TL;DR • Yield is not a means of appreciation, but a core part [current yield is a subsidy mechanism] • The last mile of stablecoins is not fiat currency inflow and outflow, but becoming permissionless fiat; when you cannot destroy USDT, launching alternative or permissioned currencies is meaningless • Banks screen customers, retail investors choose DeFi products • Risk control and regulation need to be "programmable," integrated into existing business flows • Regions have already been occupied by USDT, only scenarios remain; flow payments are more imaginative than cross-border payments, representing a new distribution channel rather than a mechanical "plus stablecoin" attempt by existing giants

Humans do not need banks; payments do not need humans

In 2008, under the shadow of the financial crisis, Bitcoin attracted the first batch of ordinary users disappointed with the fiat currency system, stepping out of the niche community of crypto punks.

At the same time, the term FinTech began to gain popularity around 2008, almost concurrently with Bitcoin, which may be coincidental.

It could be even more coincidental; in 2013, Bitcoin's first bull market arrived, with prices breaking through $1,000, and FinTech began to mainstream. The then-glorious Wirecard and P2P later fell, while Yu'ebao defined the yield system of the internet era, and Twitter founder Jack's new payment solution Square reached a valuation of over $6 billion.

This was not artificially manufactured; since 1971, the growth rates of gold prices and U.S. Treasury debt have been almost synchronized at 8.8% vs. 8.7%. After the gold dollar came the petrodollar; will the new energy dollar be stablecoins?

From a regulatory perspective, FinTech is the salvation of the banking industry, aiming to rebuild or supplement the financial system with internet thinking, hoping to create an internetized financial system amidst the tangled political and business relationships.

Starting from the payment sector, it has become a global consensus, encompassing acquiring, aggregation, P2P, cross-border settlement, and micro-lending, crossing boundaries and mixed operations, creating endless prosperity or crises.

Unfortunately, the unintentional success of the willow tree has overshadowed the real change in banks and the traditional financial system, which is driven by blockchain practices, moving from the margins to the mainstream, all happening outside of regulation.

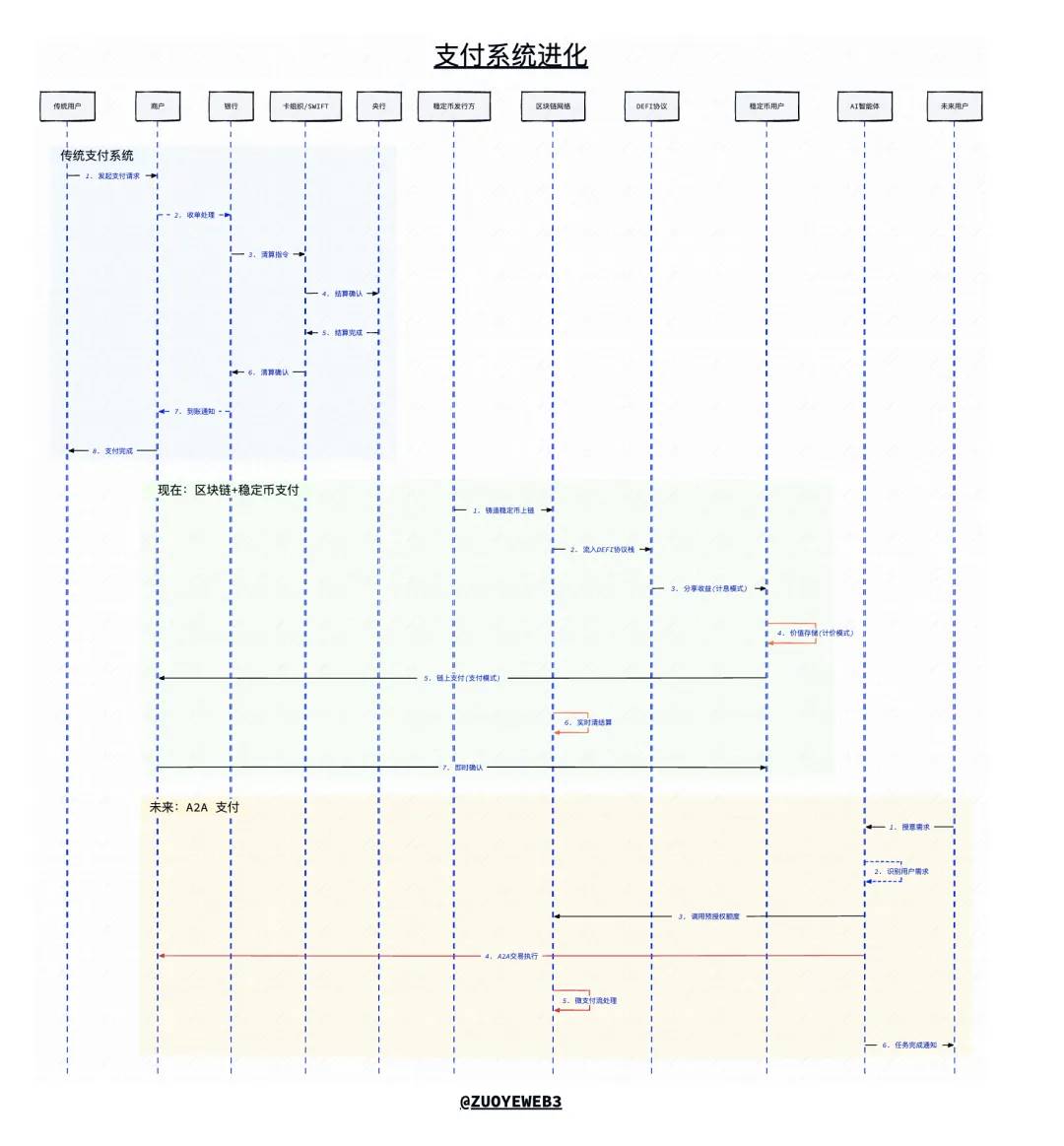

Image description: Evolution of payment systems

Image source: @zuoyeweb3

Payments are rooted in code rather than finance

Yield-bearing stablecoins using USDT for dividends serve as a maturity judgment marker.

Payments, for hundreds of years, have operated at the core of the banking industry; all electronic, digital, or internet-based advancements have been built to support the banking sector until the emergence of blockchain.

Blockchain, especially stablecoins, has created an inverted world, completely reversing the order of payment, clearing, and settlement; only after confirmation can clearing and settlement occur, allowing the payment process to be completed.

In the traditional banking system, the payment issue is essentially a bifurcated process of front-end transfers and back-end clearing, with the banking industry at the absolute center.

Under FinTech thinking, the payment process is about aggregation and B-end services; the internet's customer acquisition mindset demands that no acquiring traffic be overlooked, as traffic determines the confidence of FinTech companies in facing banks. Fake it till you make it; network connections and margins are accepted as the final result.

In blockchain thinking, stablecoin systems like USDT, with Tron as the earliest stablecoin L1 and Ethereum as a large-scale clearing and settlement system, have achieved the "programmability" that should have been realized by the internet.

The lack of interconnectivity is an external manifestation of platforms competing for territory; the core issue is the insufficient degree of dollar internetization. Being online is always just a supplement to the fiat currency system, but stablecoins are a native asset form for blockchain, allowing any public chain's USDT to be exchanged with each other, with friction costs depending solely on liquidity.

Thus, based on the characteristics of blockchain, only after verification can clearing and settlement be confirmed before payment, with Gas Fees determined by market mechanisms, allowing for real-time circulation after confirmation.

A counterintuitive thought: blockchain did not give rise to stablecoin systems through unregulated arbitrage, but rather the efficiency brought by programmability has shattered the traditional financial system.

Important

Payments are an open system rooted in code rather than finance.

We can provide a counterexample: the reason traditional bank wire transfers take time is not merely due to compliance requirements and outdated network architecture; the core issue is that participating banks have a "retention" demand, as massive funds generate continuous yields, the user's time becomes passive compounding for the banking industry.

From this perspective, after the Genius Act, the banking industry continues to frantically block yield systems from entering the banking system, with the superficial reason still being yield, or that paying interest to users would distort the banking industry's deposit and loan mechanisms, ultimately leading to systemic crises in the financial industry.

The on-chain programmability of yield systems will ultimately replace the banking industry itself, rather than create more problems than the banking industry, as this will be an open system.

Traditional banking earns from the interest spread between user deposits and loans to businesses/individuals, which is the foundation of all banking operations.

The interest spread mechanism gives the banking industry the dual power to select users, creating unbanked populations on one side and selecting businesses that do not meet "standards" on the other.

Ultimately, losses caused by triangular debts or financial crises created by banks are borne by ordinary users; in a sense, USDT is similar, as users bear the risk of USDT while Tether takes the issuance profits of USDT.

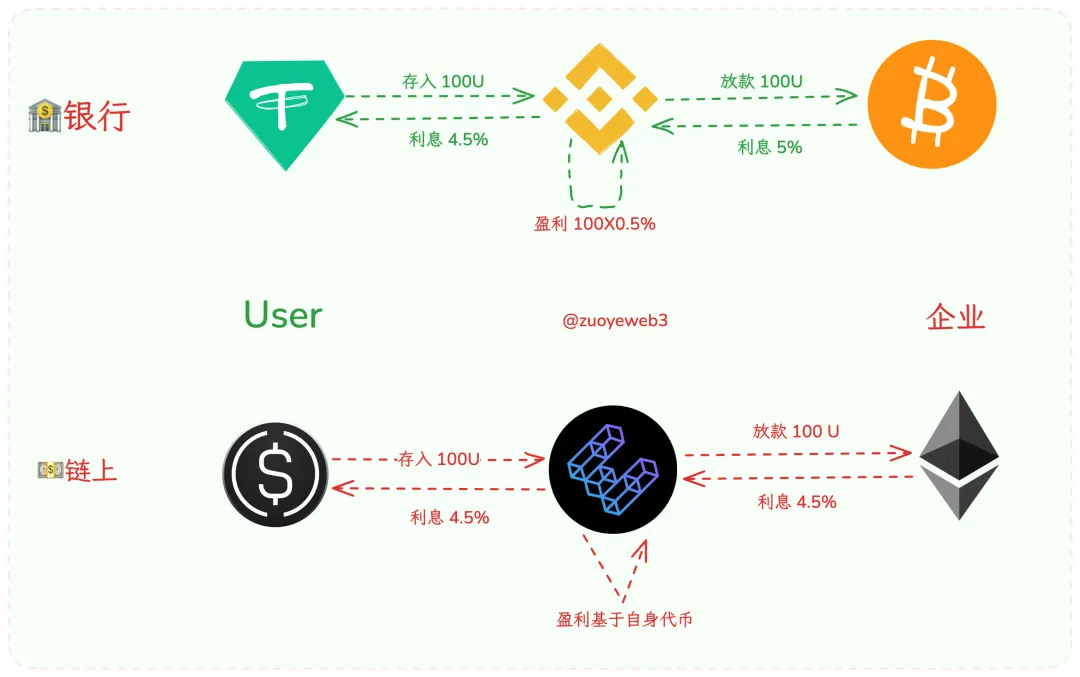

YBS (Yield-bearing Stablecoins) like Ethena do not rely on the dollar for issuance and do not operate under the traditional banking interest spread mechanism, but are entirely based on on-chain facilities like Aave and public chains like TON for payment attempts.

Currently, yield-bearing stablecoin systems have created a globally liquid payment, interest calculation, and pricing system, with the banking industry becoming the target of transformation by stablecoins, not through altering the participation methods of payment processes, but by changing the intermediary status of credit creation in the banking industry.

In the face of the offensive from yield-bearing stablecoins, small banks are the first to bear the brunt. Minnesota Credit Union has already attempted to issue its own stablecoin, and previous Neo Banks are rapidly moving on-chain, such as Nubank starting to reattempt stablecoins.

Even SuperForm and others are beginning to transform themselves into stablecoin banking systems, sharing profits generated by banks with users, thereby correcting the distorted banking system.

Image description: The impact of YBS on the banking industry

Image source: @zuoyeweb3

In summary, yield-bearing stablecoins (YBS) are not merely a customer acquisition channel, but a precursor to reshaping the banking industry; the on-chain migration of credit creation is a more profound transformation than stablecoin payments.

FinTech has not replaced the role of banks but has improved segments that banks are unwilling or unable to engage in. However, blockchain and stablecoins will redefine banks and currency.

We hypothesize that YBS will become the new dollar circulation system; payments themselves are synonymous with on-chain payments. Again, note that this is not a simple on-chaining of the dollar; unlike the internetization of the dollar, on-chain dollars are the fiat currency system.

At this stage, the traditional payment system's view of stablecoins remains limited to clearing and cross-border areas, which is a completely erroneous established mindset. Please grant stablecoins freedom; do not embed them into outdated and obsolete payment systems.

Blockchain inherently does not distinguish between domestic and foreign, card/account, individual/business, or receiving/sending; everything is merely a natural extension and variation of transactions. As for stablecoin L1's enterprise accounts or privacy transfers, they are merely adaptations of programming details, still adhering to the basic principles of blockchain transactions: atomicity, irreversibility, and immutability.

Existing payment systems remain closed or semi-closed; for example, SWIFT excludes specific regional customers, and Visa/Mastercard require specific software and hardware qualifications. A comparison can be made: the banking industry rejects unbanked individuals without high profits, while Square and Paypal refuse specific customer groups; blockchain accepts all.

Closed systems and semi-open systems will ultimately yield to open systems; either Ethereum becomes the stablecoin L1, or stablecoin L1 becomes the new Ethereum.

This is not blockchain engaging in regulatory arbitrage, but a dimensionality reduction brought about by efficiency upgrades; any closed system cannot form a closed loop, and transaction fees will diminish at various stages to compete for users, either leveraging monopolistic advantages to increase profits or using regulatory compliance to exclude competition.

In an open system, users possess absolute autonomy; Aave does not become the industry standard due to monopoly but because the DEX and lending models of Fluid and Euler have yet to fully explode.

Regardless, on-chain banks will not be tokenized deposits of the banking industry but rather tokenized protocols rewriting the definition of banks.

Warning

Replacing banks and payment systems will not happen overnight; Paypal, Stripe, and USDT are products from 20, 15, and 10 years ago, respectively.

Currently, the issuance volume of stablecoins is around $260 billion; we will see an issuance volume of $1 trillion in the next five years.

Web2 payments are a non-renewable resource

Credit card fraud handling largely relies on experience and manual operations.

Web2 payments will become the fuel for Web3 payments, ultimately completely replacing rather than supplementing or coexisting.

Participating in the future based on Stripe and Tempo is the only correct choice; any attempt to incorporate stablecoin technology into the existing payment stack will be crushed by the flywheel—it's still an efficiency issue. On-chain YBS separates yield rights and usage rights, while off-chain stablecoins only have usage rights; capital will naturally flow towards appreciation tracks.

While stablecoins strip the banking industry of its social identity, they also clear the established thinking of Web2 payments.

As mentioned earlier, the issuance of stablecoins is gradually breaking away from mere imitation of USDT; although completely breaking away from the dollar and banking system is still far off, it is no longer a complete fantasy. From SVB to Lead Bank, there will always be banks willing to engage in cryptocurrency business, a long journey of persistent effort.

By 2025, not only will the banking industry accept stablecoins, but the major obstacles that have troubled blockchain payment businesses will gradually thaw. The resonance of Bitcoin has already become the booming sound of stablecoins.

• Inflow and outflow: No longer pursuing the finality of fiat currency, people are willing or inclined to hold USDC/USDT to earn yields, use directly, or preserve value against inflation. For example, MoneyGram and Crossmint are collaborating to handle USDC remittances.

• Clearing and settlement: Visa has completed $1 billion in stablecoin clearing volume, with Rain as its pilot unit, and Samsung as an investor in Rain. The anxiety of old giants will become a funding source for stablecoin payments.

• Large banks: RWA or tokenized deposits are just appetizers; considering competition with DeFi is not far off. The evolution is a passive adaptation of traditional finance, with internet alliances like Google AP2 and GCUL representing the unwillingness and struggle of old-era hegemons.

• Issuance: From Paxos to M0, traditional compliance models and on-chain packaging models are advancing simultaneously, but yield systems will be taken into account. Although Paxos's USDH plan failed, empowering users and tokens is a common choice.

In summary, the competition for positioning in stablecoin on-chain payments has ended, and the combination competition has begun, namely how to push the network effect of stablecoins globally.

In a sense, USDT has already completed the push of stablecoins into Asia, Africa, and Latin America; there is no new growth space in regions, only "scenarios" remain. If existing scenarios are to be enhanced by payment players with "blockchain."

Then, the only option is to seek new "blockchain+" / "stablecoin+" scenarios, which is the clever use of internet strategies in Web3, buying traffic for growth, cultivating new behaviors; the future will define today's history, and Agentic Payment will definitely be realized.

After changing the banking industry and payment systems, let's delve into the future of payment systems under an agent-oriented approach. Please note that the following discussion completely disregards the scenarios of "+blockchain" or "+stablecoin," as it would be a waste of ink; the future will have no market space for existing payment giants.

Yield systems can incentivize end-user usage, but new payment behaviors require supporting consumption scenarios. For example, using cryptocurrency for consumption in a built-in mini-program on Binance is reasonable, but using a bank card in a WeChat mini-program is quite strange.

Brand new scenarios, from the perspective of Google, Coinbase, and even Ethereum, can only be A2A (Agent 2 Agent), requiring no deep human involvement. Web2 payments are a non-renewable resource because the future will be omnipresent in payments.

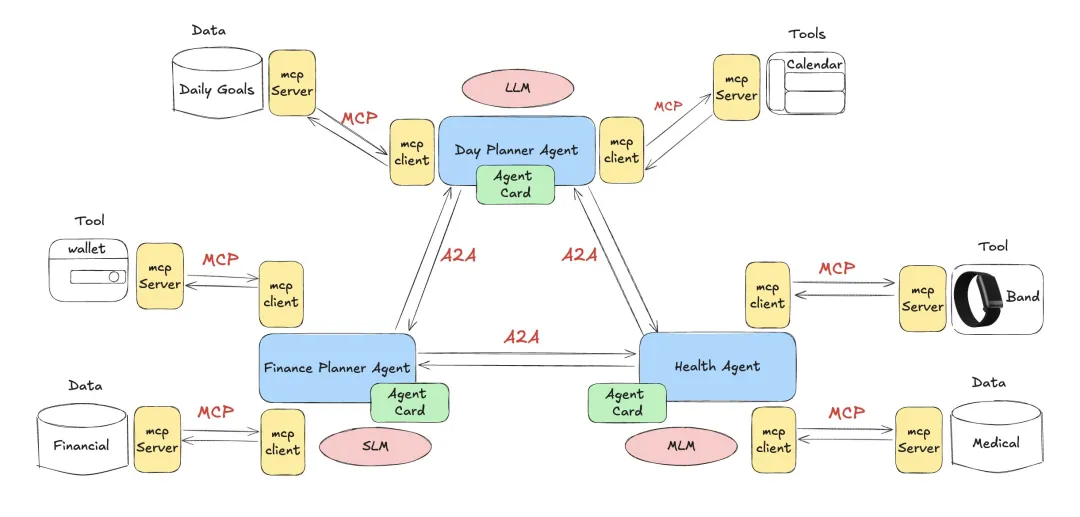

In simple terms, in the future, people will have multiple agents handling different tasks, while the MCP (Model Context Protocol) will configure resources or call APIs within agents, ultimately presenting us with agents matching and creating economic value.

Image description: Connection between A2A and MCP

Image source: @DevSwayam

Human behavior will be more reflected in delegation rather than authorization; it is necessary to transfer multidimensional data from the delegator to allow AI agents to meet your intrinsic needs.

Note

• The value of humans lies in authorization

• Machines operate tirelessly

Existing pre-authorization and pre-payment, buy now pay later, acquiring/issuing, clearing/settlement will occur on-chain, but the operators will be agents. For instance, traditional credit card fraud requires manual processing, but agents will be smart enough to identify malicious behavior.

From the perspective of the existing payment stack and the "central bank—bank" system, it may indeed seem that the above thoughts are overreaching. However, do not forget that the digital yuan's "immediate payment and transfer" also stems from a yield perspective, ultimately compromising with the banking system.

It is not that it cannot be done, but that it cannot be done.

Google is pulling the AP2 protocol built by Coinbase, EigenCloud, and Sui, which has already been highly integrated with Coinbase's x402 gateway protocol. Blockchain + stablecoin + internet is currently the optimal solution, targeting microtransactions. In their vision, real scenarios include real-time cloud usage, article paywalls, etc.

How to say it? We can be confident that the future belongs to AI agents, transcending clearing and settlement channels, but the specific path of how it changes humanity remains unknown.

The DeFi sector still lacks a credit market, which is naturally suitable for corporate development. However, in the long term, the retail or individual market relies on an over-collateralization mechanism to become the main force, which is itself an abnormal phenomenon.

Technological development has never been able to imagine the path of realization; it can only outline its basic definitions. Fintech is like this, DeFi is like this, and Agentic Payment is too.

Caution

The irreversible nature of stablecoin payments will also give rise to new arbitrage models, but we cannot imagine their harmfulness.

Additionally, existing distribution channels will not be the core battlefield for the large-scale use of stablecoins. There may be usage volume, but it will damage their yield potential in interacting with the on-chain DeFi stack. This remains a fantasy that the emperor will use a golden hoe to dig vegetables.

Stablecoin payments can only be called a Web3 payment system after replacing banks and existing distribution channels.

Conclusion

The path to realizing my imagined future non-bank payment system: yield + clearing and settlement + retail (network effect) + agent flow payments (after breaking free from the self-rescue of old giants).

The current impact is still concentrated on Fintech and the banking industry, with little ability to replace the central bank system. This is not because it is technically unfeasible, but because the Federal Reserve still plays the role of the ultimate lender (the scapegoat).

In the long run, distribution channels are an intermediate process. If stablecoins can replace bank deposits, no channel can lock in liquidity. However, on-chain DeFi has no entry barriers and unlimited users; will this trigger an even more violent financial crisis?

The Soviet Union could not eliminate the black market, and the United States cannot ban Bitcoin. Whether it is a catastrophic flood or a happy shore, humanity has no way back.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。