosling, and the perpetual bears are McAdams:

In terms of who is driving the price up and who is accumulating the fastest, Bitcoin has gone through several major eras.

In the first era, people mined on computers or sent money to the Japanese card exchange (Mt. Gox) to buy Bitcoin, along with other early adopter types filled with friction. This was the ultra-early user era.

In the second era, especially after the bankruptcy of Mt. Gox, purchasing and using Bitcoin became easier. Onshore exchanges made it easier for people in many countries to buy Bitcoin than before. The first hardware wallets emerged in 2014, making it safer to self-custody Bitcoin. This was the era of retail buyers, where friction still existed but was gradually decreasing.

In the third phase, Bitcoin's scale and liquidity became large enough, and it had a long enough track record to attract more institutional investors. Various entities established institutional-grade custodians for it. Publicly traded companies began purchasing Bitcoin, and various ETFs and other financial products emerged, providing investment opportunities for various funds and managed capital pools. Some nation-states, such as the Kingdom of Bhutan, El Salvador, and the UAE, mine or purchase Bitcoin and hold it at the sovereign level. Other countries, like the United States, choose to hold confiscated Bitcoin rather than continue to sell it back to the market.

Fortunately—this is important—each era contains elements of the previous ones. Although companies currently account for most of the net buying volume, retail investors can still purchase freely. Buying and safely storing Bitcoin has never been easier. There are abundant resources explaining how to do it, a variety of affordable and powerful wallet solutions, and on-chain transaction fees are currently low.

I have seen people say, "I thought Bitcoin was supposed to serve the people, to be peer-to-peer cash. Now it's all big companies." Bitcoin indeed serves the people—anyone with internet access can buy, hold, or send it. The fact that large entities (which are also run by people) buy it does not negate that.

This is why I resonate with both the cypherpunk and suitcoiner perspectives. I hope Bitcoin can become a useful free currency, which is largely why I serve as a general partner at Ego Death Capital. We fund startups that build solutions for the Bitcoin network and its users. This is also why I support the Human Rights Foundation and other nonprofits, as they fund developers and educational institutions focused on providing financial tools for people in dictatorial or inflationary environments. However, once the principles of Bitcoin are understood, it is reasonable for large amounts of capital—whether from corporations, investment funds, or sovereign entities—to purchase it. Bitcoin's scale is large enough, and its liquidity strong enough, that it has now caught their attention.

It is important to remember that most people are not active investors. They do not buy individual stocks, nor do they deeply analyze the differences between Bitcoin and other cryptocurrencies. If they do speculate as traders, they are likely to buy at price peaks and then get wiped out at price lows. Investments are typically passively allocated to them rather than chosen by them. In the past, it was usually pensions. Nowadays, it is typically employer-matched 401(k) accounts, combined with various index funds, or investments selected for them by financial advisors.

In my view, it is unrealistic to expect billions of people to actively flock to Bitcoin. However, it is reasonable to strive to make it an option for anyone to use Bitcoin, which can be achieved through technological solutions and educational resources that lower barriers and reduce friction as much as possible. Thanks to the efforts of many, friction has never been lower than it is now.

The best expression I have seen is: "Bitcoin is for anyone, but not everyone." In practice, this means that everyone should be guided to the water's edge on this issue, but only a small portion will choose to drink.

III. Risks and Opportunities in the Era of Bitcoin Treasury Companies

On the surface, whether Bitcoin treasury companies are good or bad for Bitcoin is almost irrelevant, as the existence of companies is inevitable for Bitcoin at this scale.

Once this asset develops into a trillion-dollar liquid network, it is hard to expect it to belong solely to individuals and not to companies or governments. As an open and permissionless network, anyone with internet access can purchase it. Therefore, if Bitcoin cannot succeed in the context of purchases by companies or governments, it will never succeed. It is like a science fiction scenario where aliens invade Earth but ultimately fail due to their inability to tolerate water ("The Abyss") or resist basic bacteria ("War of the Worlds"). This was never destined to happen.

If I believed that the technical design and economic incentives of the Bitcoin network were not strong enough to support large purchases by institutional investors, I would not have bought in the first place. In fact, this was part of my reasoning for purchasing Bitcoin. I discussed this in my fireside chat at the Pacific Bitcoin Forum in 2023.

When we look beyond the surface and accept the inevitability of large entities appearing in the blockchain space, there are still many questions worth pondering. What risks does excessive corporate acquisition pose to the network? If so, can these risks be mitigated in some way?

Risks: Concentration and Control

The main risk to consider is that if Bitcoin is held by a large amount of capital, it may lose some of its decentralized characteristics.

While this concern is not to be ignored, I believe this risk is overstated because the network has strong anti-fragility. This is why it has been able to reach today’s state (16 years and counting) while remaining open and permissionless.

Bitcoin is a proof-of-work network, not a proof-of-stake network. In other words, holding a large amount of Bitcoin does not grant the holder the right to censor transactions.

Bitcoin miners can censor transactions, but only if the vast majority of miners choose to do so (i.e., most miners only mine on blocks that have previously been verified). If they do censor transactions, those censored transactions can offer high fees to attract miners to switch pools or jurisdictions to lift the network's censorship and earn those fees. Additionally, due to the low profit margins and intense competition in Bitcoin mining, miners must go to places where various cheap energy sources exist, which often disperses the concentration of jurisdictions to some extent. This is a simple yet powerful combination of technology and economic incentives.

Entities run nodes, which are software clients that operate the Bitcoin network. No one can force users to run a certain type of node software or to update it. Changing the Bitcoin network in a way that benefits corporations or governments at the expense of individual interests is not entirely impossible, but it would be an extremely arduous battle compared to widely distributed software.

Historically, Bitcoin holders have been large. In the early years, it was estimated that Mt. Gox held about 850,000 Bitcoins when the total number of Bitcoins was roughly half of what it is now. It is estimated that Satoshi Nakamoto holds over a million Bitcoins, which were mined by him and others. Given that these Bitcoins have gone through multiple booms and busts over the past 16 years, it is widely believed that the private keys to these Bitcoins have been burned or lost.

Nevertheless, monitoring potential risks is always best practice. As early as 2024, I collaborated with Ren from Electric Capital and Steve Lee from Block Inc (SQ) to write a paper analyzing Bitcoin consensus and its associated risks, which we open-sourced as a dynamic document to be updated over time to reflect changing circumstances and other viewpoints. You can view it here.

Critics of large institutions and sovereign Bitcoin holders can and should point out any existing malfeasance. People can and should support or donate to legitimate causes or software development that can benefit small users. Like any public good, it relies on millions of individual participants working in areas they care about.

Opportunities: Improving the Top-of-Funnel

With the surge of spot ETFs and leveraged Bitcoin treasury companies, the biggest opportunity facing the Bitcoin network may be that it has changed the channels through which retail investors access Bitcoin.

Until recently, most users went to cryptocurrency exchanges to buy Bitcoin, only to be lured by casino-like marketing into purchasing altcoins. The vast majority of altcoins only experience one major price surge before they begin to flip and remain stagnant relative to Bitcoin, with later retail investors ultimately becoming arbitrageurs. However, in cycle after cycle, everyone is attracted by the marketing of "the next Bitcoin." Read my article "Digital Alchemy" for more information on this topic.

Now, compared to casino-like cryptocurrency exchanges, spot Bitcoin ETFs and Bitcoin treasury companies are more likely to become the preferred way for people to access Bitcoin. They will passively invest in Bitcoin through index funds (as some Bitcoin companies have now entered top indices), and they or their advisors may consider investing in spot Bitcoin ETFs, among other options. Some of these individuals may decide to further research and consider purchasing some Bitcoin and self-custodying it to fully leverage these assets.

Another historical use of altcoins has been the desire for greater short-term gains than Bitcoin can provide, given the overall scale of the Bitcoin network. Bitcoin is already one of the best-performing assets of all time, but some people even hope for greater volatility.

Leveraged Bitcoin companies offer a more volatile investment option for those looking to invest in Bitcoin. As I mentioned earlier, the leverage employed by Bitcoin companies is often higher than what individuals and hedge funds can obtain. Some leveraged Bitcoin treasury companies operate more conservatively or aggressively than others. If people really want to speculate and trade, they can even purchase options from some of the most liquid Bitcoin treasury companies.

Thus, the outlook for altcoins could be said to have never been so bleak. Given their overall poor track record, I think this is healthy. Currently, the altcoin industry seems to have run out of excuses for how to significantly enhance its networks. Directly holding Bitcoin and/or investing in or speculating on those companies that combine Bitcoin with optimal leverage makes more sense than buying altcoins.

IV. Summary Points

To summarize this lengthy article, the development of Bitcoin monetization has roughly unfolded as follows, which is not surprising:

First, Bitcoin initially was just a collectible for enthusiasts and/or those with dreams of change. It was a brand new technology that might one day become valuable or provide some value to people, depending on the level of belief people had in it.

Second, Bitcoin began to become a useful medium of exchange in certain contexts, even attracting the attention of pragmatists who originally did not care about it. Need to remit money to a country with capital controls, like Casares? Bitcoin can succeed where other payment methods fail. Need to receive payments or donations, even though platforms like WikiLeaks have been delisted by major online payment portals? Bitcoin might be a great solution. This established a new level of utility.

Third, high volatility, countless competitors, and various frictions such as capital gains taxes have hindered Bitcoin's continued growth as a universal medium of exchange. While the use cases for Bitcoin continue to grow, the rate of growth remains relatively small compared to some people's expectations 16 years later. If you use Bitcoin at a merchant that does not hold Bitcoin, and they automatically convert Bitcoin to fiat currency, then Bitcoin's advantages cannot be fully realized, and its practicality in this use case has limits. Each currency exchange step involves friction, and for an asset/network that is "sell upon receipt," its network effects are weaker, leading to exceptionally fierce competition at this stage.

Fourth, Bitcoin is increasingly recognized as an ideal portable store of value. Unlike other cryptocurrencies, it has reached a certain level of decentralization, security, simplicity, scarcity, and scalability, making it attractive enough for people to hold with peace of mind for years. This is where the network effects are even stronger. While buying coffee with Bitcoin is not always that easy, it has begun to rank among the top ten bearer assets that can be taken abroad and exchanged for local value, surpassing the vast majority of over 160 fiat currencies in this regard.

Fifth, the Bitcoin network has reached sufficient liquidity, scale, and longevity to attract active interest from companies and governments. Large pools of managed capital are interested in this asset, and companies and funds provide them with indirect access. Meanwhile, Bitcoin continues to exist as an open and permissionless network, meaning individuals can continue to use it and develop on top of it.

Then, we can look at two additional layers that may lead if the network continues to expand:

Sixth, as the Bitcoin network continues to grow in scale, liquidity, and reduced volatility, the interest from large sovereign entities also increases. What initially was just a small sovereign fund investment could eventually become a currency reserve or a means for large-scale international settlements. Countries are continually trying to build closed-source alternative payment methods, but few have been adopted or recognized, while this open-source settlement network with its own independent unit and limited supply is gradually growing globally.

Seventh, the larger Bitcoin's scale, the stronger its liquidity, and the lower its volatility, the more attractive it becomes for short-term holding, potentially making it a more universal medium of exchange. This can only happen if a large number of people holding Bitcoin have become accustomed to it, and its purchasing power is trusted in both the short and long term.

Overall, I still believe that Bitcoin is in a good state technically and economically, and its adoption path is expanding as expected.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。