Author: Matt Brown

Translated by: TechFlow

TechFlow Guide: Matrix VC partner Matt Brown presents a counterintuitive argument: AI is making code cheaper, but it is making the truly hard-to-replicate things in Fintech—bank licenses, underwriting data accumulated from credit loss, and risk control models fed by real transaction volumes—more valuable than ever.

"You can't obtain a bank license through vibe coding," this statement encapsulates the core of the entire article.

This is not just an analysis of Fintech; it is a map of "which moats are tougher" in the AI era.

The full text is as follows:

The term "Fintech" has long relied on the ambiguity within its name for arbitrage.

"Fin" means from. A large quantity of emails from .gov domains, audits lasting months, compliance officers more familiar with your SAR filing history than you are, and business trips to Charlotte or Washington. "Tech" represents a refined mobile app, a tenfold user experience, and discussing investments over coffee at Blue Bottle.

"Fin" and "tech" have always been a lineage, but the market often rewards Fintech companies that resemble "tech" as much as possible and involve "fin" as little as possible.

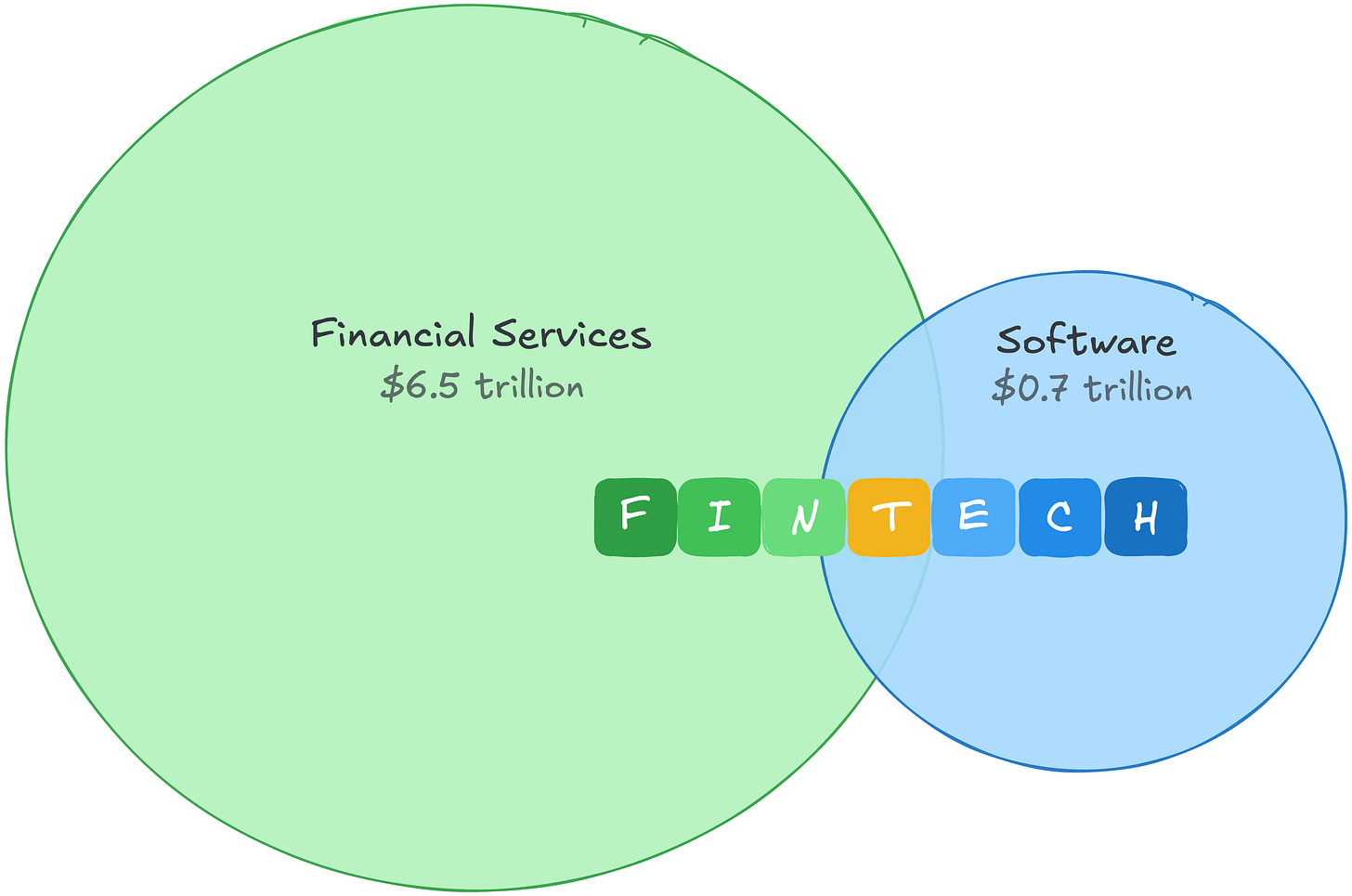

This is easy to understand. In 2021, the gross profit pool of software was about $0.7 trillion, enjoying a high premium. The gross profit pool of financial services is an order of magnitude larger but valued far more conservatively. Fintech allows you to arbitrage both ends: the economics of financial services paired with the valuation multiples of software companies.

The gap in this profit pool also tells you where the real money is. Financial services generate the most gross profit among all global industries. The "fin" side of Fintech is not only more defensive but also a much larger market.

Then AI arrived, and the arbitrage space vanished. As investors repriced "how much code is worth in an increasingly cheap code world," software valuations compressed. Fintech companies were categorized by the market as software companies and thus were also affected.

But the market misclassified them. The costs of Fintech and its moat have never been in the code, and in the face of AI-driven cost compression, they appear increasingly anti-fragile.

The story of two cost structures

Software once had one of the best business models in history: high costs of creating code, but once written, distribution is almost free. The gap between "expensive to build" and "free to distribute" is the profit margin. If you are a SaaS company, spending 22% to 25% of your revenue on R&D, that expenditure is also your barrier to entry. Competitors cannot easily replicate what took years and tens of millions of dollars to build.

AI has compressed this gap from the top. If code is cheap to build and cheap to distribute, profit margins will shrink. The wall that blocks competitors has lowered, more players enter the arena, and pricing power is thereby eroded.

If your business is software, this is a real issue. But Fintech's expenses are not engineering expenses. Follow the money, and the distinction quickly becomes apparent.

PayPal spends 9% of its revenue on R&D, while Block spends 12%. This is not because Fintech engineering is unimportant—Stripe's engineering capabilities are world-class and a real competitive advantage. Rather, most of the money does not flow to engineering.

The money flows to "fin." Unlike R&D expenses, these costs are not just product creation; they create a moat:

Credit losses buy underwriting data

Affirm spends 35% of its revenue on credit losses and funding costs before paying an engineer. Every bad debt loss is repayment data that competitors cannot access. A new entrant trains models with synthetic data and has no real benchmarks. Reliable loss histories cannot be established with synthetic data alone.

Compliance spending buys regulatory licenses

Wise allocates one-third of its employees to compliance and financial crime prevention across more than 65 regulatory licenses. Remittance licenses from all 50 states, BSA/AML compliance programs, and charter requirements. These are not advantages you build; they are licenses you continuously win. You can't obtain a bank license through vibe coding.

Transaction volume buys proprietary data

Toast's payment segment gross margin is about 22%, far below its SaaS segment's 70%, but the gross profit generated is nearly twice that of the latter. Those costs yield merchant-level transaction data, which in turn feeds Toast Capital, which has issued over $1 billion in loans. Adyen's risk models are trained on transaction patterns from over 30 markets.

Fintech's profit margins were never high, and that's the key

Payment companies have gross profit margins of 20% to 50%, rather than 80%. But low margins do not equate to weak businesses. Fintech has low margins because significant costs are creating compounding advantages. Even those costs that do not produce advantages are outside the range of AI-driven cost compression.

AI has strengthened each of these moats. Better models reduce loss rates, improved fraud detection decreases chargebacks, and enhanced compliance tools enable smaller teams to hold more licenses. AI will not replace moats; it rewards those that choose to build in the hardest areas of Fintech: capital flow, risk assumption, proprietary data, and regulation.

So the real argument is not just "AI helps Fintech," but that AI shifts value from product surface area to proprietary data, risk assumption, regulatory licenses, and embedded channels of real capital flow. If you build in these areas, AI compounds in your favor. If your differentiation lies in code, AI compounds against you.

Demand is also steadily increasing. Every vibe-coded checkout process is a new vector for fraud, and every self-trading AI agent carries chargeback risk. The more built on Fintech infrastructure, the more indispensable that infrastructure itself becomes.

"Fin" is the real winner

This realization has begun to force smart Fintech founders to rethink their position in the "fin" and "tech" lineage:

Are we assuming and pricing risks ourselves or passing them to partners and letting them take the profits?

Do we have regulatory relationships, or are we renting them from those who do?

Is each transaction making our own risk models more accurate, or training others' models?

Is our ledger the source of real data, or an incomplete mirror of others' ledgers?

This distinction divides the Fintech landscape into two. Companies that have regulatory relationships, assume credit losses, and accumulate transaction data are building moats that AI will deepen. Those renting "fin"—using the licenses of partner banks, the ledgers of BaaS providers, and others' risk models wrapped with better interfaces—face exactly the same issues as SaaS companies. Their differentiation lies in code, and code has just become cheaper.

The old arbitrage of applying software valuation multiples to financial services economics is dead. The new arbitrage is simpler: own the "fin."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。