For speculators: what they chase is greater price increases, not who holds more Bitcoin.

Written by: Sima Cong AI Channel

There is no foolproof strategy in the financial realm.

The failure path of MicroStrategy does not require a significant drop in Bitcoin prices, and MicroStrategy is not even worried about a decline in Bitcoin prices.

For speculators: what they chase is greater price increases, not who holds more Bitcoin.

We need to clarify a widely overlooked fact: the true target of investors trading is MicroStrategy's stock, and the persistent claims by MicroStrategy's Saylor through social media platforms that Bitcoin is the promised land are not based on faith, but rather cleverly utilize the techniques of conceptual equivalence and substitution, shifting investors' expectations from stock prices to the future of Bitcoin. The financing suppliers of MicroStrategy are very aware of this but tacitly accept it; whether it is convertible bonds, preferred stocks, or common stocks, they all return to a fundamental fact: stock prices need the next buyer.

In an era of information overload and scarce faith, capital no longer merely chases profits but pursues "the securitization of narratives."

At the same time, I will systematically explain why MicroStrategy has been buying Bitcoin at price peaks.

Introduction

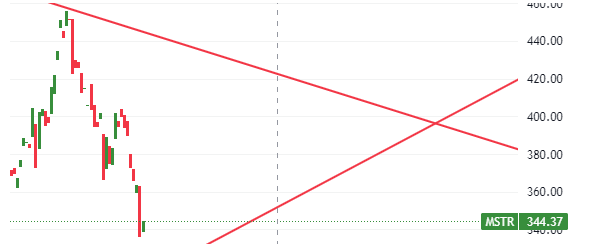

Recently, discussions about the potential operational halt of MicroStrategy's model have appeared on social media platforms, creating a widespread sense of déjà vu, triggered by the continuous shrinkage of MicroStrategy's mNAV metric, falling stock prices, and subsequent financing difficulties, leading to discussions about a possible halt.

The first issue is the continuous decline in its stock price, which has not risen alongside its Bitcoin purchases, having dropped more than 20% compared to the peak in July.

Meanwhile, Bitcoin prices have not significantly dropped during the same period.

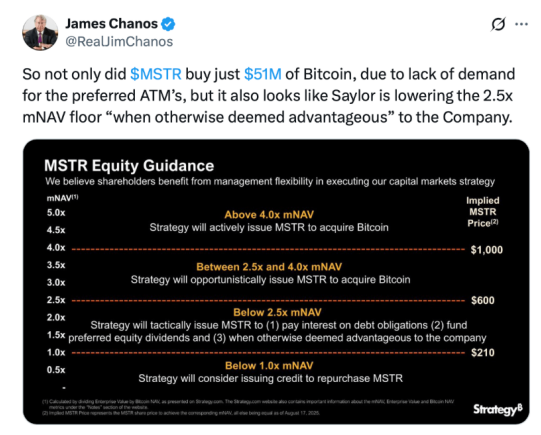

During the Q2 2025 earnings call, the company promised not to issue new common stock unless the mNAV is below 2.5 times, except for specific obligations. Many believe this promise is aimed at protecting shareholders from excessive dilution.

But the reversal was extremely rapid.

On August 18, 2025, observers insisted that the company suddenly abandoned this protective measure. Its new policy allows for stock issuance when mNAV is below 2.5 times "if management believes it is beneficial." This announcement triggered strong outrage from investors, who viewed this move as a bait-and-switch, significantly increasing dilution risk, especially as the recently reported mNAV approached 1.68 times.

On August 20, Strategy (MSTR) announced a reduction in the threshold for stock issuance to raise more funds for Bitcoin purchases.

A collective lawsuit filed this year accuses the company of making misleading statements regarding its Bitcoin strategy and financial condition. At the end of last year, investment analyst Michael Leibowitz and other critics accused the strategy company of "plundering investors" by using optimistic Bitcoin rhetoric to increase its stock volatility and achieve cheaper financing.

As for why it abandoned a promise that seemed to be made just yesterday, the reason may be the limited demand for MicroStrategy's preferred stock in the entire market.

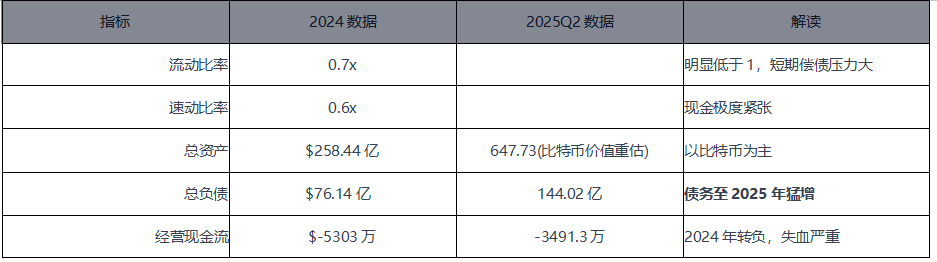

First, let's take a look at MicroStrategy's financial situation.

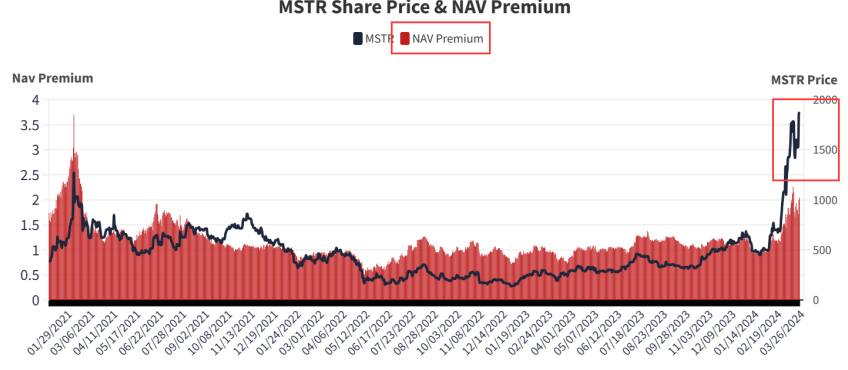

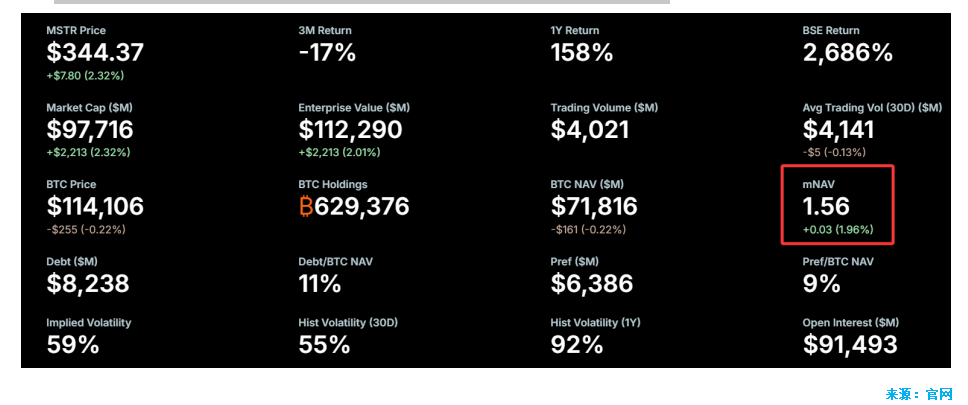

MicroStrategy's mNAV has dropped from 3.89 times in November 2024 to 1.56 times in August 2025, a significant contraction.

Now let's look at its financial data:

Using 2024 data as an example:

EBITDA: -1.85 billion USD (significant loss, reflecting pressure from core business and Bitcoin's volatility)

Leveraged free cash flow: -66.51 million USD (actual cash outflow after interest and capital expenditures, resulting in a "cash deficit")

This indicates that even with negative EBITDA, the company still has to continue paying interest and capital expenditures, further increasing cash flow pressure and risk.

EBITDA: reflects the company's "pure profitability from core business," not deducting any capital expenditures, interest, or taxes. Leveraged free cash flow: is the actual "money going into shareholders' pockets." It deducts: operating taxes, capital expenditures (such as equipment purchases, R&D investments), and all debt interest expenses.

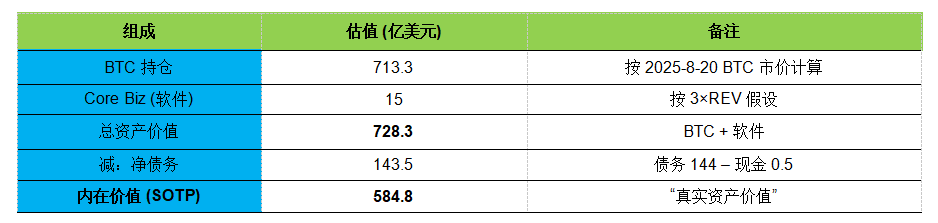

Valuation

Next, we will use the latest data to value it using two methods.

SOTP

Implied Bitcoin equity value

The EV/REV multiples for SaaS/software companies, traditional software with low growth: 2-6 times. MSTR's software business has almost zero growth, valued at 3 times.

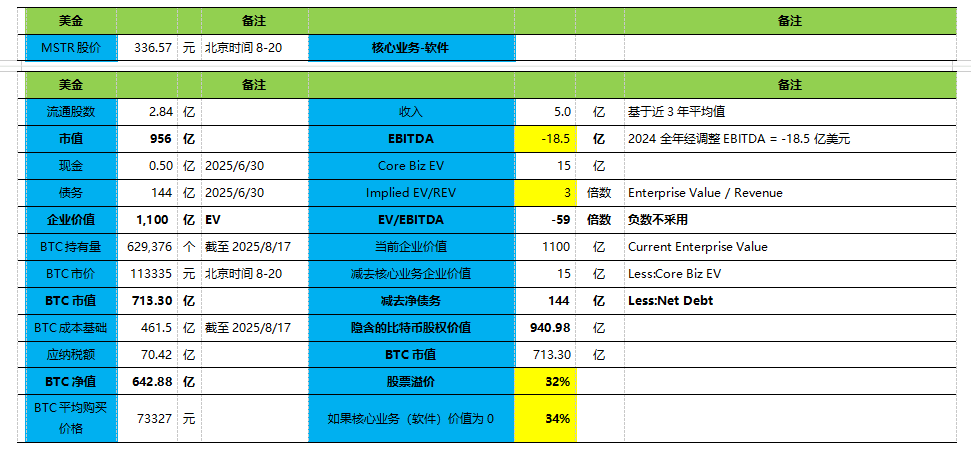

Conclusion:

MSTR's implied Bitcoin value (94.1 billion) is significantly higher than the actual BTC market value (71.3 billion);

If the core business (software) value is 0, then the premium is 34%;

Implied BTC EV = 108.5 billion, compared to the actual BTC market value of 71.3 billion → premium of 52%;

MSTR's stock price needs to reach 256.4 to eliminate the premium, requiring a further drop of 24% (336.57);

Assuming the quantity remains unchanged, Bitcoin needs to rise to 150,000 to eliminate the premium (8-20 is 113,335), requiring a 32.35% increase;

Assuming MicroStrategy stops buying any Bitcoin, with quantity and stock price remaining unchanged, even if Bitcoin prices drop to 70,000, there would still be a 112% premium;

However, if the quantity remains unchanged and Bitcoin prices stay at 120,000, if MicroStrategy's stock price drops to 200 USD, it would be a negative premium;

An undeniable phenomenon

As of May 2025, a total of 199 entities collectively hold 3.01 million BTC (approximately 315 billion USD), and this number is still rapidly growing.

According to data from Bitcointreasuries.net, there are currently 199 entities holding a total of 3.01 million BTC (315 billion USD). Among them, 147 private and public companies hold 1.1 million BTC (11.5 billion USD).

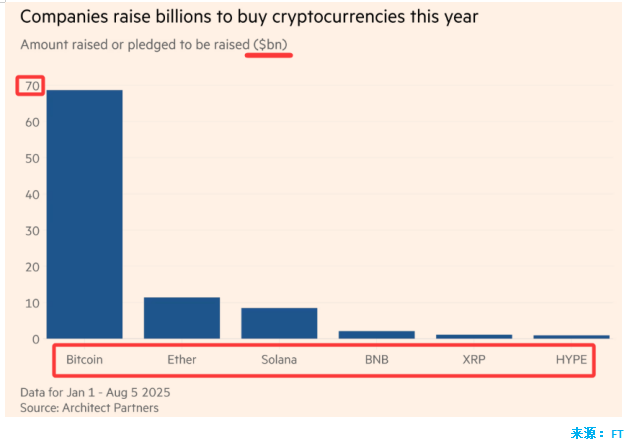

Recently, a wave of companies announced new Bitcoin treasury strategies. These companies include those diversifying their balance sheets and those specifically engaged in Bitcoin treasury management, covering different countries and industries.

As of the first half of 2025, over 40 companies have publicly announced plans to adopt Bitcoin on their balance sheets, collectively raising hundreds of billions of dollars to execute these strategies, with variations in industry, region, execution model, and listing path.

Notable examples include:

· Metaplanet (Japan): One of the earliest international participants, leveraging Japan's ultra-low interest rate environment;

· Semler Scientific and GameStop (USA): Their Bitcoin treasury strategies have attracted mainstream media attention;

· Twenty One Capital: A specialized enterprise supported by Tether and Cantor;

· Strive and Nakamoto: Rapidly listed through reverse mergers.

The expansion of Bitcoin treasury companies is still in its early stages; however, this model has begun to extend to other crypto assets—

For example: Solana: DeFi Development Corp (market cap 100 million USD, holding over 420,000 SOL), Upexi and Sol Strategies; Ethereum: SharpLink Gaming raised 425 million USD in financing led by Consensys.

A very concrete fact: stock prices have soared significantly

Metaplanet, known as the "Japanese version of MicroStrategy," has seen its stock price rise 145.59% YTD in 2025.

Sequans Communications raised 384 million USD through debt and equity financial markets to purchase the world's most popular tokens. Following the announcement, its stock price surged by 160%. However, this is an obscure semiconductor company.

Much of this can be attributed to the guidance of Bitcoin evangelist Michael Saylor. Since 2020, this American cryptocurrency giant has spent billions of dollars almost weekly purchasing Bitcoin and holding conferences to encourage others to follow suit. Saylor's company, Strategy, was originally a software company but has now transformed into a Bitcoin hoarder, with its stock price soaring over 3000% in the past five years.

Biotechnology companies, gold mining companies, hoteliers, electric vehicle manufacturers, and e-cigarette producers are all competing to purchase crypto tokens.

As of August 5, approximately 154 publicly traded companies have raised or committed to raising a total of 98.4 billion USD for purchasing cryptocurrencies. Before this year, only 10 companies had raised 33.6 billion USD.

Trump's family media company raised 2 billion USD in July to purchase Bitcoin and related assets.

Companies that can prove their commitment to continuously raising funds to purchase cryptocurrencies will be favored by investors, with valuations of these companies' stocks even exceeding the value of the Bitcoin they hold.

Underestimated but Potentially Triggering Severe Volatility Risks

The collapse of MicroStrategy may not require a significant drop in Bitcoin prices.

Why do investors pay a premium early on, hoping to gain more Bitcoin returns per share in the future? It is because if the company can quickly purchase more Bitcoin, equity investors effectively hold more Bitcoin per share indirectly.

More publicly traded companies are stepping up to announce this reserve strategy, expanding from Bitcoin to other cryptocurrencies.

These two points reveal a significantly underestimated fact: a potential crisis path.

MicroStrategy's premium convergence → financing difficulties → forced use of Bitcoin → signal effect diffusion → market chain reaction, forms a potential crisis path.

Starting point: Premium convergence — The premium of MSTR's stock price relative to its held BTC value gradually disappears.

Intermediate link: MSTR constrained — MSTR can no longer finance the purchase of more BTC at a "high premium," and the market expects its buying power to dry up.

Direct transmission: Demand weakens — As a major buyer, MSTR loses its leverage ability, amplifying the demand gap for BTC.

Endpoint: BTC decline — Investor expectations worsen, leading to a systemic decline in BTC prices.

Feedback loop — BTC decline → MSTR asset shrinkage → lower stock price → premium turns into discount → accelerates market panic.

When the market sees other similar "Bitcoin proxy stocks" with greater price increases, speculative capital will naturally flow to the higher-return targets. MicroStrategy, once the exclusive agent, is seeing its scarcity diluted by other "imitators" and more direct ETFs.

MicroStrategy's financing structure includes interest-bearing liabilities such as convertible bonds. These debts require interest payments, which are rigid expenditures. When equity financing is obstructed, the company’s most direct choice to maintain operations and debt payments is to use its most valuable asset—Bitcoin—for collateralized loans.

If Bitcoin prices do not rise significantly, or if the company can no longer obtain new loans to "service debt with debt," it will ultimately face rigid debt repayment or interest payments. Selling Bitcoin will become the only option. This scenario is entirely possible. MicroStrategy's financial model is essentially a massive, one-way Bitcoin call option; if the underlying price does not rise, it will ultimately face a liquidity crisis.

It is not about quantity. For a company that holds "buy and never sell" as a tenet and positions itself as a Bitcoin believer, even selling 1,000 Bitcoins carries far greater signaling significance than financial significance.

Faith collapse: It will send a signal to the market — Saylor's faith is not unconditional, the company's model is not infallible, and they too will yield under pressure.

Model collapse: This will trigger a trust crisis in the market regarding all "Bitcoin proxy stocks" and cryptocurrency lending models, as MicroStrategy, being the leader, will call into question the entire model if it falls.

In the game of "whoever hoards the most coins is the winner," MSTR is not irreplaceable — it is merely a "leveraged BTC holder," and the ultimate winner of this game is not the earliest player, but the one who is "wealthiest, best at financing, and most skilled at storytelling."

What everyone chases is whose stock price has a greater increase and is more speculative. The real competition is not "who believes in BTC more," but "who can finance better and whose stock price rises faster."

Although Saylor promotes Bitcoin as the "promised land," the ultimate goal investors chase is the speculative increase in stock prices. When MicroStrategy's stock price increase lags behind its peers, or even behind Bitcoin itself, investors will abandon it because its speculative value has diminished.

For speculators: what they chase is "the target with a greater and more exciting stock price increase," not who holds more Bitcoin.

This pursuit of speculation disconnects the company's fate from Bitcoin prices, instead tightly linking it to its relative stock price performance.

If hoarding Bitcoin is the promised land, then who has more money is the answer.

MicroStrategy's model lacks any moat. Its core competitiveness is merely "being the first to start," without patents, technology, or brand barriers. Any company with sufficient funds can replicate this model: issue stock, borrow, and purchase Bitcoin.

154 publicly traded companies have raised or committed to raising a total of 98.4 billion USD for purchasing cryptocurrencies, which has fully validated this point.

MicroStrategy's potential failure point is not the price of BTC itself, but the exhaustion of its stock model's attractiveness. When it can no longer attract funds through "stock market arbitrage," this model will automatically stall, and may even trigger reverse liquidation due to rigid expenditures. Bitcoin is merely its "chip"; the real core lies in "whether the market is still willing to pay a premium for its stock price."

Vulnerability of corporate financial structure;

Leverage effect of market faith;

Non-linear risks in the cryptocurrency asset ecosystem;

This is precisely the typical prelude to a "black swan" event: a seemingly localized issue (MSTR's financing difficulties) may trigger global turbulence due to signal effects.

This may even be a dead-end

This is no longer about "MicroStrategy" or "Saylor's" personal beliefs, but about the mathematics and human logic of the business model itself.

This is a game of "who rises faster": MicroStrategy's business model essentially leverages its first-mover advantage to have the market pay a premium for its stock. However, as more players enter the game, it becomes a contest of whose stock rises faster and is more attractive. If MicroStrategy's stock increase is surpassed, it will lose the favor of speculators, thereby losing its only source of financing.

The divergence between core assets and value sources:

The company's core asset is Bitcoin.

But its value source is speculative premium.

These two sources are not directly linked. Bitcoin's price can stagnate, but if new, more speculative targets emerge in the market, MicroStrategy's premium will be siphoned away.

MSTR's "rationality" is based on "relative performance advantage," not absolute value.

Investors will not say: "BTC rose, MSTR also rose, that's good."

They will say: "BTC rose 30%, MSTR only rose 10%, why don't I just buy BTC directly?"

Its life and death do not depend on the price of Bitcoin itself, but on:

Whether speculators are still willing to treat it as a "leveraged version of Bitcoin" to speculate on.

Once the market no longer believes it is the best proxy for the "promised land of Bitcoin," it will fall into the path of automatic cessation → reverse liquidation.

Why MicroStrategy has been buying at Bitcoin price peaks

This has always been a question that seems to defy common sense: even though Saylor has consistently claimed that Bitcoin is the future, why buy at peaks when Bitcoin has a public market price?

The answer is: MicroStrategy's model itself has an inherent requirement to buy at peaks.

MicroStrategy's "buying" behavior is one of the most important links in its business model, and its purpose goes far beyond merely increasing Bitcoin holdings.

For a company that heavily relies on financing, the scale of its balance sheet is crucial.

When MicroStrategy raises funds through high premiums by issuing stocks or bonds, it converts these funds into Bitcoin. This rapidly expands the company's total assets, amplifying the profit and loss statement's elasticity (recognizing gains when BTC appreciates, attracting speculative funds), making the company appear "larger" and "more powerful" on financial statements.

This scale effect makes it easier to obtain the next round of financing, whether from bank loans (using the expanded assets as collateral) or from capital market stock issuances. After completing a round of financing, the company has transferred the risk to new investors. Unless Bitcoin prices plummet to the point of insolvency, the company is safe in the short term.

This "buying at peaks" behavior is the most effective non-verbal promotion.

When retail investors hesitate about "whether this is the peak," Saylor and MicroStrategy provide the answer through their actions: "It is not."

This is a sophisticated marketing tactic that reinforces the narrative through action. It sends the market the following signals:

"We have enough confidence to buy in fully, even at the current price."

"Compared to the future value of Bitcoin, the current price is negligible."

"Don't worry, just follow us and buy."

This behavior of buying at peaks is designed to attract new "buyers." By demonstrating fearless "faith," it alleviates the fears of new investors, ensuring that funds can continue to flow in. It gives retail investors the illusion that "timing is unnecessary," demonstrating through "daring to buy at high positions" → reinforcing faith.

Two Direct Pieces of Evidence

First, Saylor has been continuously posting on the X platform about the number of Bitcoins he holds and their total market value, and second, he has been tirelessly claiming the paper profits he has realized.

1. Balance Sheet Expansion

Digital assets (BTC) are recorded at fair value:

BTC price rises → asset value skyrockets → total assets and shareholders' equity increase → asset-liability ratio improves (appears safer);

2. Profit and Loss Statement "Beautification"

If BTC price rises → generates "unrealized gains" → recorded as "other income" → reverses the micro-profit or loss of the software business → net profit turns positive → appears "profitable";

But note that these gains are unrealized, non-cash, and unsustainable, merely paper wealth, yet sufficient to support stock prices and financing.

So, this is why MicroStrategy has been buying at Bitcoin price peaks. Now, do you understand why Saylor dares to claim extreme future high prices for Bitcoin?

December 14, 2000

The U.S. Securities and Exchange Commission (SEC) today announced that two executives of MicroStrategy Inc. and its former CFO have agreed to pay a total of 11 million USD to settle civil accounting fraud charges related to the restatement of the software vendor's financial performance last March.

The SEC stated that MicroStrategy indeed agreed to a cease-and-desist order and committed to making "significant" internal changes to ensure compliance with securities laws in the future. Additionally, the company's corporate finance director and accounting manager agreed to issue separate cease-and-desist orders for violations of reporting and record-keeping.

As part of the settlement agreement with the SEC, MicroStrategy CEO Michael Saylor, along with the company's COO Sanju Bansal and Mark Lynch, resigned from their positions as CFO of the data analytics software developer earlier this year.

According to the SEC, the three executives did not admit or deny the accounting fraud charges. However, the commission stated that they agreed to each pay a civil penalty of 350,000 USD and "disgorge" a total of 10 million USD, of which Saylor accounted for 8.3 million USD. Lynch also agreed to an order prohibiting him from engaging in accounting work for at least three years.

The SEC launched an investigation after revealing in March that MicroStrategy had inflated its revenue and earnings over the past two years, necessitating a restatement of its financial performance.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。