Original Title: "The Fund Shorting MicroStrategy Sets Its Sights on Ethereum Treasury Company"

Original Author: Eric, Foresight News

On the evening of October 8, Beijing time, at 21:47, which is 8:47 AM local time in New York on the same day, the short-selling institution Kerrisdale Capital publicly announced on X that it has shorted the stock of Ethereum treasury company BitMine (BMNR). Kerrisdale stated in its tweet that it does not have a negative outlook on Ethereum; it simply believes that the premium of BitMine's stock price relative to its net asset value due to the treasury company model is about to disappear, and Kerrisdale is betting on a decline back to parity or even a discount.

This shorting of BMNR is not Kerrisdale Capital's first foray into shorting crypto concept stocks. In mid-2024, it shorted Bitcoin mining company Riot and the ancestor of DAT, Strategy (formerly known as MicroStrategy), and the stock prices of the companies being shorted saw a significant decline after the news of Kerrisdale's shorting was released. This time, after Kerrisdale announced its short position on BMNR, the stock price did not immediately show a significant drop; the large decline last night was more in line with the overall market trend. However, in terms of price, the closing price of BMNR on October 10 (52.47 USD) was down more than 10% from the closing price on the 8th (60 USD).

A close reading of the short report reveals that Kerrisdale's six reasons for shorting BitMine's stock hit the nail on the head, and unlike when it shorted Riot and Strategy while simultaneously going long on Bitcoin as a hedge, this time the naked shorting of BMNR reflects Kerrisdale's extreme pessimism towards BitMine.

"The Flywheel" Has Become a "Death Spiral"

Kerrisdale's bearish outlook on BitMine is based on six main reasons:

1. Severe dilution of Ethereum per share: BMNR has issued over 240 million shares through ATM (at-the-market) offerings in just three months, raising over 10 billion USD, with an average daily financing of about 170 million USD, severely diluting the Ethereum content per share;

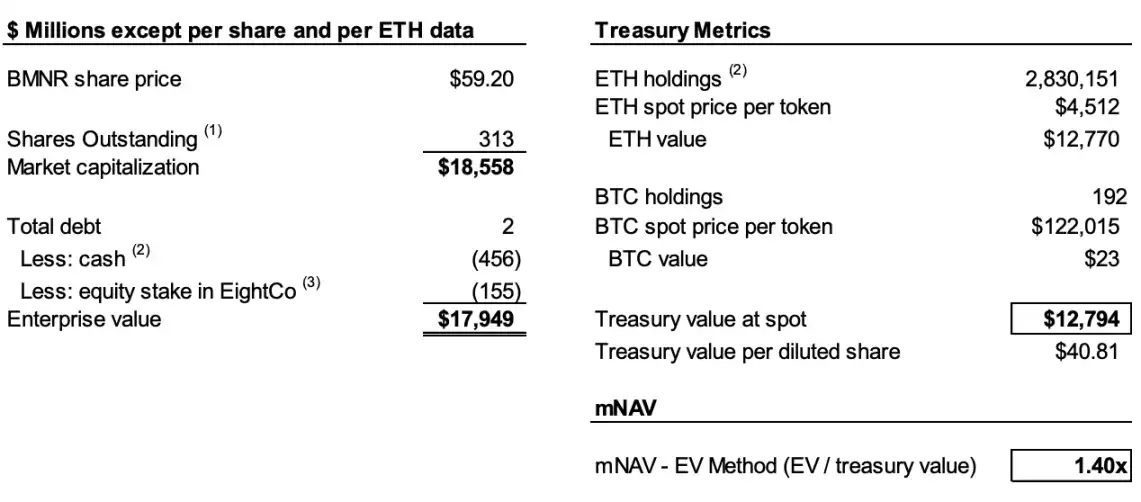

2. Continuous decline in mNAV: The premium of BMNR's market capitalization to its net crypto asset value (mNAV) has dropped from 2.0 times in August to 1.4 times, with the trend continuing to worsen;

3. Financial maneuvers to obscure cash-out facts: The recent 365 million USD "premium" financing is actually at a deep discount, and the accompanying warrants significantly dilute the value of common stock;

4. Lack of transparency in disclosures: The company stopped disclosing the NAV per share and total share capital since August 25, making it impossible for investors to assess whether the Ethereum "content" per share has increased;

5. Intensifying competition: There are already 154 companies in the U.S. planning to raise nearly 100 billion USD for crypto treasury strategies, and the launch of ETFs will further weaken the scarcity of DAT;

6. Failure of the Strategy model: The mNAV premium of Strategy, the ancestor of DAT (formerly known as MicroStrategy), has dropped from 2.5 times to 1.4 times, indicating a loss of market confidence in this model.

To understand the logic behind the shorting, we first need to explain the core logic of how DAT companies operate. As Kerrisdale stated in the report, the core logic is: issue shares at a price above the book value of tokens → raise funds → buy more coins → increase the amount of coins per share → maintain the premium → issue more shares, forming a self-reinforcing cycle.

For example, if Company A has Bitcoin worth 1 billion USD on its books and a total share capital of 100 million shares, it would issue new shares at a price above 10 USD per share to raise funds, because investors expect that the company's continued purchase of Bitcoin after fundraising will increase the "content" of Bitcoin per share, thereby raising the stock price, making them willing to buy new shares at a premium. Thus, after completing the fundraising, Company A continues to buy Bitcoin, increasing the amount of Bitcoin per share and simultaneously raising the stock price. Company A can continue this type of operation to keep raising the stock price.

However, two necessary conditions must be met to maintain this cycle: first, there must be a premium or at least an expectation of a future premium in the initial stage of mNAV; second, the premium and premium rate must be sustained. If the premium rate is 0 or even negative, investors might as well buy the corresponding crypto assets directly.

Thus, we can combine points 1, 2, and 4 to explain the reasons for the bearish outlook. According to the report, Kerrisdale estimates that as of October 6, BitMine has issued a total of over 240 million shares, bringing the total share capital to 311.7 million shares. Although from July to August, BitMine increased its content from 2.7 ETH per thousand shares to 7 ETH per thousand shares through the flywheel, Kerrisdale estimates that from August 25 to October 6, the company's Ethereum holdings increased by 65%, but the Ethereum content per share only increased by 17%.

In other words, Kerrisdale believes that the dilution means that the growth rate of content will continue to lag behind the growth rate of Ethereum holdings, and coupled with the mNAV already dropping from 2 times in August to 1.4 times, the decline in content growth and the decline in premium may lead to a vicious cycle, causing both numbers to continue to decline under mutual influence, ultimately resulting in parity or even a discount.

If the data still contains speculative elements, then BitMine's cessation of disclosing NAV per share and total share capital since August 25 has solidified Kerrisdale's judgment, as it stated on X: "If earnings per share were improving, they should be promoting it vigorously."

"Premium Financing" is Actually "Discount Cash-Out"

On September 22, BitMine announced that it had signed a securities purchase agreement with an institutional investor to directly issue 5,217,715 shares of common stock at a price of 70 USD per share, along with warrants to purchase up to 10,435,430 shares of common stock (exercise price of 87.50 USD per share). After deducting placement agent fees and other estimated issuance costs, the company expects total proceeds from this issuance to be approximately 365.24 million USD.

This news, which typically would drive the stock price up, was viewed by Kerrisdale as BitMine's attempt to cash out at a discount through financial maneuvers.

The report states that the issuance price of 70 USD has a premium of about 14% over the closing price of 61.29 USD on that day, but each share comes with 2 warrants (exercise price of 87.5 USD, valid for 1.5 years). According to the Black-Scholes model (vol 100%, rate 4%) and accounting for a 40% liquidity discount, each warrant is valued at about 14 USD.

Black-Scholes is a mathematical model proposed by Fischer Black and Myron Scholes in 1973, for which they won the Nobel Prize in Economics. It addresses the question of "how much should an option that can only be exercised at expiration be worth today under given conditions." The calculation formula involves several set parameters, with Kerrisdale setting volatility (vol) at 100% (indicating high volatility for such stocks) and the risk-free rate at 4%, calculating that each warrant in BitMine's issuance on September 22 is worth about 14 USD.

Therefore, if we exclude the two warrants currently valued at 14 USD each, BitMine's actual financing amount is only 220 million USD, equivalent to an actual issuance price of only 42 USD per share, representing a discount of about 31% compared to the closing price on that day. Kerrisdale believes that while this transaction may not result in a loss for investors, if a DAT company needs to raise funds at an actual discount, it has already invalidated one of the necessary conditions for the flywheel to operate, further indicating that BitMine's model is showing signs of fatigue.

DAT is No Longer Scarce

The report states that when MicroStrategy launched its Bitcoin treasury strategy in 2020, the market lacked compliant and convenient investment tools for crypto assets, making DAT a "leveraged substitute." However, to date, over 150 companies in the U.S. have announced similar strategies, planning to raise a total of nearly 100 billion USD. At the same time, the SEC has simplified the ETF approval process, and a "tsunami of ETFs" is expected, with lower-cost, higher-liquidity Ethereum investment channels likely to quickly capture the market.

Kerrisdale states that even the mNAV premium of the oldest Strategy has dropped from a peak of 2.5 times this year to 1.4 times, indicating that market confidence in the DAT model has weakened. Even Strategy itself suddenly canceled its commitment to issue new shares only at a 2.5 times premium in August, and once this trust and discipline collapse, it is difficult to repair. Therefore, if the market lacks confidence in Strategy, even in Strategy itself, then imitators are bound to collapse first.

Kerrisdale has already provided the best summary at the beginning of the report: "We are not shorting Ethereum, but rather shorting the notion that 'investors should still pay a premium for ETH.' If you want to hold ETH, just buy, stake, or buy an ETF. BMNR's selling point is that it is 'worth more than ETH itself,' but its strategy is mediocre, competition is fierce, disclosures are opaque, the growth rate of Ethereum per share is slowing, and the so-called 'premium financing' is actually dilution (plus there is no scarcity). Against this backdrop, BMNR's premium is destined to continue to decline."

"Kerrisdale, which 'loves' shorting, and the controversial DAT"

Kerrisdale Capital is one of Wall Street's most active "long-short hedge + event-driven" funds, known for its aggressive public shorting. In recent years, it has focused its firepower on areas such as "valuation detachment from reality" in cryptocurrency concepts, quantum technology, and SPACs. At the end of 2023 and the beginning of 2024, Kerrisdale targeted Marathon Digital and Cipher Mining, both causing single-day declines of 5% to 8%. In addition to cryptocurrency-related stocks, Kerrisdale shorted quantum computing concept stocks IonQ and D-Wave Quantum in the first half of the year, but both only saw slight declines on the day the short reports were released, subsequently experiencing significant increases.

Sahm Adrangi, the founder and Chief Investment Officer of Kerrisdale Capital, initially worked at Deutsche Bank in high-yield bonds and leveraged loan debt financing and served as a bankruptcy and out-of-court restructuring advisor for creditor committees at Chanin Capital Partners. Later, Adrangi worked as an analyst at Longacre Management, a distressed debt hedge fund with an asset management scale of 2 billion USD.

Sahm Adrangi is known for shorting and exposing fraudulent Chinese companies in 2010 and 2011, including China Marine Food Group, China-Biotics, and Lihua International. His then-short target, China Education Alliance, and ChinaCast Education Corp were later investigated and penalized by the SEC.

Kerrisdale is not a fund that only shorts without going long, but recently its main focus has been on companies with inflated valuations, with DAT being the latest target. As mentioned at the beginning, this confident naked shorting operation must have identified fundamental logical flaws. Kerrisdale's shorting performance this year has not been outstanding; most of the companies it shorted turned to rise after a brief decline, but we cannot overlook its unique insights into the DAT company model.

This year, although many U.S. publicly listed companies have begun experimenting with the DAT company model for Bitcoin, Ethereum, and even other altcoins, and there are no shortage of well-known investors rallying behind it, industry figures in Web3, including Vitalik, have expressed some concerns. In hindsight, these concerns are not without reason. In a hot market with ample liquidity, DAT company stock prices can indeed soar, but this bubble-like accumulation of growth is bound to be unsustainable in the long run.

We do not deny that when the overall market is favorable, DAT companies can add fuel to the fire, but when the bubble bursts, whose eyes will be blinded by the ashes of these already carbonized logs?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。