Original text: galaxy

Translation by: Yuliya, PANews

Bitcoin reached $112,000 this morning, setting a new historical record. This surge is the result of multiple factors, including the continued weakening of the dollar, ample global liquidity, and accelerated institutional capital entry. Galaxy reviews the market dynamics since June, analyzes the impact of geopolitical conflicts and economic data on risk assets, and explores Bitcoin's unique performance in this rebound and its future direction. Below is the original article, translated by PANews.

June Review

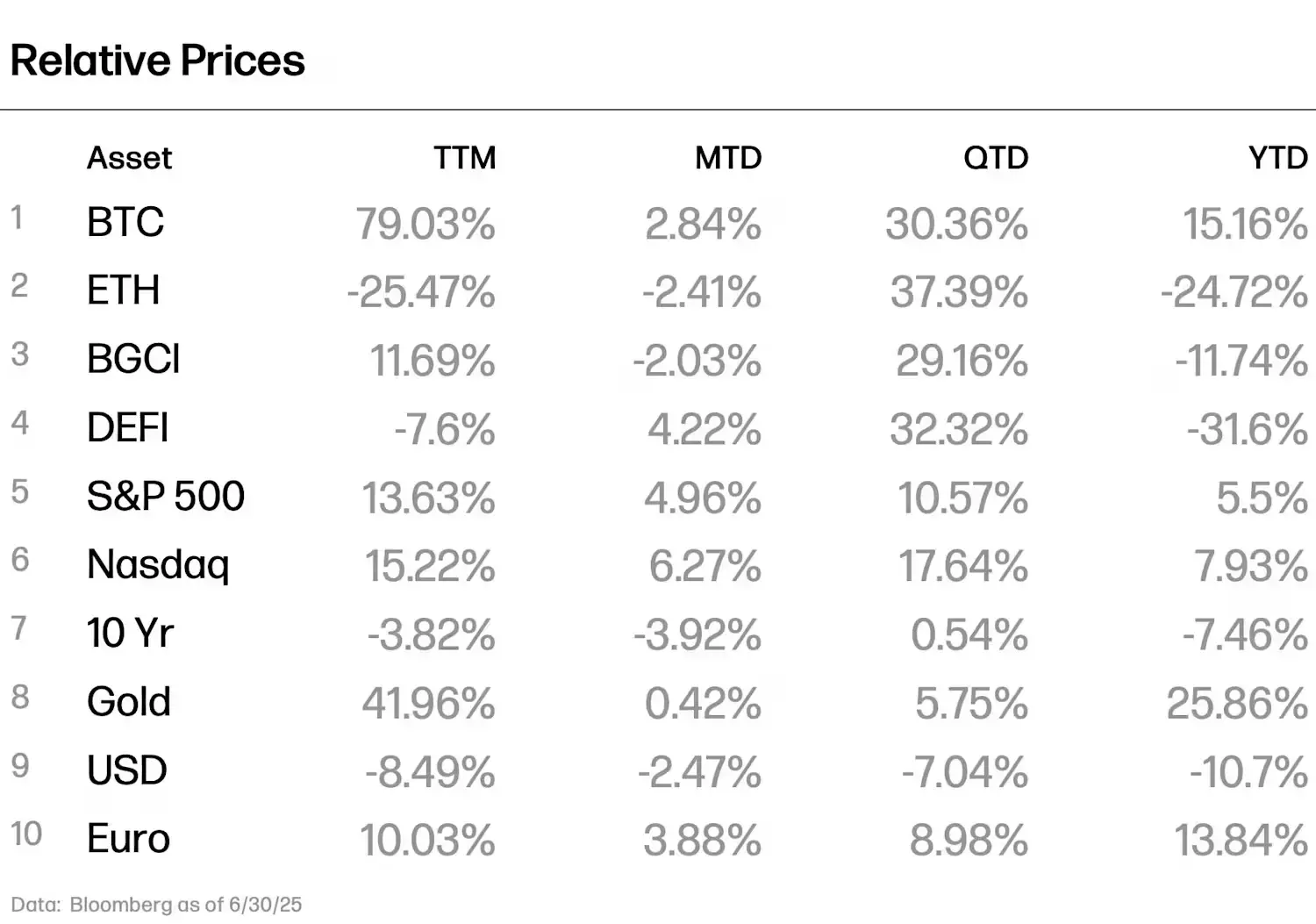

The market in June 2025 was shrouded in trade uncertainty, geopolitical conflicts, and complex economic data. However, despite the severe macro backdrop, risk assets generally rebounded. The U.S. stock market closed higher across the board, with both the Nasdaq 100 and S&P 500 indices reaching historical highs. Bitcoin briefly fell below $100,000 mid-month but then rebounded strongly, ending the month up 2.84%. In contrast, the overall cryptocurrency market fell by 2.03%, with Ethereum experiencing higher volatility and underperforming other mainstream assets, recording a decline of 2.41%.

At the beginning of the month, the market was generally optimistic, with investors digesting macro data and geopolitical situations. U.S.-China trade tensions initially escalated but eased after a phone call between the leaders of the two countries. The Chinese manufacturing Purchasing Managers' Index fell to its lowest point since 2022, and the OECD again lowered its global growth forecast. In the U.S., economic data was mixed: non-farm payrolls exceeded expectations, the unemployment rate remained stable, initial jobless claims unexpectedly decreased, while retail sales showed a decline. The June Consumer Price Index (CPI) again fell below expectations, reinforcing the view of cooling inflation. The Federal Reserve maintained interest rates at the June FOMC meeting for the fourth consecutive time, stating that it needed to wait for clearer signals regarding inflation and the labor market.

The cryptocurrency market experienced several short-term shocks in June, including a public conflict between Trump and Musk over tax policies and a brief escalation in geopolitical tensions. After the market was under pressure in the penultimate week of June, Bitcoin rebounded alongside improved market sentiment and increased institutional participation. Bitcoin ETFs saw total net inflows exceeding $4 billion in June. Ethereum faced higher volatility and deeper corrections, with specific triggers still unclear. Meanwhile, cryptocurrency treasury strategies gained attention, with several companies beginning to expand their holdings to non-Bitcoin assets such as ETH, SOL, BNB, and HYPE, indicating strong market recognition of this strategy.

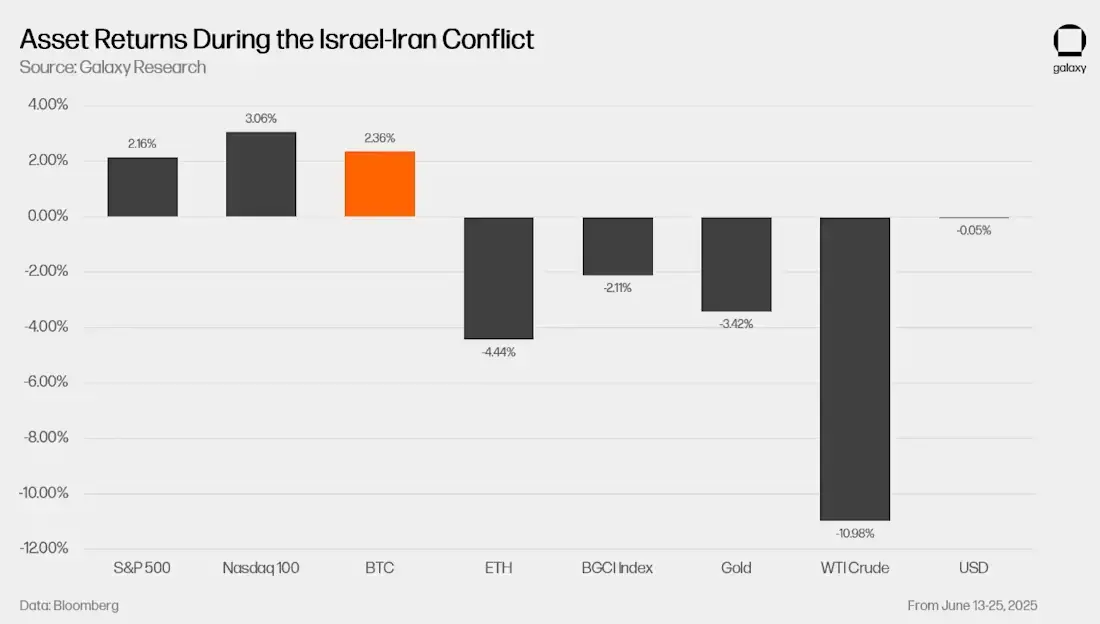

Geopolitics became the focal point in late June. On June 13, war broke out between Israel and Iran. Despite Israeli airstrikes on Iranian nuclear facilities and subsequent Iranian missile retaliation, the market initially reacted calmly. On June 21, after the U.S. airstrikes on three Iranian nuclear facilities, cryptocurrency prices fell sharply, while U.S. stocks remained stable. Trump announced a ceasefire agreement mediated by Qatar on June 24, alleviating short-term market panic. Although sporadic missile attacks continued, the cryptocurrency market gradually recovered after the ceasefire, while traditional safe-haven assets like gold and oil retreated, reflecting a decrease in market concerns about long-term conflict.

June Highlights:

- Cryptocurrency treasury craze: 53 companies are currently involved in cryptocurrency treasury allocations, covering 8 different crypto assets.

- Accelerated demand for stablecoins: After the passage of the GENIUS Act, several companies are preparing to issue their own stablecoins.

- "12 Days that Shook the World": The Israel-Iran conflict drew global attention but had limited impact on risk assets.

Diversified Allocation After BTC

An unexpected trend in 2025 is the rapid adoption of cryptocurrency treasury strategies by companies, particularly in June, where this trend significantly accelerated, with the number of related companies nearly doubling. Measured by trading volume, the scale of Bitcoin purchases by cryptocurrency treasury companies in June exceeded the total net inflows of the U.S. spot Bitcoin ETF (which was $4 billion that month).

Although Bitcoin and Ethereum still dominate, an increasing number of companies are beginning to allocate a broader range of crypto assets, such as SOL, BNB, TRX, and HYPE, indicating a growing trend of diversification beyond mainstream coins. According to Galaxy Research data, of the 53 confirmed cryptocurrency treasury companies, 36 focus on BTC, 5 allocate SOL, 3 allocate XRP, 2 each allocate ETH, BNB, and HYPE, and 1 allocates TRX, FET, along with a diversified altcoin investment portfolio.

The continuation of this trend is strongly anticipated, as some companies continue to push this strategy, while the market also shows a strong willingness to provide ample funding and support for multi-asset allocations.

However, the market has also begun to express skepticism about this strategy, particularly as some companies allocate crypto assets through debt financing, raising concerns about potential leverage risks. Currently, zero-interest or low-interest convertible bonds are commonly used; these bonds can be converted into company equity if they are "in the money" at maturity (i.e., if the company's stock price exceeds the conversion price, making conversion economically advantageous). However, if they are "out of the money" at maturity, the company must repay the principal and interest in cash, raising concerns about liquidity and solvency. Some companies even lack sufficient cash to pay interest.

In this situation, companies typically have four response options:

- Sell crypto assets to raise funds, which may exert downward pressure on market prices, affecting other treasury companies holding the same assets;

- Issue new debt to repay old debt, equivalent to refinancing;

- Issue new equity to finance debt repayment or asset acquisition, which carries less default risk;

- If asset values are insufficient to repay debts, default may occur.

The path a company ultimately takes will depend on market conditions at maturity. Generally, companies are only likely to resolve issues through refinancing when the market allows.

In contrast, the method of issuing stock to acquire more crypto assets carries less risk, as it does not involve debt and does not create mandatory repayment obligations, making it more easily accepted by the market within the overall risk structure.

According to a report released by Galaxy on June 4, current market concerns about leverage structures may be exaggerated. Most of the debt issued by Bitcoin treasury companies will mature between June 2027 and September 2028. Although the cryptocurrency industry has previously faced systemic risks due to high leverage, this type of debt structure does not currently pose an imminent threat. However, it is worth noting that if more companies adopt this strategy and issue shorter-term debt, potential risks will gradually accumulate.

Circle's IPO and the GENIUS Act Catalyze Industry Turning Point

June 2025 became a critical turning point for the stablecoin industry, primarily driven by two significant events: Circle's successful IPO and the U.S. Senate's passage of the GENIUS Act, the first comprehensive stablecoin legislation in U.S. history.

As the world's second-largest stablecoin issuer, Circle became the first native stablecoin company to go public in the U.S., with its stock price soaring over sixfold in June. While such a significant increase suggests that the IPO pricing may have been too low, more importantly, it indicates a substantial increase in investor recognition of the future infrastructural role of stablecoins.

On June 25, the GENIUS Act was passed in the Senate by a vote of 68 to 30, marking a breakthrough after months of procedural voting and political maneuvering. This included a critical procedural vote failure on May 8 due to last-minute disagreements. The bill has now been sent to the House of Representatives, where some lawmakers have suggested incorporating it into the broader CLARITY Act. However, the prospects for merging remain unclear, especially in light of President Trump's public opposition.

Under regulatory impetus, corporate interest in stablecoins continues to rise. U.S. retail giants like Walmart and Target are considering issuing their own stablecoins; Mastercard is further expanding ecosystem support by integrating stablecoin products from Paxos, Fiserv, and PayPal. These companies are not only competing to issue stablecoins but also aiming to lead in circulation scale and practical use. The industry's focus has shifted from "Can we issue?" to "Can we implement?" The success of stablecoins will depend on their penetration in real payment scenarios and user coverage.

Internationally, this trend is also gradually spreading. For example, Ripple has obtained regulatory approval for its RLUSD stablecoin in Dubai, and the Bank of Korea is exploring the issuance of a stablecoin pegged to the Korean won. However, the U.S. is currently the most advanced in this development.

Stablecoins are just the starting point. They represent the first phase of bringing traditional fiat currencies onto the blockchain, achieving the deployment of 24/7, fast interoperable infrastructure. The next phase will focus on the introduction of on-chain financial assets, starting with tokenized stocks.

Recently, Robinhood has launched a tokenized trading feature for 200 listed stocks to users in Europe, becoming a pilot platform to test user demand and execution quality. Coinbase is also seeking corresponding regulatory approval in the U.S. to promote similar products. These early attempts pave the way for the on-chain transformation of more traditional financial products, with the next steps expected to cover asset classes such as private credit and structured funds.

Limited Market Impact of Geopolitical Conflicts

The Israel-Iran war that broke out on June 13, 2025, lasted for 12 days. Although it drew global media attention, its long-term impact on risk assets was limited. In the early stages of the conflict, the cryptocurrency and stock markets reacted mildly; however, after the U.S. government initiated "Operation Midnight Hammer" and bombed Iranian nuclear facilities on June 22, cryptocurrency prices fell sharply. Following Trump's announcement of a ceasefire agreement reached with Qatar on June 24, prices quickly rebounded. Although sporadic missile attacks continued at the end of the month and the war had not officially ended, the market overall had stabilized.

During this period, Bitcoin's performance rose in sync with U.S. stocks, showing no safe-haven characteristics. Compared to April and mid-May, when Bitcoin was viewed as a store of value asset due to trade tariffs and global bond market tensions, this time it leaned more towards the logic of risk assets. Bitcoin outperformed gold and the overall cryptocurrency market, partly due to strong institutional support, including monthly inflows into ETFs reaching $4 billion, continuous purchases by treasury companies, and signs of sovereign buying, indicating that the impact of geopolitical shocks on Bitcoin was relatively short-lived.

This conflict also rekindled market interest in Iran's local cryptocurrency infrastructure, particularly the Bitcoin mining industry. According to estimates by Elliptic in 2021, approximately 4.5% of global Bitcoin mining occurs in Iran, primarily relying on low-priced government-subsidized electricity settled in rials. This structure has generated considerable profits during Bitcoin's upward cycle.

After the U.S.-Israeli airstrikes, rumors circulated that some Iranian mining farms were damaged, leading to a decline in network hash rate. However, short-term fluctuations in hash rate are often more likely caused by block time differences or data noise, and there is currently no clear evidence that this conflict caused systemic damage to mining facilities. Another possible explanation is that the heatwave in the U.S. East and Midwest regions forced miners to temporarily reduce production.

In addition to infrastructure, this conflict has also sparked discussions about the role of cryptocurrency in Iran's financial system. For a long time, high inflation, international sanctions, and an unstable exchange rate against the dollar have driven significant adoption of cryptocurrencies in the private and gray economies.

Chainalysis' past data shows that during the assassination of Hezbollah leader in 2024 and multiple missile exchanges, there was a significant increase in the outflow of Iranian crypto assets.

Bitcoin and Tron have traditionally been the main blockchain networks used in Iran, especially Tron for USDT stablecoin transfers. However, during this round of conflict, on-chain stablecoin trading and settlement volumes did not show a significant increase, indicating that the overall crypto usage pattern did not change due to the war, and the on-chain activity of short-term holders actually decreased.

Although there were no significant anomalies in on-chain data, the crypto industry emerged symbolically during this conflict: Iran's largest crypto exchange, Nobitex, suffered a $90 million hack during the hostilities, with the attackers being a pro-Israel organization called "Predatory Sparrow," leaving messages such as "F*ckiRGCTerrorists" through wallet addresses. Nobitex has previously been associated with the flow of funds related to IRGC-affiliated entities, and this attack appears more like a cyber psychological operation rather than a profit-driven attack.

Iran is one of the countries with the most severe currency depreciation and long-term sanctions. For such societies, crypto assets indeed play an important role in cross-border capital flows. The political and cyber dimensions exhibited during this round of conflict further indicate that crypto has become part of the financial systems of certain countries.

Key Variables in July Will Influence Macroeconomic and Market Trends

As we enter July 2025, the market's core focus will be on several key events and macro indicators that could significantly impact asset pricing and the overall environment.

Trump signed the "Big and Beautiful" Act on July 4, which could significantly expand the already higher-than-expected fiscal deficit. According to the latest economic data, U.S. fiscal spending continues to exceed revenue levels.

Inflation pressure remains a core consideration, but recent data shows that inflation has eased somewhat. The core Personal Consumption Expenditures (PCE) index is on a downward trend, having recorded a monthly increase only in February 2025, and that increase may primarily stem from prior pricing pressures related to tariffs. Currently, inflation seems to be under control, but the real risk lies in the Federal Reserve potentially reigniting price increases if it lowers interest rates too early.

The labor market remains tight, providing greater flexibility for Federal Reserve decision-making. June's job additions exceeded expectations, and the unemployment rate fell to 4.1%, below the most optimistic market predictions. This decline is partly due to the labor force participation rate dropping from 62.4% to 62.3%. Currently, market expectations for a rate cut in July have fallen to zero, with an overall expectation of two rate cuts for the year, depending on the direction of tariff and growth data.

Another trend to closely monitor is the continued weakness of the dollar. Economic uncertainty, unclear fiscal policy, and expectations of potential future rate cuts are collectively driving the dollar weaker. The dollar index (DXY) is heading towards its worst first-half performance since 1973. Risk assets priced in dollars benefit from a weaker dollar, which helps explain the current resilience of the stock market and the strong performance of Bitcoin, despite complex fundamental data. Meanwhile, the U.S. M2 money supply is nearing historical highs, and market liquidity is ample; if the Federal Reserve shifts to easing in the second half of the year, the dollar may come under further pressure.

Key Dates to Focus on in July:

- July 11: Consumer Price Index (CPI) release

- July 16: Producer Price Index (PPI) and Federal Reserve Beige Book release

- July 30: FOMC interest rate decision

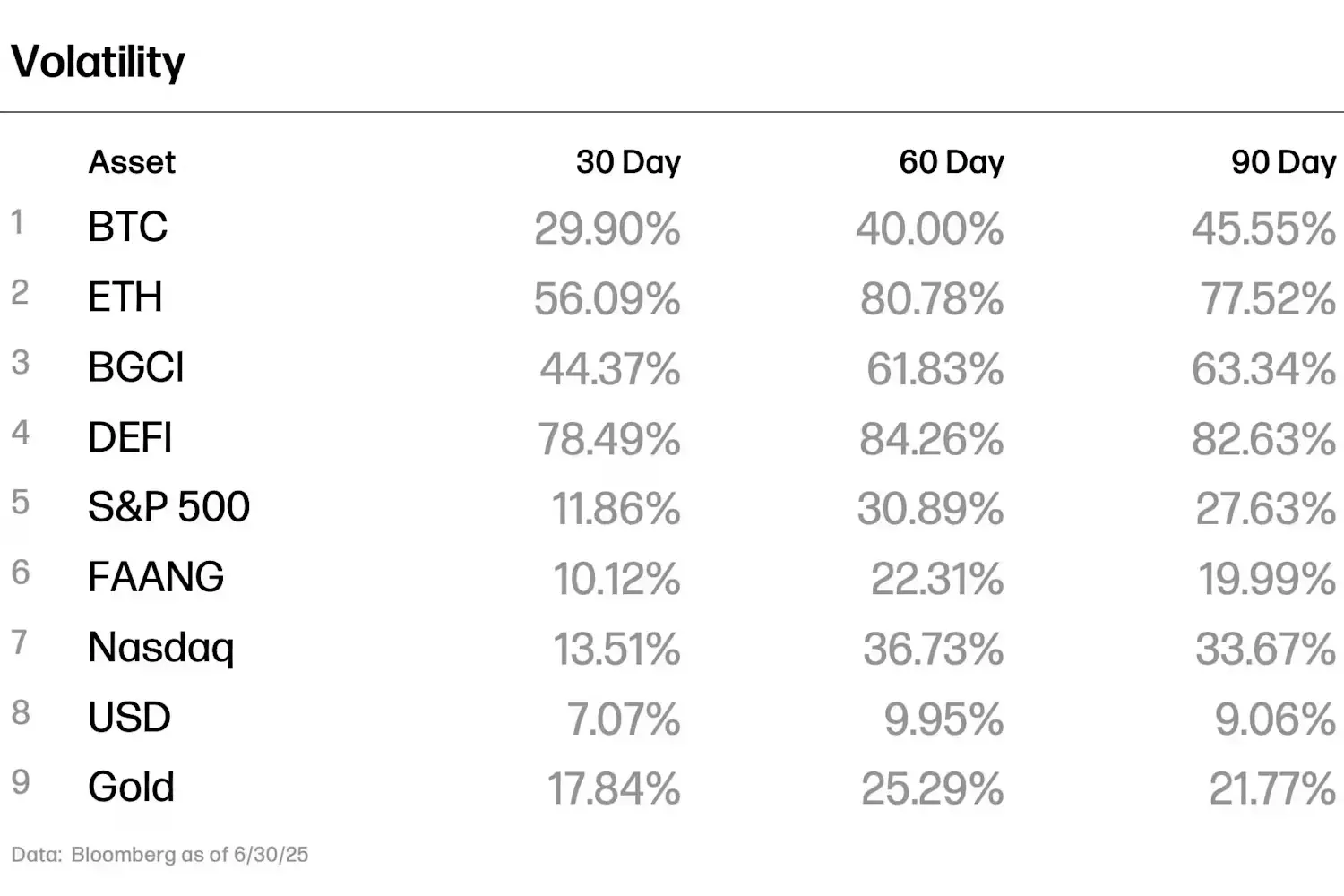

Cryptocurrency Performance

Volatility Data

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。