Author: Ethan, Odaily Planet Daily

Earnings season is the most honest moment in the capital market.

When Bitcoin and Ethereum are no longer just "considered investment targets," but enter corporate financial statements as assets, they become more than just code and consensus; they also become part of valuation models—indeed, one of the most sensitive variables in market capitalization elasticity.

In the second quarter of 2025, a group of publicly listed companies strongly tied to crypto assets delivered a diverse "mid-term report card": some achieved geometric net profit expansion through BTC's price increase, some reversed core business losses with ETH staking income, and others embedded crypto assets' "indirect exposure" in the form of ETFs.

Odaily selected six companies for an in-depth analysis—DJT, Strategy, Marathon, Coinbase, BitMine Immersion, and SharpLink Gaming. They span different industries, markets, and strategic stages, yet collectively exhibit a trend: when BTC acts as a valuation amplifier and ETH serves as a cash flow engine, corporate balance sheets are undergoing a paradigm shift.

Bitcoin in the financial statements: Faith remains the main theme, but variables are increasing

DJT: Writing stories with BTC, amplifying valuation with options

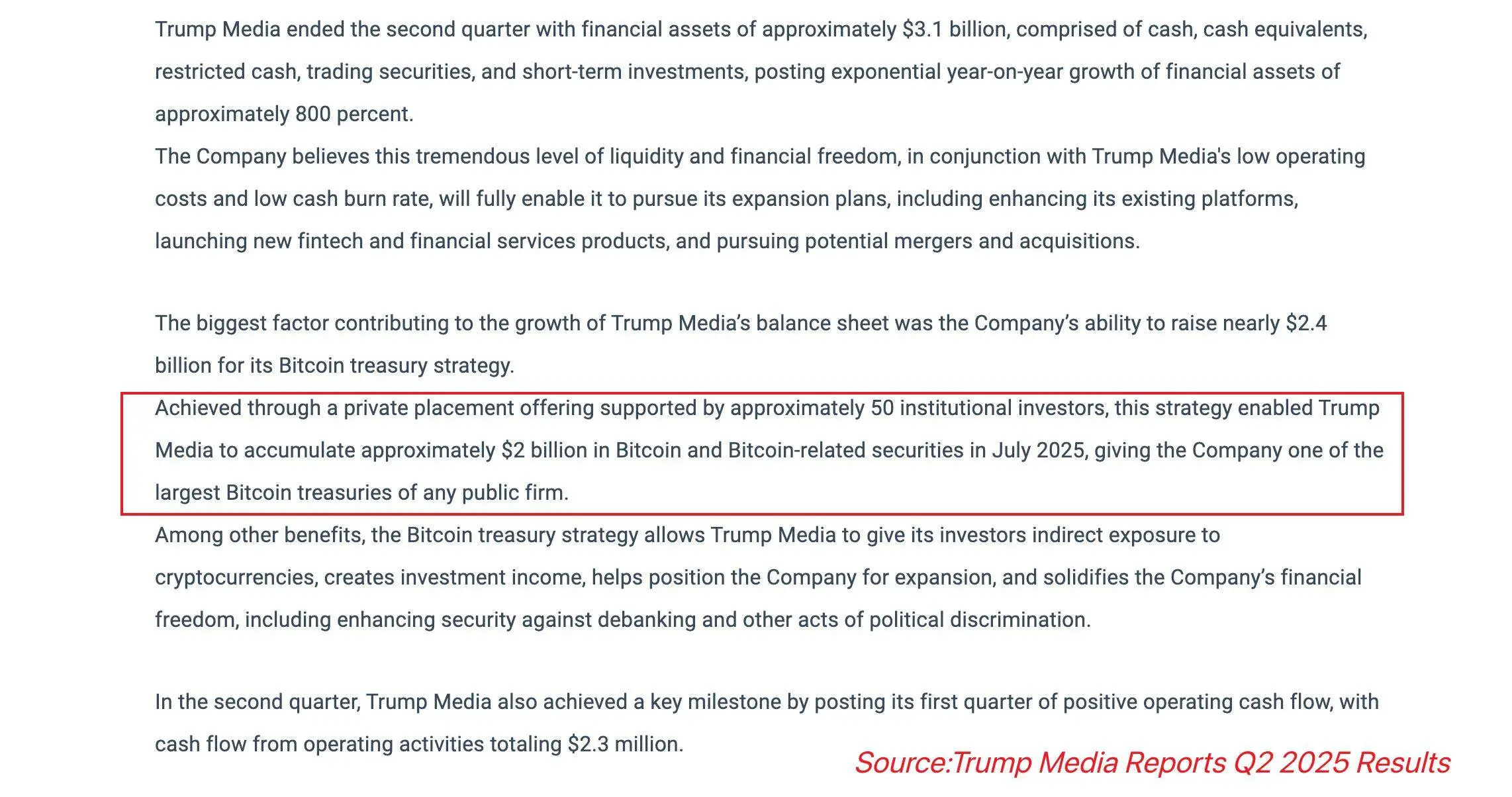

No one understands how to incorporate Bitcoin into financial reports and amplify it as a valuation engine better than DJT (Trump Media & Technology Group).

In the second quarter of 2025, DJT disclosed that it holds approximately $2 billion in Bitcoin assets, structurally comprising about $1.2 billion in spot holdings and about $800 million in BTC call options. This structural combination is essentially a "leveraged digital asset bet"—not only benefiting from price increases but also embedding non-linear elasticity in market capitalization growth.

Its EPS surged from -$0.86 in the same period last year to $5.72, with net profit exceeding $800 million, almost entirely driven by unrealized valuation gains from BTC and changes in the market value of options exposure.

Unlike Strategy's "long-term allocation," DJT's BTC strategy resembles a radical financial script experiment: leveraging market expectations of BTC's rise to write a story-driven valuation model, hedging risks from unformed business, and creating financial "narrative spillover."

At the same time, DJT's report also mentioned plans to continue developing the Truth+ reward mechanism and embedded tokens in crypto wallets, while simultaneously submitting registration applications for multiple Truth Social brand ETFs, attempting to lock in broader liquidity through a "content platform + financial products" composite path.

Strategy (MSTR): The first defender of BTC

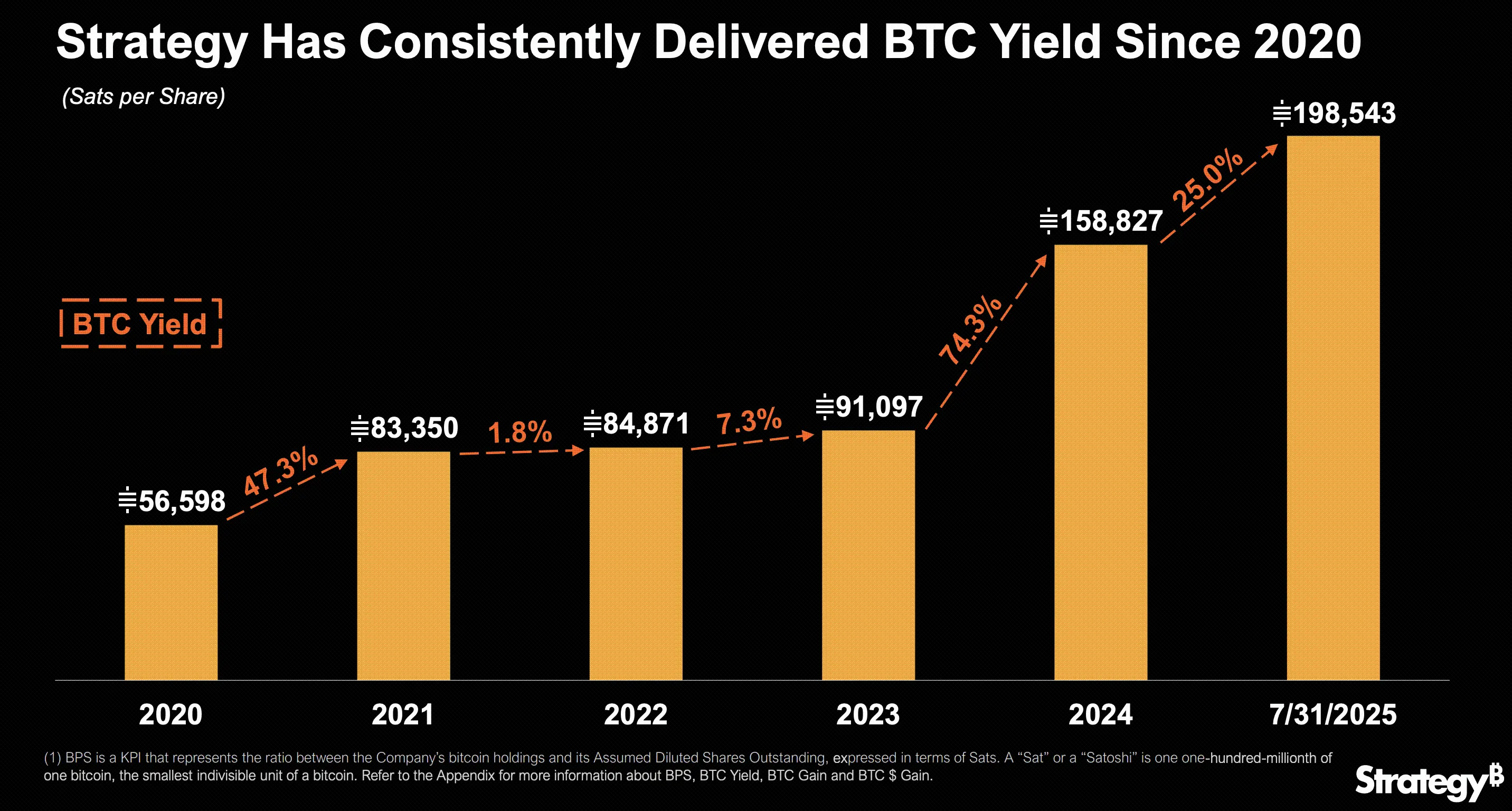

In contrast to DJT's high volatility and high elasticity path, Strategy (formerly MicroStrategy) remains a paradigm builder for BTC financialization.

As of Q2 2025, Strategy's Bitcoin holdings reached 628,791 coins, with a total investment cost of approximately $46.07 billion and an average purchase cost of $73,277, adding 88,109 coins in the quarter. Due to the company's adoption of a fair value measurement model, Q2 revenue soared to $14.03 billion, with $14 billion coming from unrealized gains on BTC, accounting for over 99%.

Traditional software business contributed only $114.5 million, making up less than 1%, and has almost become marginalized.

Its Q2 net profit reached $10.02 billion, turning a profit from a loss year-on-year, with EPS hitting $32.6, and the company expects full-year EPS to exceed $80. Meanwhile, the company announced it would raise $4.2 billion through the issuance of STRC perpetual preferred shares to continue increasing its Bitcoin holdings, showcasing a typical expansion path of "capital reinforcement, faith progression."

Strategy's model is to write Bitcoin into the main axis of financial statements during the financialization process, transforming into a "digital asset reserve platform," and highly binding BTC with the U.S. stock valuation system.

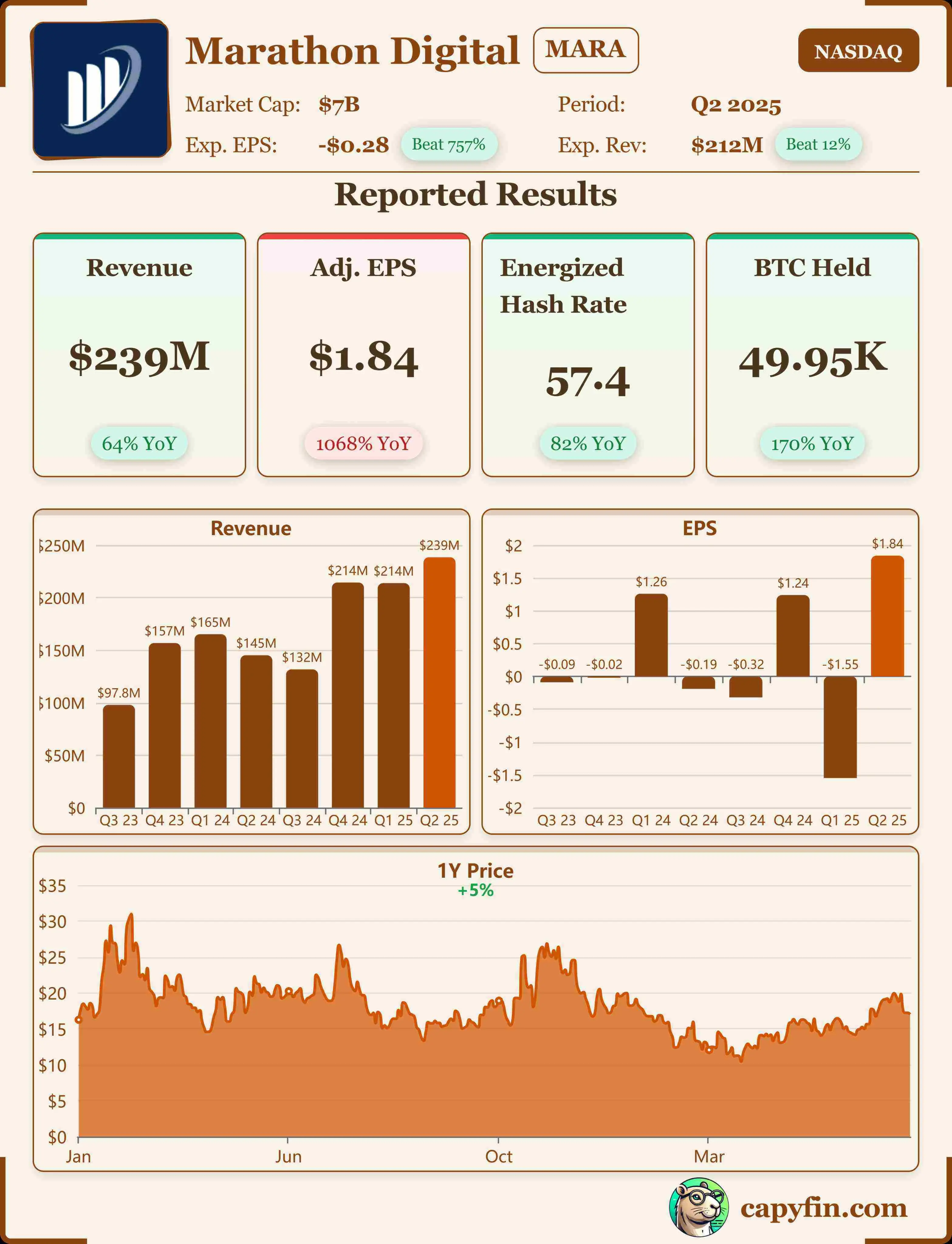

Marathon: The financial report boundaries of BTC miners

As one of North America's largest mining companies, Marathon achieved BTC output of 2,121 coins in Q2 2025, a 69% year-on-year increase, contributing revenue of $153 million. Its Bitcoin inventory reached 17,200 coins, valued at over $2 billion.

Unlike DJT and Strategy, Marathon's BTC is more of an "operational output," reflected as operating income rather than asset allocation, fitting into a typical "output faction" logic in financial reports. It cannot actively influence the balance sheet but can only passively record the income and costs brought by BTC.

Q2 net profit reached $21.9 million, with EBITDA soaring to $49.5 million, reflecting its high operational leverage in the context of a BTC bull market. However, facing structural factors such as a surge in global computing power, fluctuations in electricity prices, and halved block rewards post-halving, its report elasticity may face some compression in the future.

Marathon is a typical "computing power premium" company—when BTC rises, it generates high profits; when BTC corrects, it faces challenges at the breakeven point.

Staking companies: Is ETH the "cash flow engine" in financial reports?

Unlike the financial logic of BTC primarily focused on "valuation amplification," Ethereum, due to its native staking income capability, is becoming a tool for some companies to explore "report cash flow construction." Especially in the context of U.S. financial accounting standards allowing staking income to be classified as recurring revenue, this structure is beginning to become feasible.

Although there are currently few publicly listed companies directly holding ETH, a few "pioneers" have already demonstrated the new role ETH may play in corporate balance sheets.

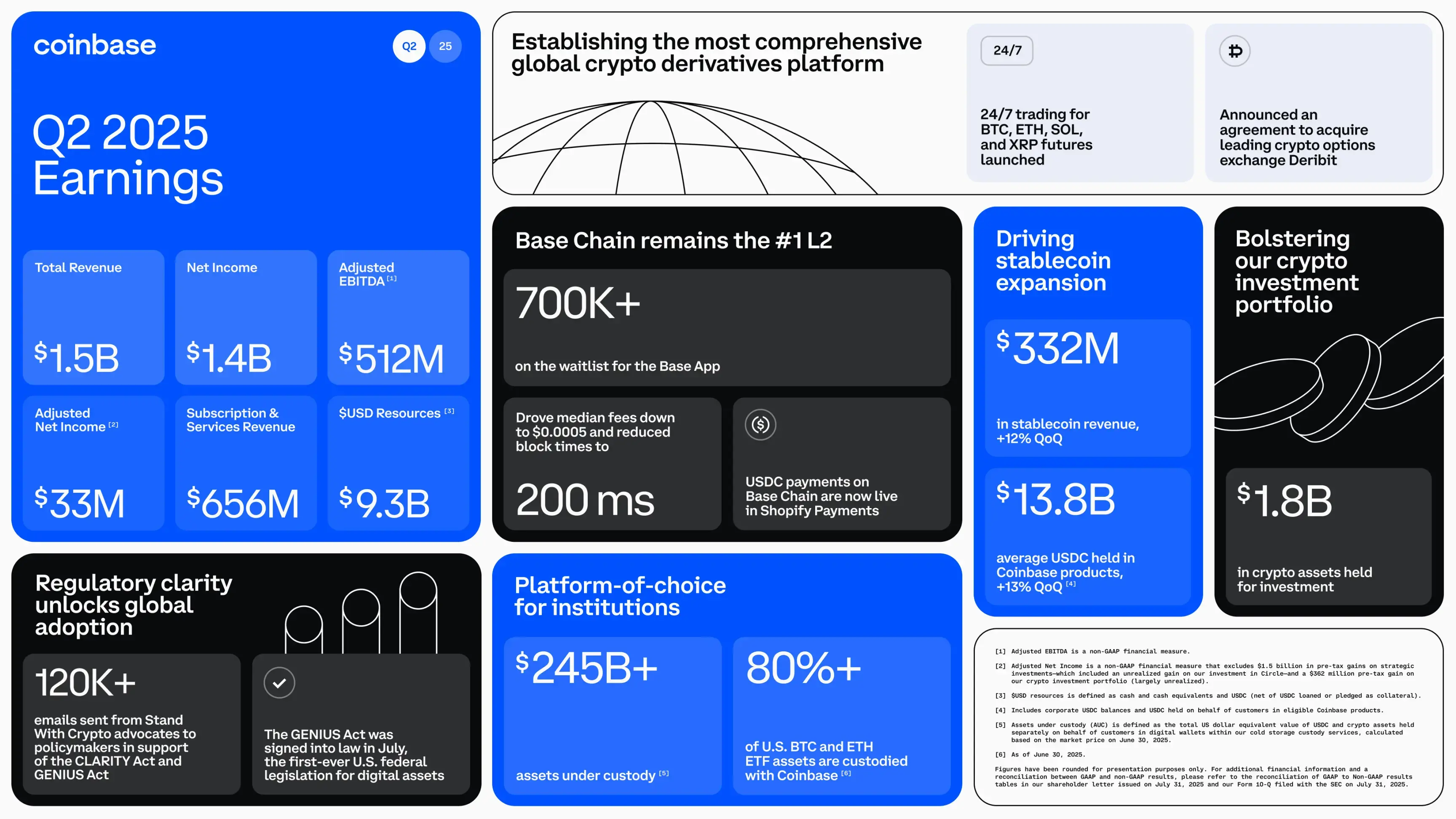

Coinbase: Revenue surpasses trading fees for the first time; ETH staking is generating measurable income under the dual-holding model

As one of the largest crypto exchanges globally, Coinbase's balance sheet includes both BTC and ETH holdings. As of June 30, 2025:

- Coinbase holds approximately 137,300 ETH in its proprietary addresses;

- Through Coinbase Cloud and Custody services, the total amount of ETH held and staked is approximately 2.6 million coins, accounting for about 14% of the total network staking share;

- Q2 staking service revenue was approximately $191 million, with over 65% coming from ETH staking, approximately $124 million.

This portion constitutes the core source of its Subscription & Services Revenue, classified as recurring revenue, and Coinbase officially included ETH staking in the recurring revenue section of its Q2 report.

In Q2 2025, Coinbase achieved total revenue of $1.497 billion, with staking service revenue reaching $191 million (accounting for 12.8%), of which ETH staking contributed approximately $124 million, with an annualized growth of over 70%.

This stands in stark contrast to a 40% decline in trading volume and a 39% quarter-on-quarter drop in trading fee revenue, with staking income becoming the core of Coinbase's counter-cyclical hedging structure. The official financial report disclosed the details of staking income for the first time, including user yield returns, platform operation shares, and self-operated node income.

Notably, Coinbase is currently the only publicly listed company systematically disclosing ETH staking income, and its model holds industry paradigm guiding value.

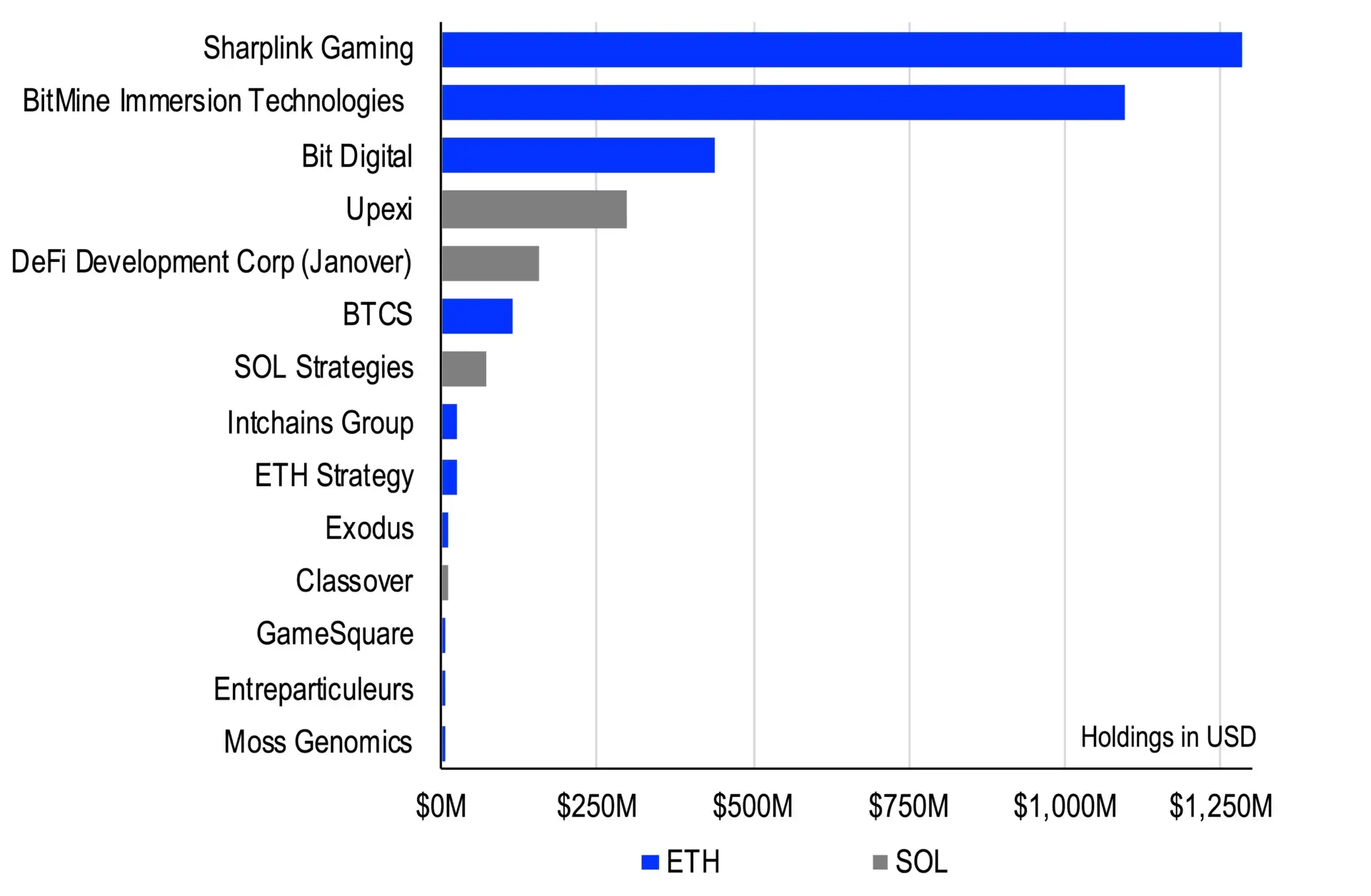

BitMine Immersion Technologies: ETH reserves first, aggressive unofficial financial model

As of now (August 2025), BitMine Immersion has not disclosed its Q2 report to the SEC, and its ETH reserves and income data mainly come from media reports and on-chain address analysis, lacking the basis for inclusion in financial analysis models, currently only possessing trend observation value.

According to multiple cross-reports from Business Insider, AInvest, and Cointelegraph at the end of July, BitMine has become the publicly listed company with the largest ETH reserves, claiming to have completed the acquisition of 625,000 ETH in Q2, equivalent to a market value of over $2 billion, with over 90% staked, yielding an annualized return between 3.5% and 4.2%.

Media speculates that its Q2 unrealized income from ETH staking rewards reached $32 million to $41 million. However, since it has not disclosed a complete financial report, we cannot confirm whether this income is included in the statements or how it is accounted for (e.g., included as "other income" or as asset appreciation).

Nevertheless, BitMine's stock price surged over 700% in Q2, with a market capitalization exceeding $6.5 billion, and it is widely regarded as a pioneering experimenter in the direction of ETH financialization, similar to MicroStrategy's positioning in BTC financialization.

SharpLink Gaming: The second-largest ETH reserve company, but Q2 report not disclosed

Based on publicly available ETH reserve tracking data, SharpLink holds approximately 480,031 ETH, ranking second only to BitMine. The company has staked over 95% of its ETH into staking pools (including Rocket Pool, Lido, and self-built nodes), creating a structure similar to a "on-chain yield trust."

According to its Q1 financial report, ETH staking income has, for the first time, covered the costs of its core advertising platform business, and it has recorded positive operating profit for the quarter. If ETH prices and yields remain stable in Q2, it is estimated that its total income from ETH staking will be in the $20 million to $30 million range.

Notably, SharpLink conducted two strategic equity financings in the first half of 2025, introducing an on-chain fund structure as collateral, and its ETH reserves were also used as "on-chain proof" for these financings, indicating that the company is actively exploring the use of ETH staking as a "financial credit tool."

However, SharpLink Gaming (NASDAQ:SBET) has not yet released its Q2 2025 financial report; its ETH reserve and income structure are derived from the Q1 2025 report and media tracking data, thus serving only as a reference for financial report structure and not constituting an investment data basis.

Conclusion

From DJT to SharpLink, these companies collectively exhibit a trend shift: crypto assets are no longer merely speculative tools or hedging configurations, but are gradually internalizing as the "financial engine" and "reporting structure variable" of enterprises. Bitcoin brings non-linear valuation amplification to financial reports, while Ethereum builds stable cash flow through staking.

Although it is still in the early stages of financialization, compliance challenges and valuation volatility remain, the Q2 performance of these six companies suggests a possible direction—Web 3 assets are becoming the "next syntax" for Web 2 financial reports.

Click to learn about job openings at ChainCatcher

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。