This unresolved debt collection may tear apart the last fig leaf of compliance.

Written by: Tuo Luo Finance

As the industry environment improves and the market eagerly anticipates interest rate cuts, the hearts of FTX's creditors remain restless.

After three years of twists and turns, countless disputes, the compensation process for FTX has finally started, entering its second phase. The market has not seen significant fluctuations due to selling pressure, and everything seems to be on track. However, a statement from the creditors' representative shattered the hopes of many in China.

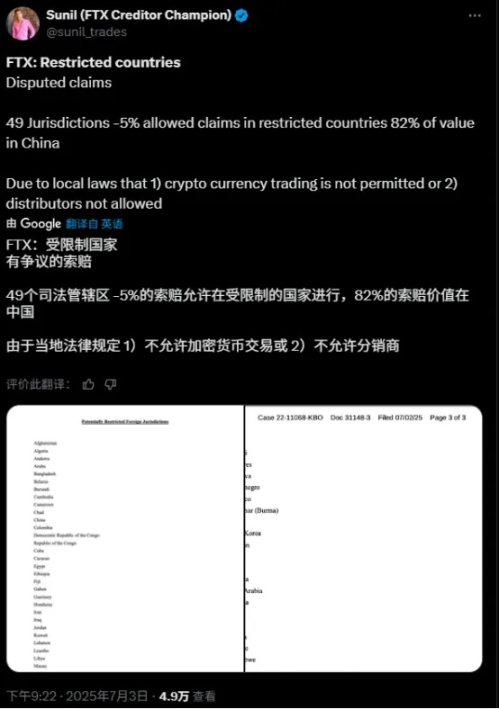

On July 4, FTX creditors' representative Sunil posted on X platform, stating that creditors from 49 jurisdictions, including China, may lose their right to claim compensation, with these regions accounting for 5% of the total claims. On July 7, he reiterated that the total claims from restricted jurisdictions amount to $470 million, with Chinese investors being the largest group of FTX creditors, holding $380 million in claims, which constitutes 82% of the restricted claims.

This news caused an uproar in the market. After years of waiting and expending significant time and energy, Chinese creditors were left facing the prospect of legal confiscation, a conclusion that no one could accept.

Since FTX announced its bankruptcy liquidation in November 2022, creditors have experienced numerous false alarms about restarting, acquiring, and restructuring. During this time, FTT became a meme coin amid the turmoil. Finally, on January 3 of this year, the FTX debtors' restructuring plan officially took effect. The first batch of debts began compensation within 60 days after January 3, prioritizing users with claims of $50,000 or less, with BitGo and Kraken assisting FTX in the compensation process.

On February 9, Kraken announced it had completed the first distribution of funds from the FTX estate, compensating over 46,000 creditors. More than three months later, the second round of compensation began, with FTX creditors' representative Sunil stating that the repayment date for FTX would be May 30, with users holding claims over $50,000 receiving 72.5% of their compensation; the remaining compensation (up to 100%) and interest would be distributed later, with expectations to distribute over $5 billion to creditors.

It was thought that creditors only needed to wait for their compensation to arrive, but a message on July 4 disrupted everyone's rhythm. Sunil tweeted that FTX would initiate a motion to seek legal advice, and if distribution to restricted foreign jurisdictions could proceed, it would continue; if it was determined that residents belonged to restricted foreign jurisdictions, claims would be disputed, and users might lose their rights to claim. The trust established 49 foreign jurisdictions, including Russia, Ukraine, Pakistan, and Saudi Arabia, with China also prominently listed. The document indicated that the deadline for creditors to oppose this motion was July 15. Additionally, creditors had a 45-day period to dispute the claims distribution.

This news hit the Chinese creditors like a hammer. Chinese creditors hold a significant proportion of the bonds, accounting for 82% of the total claims from restricted jurisdictions, with $380 million in claims. Faced with the prospect of losing such a substantial compensation, creditors found it hard to accept, and the critical question remained: why should their rightful claims be confiscated by the U.S.? Whose law is this?

Theoretically, FTX's segmented compensation approach has certain issues. Firstly, FTX, as the compensation entity, is an American company and must adhere to local laws. The U.S. Bankruptcy Code Section 1123(a)(4) clearly states "equal treatment of similarly situated creditors." In the early stages of compensation, FTX's bankruptcy liquidation team did not mention nationality but clearly stated that submitting a claim and voting in favor of the restructuring plan would allow for distribution. Secondly, consistent with traditional compensation processes, all claims are compensated in U.S. dollars, meaning that cryptocurrency does not need to be involved, and Chinese residents can receive compensation through wire transfers and traditional payment methods. Even if paid in stablecoins, according to current Chinese law, virtual currencies are recognized as property, and there is no prohibition on residents holding virtual currencies. Moreover, according to current policies in Hong Kong, a one-size-fits-all approach should not be adopted. In previous bankruptcy compensation cases, Chinese creditors were not given extra scrutiny; for example, in the Celsius case, a U.S. court successfully paid U.S. dollar compensation to Chinese creditors via international wire transfer.

From the perspective of Chinese creditors, it is hard not to suspect that this is a premeditated "legal robbery." In fact, as early as February, there were signs of this news, with creditors' representatives tweeting that FTX bankruptcy claims did not include jurisdictions like Russia and China, but at that time, creditors had not yet felt the impact.

Looking at the operations of the FTX bankruptcy liquidation team, there seems to be a clearer pattern. The liquidation team is exceptionally experienced and well-connected. John J. Ray III, the team's CEO, previously handled the Enron bankruptcy and earned over $700 million from it. This time, he brought along the same old team from the prestigious law firm Sullivan & Cromwell to carve up FTX's remaining value.

Ordinary creditors may need to consider prices when selling assets, but professional liquidation teams clearly only care about the speed of monetization. As early as the end of August 2023, shareholder reports disclosed FTX's crypto assets, with the top ten cryptocurrencies accounting for 72% of FTX's total crypto holdings, valued at approximately $3.2 billion at the time. Among these, SOL had the largest holding, reaching 55 million coins, while BTC held about 21,000 coins, and ETH held 113,000 coins. In addition to crypto assets, due to previous extensive investments, FTX also has a large equity portfolio, including high-quality assets like Cursor, Mysten Labs, and Anthropic.

Such an excellent asset portfolio ignited hope among creditors and filled the pockets of the liquidation team. Almost all these assets were sold off at bargain prices; Cursor, bought for $200,000, was sold at its original price, while its valuation had already reached $9 billion. The $890 million SUI token subscription rights were sold off for $96 million, despite its peak value reaching $4.6 billion. An 8% stake in Anthropic was sold for $1.3 billion, which seemed reasonable, but a year later, Anthropic's valuation soared to $61.5 billion, delivering a harsh slap to the market. Not to mention that the SOL tokens the team plans to auction off at low prices in 2024 have now risen to $151, making the creditors who bought them at that time very profitable.

The liquidation team's disregard is predicated on the exorbitant consulting fees they have already received. Court records show that as of January 2 of this year, FTX had paid nearly $948 million to over a dozen companies hired to handle its bankruptcy case, with court-approved fees exceeding $952 million. FTX's chief law firm, Sullivan & Cromwell LLP, has received over $248.6 million in fees, while financial advisor Alvarez & Marsal has received about $306 million. Advisors representing FTX clients and other creditors have charged approximately $110.3 million in fees. From a surface-level financial perspective, this is already one of the most expensive bankruptcy cases in U.S. history, not to mention the hidden profits arising from nepotism in asset liquidation.

This also seems to explain SBF's testimony, which was hardly believed at the time, about being severely threatened by the liquidation team, forcing FTX to quickly initiate bankruptcy proceedings. Even more frightening is that the new proposal submitted by the FTX team to the bankruptcy court contains hidden clauses that exempt advisors from liability, meaning that regardless of how things are handled later, the liquidation team bears no legal responsibility. Liquidation has completely become a tool for the team to amass wealth, while other creditors are merely the least important part of the outer circle.

Currently, the situation for Chinese creditors is indeed not optimistic. Firstly, cross-border debt collection is complex, and the deadline for opposing the motion on July 15 is very tight. If the motion passes and enters the stage where the liquidation party appoints lawyers, it will be very unfavorable for creditors. Secondly, the motion is subject to a voting system, and while Chinese creditors account for a high proportion in restricted jurisdictions, they do not even reach 5% of the total claims, with over 95% belonging to other creditors. To expedite claims distribution, the other creditors, who are not directly affected, may more easily vote in favor of the motion.

However, even so, Chinese creditors will not sit idly by. They are forming groups and protesting, making self-rescue crucial. On July 9, according to Cryptoslate, over 500 Chinese creditors questioned the freeze on FTX payments in U.S. courts. A Chinese creditor, using the pseudonym Will, stated in an interview that they have hired a U.S. lawyer, and over 500 Chinese creditors are organizing a response to FTX's decision. This creditor also urged other creditors to seek professional legal assistance or send letters of opposition to the court in their personal capacity.

In addition to taking legal action, many debt transfer schemes have emerged in the market, where debts are packaged and sold to qualified debt purchasers to quickly recoup funds. The motion has, in a paradoxical way, induced this method; according to Will, there is a clause in the motion stating, "If a third-party institution buys your debt, your original country of holding will no longer be considered when determining compensation eligibility."

As for why some are buying debts in bulk, the core essence lies in profit. In FTX's compensation, debts accrue interest at a 9% annual rate, nearing three years now, and will continue to accrue over time. Besides the guaranteed interest income, FTX is also in the process of recovering other assets, with the possibility of additional distributions later. Overall, FTX's debts are undoubtedly classified as high-quality debts, not only welcomed by individual purchasers but also favored by institutional markets. Furthermore, mature financial institutions can even package these debts as underlying assets and engage in arbitrage through derivatives.

Selling in the market is a reasonable exit strategy, but being forced to sell will clearly change the nature of the entire situation. Whether the efforts of Chinese creditors will yield returns and whether they can reclaim their rightful debts remains uncertain. As previously mentioned, even if compliant with legal regulations, the liquidation team has begun to exploit the topic of "jurisdiction" to attempt to withhold the assets of Chinese investors, raising stronger questions about the meaning of compliance. Is the purpose of compliance to protect investors' assets or to provide an unavoidable reason for confiscation?

This unresolved debt collection may tear apart the last fig leaf of compliance.

Reference materials:

https://www.theblockbeats.info/news/58868

https://www.theblockbeats.info/news/58837

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。