Author: Ba Jiuling, Wu Xiaobo Channel

As the exchange rate of the Renminbi runs wildly on the path of appreciation, the central bank has finally intervened personally to stabilize the exchange rate.

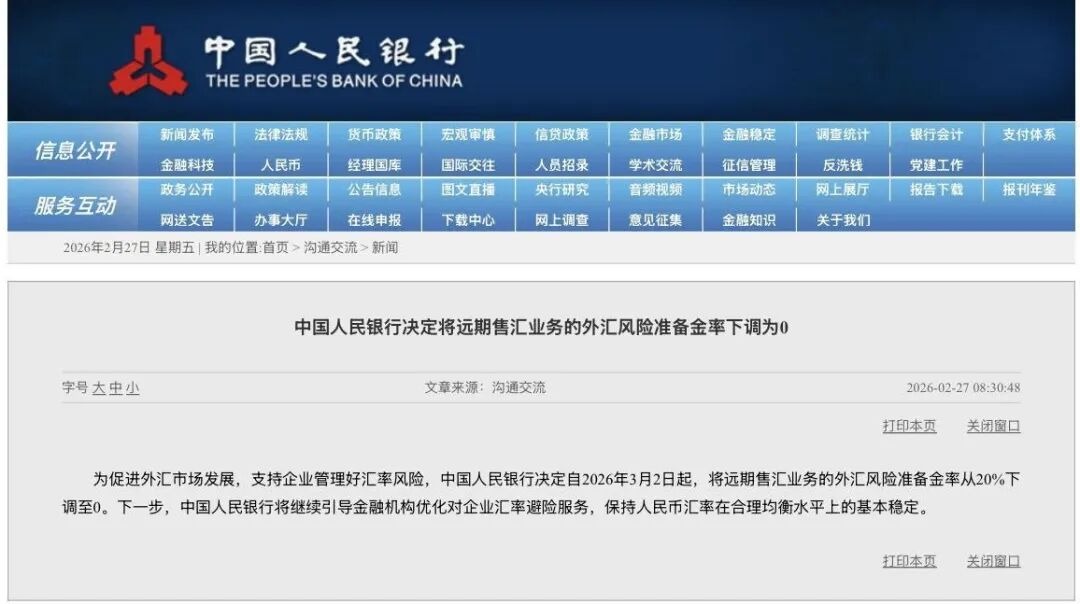

At 8 AM on February 27, 2026, the People's Bank of China announced: To promote the development of the foreign exchange market and support enterprises in managing exchange rate risks, it has decided to lower the foreign exchange risk reserve ratio for forward foreign exchange sales from 20% to 0, effective from March 2, 2026.

The announcement was brief, but the effect was immediate. The offshore Renminbi exchange rate, which was trading at 1 USD to 6.839 CNY, depreciated rapidly by 0.3%, reaching a peak of 6.859, pressing the pause button on the continuously appreciating Renminbi.

So, what exactly is the foreign exchange risk reserve for forward foreign exchange sales? How will this policy impact the exchange rate, investors' wallets, and import/export enterprises?

Soaring Renminbi Exchange Rate

To understand this policy, we must first discuss why the central bank took action.

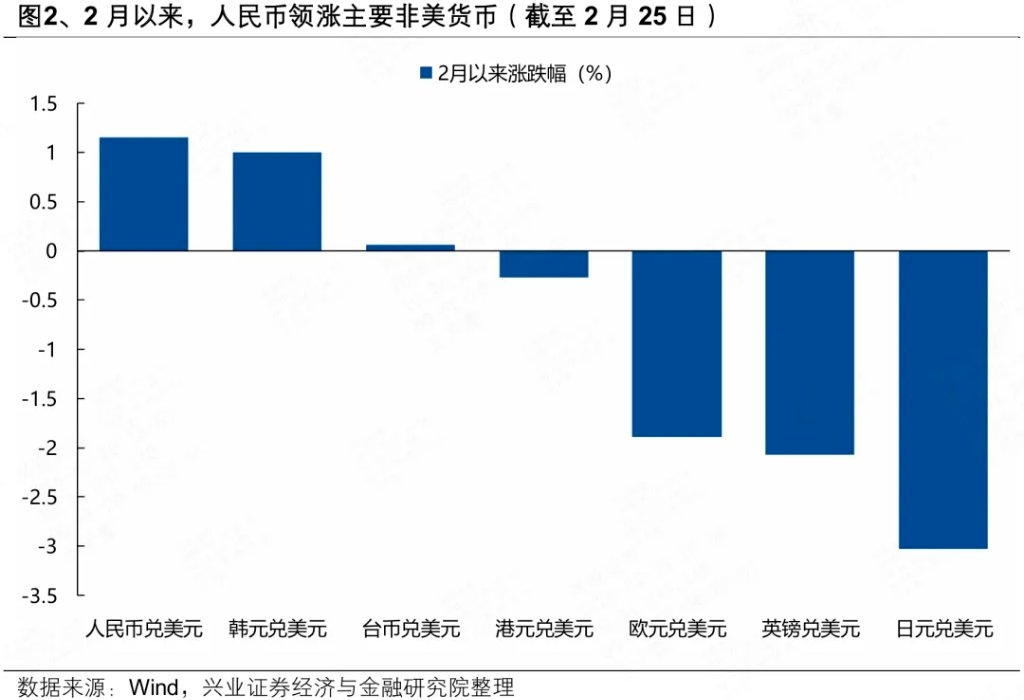

Since the Renminbi exchange rate "broke 7" in December last year, the exchange rate against the US dollar has entered an "acceleration mode." It appreciated by over 800 points in just three trading days after the Spring Festival holiday, especially on February 26, 2026, where the annual increase momentarily exceeded 2% during trading.

The reason for the appreciation of the Renminbi is not complicated.

First, the external factors: the continuous weakening of the US dollar is the core driver.

With the Federal Reserve starting a rate-cutting cycle, the market generally expects the US dollar to continue to depreciate, combined with other factors, leading to a continuous weakening of the US dollar index, dropping from 100 last year to 95.5 in January this year.

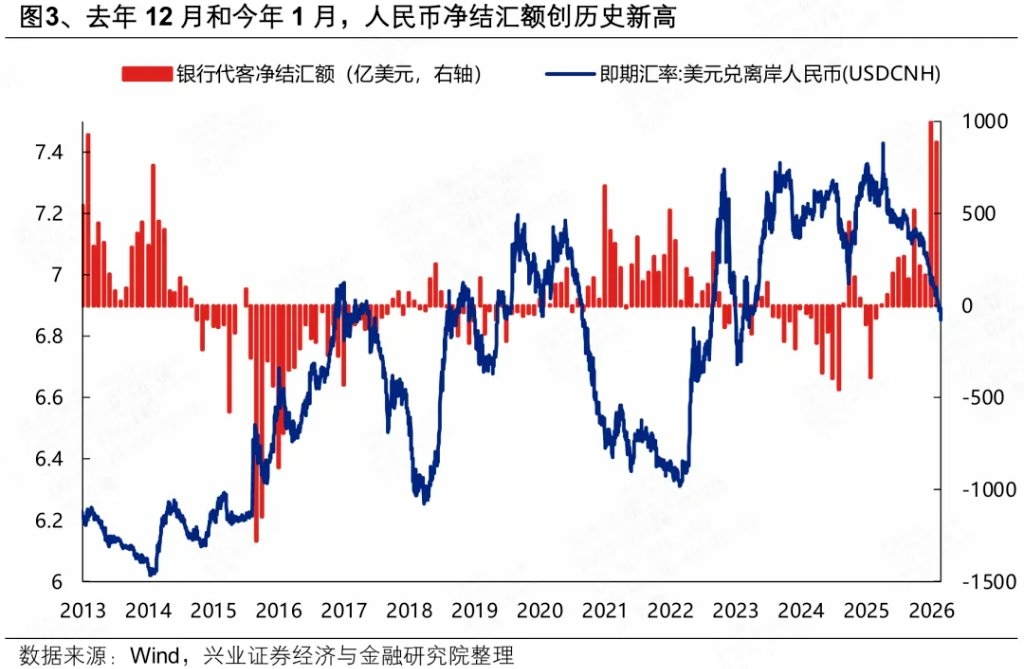

Second, there are internal factors. The resilience of the Chinese economy lays the foundation for the strengthening of the Renminbi. The upgrade of export structures, enhanced manufacturing competitiveness, and a high surplus in the current account provide solid fundamental support for the Renminbi. Data shows that in 2025, China had a trade surplus of 1.19 trillion USD, which means that a large number of export enterprises hold a substantial amount of US dollars.

When these enterprises began to "settle"—selling US dollars to buy Renminbi ahead of the Spring Festival—this further propelled the Renminbi's appreciation.

With the confluence of internal and external factors, this creates what is known as the "pro-cyclical effect": the depreciation of the dollar triggers more settlements, which in turn pushes for further appreciation, forming a positive feedback loop.

Wang Qing, chief macro analyst at Dongfang Jincheng, believes that with the offshore Renminbi leading the charge, market sentiment during this period has been high, further boosting the Renminbi's increase.

However, the central bank's target for exchange rate control is: to maintain basic stability for the Renminbi exchange rate at a reasonable and balanced level based on market supply and demand, reinforced by guiding expectations to prevent risks of excessive fluctuations.

If the Renminbi exchange rate experiences a sharp rise or fall that deviates from its fundamentals, regulatory authorities will decisively intervene with tools to stabilize the foreign exchange market, releasing clear policy signals to prevent the Renminbi from appreciating too quickly.

For some, a stronger Renminbi is a good thing, but for export enterprises, the situation is quite the opposite.

In 2025, the contribution of China's net exports to economic growth reached 32.7%. If the Renminbi appreciates too quickly and by too much, the impacts on export enterprises will gradually become apparent.

According to media reports, after conducting research on several export-oriented listed companies, it was found that the appreciation of the Renminbi has already had a significant impact on their operations.

For example, in the case of a certain publicly listed company in the smart mobility sector, the foreign exchange impact amount in the fourth quarter of 2025 was 130 million yuan. Although the company has used hedging tools for risk management, achieving a hedging gain of 53 million yuan, it still faced a loss of 70 to 80 million yuan in net profit.

Guan Tao, chief global economist at Bank of China Securities, said: If domestic enterprises receive exports in US dollars, they will suffer foreign exchange losses due to the appreciation of the Renminbi. The nominal bilateral exchange rate appreciation of the Renminbi evolving into an appreciation in the real effective exchange rate will affect the export competitiveness of enterprises.

Against this backdrop, the central bank has taken out its toolbox and introduced the "foreign exchange risk reserve for forward foreign exchange sales."

The Central Bank Took Out Its Toolbox

To understand this tool, we need to clarify four key concepts: settlement, sale of foreign exchange, forward foreign exchange sales, and foreign exchange risk reserve.

Settlement refers to enterprises and individuals selling their foreign exchange to banks in exchange for Renminbi, while sale of foreign exchange refers to enterprises and individuals using Renminbi to buy foreign exchange from banks.

The so-called forward foreign exchange sales business is a currency hedging derivative product provided by banks to enterprises. Generally, to avoid fluctuations in exchange rates, exporting enterprises tend to lock in exchange rates in advance through forward foreign exchange sales and options. Enterprises do not immediately purchase foreign exchange, and banks conducting this business need to buy foreign exchange in the spot market, which will affect the spot exchange rate.

As for the foreign exchange risk reserve, it dates back to the "August 11 exchange rate reform" of 2015.

To address the significant fluctuations in the Renminbi exchange rate at that time, the central bank introduced a series of innovative policy tools, one of which was the "foreign exchange risk reserve." It stipulates that for every foreign exchange transaction conducted by a bank, a certain percentage of margin must be submitted to the central bank.

Bank staff counting US dollars

So how does the central bank's tool manage to "cool down" the trend of the Renminbi? This involves a complex transmission chain.

First, according to the central bank's foreign exchange risk reserve regulations, for every forward foreign exchange sale business conducted by a bank, a portion of the money must be "locked" at the central bank. Since these funds do not earn interest, this means the bank incurs higher costs when conducting forward foreign exchange sales.

Now, with the central bank lowering the foreign exchange risk reserve ratio for forward foreign exchange sales, banks no longer need to freeze interest-free foreign exchange funds, significantly reducing the costs of the forward foreign exchange sales business.

As banks' business costs decrease, enterprises engaging in forward foreign exchange purchases will find that the cost of obtaining forward US dollars has become cheaper, which will increase the willingness of import enterprises in need to purchase foreign exchange in advance.

Thus, more and more enterprises and banks are signing forward foreign exchange sales contracts, and banks, in order to hedge risks, will immediately buy US dollars in the spot market, leading to an increase in the demand for US dollars in the market. Since the exchange rates of the US dollar and the Renminbi behave like a seesaw, when the demand for US dollars increases, it will cool down the appreciation of the Renminbi.

The central bank has used similar measures more than once.

For instance, on October 10, 2020, the central bank announced it would lower the foreign exchange risk reserve ratio for forward foreign exchange sales from 20% to 0%. At that time, the central bank's action aimed to slow down the appreciation of the Renminbi, and the current policy change is virtually a reenactment of six years ago.

Liu Tao, a senior researcher at Guangkai's chief research institute, believes that the reduction in the foreign exchange risk reserve ratio for forward foreign exchange sales signifies a shift from previously "curbing depreciation" emergency controls to regularized management, allowing market mechanisms to play a fuller role, guiding all parties to rationally view exchange rate fluctuations, reducing pro-cyclical "herd effects," and maintaining the basic stability of the Renminbi exchange rate at a reasonable and balanced level.

Wen Bin, chief economist at Minsheng Bank, stated that under the current conditions where there is no pressure for exchange rate depreciation, the counter-cyclical adjustment tool naturally retreats, allowing policies to return to neutrality and reducing direct intervention in the market.

What Are the Impacts After Policy Implementation?

The central bank's policy adjustment is a tangible benefit for enterprises.

Liu Tao stated: "Although the previous 20% foreign exchange risk reserve for forward foreign exchange sales was paid by banks, in actual business, some banks possibly transferred this implicit cost to enterprises through adjusting forward quotes or widening spreads."

For example, suppose a certain bank wants to conduct a forward foreign exchange sale business of 1 million USD. When the reserve ratio is 20%, it needs to set aside 200,000 USD as a foreign exchange risk reserve, which will be deposited at the People's Bank of China interest-free for one year.

In this case, this interest would be considered a cost, ultimately borne by the clients signing the forward contract with the bank, leading to a decrease in clients' willingness to participate in forward foreign exchange purchases. However, with the reserve ratio lowered to 0, enterprises with actual trade needs will be able to achieve purchases at a lower cost.

For some small and medium-sized enterprises, the costs of using forward foreign exchange sales to lock in exchange rates were previously not low, which also led those enterprises that could avoid exchange rate risks to forgo using this tool due to "cost issues."

Now, with the reserve ratio down to 0%, it is equivalent to the central bank encouraging more small and medium-sized enterprises to hedge exchange rate risks through forward foreign exchange sales, stabilizing production expectations and better serving the foreign exchange purchasing demands of the real economy. For import enterprises, which already have thin profit margins, this significantly enhances their profits.

It is also worth mentioning that in 2025, China's foreign exchange market trading volume reached 42.6 trillion USD, and the ratio of enterprises engaging in foreign exchange hedging increased to 30%, both of which are historical highs.

This data indicates that the awareness of foreign exchange risk management among Chinese enterprises is awakening, and hedging has become an increasingly standard practice for more enterprises. This policy adjustment is expected to further push this ratio higher.

State Administration of Foreign Exchange Building

How Should Investors Deal with Renminbi Fluctuations?

For investors focused on foreign exchange investments, fluctuations in the Renminbi will affect asset allocations, such as US dollar assets and Hong Kong dollar wealth management.

Based on various opinions from institutions and experts, they all believe that currency exchange should be based on personal needs, and unilateral betting is not advisable. In other words, individual investors need to manage exchange rate risks based on actual needs, rather than treating the exchange rate as a speculative tool.

Li Nan, an associate professor at Shanghai Jiao Tong University School of Finance, pointed out: Currently, the interest rate difference between US dollar deposits and Renminbi deposits is about 2%. As long as the US dollar depreciates by 2% against the Renminbi, this interest rate difference will cease to exist. If the US dollar depreciates more than 2%, it is better to directly deposit in Renminbi.

For investors who already hold US dollar assets, some experts suggest they can consider dividing their US dollars into several portions and gradually closing them at different exchange rate points to lower the risks of missing opportunities or chasing highs.

For individual investors with genuine currency needs for studying abroad, travel, overseas shopping, or overseas payments in the future, they can retain the corresponding amount of US dollars; for those without actual needs and holding it purely for interest rate spreads, they can moderately reduce their US dollar positions during periods of Renminbi strength.

Foreign currency exchange

Conclusion

Overall, the central bank's reduction of the foreign exchange risk reserve ratio for forward foreign exchange sales is essentially a "return to neutrality" policy. From 2015 to 2025, the central bank has made five adjustments to the foreign exchange risk reserve ratio.

From the substantial fluctuations after the "August 11 exchange rate reform" to the increasing resilience of the Renminbi exchange rate, with two-way fluctuations becoming the norm, the central bank has proven through repeated actions that it can guide the trend of the exchange rate and prevent exchange rate risks at critical moments.

In the context of a tumultuous external environment, both individual investors and enterprises need to learn to coexist with exchange rate fluctuations.

As emphasized repeatedly by the central bank: adhere to the neutral concept of exchange rate risk and manage exchange rate risks effectively. This is not just empty talk, but a required course for every market participant.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。