Introduction:

Currently, the exploration of RWA in the crypto market mainly focuses on asset tokenization—how to map ownership of real assets such as government bonds, stocks, or real estate onto the blockchain for more efficient settlement and holding. However, this solution, centered around efficient holding and settlement, cannot fully meet another side of the demand in the financial market, which is the leveraged trading and risk management of asset price fluctuations.

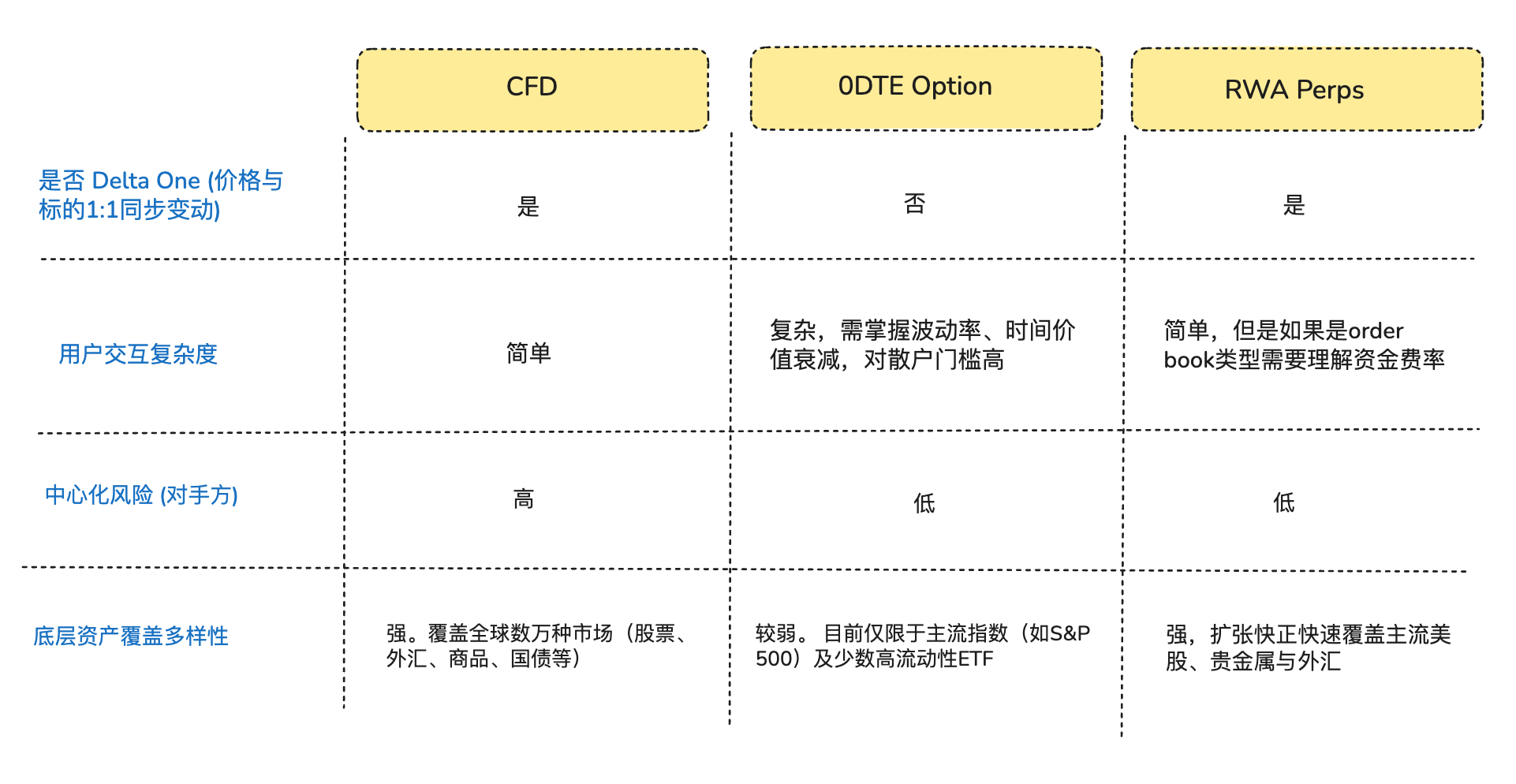

In fact, the true engine of liquidity in global financial markets is not static holders of assets, but traders seeking leveraged directional exposure. From the nominal value of the approximately $50 trillion monthly end-of-month options market in the United States, to the off-U.S. market with a monthly trading volume of about $30 trillion in the CFD (Contracts for Difference) market, the retail investors' demand for high leverage and short-term risk exposure has never paused. Despite the enormous trading scale, existing traditional financial instruments still seem inadequate to meet this demand: 0DTE Options (Zero Days to Expiration) force traders to bear both Theta (time decay) and Vega (volatility) non-linear risks while engaging in simple directional betting. The CFD market has also been criticized for its opaque black-box mechanism and centralized counterparty risks.

From the perspective of the demand of traders merely seeking directional exposure, many traders actually desire not "options" or "tokenized stocks", but a pure Delta One (linear/symmetrical return) exposure—meaning that the price volatility of the asset can be simply and directly converted into proportional investment gains and losses without any loss or deviation in between.(Arthur Hayes wrote an article last year"Adapt or Die" that reviews the full context of their development of crypto perpetual contracts, which may be of interest to read).

It is within this structural mismatch that DeFi protocols astutely capture this market opportunity. Some DeFi entrepreneurs attempt to introduce perpetual contracts—already validated and matured in the crypto market for nearly a decade—into traditional asset domains. These products adopt synthetic derivative architectures, anchoring the prices of underlying assets through oracle-fed pricing and funding rate mechanisms, providing around-the-clock leveraged trading services for stocks, commodities, and foreign exchange without the need to actually hold or settle the assets.

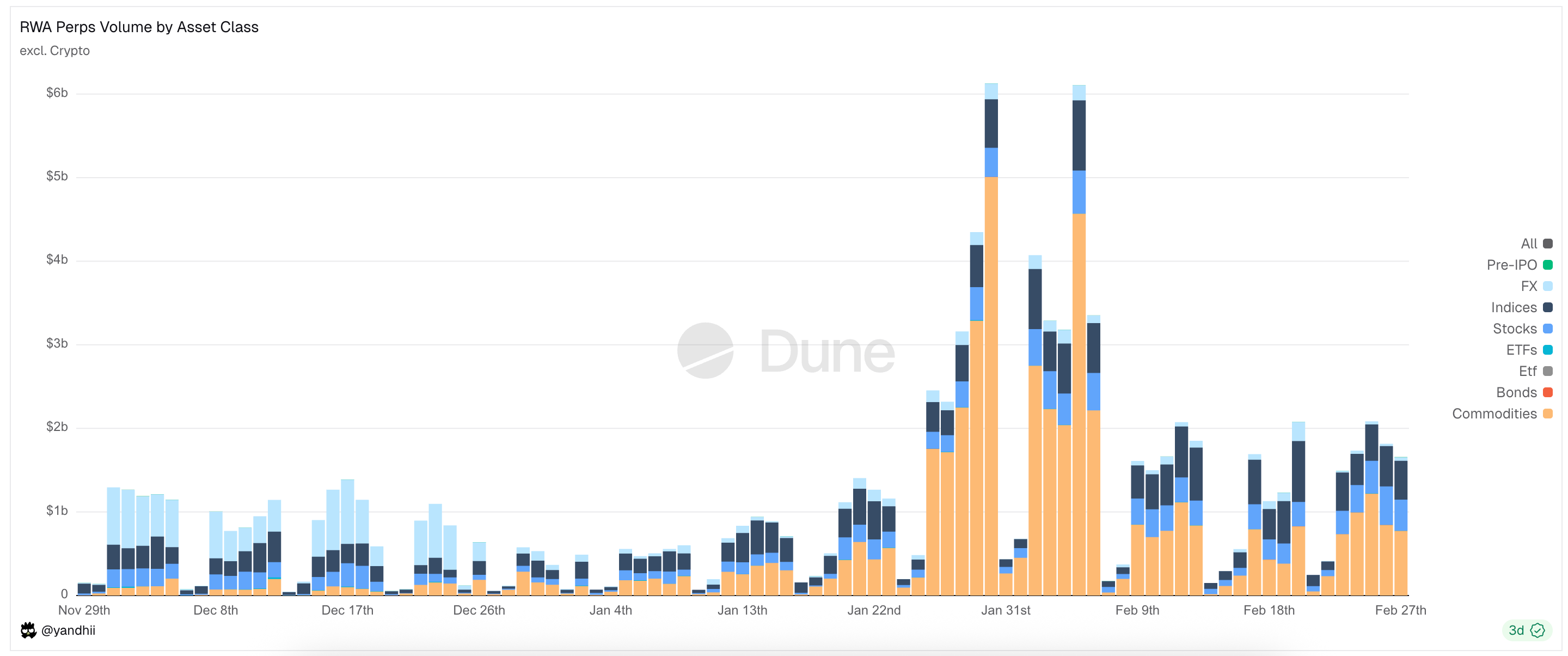

Figure: Current main trading asset types of RWA Perps Dex

1. Market Background (Opportunities to Enter the RWA Perps Market)

1.1 Market Entry 1: The 0DTE Option Market in the United States

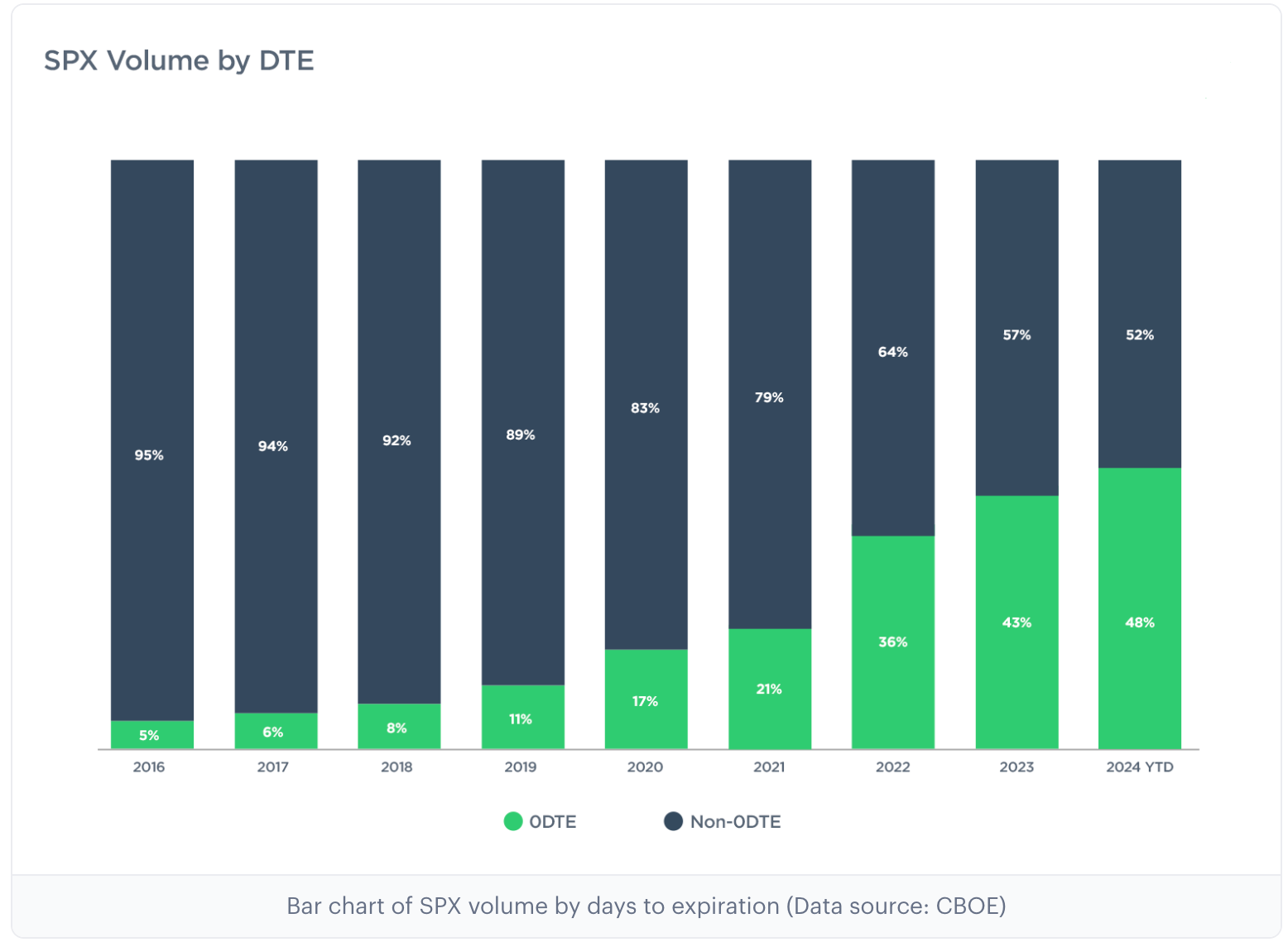

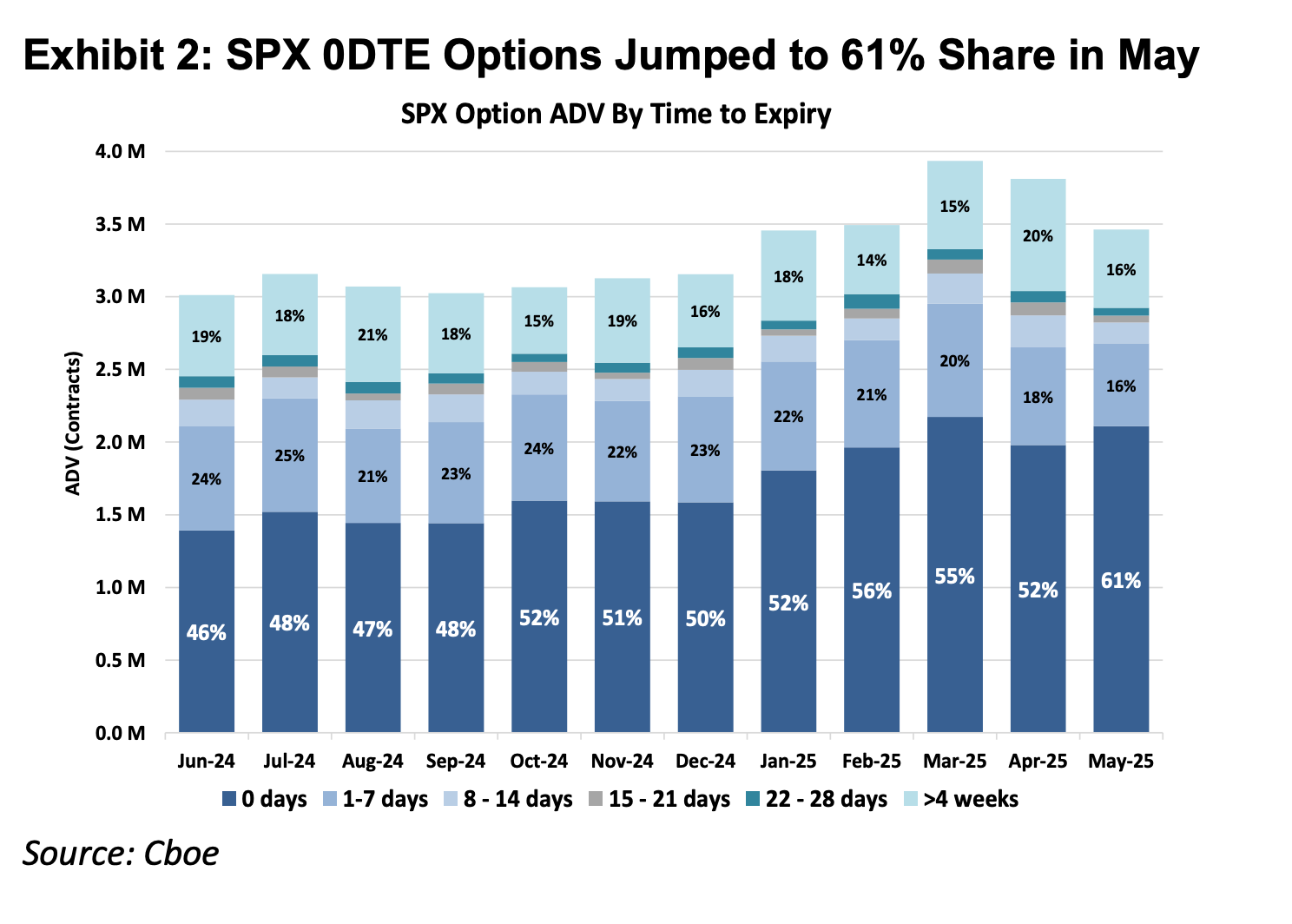

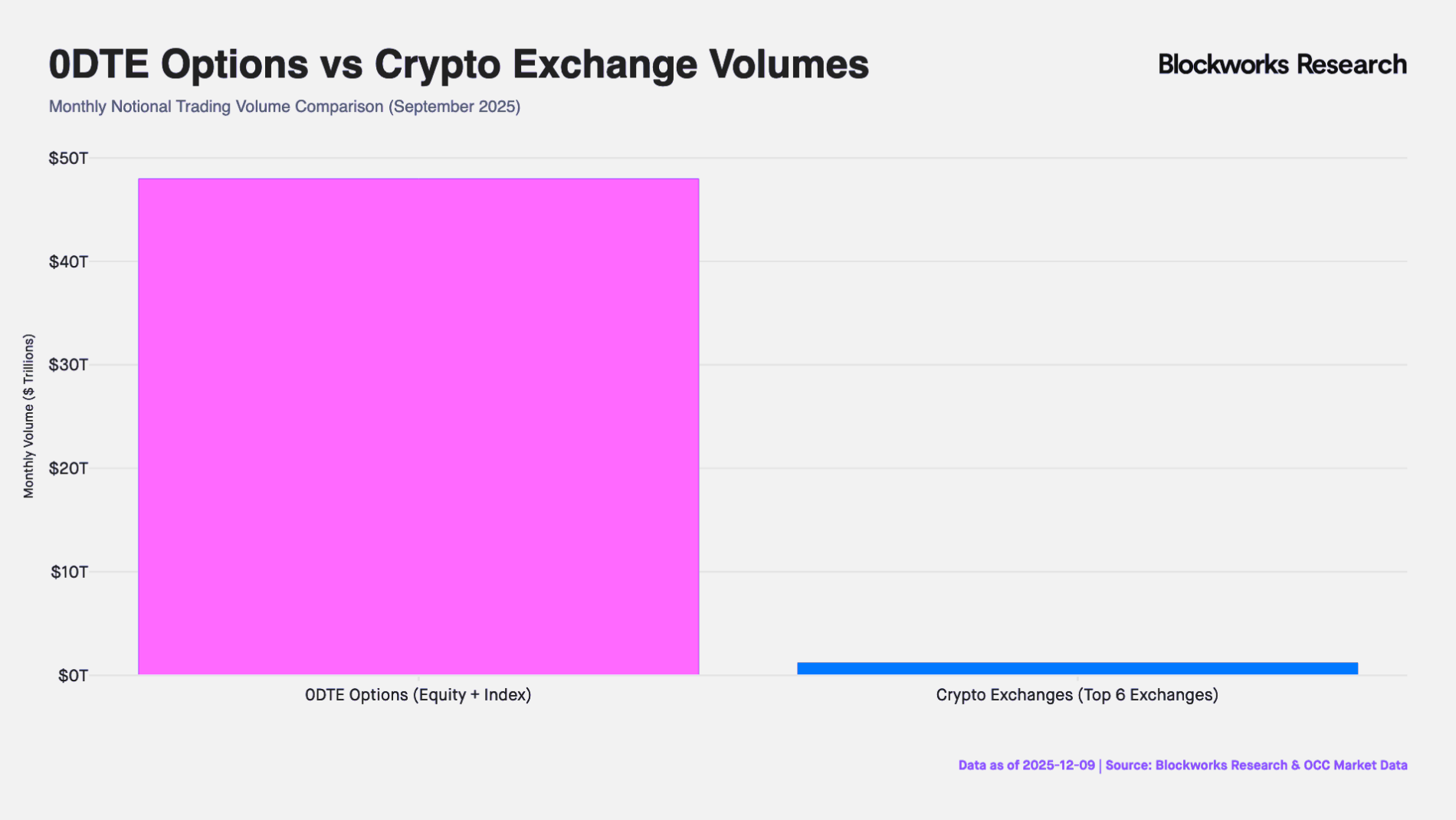

In the past decade, the U.S. options market has experienced profound structural changes, according to data from major options exchange Cboe Global Markets, the trading volume of 0DTE options in S&P 500 index options has soared from less than 5% in 2016 to over 60% currently, with a monthly nominal trading volume of $48 trillion (about 40 times the monthly trading volume of perpetual contracts on CEX exchanges). This data not only reflects an increase in trading frequency but also reveals a massive capital force in the market seeking extremely high leveraged exposure intraday.

Note: 0DTE stands for "Zero Days to Expiration," meaning options that expire the same day, which are also known as end-of-day options. Traders use them to engage in ultra-short-term speculation, gaining quick returns while avoiding overnight holding risks.

Figure: The above two images show the proportion of S&P 500 index options with different expiration times from 2016 to 2025. It can be seen that 0DTE Options accounted for nearly only 5% of the options market in 2016, but by 2025 the market share soared to 61%, indicating that nearly half of the S&P 500 index options trading is betting on intraday direction for ultra-short-term speculation.

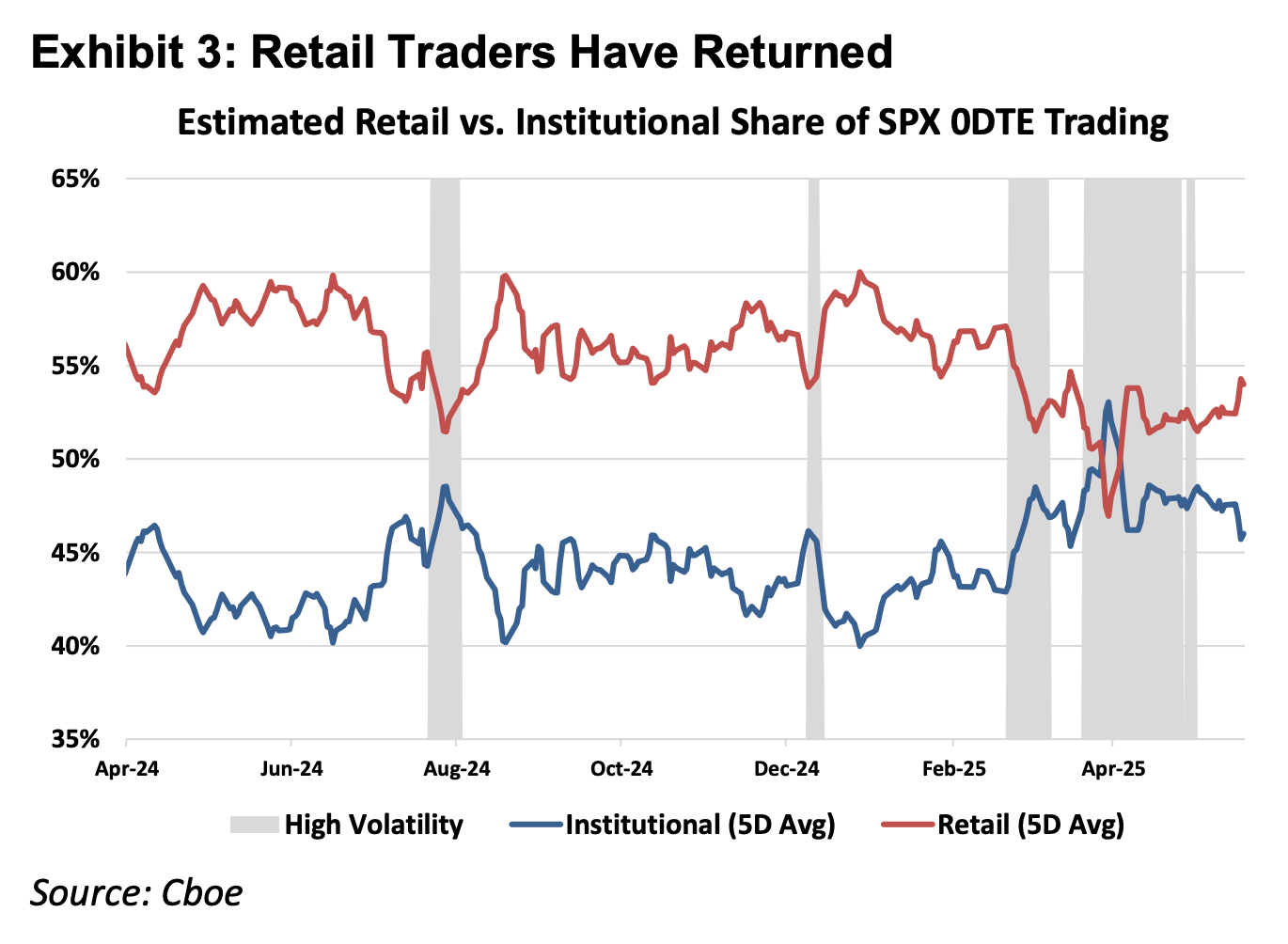

Figure: The above figure shows that retail investors are the absolute main force in the 0DTE market

From the first principles of financial instruments, financial derivatives can be divided into Delta One products and non-linear products. Traditional Delta One tools like stocks and futures have symmetric risk exposures: the gains from the rise in the underlying price and the losses from the fall are linearly proportional in scale. However, the original purpose of options design was to manage asymmetric risks.

For example, a fund manager holding a large number of Apple Inc. stocks remains unwilling to sell them due to optimism about the company's long-term fundamentals but is worried about a significant stock price decline driven by short-term earnings volatility. In this case, he can purchase put options to insure his position. In this structure, his potential for profit still remains with the rise in stock price (symmetric upside potential), but his loss is strictly limited to the premium paid (asymmetric downside risk).

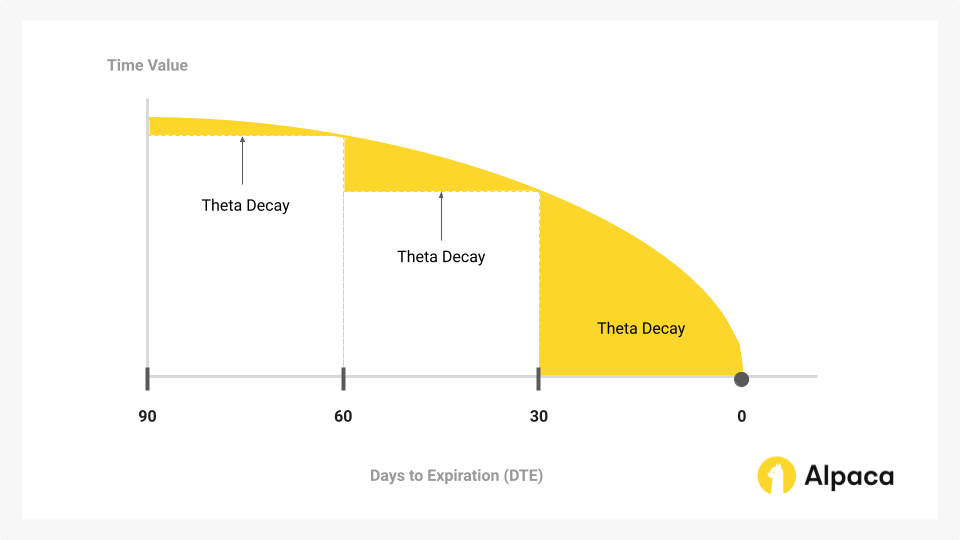

It is precisely to achieve this "separation of rights and obligations" insurance function that the cost structure of options must reflect not only the intrinsic value direction (Delta) but also include elements that reflect volatility possibility (Gamma) and time decay (Theta).

The significant growth of the 0DTE market in recent years reveals a paradox: many traders are not seeking to manage asymmetric risks or engage in complex volatility trading but rather using it as the only way to gain intraday directional leverage. In this case, traders are forced to pay a hefty time value cost (Theta Decay) for an "insurance function" they do not need. As long as the speed of increase in the underlying asset is not sufficient to cover the rate of decay in time value, even if the directional judgment is correct, the trade will still incur losses.

Figure: Time value is the main part of options that shrinks over time and is the core of 0DTE options traders' struggle.

Therefore, perpetual contracts as a type of Delta One product hold value in stripping off excess time and volatility costs, providing pure linear leveraged exposure that can match the speculative needs of this part of capital more precisely from a mathematical logic compared to 0DTE Options.

1.2 Market Entry 2: CFD Market in Non-U.S. Regions

In markets outside the U.S., retail leverage demand is mainly met by CFDs (Contracts for Difference), projected to reach a monthly average trading volume of $30 trillion in 2025.

While CFDs offer a linear return Delta One structure, their market operational model is broker-based, leading to significant transparency issues. The vast majority of CFD brokers adopt a B-Book (internal market making) model, meaning that brokers directly act as counterparties to clients (although some well-controlled brokers in the industry will hedge against profitable clients to avoid risks, due to the top companies in the CFD market only accounting for 20% market share, the remaining 80% is filled with many small and medium brokers, resulting in practices that rely on client losses to profit). In this zero-sum game structure and opaque black box, brokers have the technical authority and economic motivation to adjust quotes, slippage, and execution speed.

Compared to CFD products, RWA Perps can also be understood as a form of "transparent CFD based on smart contracts." By putting the clearing logic, funding rate computation, and oracle prices on-chain, DeFi protocols eliminate the possibility of centralized brokers intervening in trade outcomes. At the same time, the atomized settlement mechanism based on stablecoins enhances fund circulation efficiency to the second level, achieving true fund self-custody and real-time clearing.

2. Challenges in Constructing RWA Perps Products

RWA Perps are not merely a simple replication of the Perps focused on crypto assets that we have seen before. Crypto assets have characteristics such as 24/7 trading, real-time pricing, and T+0 on-chain settlements, but traditional assets are constrained by the legal framework of the physical world, holiday systems, and outdated bank settlement agreements.

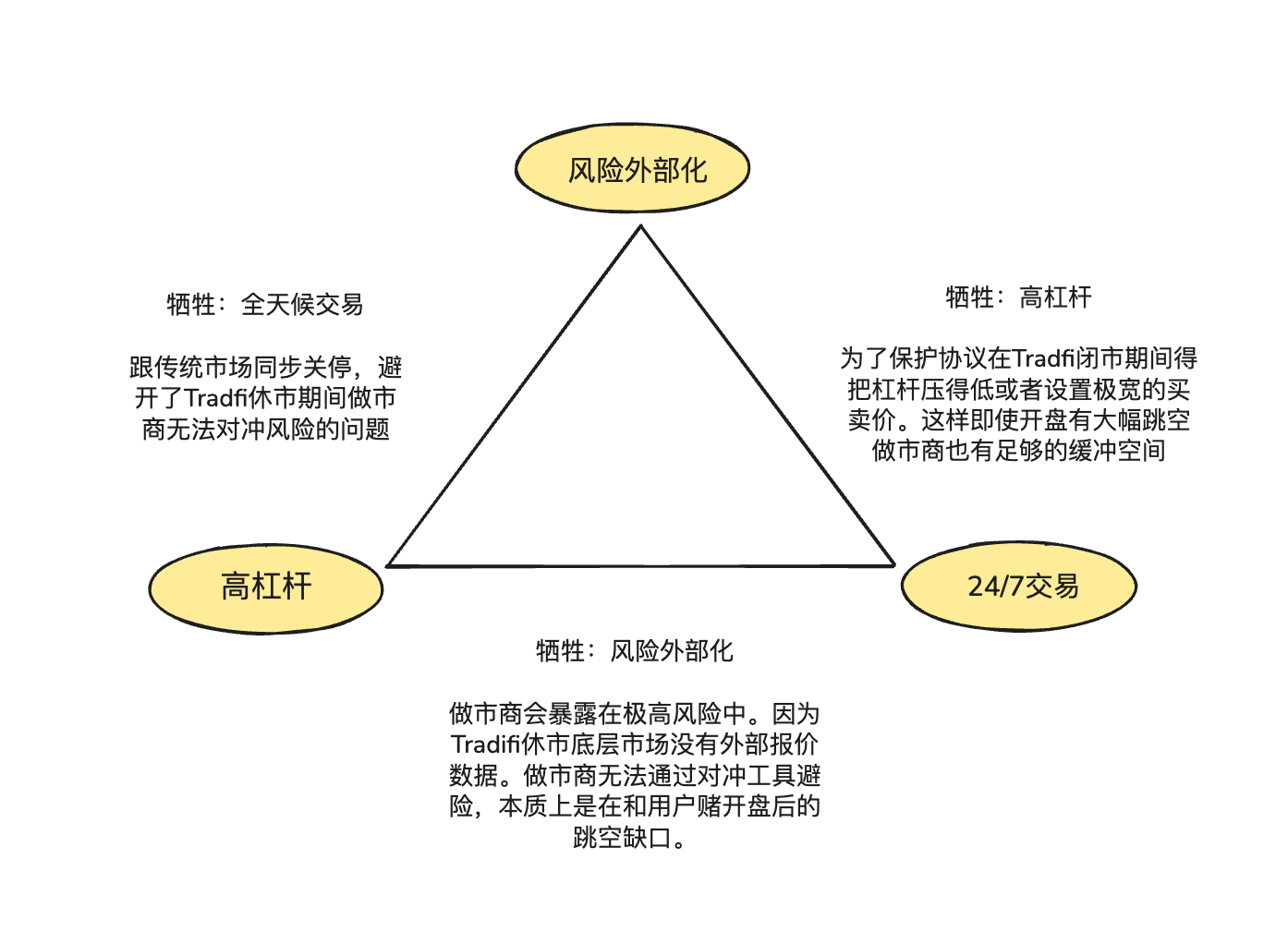

This asynchronous nature of underlying properties forms the "impossible triangle" in product design for RWA Perps:

- High Leverage: Meets retail users' speculative demands for high multiple leverage.

- 24/7 Availability: Maintains the core value of DeFi for transactions anytime and anywhere.

- Risk Externalization: Ensures that protocols and market makers do not bear directional betting risks, allowing for systematic long-term survival.

2.1 How to Anchor On-Chain Prices of RWA Perps When the U.S. Stock Market is Closed?

The essence of Perps products is "the mirror of price discovery," requiring a continuous feed of external spot prices. However, when Nasdaq or CME is closed on weekends and overnight, it causes a break in oracle data sources.

This pricing vacuum and misalignment during U.S. stock market closures generate two core risks:

Risk 1: Weekend Market Makers Lack Sufficient Hedging Channels

Professional market makers provide extremely narrow spreads and deep liquidity because they do not bet on direction but seek neutral positions while only collecting spreads. This means when market makers sell a $1 million Tesla stock contract to traders on-chain, they must immediately purchase an equal amount of the asset in traditional spot or futures markets to hedge this risk exposure.

When traditional markets are closed, hedging channels shut down, and market makers cannot adjust their hedging positions. To mitigate this risk, market makers can only choose to withdraw orders or embed significant risk premiums in their quotes during off-hours. This explains why the spreads in traditional order book models can nonlinear expand to tens of times normal levels on weekends, easily leading to liquidity drying up.

Risk 2: "Gap Risk" from High Opens or Low Opens on Monday

Due to the nature of 24/7 trading in crypto native assets, price curves are generally continuous, and the clearing engine has ample time to settle users' positions during price drops. However, in the field of RWA Perps, the pressure of price changes accumulated during market closures is instantaneously released when trading resumes on Monday. If there is significant gap opening on Monday, the clearing engine may find itself in a "price fault" vacuum, unable to find counterparties to execute settlements before triggering liquidations.

In response to the above dilemmas, there are currently two main handling solutions for RWA Perps:

- Internal Simulated Pricing (e.g., TradeXYZ / Hyperliquid): Introduces an Exponential Moving Average (EMA) algorithm to slowly allow prices to "drift" based on on-chain buying and selling strength when the oracle disconnects, maintaining a 24/7 shell but theoretically remains a potentially manipulable "shadow market."

- Mandatory Risk Downscaling (e.g., Ostium): This is a more pragmatic risk management solution. Ostium incorporates 0DTE characteristics: requiring all high-leverage positions to be automatically liquidated or significantly reduced in leverage before closing. Only low-leverage positions (with sufficient margin buffer to cover 5%-10% of gaps) may be allowed to roll over. This approach sacrifices part of "perpetuality" in exchange for the absolute safety of the system facing Monday's gap opens, preventing systemic defaults from penetrating the LP pool.

2.2 How to Provide TradFi-Level Trading Depth on-chain at Low Cost?

In developing DEXs, the choice of liquidity provision and order execution mechanism is a core variable determining system capital efficiency, risk distribution logic, and user experience. Currently, the two mainstream solutions are: CLOB (Central Limit Order Book) and Oracle-based Pool.

Hyperliquid validates the success of the order book model in crypto native assets, with the core being zero friction in hedging execution: market makers can move risks across platforms within milliseconds utilizing stablecoins. After receiving orders on-chain, market makers can use stablecoins on CEXs operating 24/7 for millisecond-level hedging. Since crypto funds and assets operate within a highly interconnected crypto network, hedging costs are extremely low, allowing market makers to compress quote spreads to an extremely narrow range to attract trading volume, creating a positive feedback loop.

In the RWA domain, market makers face significant cross-border hedging friction: on one hand, the time mismatch between on-chain USDC (T+0) and traditional fiat settlements forces market makers to keep large amounts of dollars idle in traditional accounts as hedging reserves; on the other hand, the closure mechanisms of traditional banks on weekends and holidays result in market makers being unable to hedge promptly during unanticipated market movements.

This is also why the founder of Ostium, Kaledora, has insisted on adopting a pool-based model instead of an order book, as she believes that the zero-friction hedging seen in crypto native exchanges is challenging to implement in the RWA perps space, as market makers cannot use stablecoins to hedge NVDA orders in milliseconds due to the numerous obstacles posed by traditional bank pathways.

2.3 How Does the System Ensure It Doesn't Go Bankrupt When Traders Profit from One-Sided Market Trends?

The third dilemma concerns how the protocol ensures long-term solvency through external hedging. GMX's pool model persists in the crypto market thanks to its role as a "passive dealer", leveraging statistical advantages under large samples to stabilize the absorption of position wear and liquidation profits generated by high-leverage positions in frequent fluctuations. This model's mathematical expectation is favorable for pool LPs in the highly volatile crypto market.

However, the risk distribution of RWA assets is entirely different. Mainstream indices like the S&P 500 often exhibit prolonged one-sided bullish trends lasting several years. In the absence of a risk externalization (hedging) mechanism, users' continuous profits will directly transform into net losses for the LP funding pool, causing the system to not only fail to capture volatility dividends but to be entirely drained by one-sided positions, ultimately facing solvency exhaustion.

3. Representative Projects and Structural Conflicts: Oracle Pricing + Pool (Pool Based + Oracle Pricing) vs. Order Book

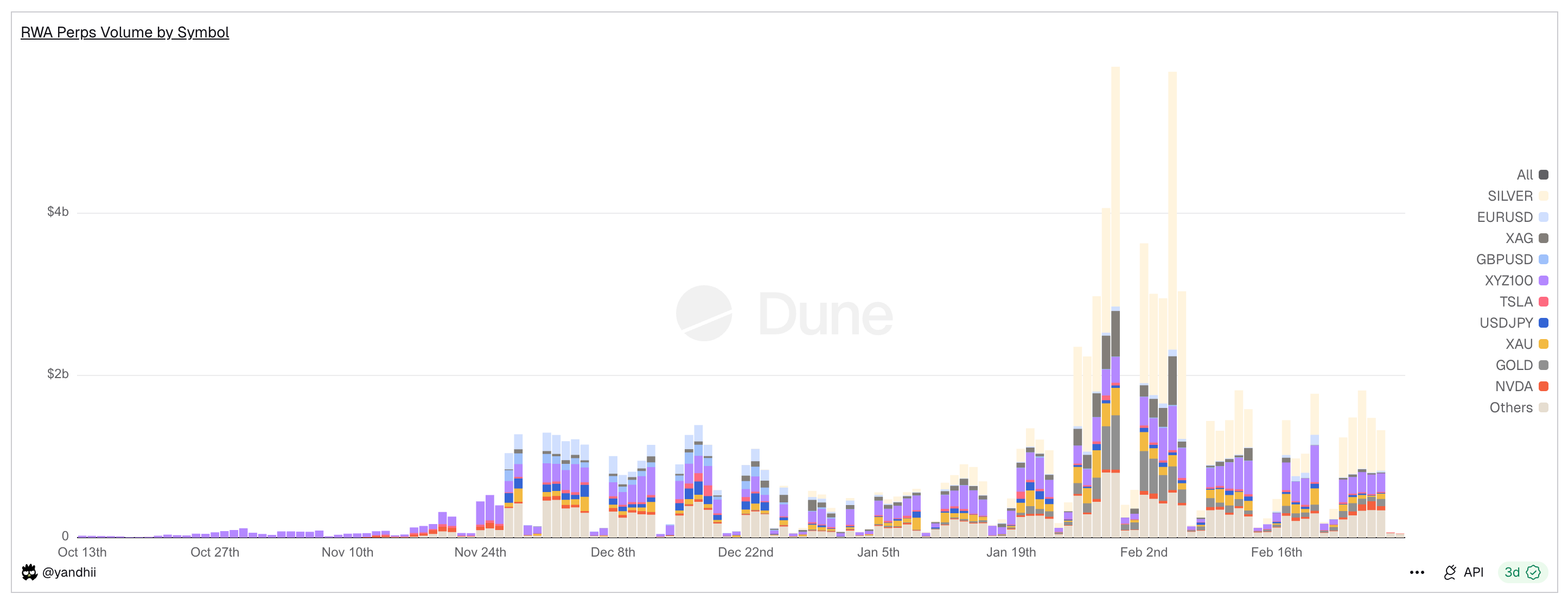

Figure: Daily trading volume of RWA Perps Dex, where trading volume significantly dwindles over the weekend

The core contradiction of RWA Perps revolves around "the fault of physical time": although various RWA Perps Dex platforms have generated over $20 billion in trading volume within 30 days, there is a sharp decline in trading volume of 70-90% during weekends. This data reveals the real status of the industry: despite DeFi's efforts to free itself from the gravity of traditional finance, liquidity remains heavily dependent on TradFi's opening hours.

In response to this fault, the market has evolved two distinct architectural paradigms: the active hedge pool model represented by Ostium, and the internal pricing order book model represented by Trade.xyz in the Hyperliquid ecosystem.

3.1 Early RWA Perps Projects: Synthetix, Gains Network

Before Ostium and Hyperliquid attempted to reconstruct RWA trading through complex hedging mechanisms or order books, the DeFi market had already conducted the first round of "synthetic assets" experiments. Early protocols represented by Synthetix and Gains Network validated the concept of RWA Perps, demonstrating strong demand for on-chain capital exposure to traditional assets but also exposing the limitations of first-generation mechanisms in capital efficiency and risk control.

Synthetix: Global Debt Pool Model

Synthetix was one of the first protocols to attempt to bring real asset prices onto the blockchain. Between 2020 and 2021, Synthetix aggressively tried to launch sAAPL, sTSLA, and other mirror stocks, attempting to bring U.S. stocks on-chain.

As a pioneer of the "pool counterparty" model (where counterparties are all SNX stakers), Synthetix designed a model of exchange with unlimited liquidity and no order book: all synthetic assets are freely exchanged at prices provided by oracles, and users do not need to match trading partners, which greatly resolved the liquidity bootstrapping problem in early days (especially when liquidity mining incentives were first introduced).

However, after 2021, Synthetix delisted most RWA assets because the protocol layer lacked an active hedging mechanism, making it easily vulnerable to attacks when prices of U.S. stocks like sTSLA could not be updated during market closures.

Overall, Synthetix pioneered the model of providing on-chain RWA mirror asset liquidity through derivative collateral pools, and the design of no order book + oracle pricing remains influential to this day, but the product side essentially began to withdraw from the RWA Perps market around 2022.

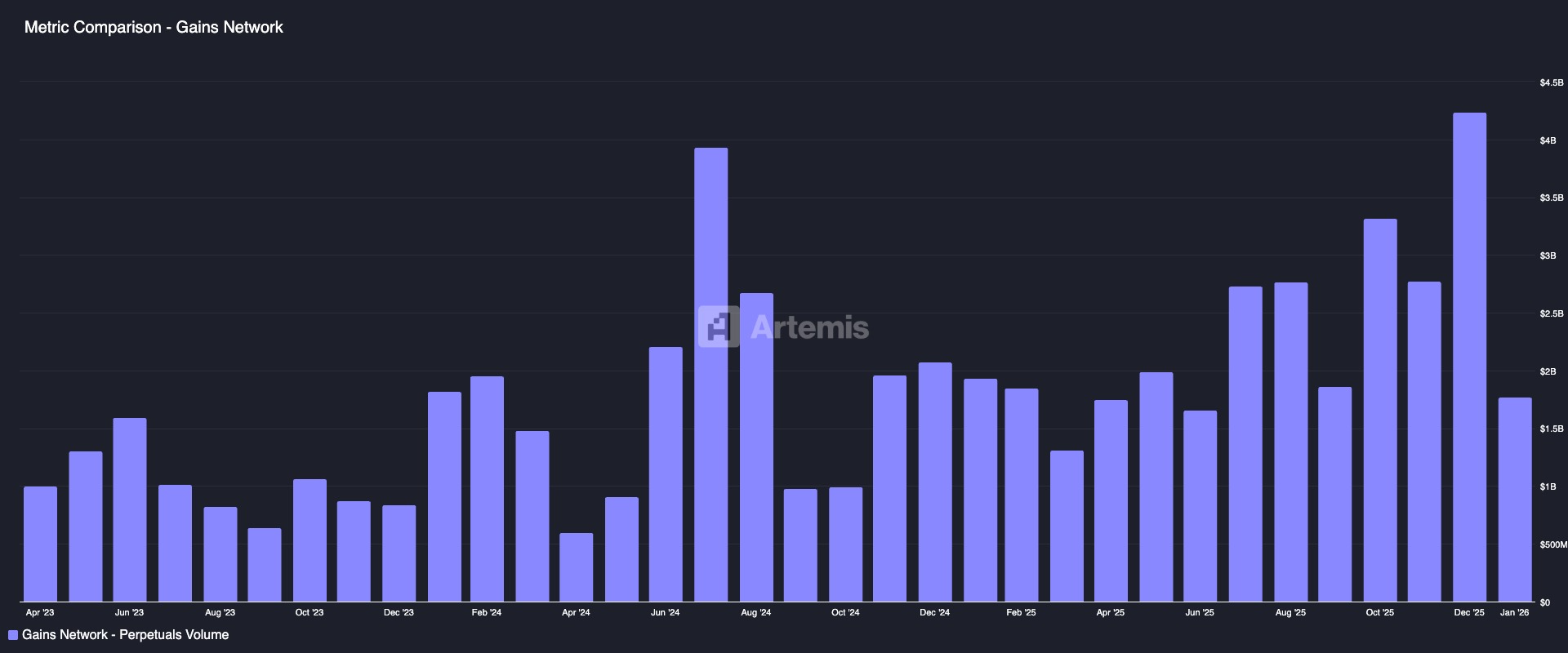

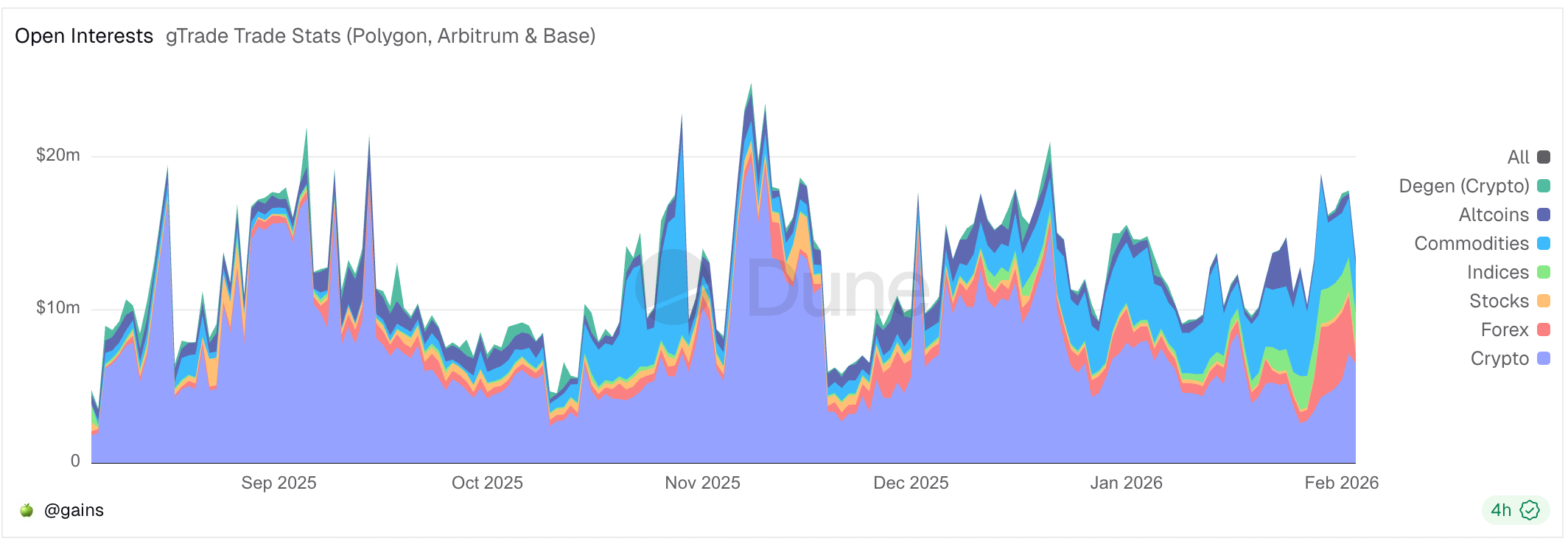

Gains Network (gTrade): Oracle Pricing Driven Market Making Pool Model

Gains is another early representative project that explores on-chain RWA synthetic leveraged trading, supporting multiple trading pairs including cryptocurrencies, forex, and U.S. stocks. Its design approach uses independent asset pools as counterparties: users initiate synthetic leveraged positions by collateralizing USDC, DAI, or ETH, with trading profits and losses borne by the funding pool (gToken Vault).

- Liquidity Model and Market Making Game Mechanism:

- Unilateral Treasury: The Gains market-making funding pool mainly consists of stablecoins like USDC/DAI.

- GNS Token as Risk Buffer and Incentive: To prevent extreme scenarios from resulting in the market-making fund pool being drained, the protocol introduced the GNS token as a last line of defense. When the market-making fund pool has surplus, the protocol will use excess profits to buy back and burn GNS tokens to reduce inflation. When the market-making fund pool incurs losses, the system will issue more GNS and sell it off-market to replenish market-making funds.

In terms of pricing, Gains obtains real-time prices based on Chainlink and adds a fixed spread, with spread income distributed as fees to LPs and GNS stakers. Risk control measures introduced include price impact fees (charging extra fees for large orders to simulate slippage and compensate for funding pool risk), limit protection (setting upper and lower limits for profits and losses to enforce forced liquidation), and other designs.

Overall, Gains provides a highly leveraged, multi-market covering synthetic trading experience and is viewed as an important example of decentralized exchanges benchmarking centralized platforms, demonstrating that the "oracle + funding pool" model can support large-scale trading under reasonable risk control, while also exposing challenges such as the need for funding pools to bear concentrated profit risks and the lack of hedging mechanisms. These issues offer insights for subsequent project mechanism innovations.

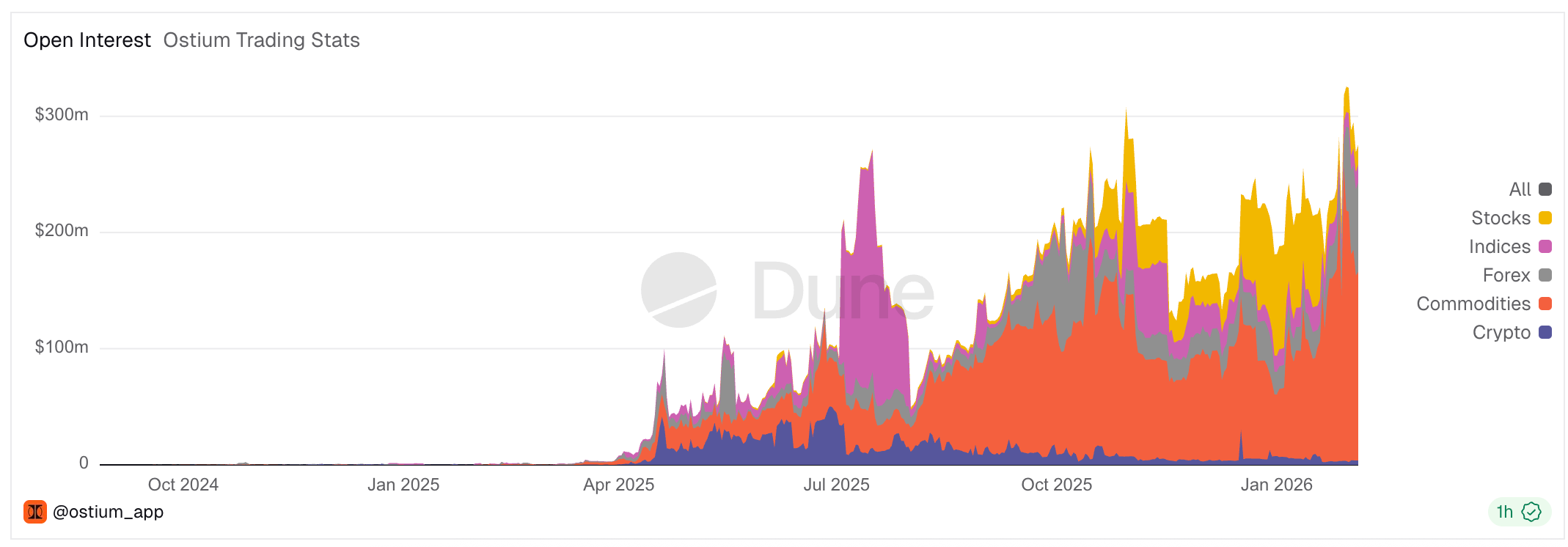

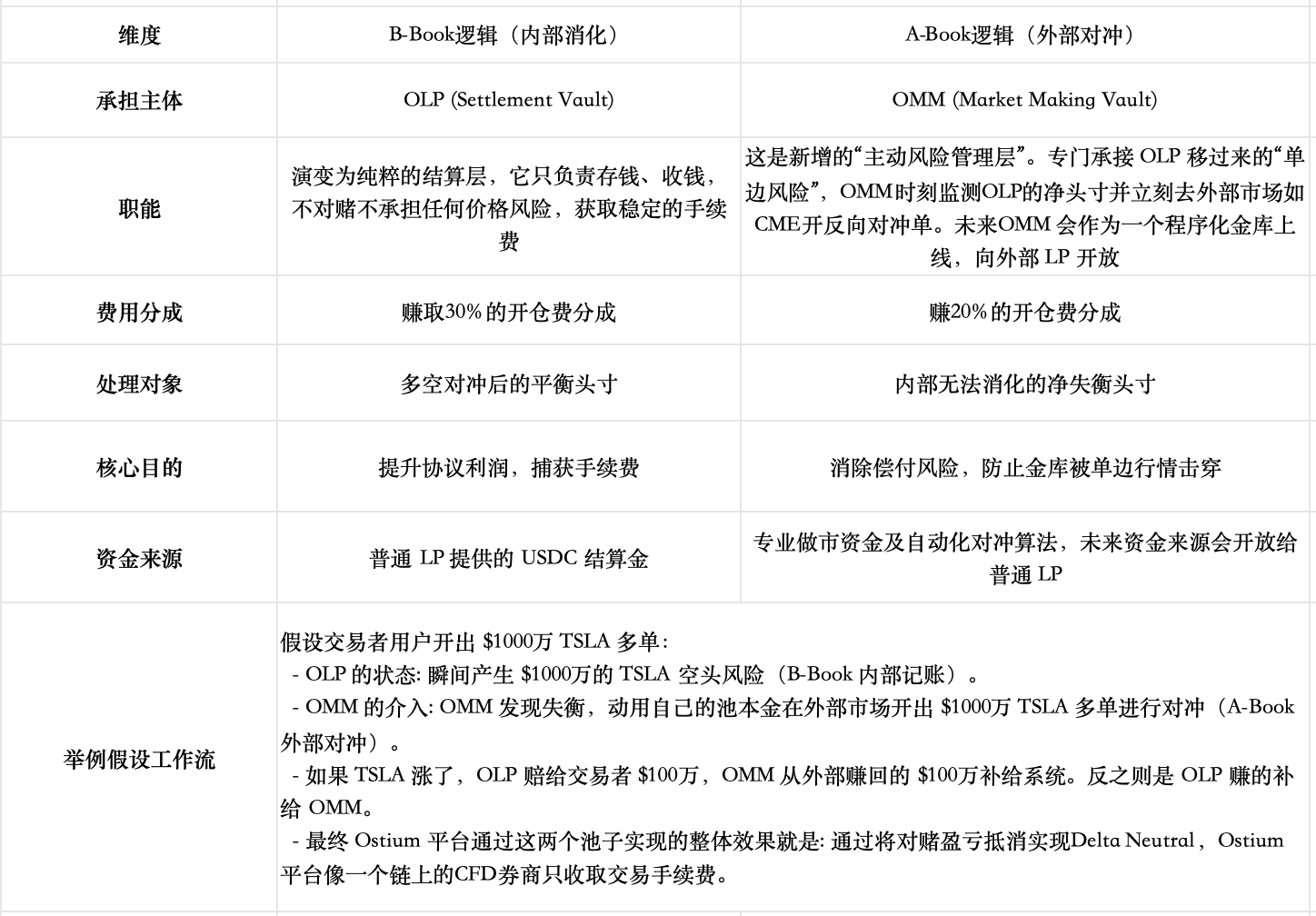

3.2 Ostium: Breaking Through the Limitations of the Pool-based Model to Create On-chain CFD Brokers

Ostium is a rising RWA Perp DEX that officially launched on the Arbitrum mainnet in August 2025. In terms of liquidity supply and order execution mechanisms, Ostium still chose a pool-based model as its core architecture. However, reflecting on the mechanisms of early projects like GMX and Gains Network, they deeply realized that the opposing game relationship of "trader profits equal LP losses" inherent in traditional pool models is disadvantageous in the long run for LPs and crucially limits trading volume caps, hindering market expansion (as analyzed in the previous Perp Dex research), leading to some special designs that integrate traditional broker A-Book (hedging) and B-Book (internal digestion) on-chain to alleviate this zero-sum game conflict.

Interpretation of Liquidity Model and Market Making Game Mechanism

- Basic Liquidity Model (Two-Tier Pool Structure)

- First Buffer: Liquidity Buffer This is the protocol's "moat," accumulated from protocol revenue. Trader profits are first covered from here, and losses initially enter here. Although the detailed mechanism differs, the role is similar to the protective buffer in the Gains Network’s market-making pool.

- Second Buffer: Market Maker Vault (OLP Vault) This is the pool of funds provided by LPs. Only when the Liquidity Buffer funds are exhausted will the OLP intervene as a direct counterparty.

- Core Evolution to Break Through Original Pool-based Model Limitations: Separating "Settlement" and "Market Making" Completely: Ostium recognizes that the simple two-tier buffers cannot handle long-term directional imbalances (the data shown in the lower chart confirms this, as funds in the liquidity buffer can be easily depleted; when version 1 of the product only had those two basic layers, LPs still faced long-term one-sided risk), that’s why Ostium has proposed more significant designs—completely separating the functions of settlement and market making from the originally passive LP market-making pool.

Currently, the treasury for the OMM market-making hedging has not yet officially launched. It is anticipated that when high trading volumes are supported, the product will require a professional market-making team with strong execution capabilities, which poses significant challenges: teams must not only have compliant entity qualifications to interface with traditional finance but must also achieve millisecond cross-market hedging to avoid oracle and external market basis risks; simultaneously, they must have powerful capital scheduling capabilities to overcome timing mismatches in fund circulation on-chain and be able to monitor delta net position imbalances in real-time, flexibly applying dynamic spreads or impact fees for precise risk control and flow limits.

Risk Control During Market Closures

Ostium deeply aligns with U.S. stock trading hours, ensuring that market orders are executed only during market opening by embedding timestamps in the oracle, effectively eliminating price vacuum risks during closures. To address the common gap risk in U.S. stocks, the platform establishes strict "forced liquidation checkpoints": 15 minutes before daily closing, the system automatically forces the liquidation of positions exceeding a threshold (e.g., 10x leverage), bringing daily maximum leverage back to a safe range.

Why Didn't Existing Pool-Based Projects Like GMX Adopt Similar Designs?

We believe the primary reason GMX insists on not separating directional risk in the pool model is that the trade-off is too significant and the market's starting points differ: the current design has achieved relative balance through internal mechanisms (such as adaptive funding fees, price impact, long/short pool separation), and introducing an external/independent hedge vault would sacrifice returns, increase complexity, and introduce centralization risks. Moreover, GMX's pool actually bears the aggregated exposure of all traders; in a highly volatile crypto market, individual random bets statistically tend toward a negative expected value, with the pool as a comprehensive counterparty capturing positive expected values. In contrast, Ostium focuses on stock and other RWA markets, which are relatively less volatile, and aims to penetrate the traditional CFD brokerage market.

Additionally, in August 2025, there was a proposal in the GMX governance forum Global Hedge Vault (GHV), hoping to introduce external market maker mechanisms to implement something like Delta Neutral, indicating that other pool-based projects are also paying attention to this new trend.

Why Use a Pool Model Instead of an Order Book?

Ostium founder Kaledora has a clear theoretical rationale for why she insists on choosing the Pool Based model and not allowing weekend trading. She has faced criticism for calling out order book projects like Trade for extreme high funding rates during weekends and has been attacked by the Hyperliquid community.

Figure: Ostium founder points out that Trade.xyz's funding rates spiked during weekend trading of traditional closures

Her theory is that the limitations of traditional pool-based models (LP carrying one-sided directional risks, the system's capital size limiting trading volume caps) have been solved by her new design. By introducing a mixed risk control of A-Book and B-Book, it transfers one-sided risks in real-time to liquidity unlimited global markets. Once one-sided risks are technically resolved, the OI cap will no longer be constrained by the pool size, and the protocol's trading volume cap will entirely depend on its distribution capability (closely resembling the business model of top CFD brokers).

In contrast, she believes the core function of an order book is price discovery, which makes sense in crypto native assets but represents a massive resource waste in the RWA domain. Because prices for stocks and forex have outstandingly perfect real-time discovery at leading global exchanges like Nasdaq and CME, recreating an on-chain order book means competing in a "anemic" environment against these trillion-dollar giants. This level of depth from traditional exchanges effectively diminishes the appeal for any large traders to choose a broker model that can quote global prices over an order book suffering from significant slippage.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。