Author: DCo (@Decentralisedco)

Translation: Deep Tide TechFlow

Deep Tide Introduction: Hyperliquid's 2025 revenue is 15% of CME's, but its market cap is only 10% of CME's—behind the valuation discount is the market's complete failure to price in the trillion-dollar TAM opened by HIP-3. The Iran war weekend was a stress test for this argument: When CME closed, the on-chain oil price futures stood alone to uphold global real-time pricing. This article illustrates with a four-scenario DCF model that HYPE’s current $37 has fallen below the bear market target price of $60, suggesting that even if HIP-3 makes almost no progress, this pricing itself has already underestimated the underlying exchange business.

Valuation Framework of HYPE

CME's 2025 revenue is $6.5 billion, with an average daily contract transaction of 28.1 million, and a market cap of $114 billion. Hyperliquid's revenue in 2025 is projected at $960 million on approximately $3 trillion in trading volume, with a market cap of $12.5 billion. Hyperliquid's current revenue is about 15% of CME's, but its market cap is only 10% of CME's. The key opportunity lies in how much of the traditional financial transaction volume can migrate to decentralized platforms like Hyperliquid.

From Crypto DEX to Global Derivatives Exchange

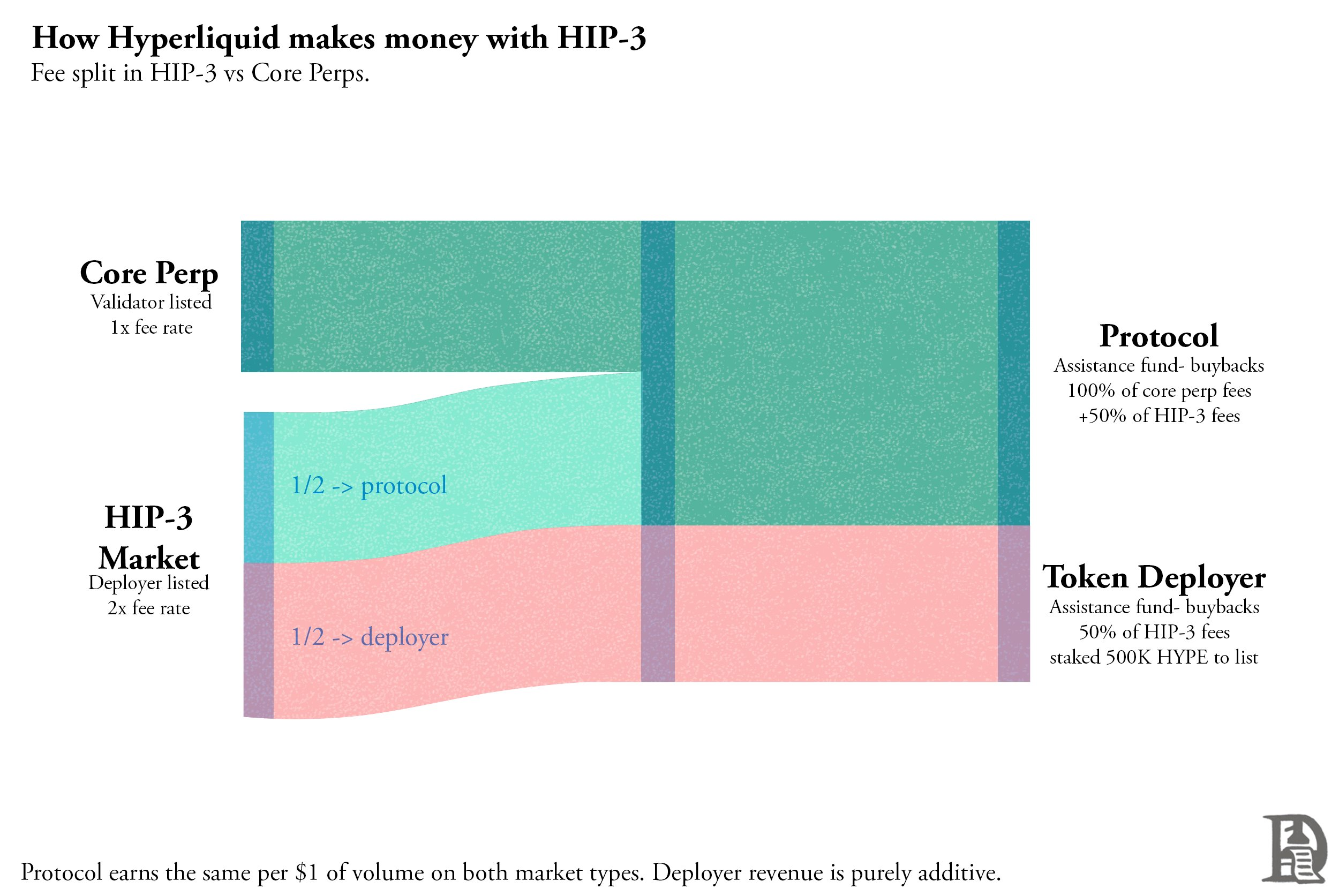

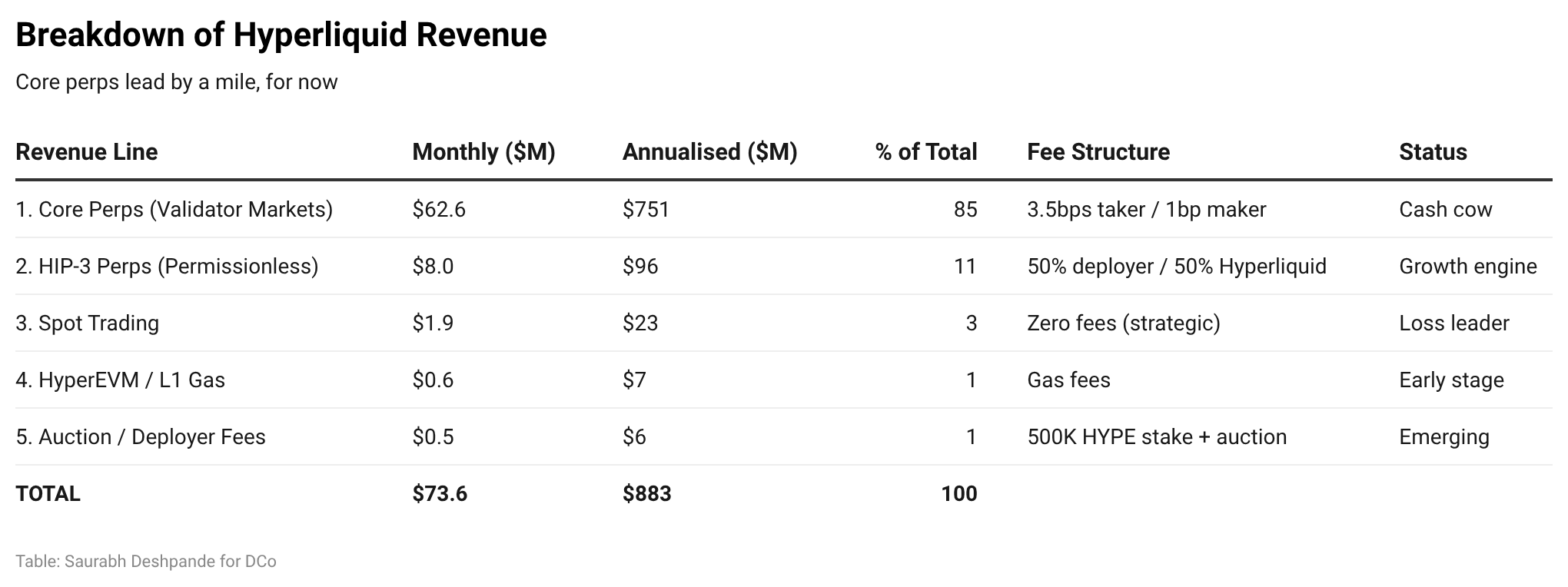

HIP-3 will launch in October 2025, supporting the listing of permissionless perpetual contracts. Deployers staking 500,000 HYPE (approximately $18.5 million at $37 each) can issue customized markets on HyperCore. The fees for these markets are double that of Hyperliquid’s core listed perpetual contracts, with half going to the deployer and the other half to the Hyperliquid protocol for buybacks. Therefore, the protocol's revenue per dollar of trading volume is the same as that of the core market, while the deployer earns additional equal profits as an incentive for listing and maintaining the market.

Within five months, HIP-3's trading volume reached $100 billion, with open interest setting a record of $1.2 billion on March 10, significantly up from $260 million the previous month.

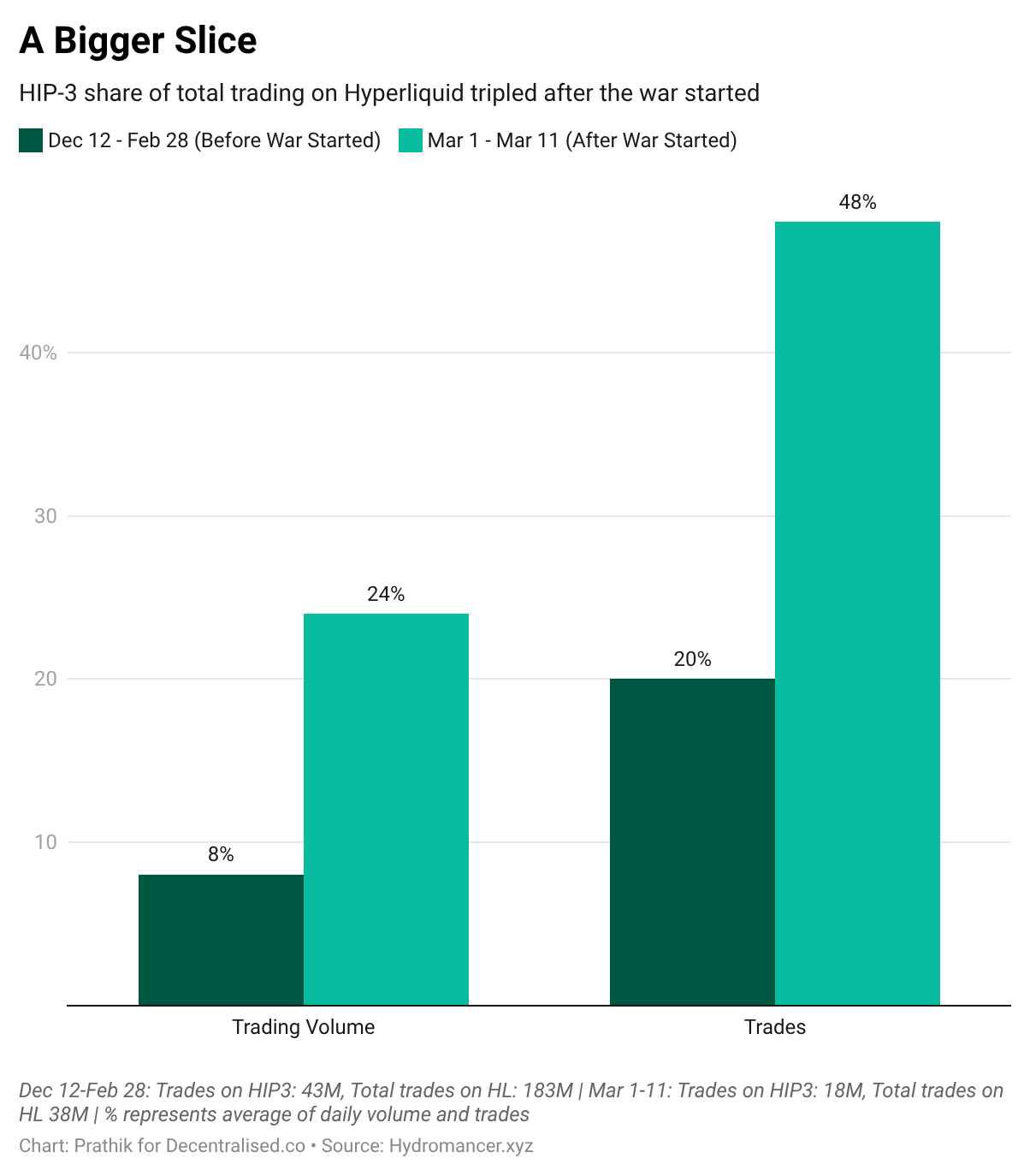

HIP-3 can list any asset: commodities, stock indices, currency pairs, Pre-IPO tokens, etc. In the past two weeks, HIP-3's share of Hyperliquid's total trading volume increased from 8% to 23%, with nearly half of the trading occurring in HIP-3 markets.

The Iran War as a Proof of Concept

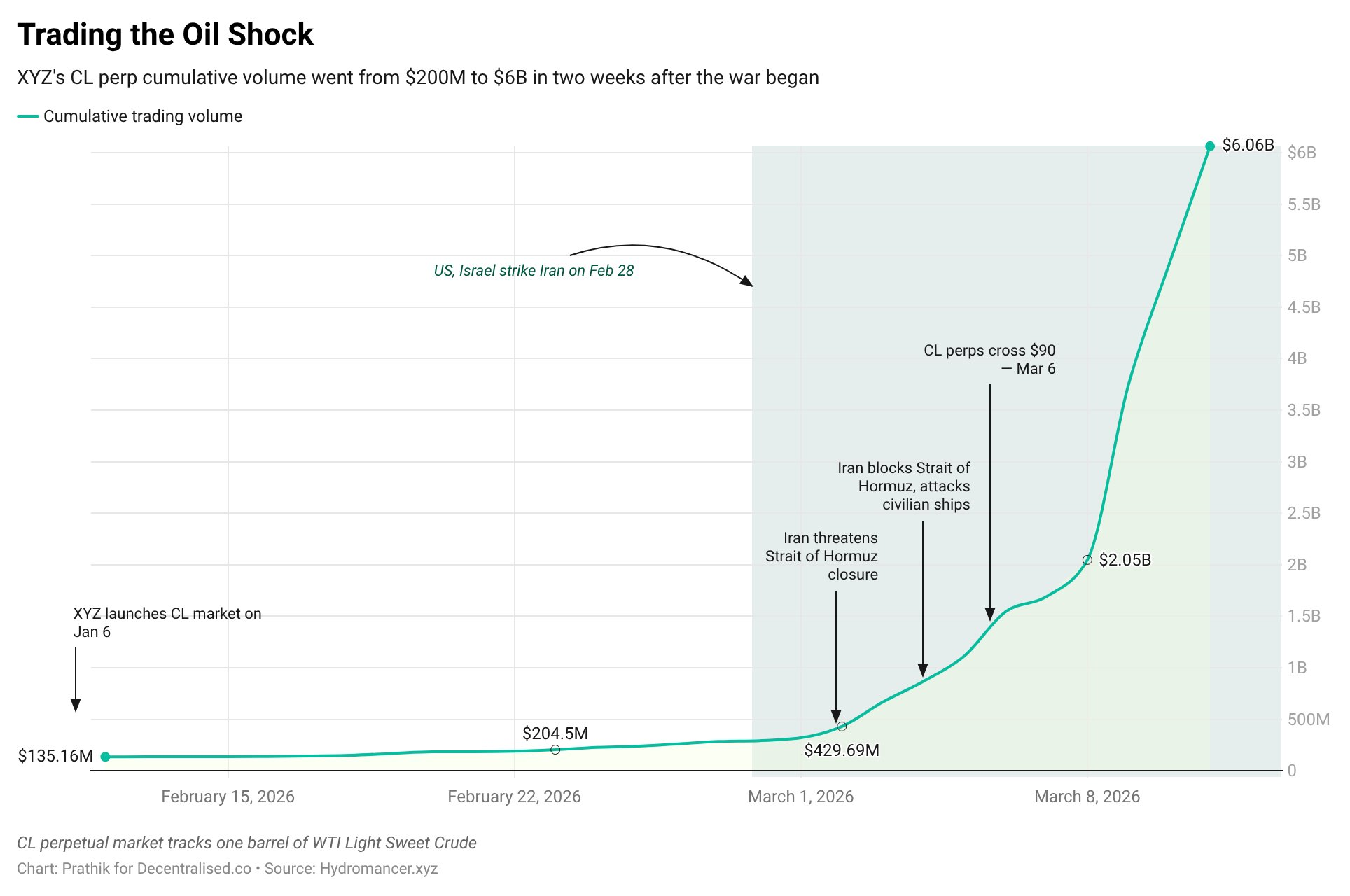

On February 28, the U.S. and Israel launched strikes against Iran during the closing hours of traditional markets. Within hours, oil-linked perpetual contracts on Hyperliquid surged 5%, as traders immediately factored in the impact on prices. The following week, after WTI recorded its largest weekly gain since 1983, the oil perpetual contract on Hyperliquid had a 24-hour trading volume exceeding $1.2 billion, with a clearing volume of $40 million. The cumulative trading volume of CL perpetual contracts rose from $200 million to $6 billion within two weeks. Bitcoin held steady around $68,000. The main battleground for macro trading was Hyperliquid, not the spot crypto market.

When CME reopened on Monday, it confirmed the pricing direction established by Hyperliquid throughout the weekend. If tokenized oil perpetual contracts can be effectively price-discovered at such volume, so too can gold, SPX, and currency perpetual contracts.

CME + 0DTE Options as HIP-3’s TAM

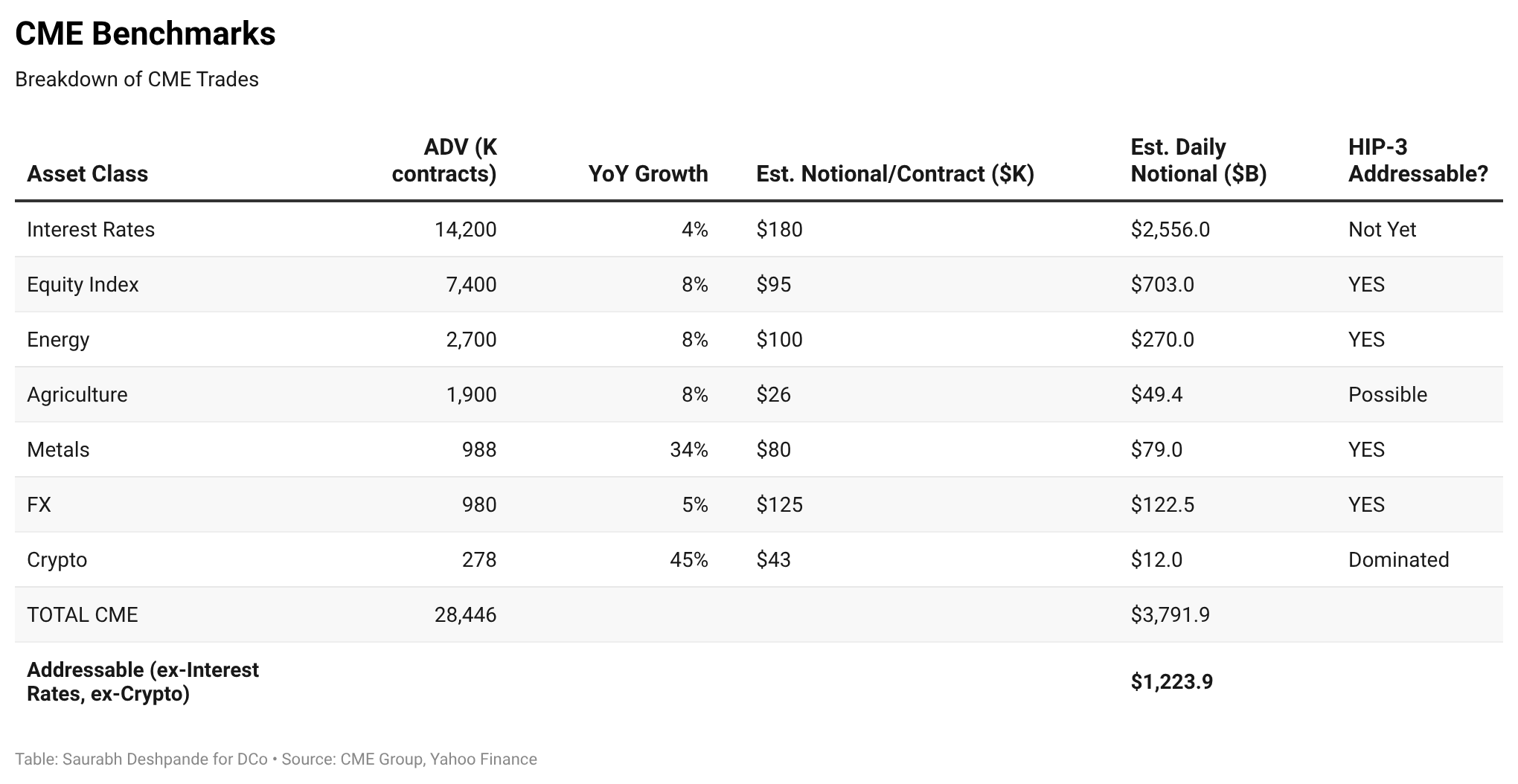

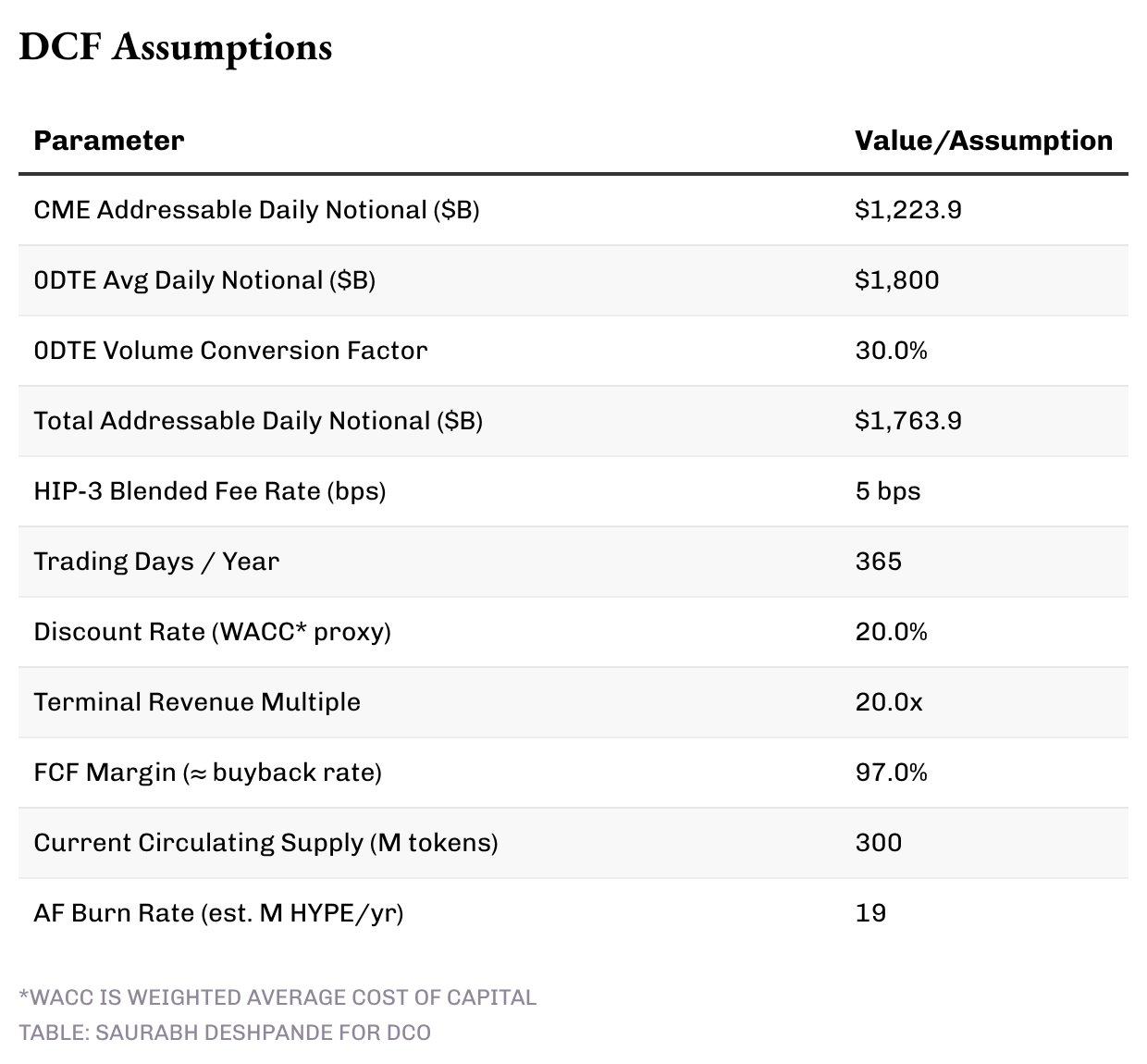

CME's average daily trading volume across all asset classes is $3.8 trillion. Excluding complex, hard-to-migrate interest rate products and crypto products already dominated by Hyperliquid, the addressable daily trading volume at CME in the fields of stock indices, energy, metals, agriculture, and foreign exchange is approximately $1.2 trillion.

Additionally, we consider the 0DTE (same-day expiration) options market. The nominal daily value of 0DTE options for SPX alone exceeds $1.2 trillion in May 2025. Combining this with the 0DTE options volume representing 45% of all SPY options, FalconX estimates the total nominal value of 0DTE options at around $1.5 to $2 trillion per day. Behavioral-wise, these represent perpetual contract traders operating on the options infrastructure—because there are currently no stock perpetual contracts in the regulated market. Perpetual contracts eliminate the complexity and costs associated with 0DTE options.

A crucial adjustment: the nominal value of 0DTE options overestimates the equivalent volume of perpetual contracts. We apply a 30% conversion factor to the nominal value of 0DTE options to estimate the actual possible migration of equivalent perpetual contracts. Therefore, HIP-3’s total addressable market is approximately $1.74 trillion daily: $1.2 trillion addressable at CME, plus about $540 billion from the 0DTE conversion.

Scenario Analysis

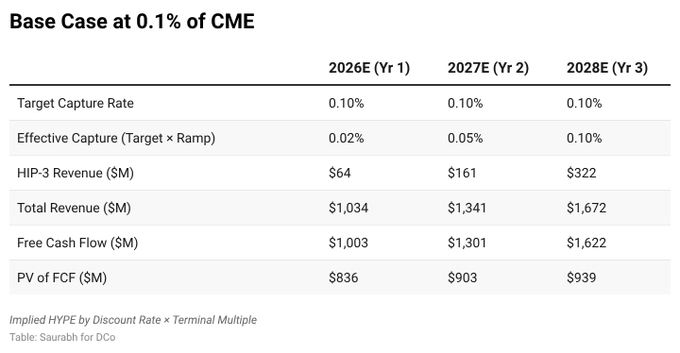

Based on the percentage of Hyperliquid's capture from the $1.74 trillion daily TAM through HIP-3, we have constructed four scenarios using a three-year discounted cash flow framework.

Each scenario assumes a gradual ramp-up in penetration: achieving 20% of the target in the first year (2026), 50% in the second year (2027), and 100% in the third year (2028), to reflect the reality of gradual market share accumulation. Baseline revenues from core crypto perpetual contracts, spot, EVM Gas, and auction fees are predicted independently from the revenue waterfall model, growing from $970 million in 2026 to $1.35 billion in 2028.

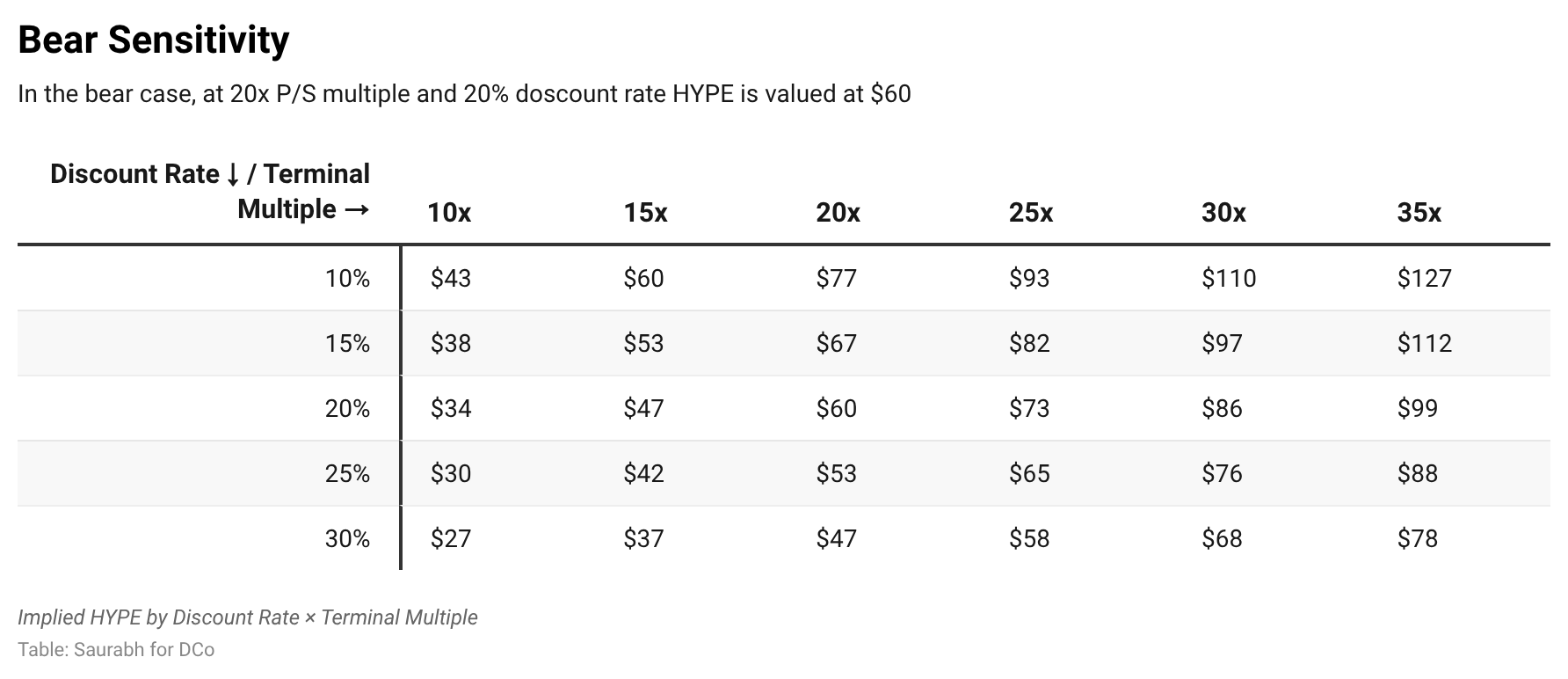

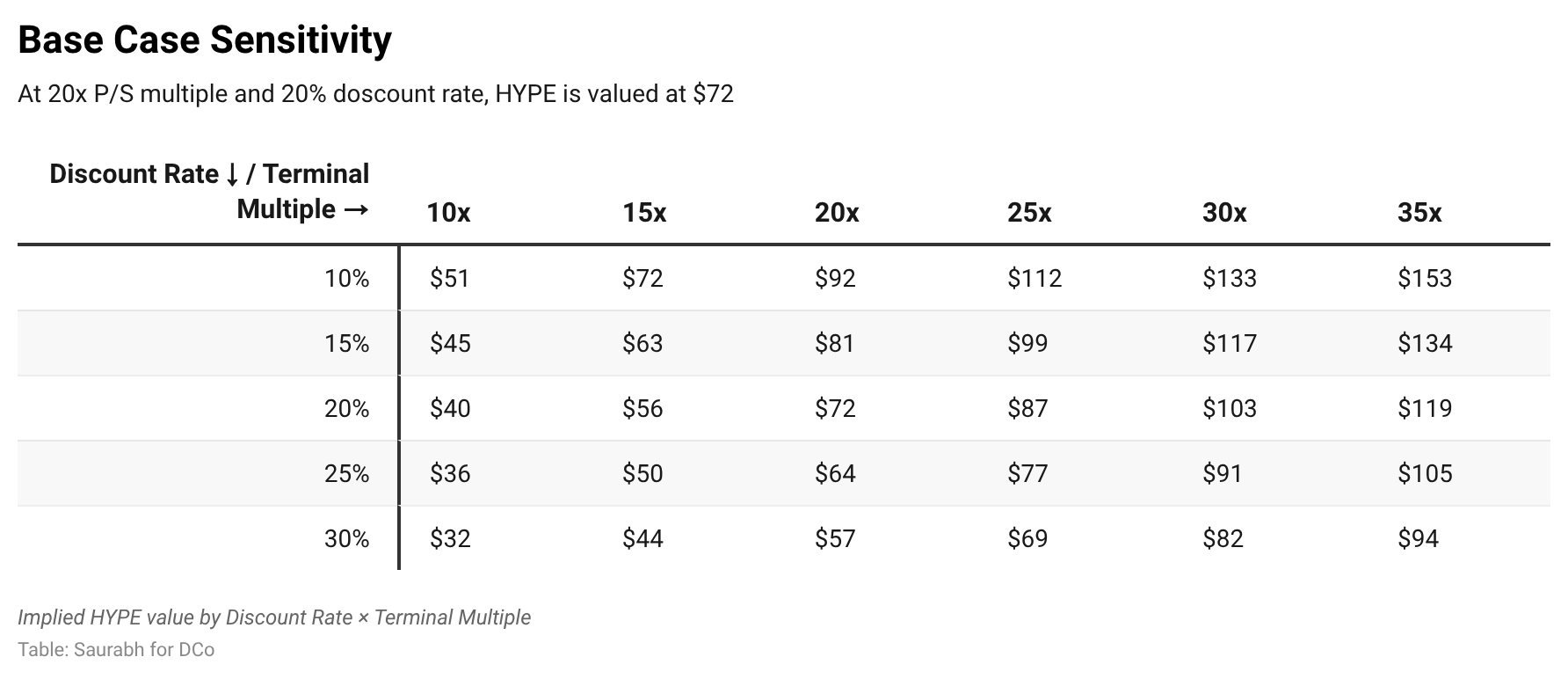

We adopt a 20% discount rate and a terminal multiple of 20 times the year 3 revenue—moderately premium to CME’s current 17.5 times EV/revenue, reflecting Hyperliquid's higher growth trajectory. The 20% discount rate reflects the risk of crypto protocols but also acknowledges that Hyperliquid is a profitable business with auditable on-chain cash flow, not a pre-product stage token. Sensitivity tables allow for stress testing up to a 30% discount rate.

The model also considers expected changes in circulating supply. On the supply side, about 23.8% of the total HYPE supply is allocated to core contributors, locked for one year, followed by a linear unlock over 24 months. Co-founder Iliensinc confirmed that distribution (if any) occurs on the 6th of each month and added that "the unlocking is not done linearly." The actual pace has varied significantly: approximately 2.6 million in December (of which 850,000 were re-locked), 1.2 million in January, and in February, the team reduced the month's unlocking volume by 90%, allowing only 140,000. As Arthur Hayes pointed out, 66.6% of contributor tokens are still locked until 2027-2028, with no investors unlocked.

We do not anchor to peak or trough values but use the average monthly value since the beginning of distribution—about 1 million HYPE, or 12 million annually—as our base assumption. Validator staking emissions, under the current approximately 400 million staked tokens and a 2.37% reward rate, contribute about 10 million additional tokens annually.

On the other hand, the assistance fund (AF) has cumulatively burned 42.8 million HYPE over approximately 16 months since genesis (November 2024), observing an annualized burn rate of about 32 million tokens. The AF obtains about 97% of trading fees through an automated buyback mechanism and also holds an additional 42.1 million HYPE awaiting destruction in its wallet. The historical burn rate includes periods when HYPE was in lower price ranges (most of 2025 being $10-25), meaning that every dollar of trading fees could retire more tokens.

At the current price of $37 and approximately $2 million in daily trading fees, the forward-looking annualized burn rate is closer to 19 million HYPE. In the model, we adopted this 19 million forward-looking estimate as the predictive benchmark, even though historical data of 32 million shows the AF's operation strength in low price environments. Importantly, AF burns and income are endogenously linked: in a strong market, higher fee revenue means significantly more tokens are bought back and destroyed. This creates a reflexive dynamic that static supply forecasts cannot fully capture.

The net effect is only a slight increase in the circulating supply. Starting from today’s approximately 300 million, the team unlocks about 1 million every month, plus the 10 million annual validator emissions, totaling an annual addition of about 22 million; while approximately 19 million are burned through AF each year. We predict about 302 million by the end of 2026, about 305 million by the end of 2027, and about 308 million by the end of 2028—resulting in a net increase of about 3 million each year. The buyback engine almost completely offsets new issuance, leading to an annual dilution rate of about 1%. The implied price of HYPE is calculated based on the projected supply in year 3.

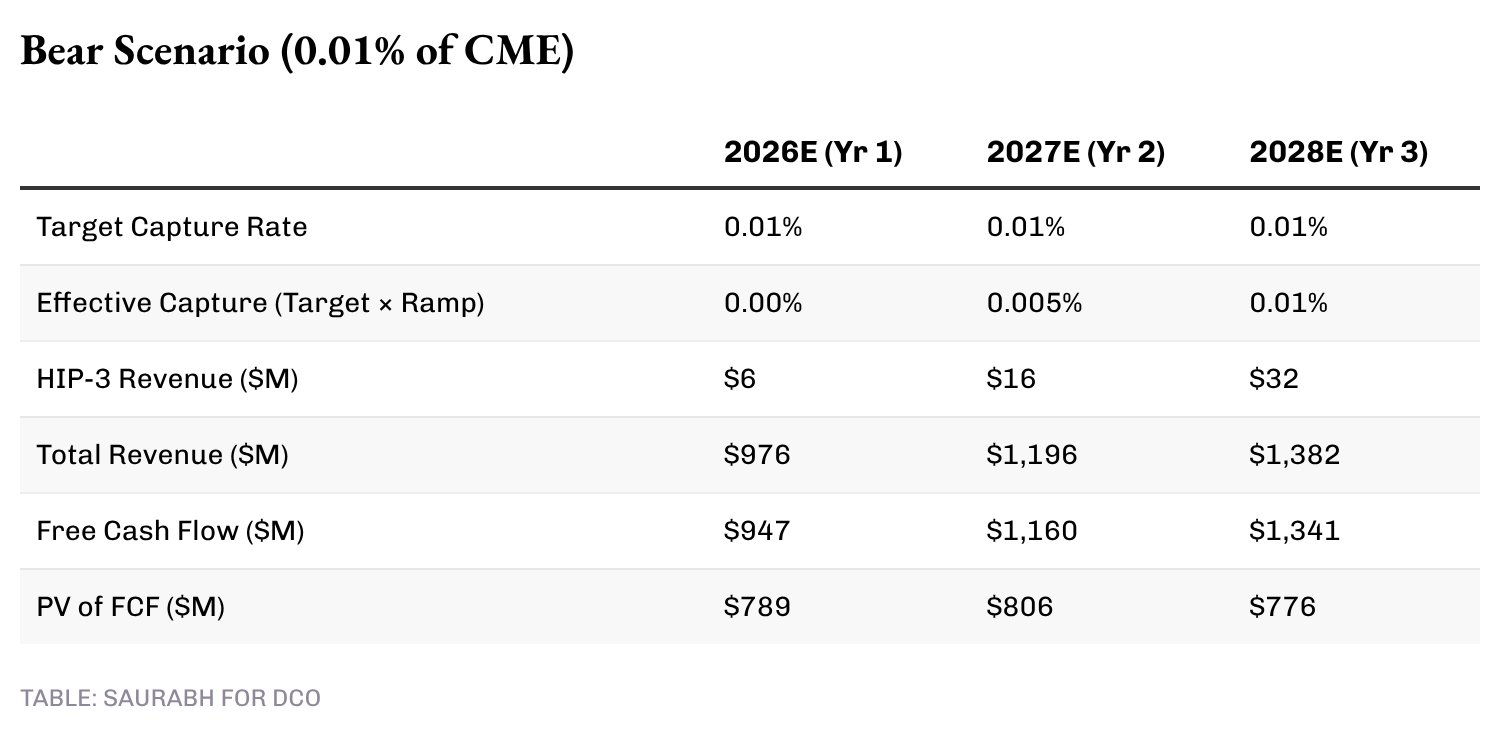

In a bear market scenario (capture rate 0.01%), HIP-3 generates $32 million in fees annually when operating at full speed in a TAM adjusted for conversion. Combined with the baseline revenue of $1.35 billion, the DCF gives an enterprise value of approximately $1.8 billion based on the terminal value from year 3 total revenue.

Corresponding to the year 3 supply of 308 million in the projections (a slight increase from today's 300 million), the implied HYPE price is about $60—still representing a significant premium over the current $37, indicating that even with extremely limited progress from HIP-3, the basic exchange economic logic alone could support higher prices.

In the baseline scenario (capture rate 0.10%), year 3 HIP-3 revenue reaches $322 million, with total revenue around $1.7 billion, corresponding to an enterprise value of about $2.2 billion, and an implied HYPE price of about $72.

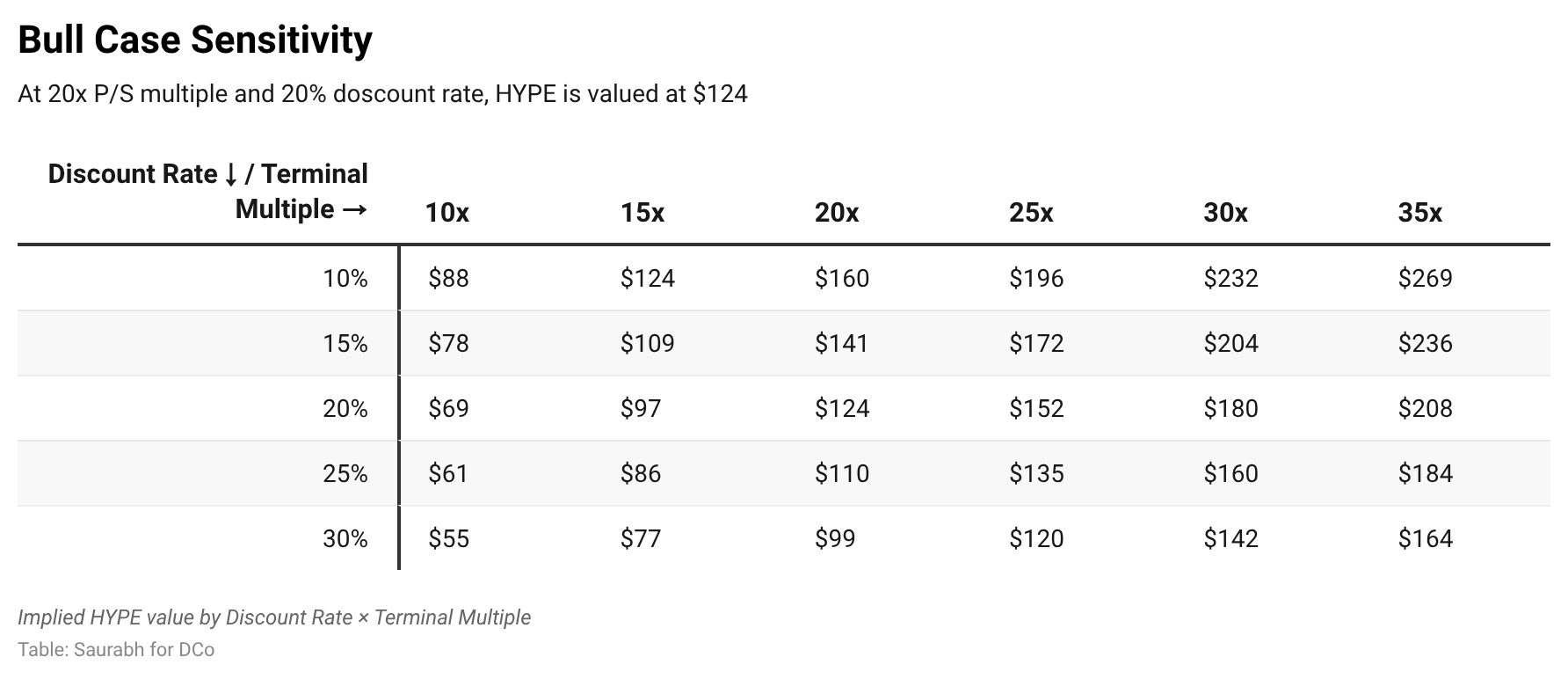

In a bull market scenario (capture rate 0.50%), year 3 HIP-3 fees reach $1.6 billion, total revenue $3 billion, enterprise value $3.8 billion, with an implied price of about $124, fully diluted valuation around $124 billion.

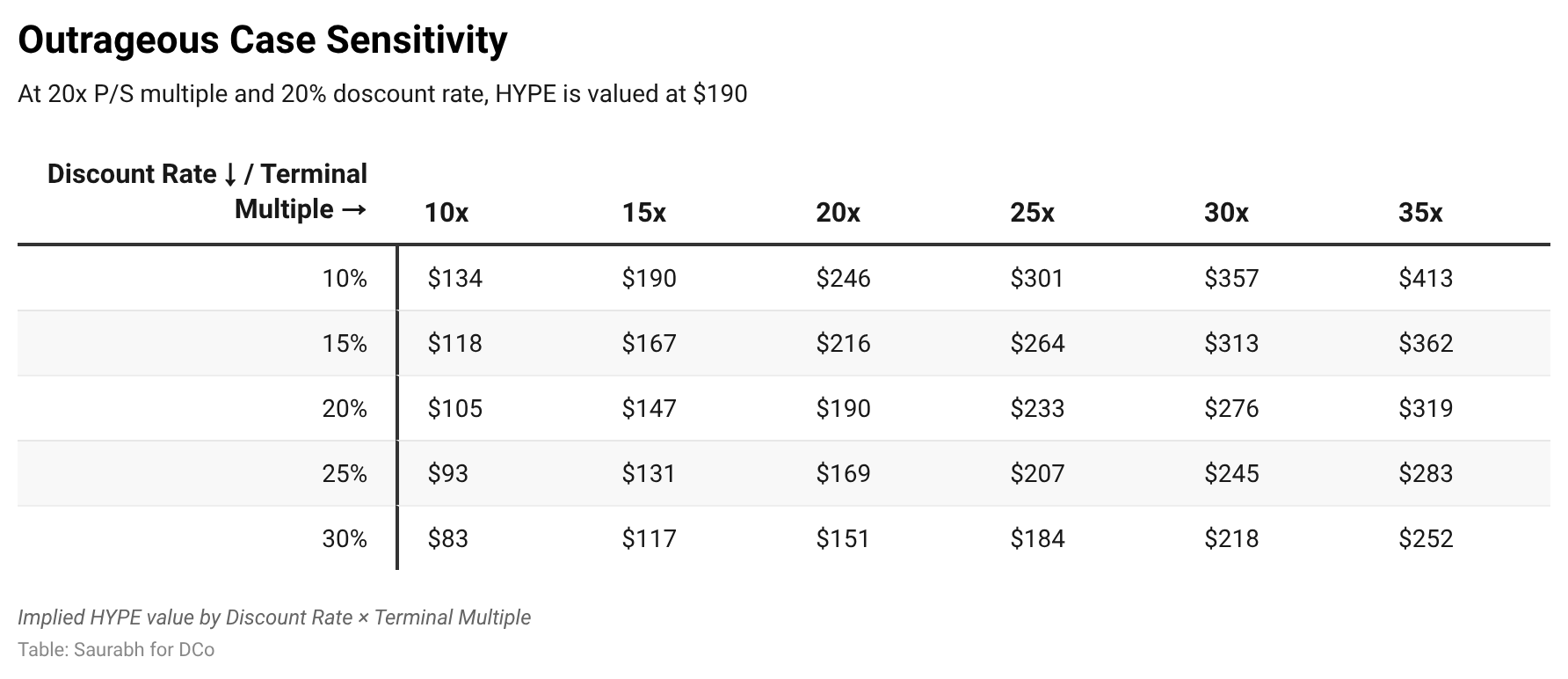

In an extreme scenario (capture rate 1.00%), year 3 total revenue reaches $4.6 billion, enterprise value $5.9 billion, HYPE approaching $190, with FDV approximately in the $190 billion range.

At this level, Hyperliquid’s price-to-sales ratio is about 13 times, still lower than CME’s current 17.5 times—indicating that the terminal multiple assumption is conservative for such a fast-growing business.

Under the default 20% discount rate and 20 times multiple, the current price of $37 is far below the bear market target price of $60, indicating the market has not priced in any meaningful contributions from HIP-3, and it can be claimed that even the basic crypto exchange business itself is undervalued. The benchmark target price of $72 implies about 93% upside from the current level, requiring only a capture of 0.10% of the addressable trading volume. Hayes' target price of $150 falls between our bull ($124) and extreme scenarios ($190), requiring a capture rate between 0.50% to 1.00%. Considering HIP-3 has only been online for five months and already accounts for about 10% of fee revenue, these three-year capture rate targets are ambitious but not baseless.

Why Hyperliquid and not Other Platforms

A natural question about the HIP-3 argument is: if traditional derivatives trading volume migrates on-chain, it could go anywhere. We believe this underestimates the inertia of liquidity concentration.

Looking at the competitive landscape, by the end of 2025, Lighter briefly surpassed Hyperliquid in 30-day perpetual contract volume while operating at zero fees and implementing one of the most aggressive incentive programs in the market. Subsequently, on December 30, $LIT's airdrop resulted in $250 million being withdrawn within 24 hours, and Lighter's volume collapsed to 8.1% market share within three weeks. Although Lighter still charges no fees, the trading volume returned to Hyperliquid. The moat lies in the depth of liquidity and execution quality, not in pricing. The ratio of open interest to trading volume confirms this: Hyperliquid is at 0.64 (capital retention), Aster at 0.18, Lighter at 0.12.

Now looking at centralized alternatives. Coinbase is preparing to launch compliant perpetual contracts, but consider the users: if you want to trade stock index or commodity exposure, you already have Robinhood, Schwab, and Interactive Brokers. Launching SPX perpetual contracts on Coinbase does not address the pain points of its users. Hyperliquid addresses a different problem: 24/7 settlement, no market hour restrictions, cross-margining with crypto assets, and permissionless listing. It complements the existing system rather than being a poor version of products already available in traditional institutions.

HYPE is Undervalued

Hyperliquid faces risks. HIP-3 needs stock index and commodity perpetual contracts to maintain trading volume after the novelty wears off. The 0DTE group needs sufficient reasons to switch from options to perpetual contracts, not just lower fees. The matching engine must perform as well at an average daily volume of $50 billion as it does at $8 billion. These are not existential risks. The core product is effective. The Iran war weekend proved that the market's demand for 24/7 commodity price discovery is real.

U.S. regulatory clarity on tokenized perpetual contracts is not a prerequisite for this argument. Hyperliquid’s volume is likely to come mostly from outside the U.S. But U.S. recognition or approval would only accelerate the growth of this category. Every dollar migrating from traditional derivatives to permissionless infrastructure expands the total addressable market, and Hyperliquid, with its depth of liquidity, execution quality, and market-making infrastructure, has the ability to capture a disproportionate share. HIP-4 introducing prediction markets and option-style contracts also opens up a new dimension of trading volume.

Currently, HYPE’s price-to-sales ratio is 10 to 13 times, while CME is at 25 times, ICE at 23 times, and CBOE at 22 times. Those are mature businesses with single-digit growth. Hyperliquid achieved revenue of $960 million in its first full year, with no debt, no personnel burdens, and a buyback mechanism that returns almost all fees to token holders. No traditional exchange can match this. We expect HYPE to be repriced as an exchange equity to reflect mixed multiples of crypto and traditional derivatives dual revenue. This means the current $37 HYPE is below its potential fair value.

This article is inspired by analysis previously published by @FalconXGlobal.

Disclaimer: DCo holds HYPE positions. This article does not constitute investment advice.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。