Original Title: A simple Lighter valuation framework (Bear/Base/Bull)

Original Author: @chuk_xyz

Compiled by: Peggy, BlockBeats

Editor's Note: As Lighter approaches its TGE, the market's divergence on its valuation stems not from sentiment, but from differing understandings of its product positioning and growth path. Is it merely another perpetual contract exchange, or a trading infrastructure with the potential to support greater distribution and asset forms? The answer determines the valuation ceiling.

This article attempts to break free from the lazy framework of "simple benchmarking" and return to more verifiable facts: the real TVL and trading volume scale, proven revenue capabilities, first-mover advantages in the RWA track, and a product expansion roadmap pointing to 2026. Based on this, the author provides a valuation range that does not rely on sentiment, using "zones" rather than "target prices" to address uncertainty.

The following is the original text:

As Lighter's TGE approaches, there is a clear divergence in the market regarding "how much is it really worth."

On one hand, some simply categorize it as "just another perpetual contract exchange," believing it will struggle to compete with Hyperliquid; on the other hand, there are already some real market signals indicating that its scale and potential impact may far exceed that of a typical Perp DEX launch.

TL;DR: The current market pricing for Lighter is still primarily concentrated in the low single-digit billion FDV range; however, if the fundamentals continue to materialize and key catalysts are realized, its reasonable repricing range may be closer to $6 billion–$12.5 billion, or even higher.

Disclosure: I am an early user of Lighter (644.3 points) and will likely receive an airdrop. This article represents my personal research and views and does not constitute any investment advice.

My Lighter Points

In my view, the current situation is roughly as follows: based on trading on Polymarket, the market implicitly values Lighter at around $2 billion–$3 billion (at least according to the current trading price signals).

In the OTC market, Lighter's points are trading at around $90; if calculated based on approximately 11.7 million points, the corresponding airdrop value is about $1.05 billion.

If this portion of the airdrop accounts for about 25% of the total token supply, then back-calculating, Lighter's fully diluted valuation (FDV) is approximately $4.2 billion.

Lighter previously completed a $68 million financing round, corresponding to a valuation of about $1.5 billion, led by Founders Fund and Ribbit (according to Fortune reports).

Founders Fund has a long and distinguished record of betting on category-defining companies, having invested in iconic enterprises such as Facebook, SpaceX, Palantir, Stripe, and Airbnb.

Additionally, $LIT is priced in the pre-market at approximately $3.5 billion FDV, which can be seen as a real-time market reference signal (although still in the early stages and not entirely precise).

Therefore, my judgment framework is actually quite simple: $1.5 billion can be seen as the valuation lower limit (bearish range, anchored by VC financing rounds). $3 billion–$4.2 billion belongs to the bearish to baseline range (predicted market, pre-market prices, and point-back valuation are roughly concentrated here).

The real core question is: based on fundamentals and catalysts, does Lighter deserve to be revalued to the range of $6 billion–$12.5 billion or even higher?

The purpose of this analysis is to try to clarify these questions logically: what exactly is Lighter as a product, what signals are released from the data perspective, which valuation frameworks are reasonable, and what catalysts might drive it further upward in revaluation.

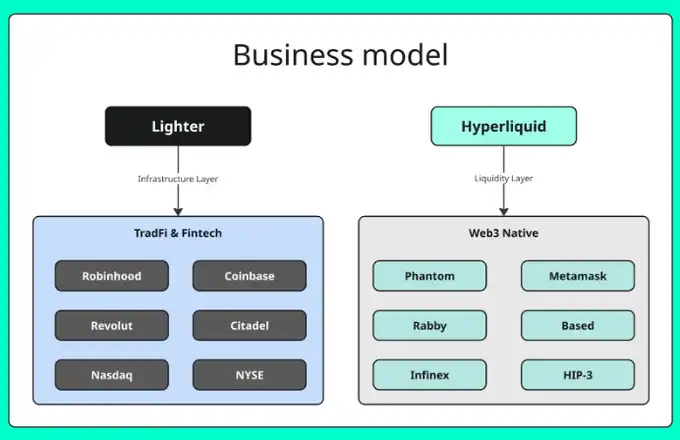

1. A Key Misunderstanding: Lighter and Hyperliquid Are Not the Same Type of Product

The clearest mental model I have found so far is:

Hyperliquid is building a Web3-native liquidity layer, with its main monetization coming from retail trading fees (and compounded by ecosystem-level network effects).

Lighter, on the other hand, is building a decentralized trading infrastructure, with the long-term goal of connecting fintech companies, brokerages, and professional market makers, while keeping execution costs extremely low on the retail side (some spot markets even achieve 0% fees).

From this perspective, the problems they solve, the customer groups they serve, and their long-term business paths are fundamentally different.

Source of Lighter vs Hyperliquid's Business Models: @eugene_bulltime

This distinction is important because it directly determines where the valuation ceiling lies.

If Lighter is merely "another perpetual contract exchange," then it being priced like other Perp DEXs is logically unsurprising; but if it is essentially a trading infrastructure that can be accessed by large distribution channels (brokerages/fintech companies), then the valuation ceiling it faces is governed by an entirely different set of rules.

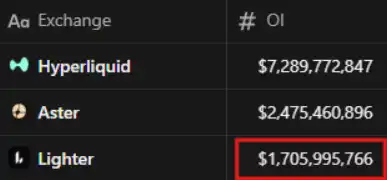

2. Where is Lighter Now (Truly Important Data)

First, let's look at the currently most critical set of metrics:

TVL: $1.44 billion

LLP TVL: $698 million (Lighter's liquidity pool for trade execution and system stability)

Open Interest: $1.7 billion

Trading Volume: 24 hours: $5.41 billion / 7 days: $44.4 billion / 30 days: $248.3 billion

Revenue: Last 30 days: approximately $13.8 million / Last year: approximately $167.9 million

The "quality" conveyed by these numbers is itself very important: this is already a real scale. A monthly trading volume of $248 billion is certainly not from a "hobbyist" exchange.

The open interest (OI) is substantial, but not so high that "an extreme liquidation could trigger systemic chaos."

The TVL is sufficiently high, allowing Lighter to reasonably position itself as a trading venue capable of handling large transactions and possessing stability—reliability is one of the core factors most valued by institutions.

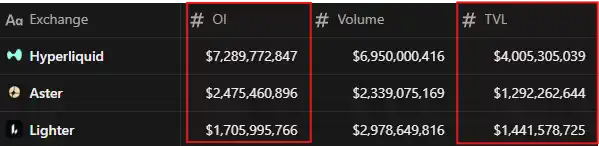

Risk Rationality Check: OI / TVL (Open Interest / Total Locked Value)

A quick method to measure leverage levels and liquidity matching is to calculate OI/TVL (open interest divided by TVL). Based on the current snapshot data:

Lighter: $1.71B / $1.44B ≈ 1.18

Hyperliquid: $7.29B / $4.01B ≈ 1.82

Aster: $2.48B / $1.29B ≈ 1.92

Intuitively, Lighter's OI/TVL is significantly lower, indicating that under relatively controllable leverage levels, it has a more ample liquidity buffer. This structure does not pursue extreme efficiency but leans more towards robust execution and system resilience—consistent with its positioning as an "infrastructure-type trading system."

Key Conclusion: Lighter already has a considerable scale of open interest, but overall it has not been overstretched relative to its liquidity levels; compared to the closest leading similar products, its risk structure is more restrained and robust.

3. Spot Market: A Key Unlocking Factor for Further TVL Growth

Lighter recently launched spot trading, and the importance of this may have been significantly underestimated by the market.

While perpetual contracts can indeed generate massive trading volumes, it is often the spot market that can solidify "sticky capital"—especially when the trading platform has clear advantages in execution efficiency and cost.

At the same time, spot trading significantly broadens the potential user base: for new users, spot trading is a lower-barrier starting point; for market makers, spot trading provides more reasons to hold and allocate inventory on the platform long-term.

Currently, ETH is the only spot asset that has been launched. This is not a limitation but a starting point. The truly noteworthy signal is that the "track" for spot trading has already been established, and the product itself has the structural foundation to smoothly expand as more assets are launched.

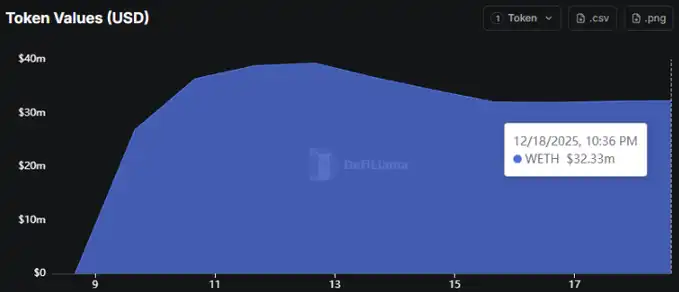

Lighter Spot Token Value Chart (WETH) (Source: DeFiLlama)

Even though only ETH is currently online, DeFiLlama data shows that Lighter's spot side has already accumulated approximately $32.33 million in WETH value (snapshot date: 2025/12/18).

This is still in the early stages, but the signal is clear: funds have begun to "dock" on the spot side.

If Lighter follows the publicly implied path and gradually introduces dozens (or even eventually hundreds) of spot assets, then spot trading will become a substantial driver of TVL growth, rather than just a "nice-to-have" feature module.

More importantly, the 0% trading fee for ETH spot itself is a powerful wedge. As long as execution quality remains stable (tight spreads, reliable transactions), it will naturally attract active traders and institutions to route high-frequency strategies and spot-perpetual basis trading to Lighter. The result is very direct: more trades → more inventory → deeper liquidity, creating a self-reinforcing positive feedback loop.

The conclusion is clear: the launch of spot trading is an important milestone. ETH is just the first step; the real upside potential comes from the expansion of the spot asset catalog, gradually positioning the platform as the default place for "trading + holding" on-chain.

4. RWA: The Unlocking Point for 2026 (and Why Lighter is Already Ahead)

One of the clearest signals that Lighter is not "just another Perp DEX" comes from RWA (Real World Assets).

RWA (tokenized stocks, forex, commodities, indices, etc.) essentially serves as a bridge between crypto trading and traditional markets. If by 2026, tokenized assets continue to migrate on-chain, then the trading platform that wins RWA first will gain not just more trading volume, but a new growth curve that most Perp DEXs are not prepared for.

The key is not the narrative, but the scoreboard. And from the data perspective, Lighter is already ahead.

RWA Leadership: The Data Speaks

Lighter is already leading in both open interest (OI) and trading volume for on-chain RWA perpetual contracts. This combination is crucial:

OI reflects the scale of exposure that traders hold long-term;

Trading volume reflects the intensity and activity of daily use.

When a trading venue leads in both metrics, it usually means that traders are not "testing the waters," but have already adopted it as their primary battleground for that product line.

This is why RWA represents a structural opportunity for Lighter: it is not chasing trends but positioning itself early in a market that is about to expand.

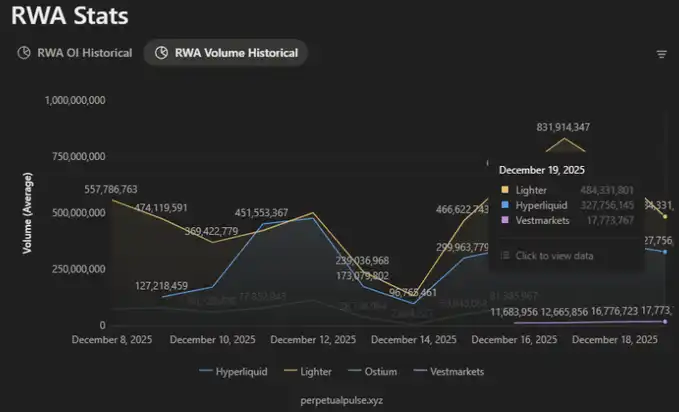

RWA Open Interest: Lighter Leads the Field (Source: PerpetualPulse.xyz)

In the current snapshot, the open interest for RWA perpetual contracts is approximately:

Lighter: about $273 million

Hyperliquid: about $249 million

The importance of this gap lies in the fact that RWA is still in its early stages. In early markets, liquidity often exhibits highly concentrated characteristics:

When a trading venue first gathers scaled liquidity, spreads will tighten, transaction quality will improve, and a better execution experience will, in turn, attract more funds and trading volume, creating a self-reinforcing positive feedback loop.

From this perspective, Lighter's lead in RWA OI is not just a static ranking but more like the starting point of a potential compounding effect.

RWA Trading Volume: Lighter Also Leads in Activity (Source: PerpetualPulse.xyz)

From the trading volume perspective, this trend is even clearer:

Lighter: about $484 million

Hyperliquid: about $327 million

This is a typical manifestation of early product-market fit (PMF): a new category begins to take shape, and a particular trading venue first attracts a disproportionate amount of trading activity. When usage frequency and execution experience continue to accumulate on the same platform, the leading advantage is often further amplified.

The Market Size is Underestimated

It is worth taking a broader view: tokenized RWA is not a niche market. On public chains, it has already reached a multi-billion dollar scale, and the growth curve is still upward.

This means that the platform that first establishes liquidity, execution quality, and user habits is not just winning current trading volume but is also locking in a long-term growth channel that is still expanding.

"Global Market Overview" Dashboard (Source: rwa.xyz)

The scale of tokenized RWA on public chains has reached over $18.9 billion and is still in its early stages.

This is important because RWA is one of the few narratives that does not need to "compete for attention" within the crypto circle: it can expand outward, bringing real-world assets and real-world trading behaviors on-chain, directly creating increments rather than internal competition.

Why This is a Major Valuation Catalyst

RWA perpetual contracts have already validated real demand; but the bigger unlocking point lies in the next step: RWA spot.

Perpetual contracts excel at speculation;

Spot is key to expanding the user base.

If Lighter can become one of the first to provide credible RWA spot trading (tokenized stocks/forex/commodities) on-chain while achieving strong execution quality and institutional-level reliability, it will not just add a feature but will substantially expand the total addressable market (TAM).

This is also directly related to the narrative alignment with Robinhood: once tokenized stocks become a real product distribution channel, the value of the "backend exchange/infrastructure layer" will be significantly amplified—because in the trading domain, distribution capability is the hardest moat to build.

The Roadmap Supports This Direction

From the product roadmap perspective, Lighter is clearly pointing towards 2026: deeper RWA expansion and the supporting capabilities needed for scaling (mobile, portfolio margin, prediction markets, etc.).

This is not a one-time narrative but a continuously expanding product curve.

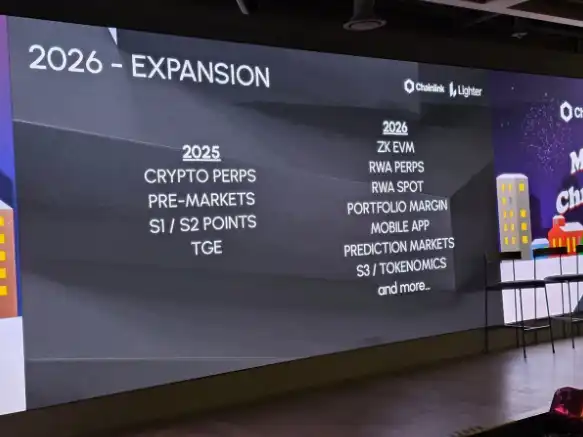

Chainlink × Lighter Seoul Offline Event "2026 – Expansion" Roadmap Slide

If RWA is one of the most important themes for 2026, then entering early and already leading in OI and trading volume is itself a very strong opening move.

The conclusion is clear: RWA is not a "side quest" for Lighter. On the contrary, it is the clearest path to achieving exceptional growth in 2026–2027—because this path expands Lighter from a purely crypto-native perpetual contract market to a broader world of tokenized financial products.

5. Robinhood Narrative Alignment: Why "Distribution" Will Change Everything

Robinhood is currently the cleanest and most imaginative distribution wedge on the table: approximately 26 million funded accounts, about $333 billion in assets under management (AUM).

A mature model: routing order flow to large market makers (a typical Citadel-style flow structure).

Once Robinhood becomes a real distribution channel for tokenized assets, the backend trading infrastructure that provides execution and settlement tracks will become extremely valuable—because in the trading domain, distribution capability is always the hardest moat to build.

If Lighter can become one of the backend tracks for tokenized assets/perpetual contracts/settlement flow (even if only partially involved), its impact will not be "a few more crypto users," but rather: bringing entirely new liquidity into the on-chain market through a familiar front-end UI.

The significance of this for valuation is that it directly attacks the biggest ceiling faced by most Perp DEXs: Web3-native liquidity is substantial, but compared to traditional finance's distribution capability, it still has limits.

And the market often does not wait for everything to settle. Even if this narrative only has "a certain probability of becoming mainstream," it is enough to trigger a repricing—because the crypto market prices probabilities, not certainties themselves.

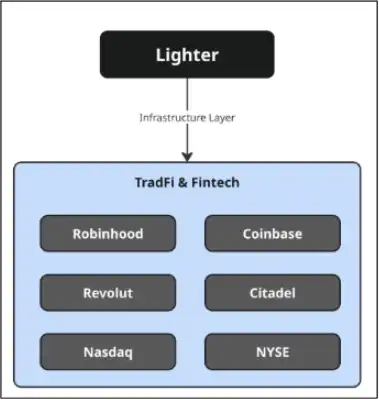

Lighter's "TradFi & Fintech" Infrastructure Positioning (Source: X @Eugene_Bulltime)

6. Valuation: A Simplified Framework Not Based on "Belief"

I prefer to use anchors + reality checks for valuation.

Valuation Anchors (Information Already Provided by the Market)

$1.5 billion FDV: lower limit / bearish anchor (from the VC pricing of the $68 million financing round). Falling below this level means that the financing round has been in a loss position from the start.

Approximately $4.2 billion FDV: market implied anchor (OTC point pricing + back-calculation of the community's approximately 25% allocation).

Reality Check #1: FDV / TVL Comparison

If we price Lighter at ~5× TVL: $1.44B TVL × 5 ≈ $7.2 billion FDV

This is not a shot in the dark but aligns with the aggregation ranges of similar platforms:

Hyperliquid: ~5.8× FDV/TVL

Aster: ~4.2× FDV/TVL

Therefore, as long as TVL can be maintained, and Lighter continues to prove its leading position in trading volume and OI, a $7–$8 billion FDV is a reasonable "fair value" range.

Reality Check #2: Income Comparison (Imperfect but Important)

Income is not the only valuation method in crypto (narrative is also important), but it is one of the hardest reality anchors that can test whether "usage has really turned into cash flow."

Estimated annual income (1y):

Hyperliquid: ~$900 million

Aster: ~$513 million

Lighter: ~$167.9 million

dYdX: ~ $10.9 million

Two conclusions can coexist: the income gap is real. Lighter's current income is lower than that of Hyperliquid and Aster, which is a reasonable justification for the market's discount on it today. If someone prices Lighter directly as "the next Hyperliquid," income is the most direct rebuttal point.

As a platform that has not yet issued tokens and whose products are not fully rolled out, this income is still quite solid. An annualized income of ~ $167.9 million is not "common." It does not automatically prove that a higher FDV is immediately reasonable, but it clearly indicates that Lighter is not running on hype; it is operating a real, monetizable business.

How Valuation Ranges Are Positioned

Bear/Benchmark ($1.5–7.5 billion FDV):

As long as TVL stabilizes and continues to prove its leading position in trading volume/OI, this range can hold even with the income gap.

Bull Market ($7.5–12.5 billion+ FDV):

Catalysts need to become consensus, specifically including:

(a) Faster income growth;

(b) Higher and sustainable activity; or

(c) The market's willingness to price in mainstream distribution narratives in advance.

In summary: income is a "proof point." It puts pressure on short-term multiples, but it is also a strong signal that Lighter already has real traction; the upside potential depends on whether income growth significantly increases after product expansion.

7. Scenario Assumptions (The Truly "Reasonable" FDV Range)

Bear Market Scenario: $1.5–4.2 billion FDV

Assumption: Weak market + TGE selling pressure + narrative absence. Prices hover around the VC lower limit or slightly above the implied value.

Benchmark Scenario: $4.2–7.5 billion FDV

Assumption: Pricing returns to fundamentals. TVL maintains above $1 billion, trading volume/OI remains at the top, priced according to comparable multiples.

Bull Market Scenario: $7.5–12.5 billion+ FDV

Assumption: Catalysts form consensus, including:

Sustained RWA momentum + clear RWA spot path; and/or

Robinhood-style distribution narrative widely accepted (even if not fully confirmed yet).

8. Roadmap Signals: Why 2026 May Be the Year of True Expansion

Considering the product rhythm and narrative path, 2026 looks like a key year for Lighter's amplification curve:

Deepening RWA, expanding spot trading, and improving supporting capabilities like mobile and portfolio margin—these are not isolated functions but point in the same direction of greater distribution and higher monetization efficiency.

Lighter 2026 Expansion Roadmap (Seoul Offline Event Slide)

Lighter has already shown impressive traction in 2025, but what will truly change the valuation ceiling is what happens next.

At the Chainlink × Lighter Seoul Meetup, a roadmap labeled "2026 – Expansion" was leaked, including:

ZK EVM, RWA Perps, RWA Spot, Portfolio Margin, Mobile App, Prediction Markets, S3 / Tokenomics… and more.

Even if viewed as "informal information before official confirmation," when you connect it with Lighter's currently validated capabilities—stable execution, rapid delivery, and clear momentum in RWA—this directional line is highly coherent.

Why This Roadmap is Important for Valuation

1) Expanding Product Scope (More Growth Paths for TVL and Trading Volume)

A DEX can grow large solely through perpetual contracts; however, adding spot trading, especially the path to RWA spot, will significantly widen the funnel.

Spot trading is stickier, better for TVL accumulation, and will attract a type of user not focused on 50× leverage.

2) Enhancing Capital Efficiency (Portfolio Margin is Key)

Portfolio margin may not sound sexy, but it is what institutions and professional traders truly care about.

It allows funds to work collaboratively across different positions, reducing fragmentation, thereby increasing activity without proportionally increasing new deposits.

3) Upgrading Distribution (Mobile)

Most retail trading occurs on mobile devices.

If Lighter wants to be a viable alternative to the "one-click trading" experience of Binance or Robinhood, a native mobile platform is not just a bonus; it is a direct growth lever.

4) Doubling Down on the Strongest Narrative (RWA)

RWA is not just a new market; it is the clearest bridge to non-crypto-native demand.

The roadmap clearly states RWA Perps + RWA Spot, signaling that this is a core strategy, not a peripheral function.

5) Increasing Optionality (Prediction Markets + "More")

Prediction markets have repeatedly validated demand in crypto.

If integrated into a larger trading stack, it could form a new product line with high engagement, enhancing retention and keeping users within the same ecosystem.

9. Risks That Need Serious Attention

Market Environment: The current total market cap of crypto is about $2.96 trillion, significantly lower than the $4.27 trillion ATH in October 2025. If macro conditions continue to weaken, all assets will be under pressure.

Post-TGE Behavior: Short-term selling pressure is almost certain; the key observation point is whether TVL/trading volume stabilizes after initial volatility.

Real Competition Exists: Hyperliquid has strong product capabilities, and other platforms will quickly replicate features.

Narrative vs Confirmation: Narratives like Robinhood/RWA spot may experience overheating pullbacks if the timeline is extended.

Closing Thoughts

A lazy valuation method is: "It's a Perp DEX → benchmark against Hyperliquid → apply a discount → done."

A better approach is to acknowledge these differences:

The scale is already real (TVL, trading volume, income).

RWA appears to be a structural wedge, not a side task.

The product direction points to a broader market (Perps → Spot → Margin → New Verticals).

Once fintech/brokerage distribution is even partially realized, the ceiling is no longer "another crypto exchange."

Therefore, my framework is: $1.5 billion is the bottom, ~$4.2 billion is the cleanest market anchor derived from implied pricing; as long as TVL stabilizes and catalysts continue to materialize, discussions of fair value should start from ~$7 billion and above.

How I’m Thinking About the Zones (Not Investment Advice, Just Personal Planning)

$LIT Valuation Scenario Analysis

To maintain my discipline, I treat these FDV ranges as "zones" rather than precise target prices.

Bear Market Zone ($1.5–4.2 billion FDV)

If the price oscillates within this range after TGE, I will view it as an "opportunity zone."

Holding the airdrop here minimizes my psychological pressure; for those who truly agree with this logic, this is also the cleanest area for risk-reward—because the traction of TVL, trading volume, and RWA is already visible and verifiable.

Benchmark Zone ($4.2–7.5 billion FDV)

If Lighter can stabilize TVL and continue to operate at a leading scale, I will view this range as fair value.

If the price reaches here, I would personally consider taking some profits ("recouping costs first") while still maintaining exposure. The reason is simple: the 2026 roadmap is the kind of configuration that can gradually raise the valuation ceiling—including RWA, spot expansion, portfolio margin, mobile, etc.

Bull Market Zone ($7.5–12.5 billion+ FDV)

This is a zone where "catalysts have become consensus."

If Lighter trades here, it often means that RWA momentum is undeniable, and/or the distribution narrative (fintech/brokerage alignment) is starting to be taken seriously by the market.

In this case, I would be more proactive in managing risk during the upswing, as this is a position where the crypto market can easily overshoot and quickly reverse.

In summary: I am not trying to catch the top. I just want a plan that allows me to navigate volatility, take profits without regret, and still maintain exposure when Lighter successfully executes through to 2026.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。