Author: Colossus

Translation: Deep Tide TechFlow

Deep Tide Introduction: This article exposes an uncomfortable fact using data from the American government: over the past 30 years, all the best-selling entrepreneurial methodologies—lean startup, customer development, business model canvas—have statistically shown no help in improving the survival rates of startups.

The problem may not necessarily be that the methodologies themselves are wrong, but once everyone is using the same strategies, it loses its advantage.

This argument applies equally to cryptocurrency and Web3 entrepreneurs, particularly worth reading for those looking at various "Web3 entrepreneurship guides."

The full text is as follows:

Whenever a method for building startups is widely disseminated, it causes founders to converge on the same answers. If everyone follows the same best-selling entrepreneurial techniques, everyone will eventually build the same kinds of companies, and without differentiation, most of these companies will fail. The fact is, whenever someone insists on teaching a method to build a successful startup, you should do the opposite. This paradox becomes clear once understood, but it also contains the direction for progress.

Before the new wave of "startup evangelists" emerged twenty-five years ago, the set of entrepreneurial advice they replaced was, frankly, worse than useless. That advice was a naive mix of Fortune 500 company strategies and small business tactics, running parallel with five-year plans and daily operations management. But for startups with high growth potential, long-term planning is meaningless— a future that is unpredictable, and focusing on daily operations exposes founders to faster competitors. The old advice was built for a world of incremental improvements, not fundamental uncertainties.

The new generation of startup evangelists offers different advice: it is intuitive and reasonable, claims of sufficient evidence provide founders with a step-by-step process to build businesses amid real uncertainties. Steve Blank introduced customer development in "The Four Steps to the Epiphany" (2005), teaching founders to view business ideas as a set of falsifiable hypotheses: get out there, interview potential customers, and verify or refute your hypotheses before writing any code. Eric Ries built on this foundation in "The Lean Startup" (2011), proposing the build-measure-learn loop: publish a minimum viable product, measure real user behavior, iterate quickly, rather than wasting time refining a product that nobody wants. Osterwalder’s business model canvas (2008) provides founders with a tool to outline nine core components of a business model and quickly adjust when any part does not work. Design thinking—promoted by IDEO and Stanford's design school—emphasizes empathy with end users and rapid prototyping to uncover problems early. Saras Sarasvathy's effectuation theory suggests starting from the founder's own skills and connections, rather than reverse-engineering a plan to achieve lofty goals.

These evangelists consciously attempt to establish a science of entrepreneurial success. By 2012, Blank stated that the National Science Foundation in the U.S. referred to his customer development framework as "the scientific method of entrepreneurship," claiming "we now know how to make startups fail less." The Lean Startup website claims "lean startup provides a scientific approach to creating and managing successful startups," and the book's back cover quotes IDEO CEO Tim Brown, stating Ries "has proposed a scientifically based process that can be learned and replicated." Meanwhile, Osterwalder, in his doctoral thesis, claims the business model canvas is grounded in design science (the precursor to design thinking).

The academic study of entrepreneurship is also research-focused, but their science is closer to anthropology: describing the cultures of founders and the practices of startups in hopes of understanding them. The new generation of evangelists has a more practical vision—something that natural philosopher Robert Boyle articulated during the initial blossoming of modern science: "I dare not call myself a true natural philosopher unless my skill enables my garden to grow better herbs and flowers." In other words, science should pursue fundamental truths but must also be effective.

Whether it is effective, of course, determines whether it is worthy of being called science. And when it comes to entrepreneurship evangelism, one thing we can be sure of is: it hasn't worked.

What have we actually learned?

In science, we use experiments to judge whether something is effective. As Einstein's theory of relativity gradually gained acceptance, other physicists spent time and money designing experiments to test whether its predictions held up. We learned in elementary school that the scientific method is science itself.

However, due to some defect in our human nature, we also tend to resist the idea that "truth is discovered in this way." Our minds expect evidence, but our hearts need to be told a story. There is an ancient philosophical position—discussed brilliantly by Steven Shapin and Simon Schaffer in "Leviathan and the Air Pump" (1985)—that argues observation alone cannot give us the truth, and that real truth can only be logically derived from other things we know to be true, i.e., starting from first principles. While this standard holds in mathematics, in fields where data is a bit noisy or the axiomatic foundations are less solid, it can lead to seemingly enticing yet absurd conclusions.

Before the sixteenth century, doctors treated patients using the writings of the second-century Greek physician Galen. Galen believed diseases were caused by an imbalance of four bodily humors—blood, phlegm, yellow bile, and black bile—and recommended therapies such as bloodletting, inducing vomiting, and cupping to restore balance. Doctors followed these therapies for over a thousand years, not because they were effective, but because the academic authority of the ancients seemed far superior to the value of contemporary observation. However, around 1500, Swiss doctor Paracelsus noticed that Galen's therapies did not actually improve patients and that some treatments—like using mercury to treat syphilis—while nonsensical within the humor theory, actually worked. Paracelsus began to advocate for listening to evidence rather than adhering to long-dead authorities: "The patient is your textbook; the bedside is your study." In 1527, he even publicly burned Galen's writings. His vision took centuries to be accepted—nearly three hundred years later, George Washington died after a radical bloodletting treatment—because people favored the neat, simple narratives of Galen over the messy complexity of reality.

Paracelsus started from what was effective, tracing the roots to find the cause. First principles thinkers assume a "cause" first and then insist it works regardless of the outcome. Our modern entrepreneurial thinkers are more like Paracelsus, driven by evidence, or more like Galen, sustaining themselves with elegant coherence of their stories? In the name of science, let’s look at the evidence.

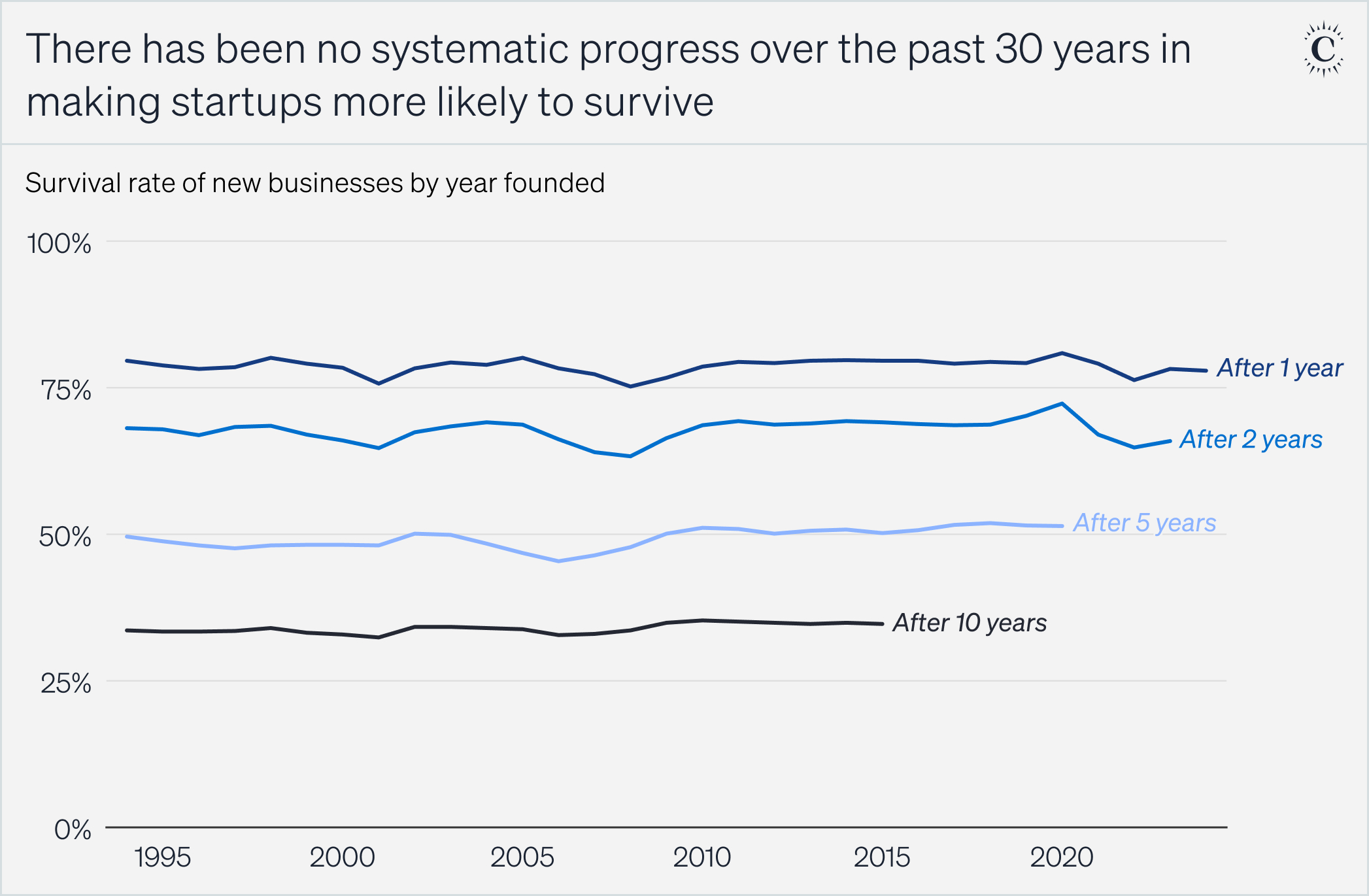

Here are the official government data on the survival rates of American startups. Each line shows the probability of a company founded in a certain year surviving. The first line tracks the one-year survival rate, the second line tracks the two-year survival rate, and so on. The chart shows that from 1995 to now, the proportion of companies surviving one year has barely changed. The two-year, five-year, and ten-year survival rates are the same.

The new generation of evangelists has been around long enough and is well-known enough—relevant book sales total millions, and almost all university entrepreneurship courses teach these ideas. If they were effective, there would be evidence in the statistics. However, in the past thirty years, there has been no systemic improvement in making it easier for startups to survive.

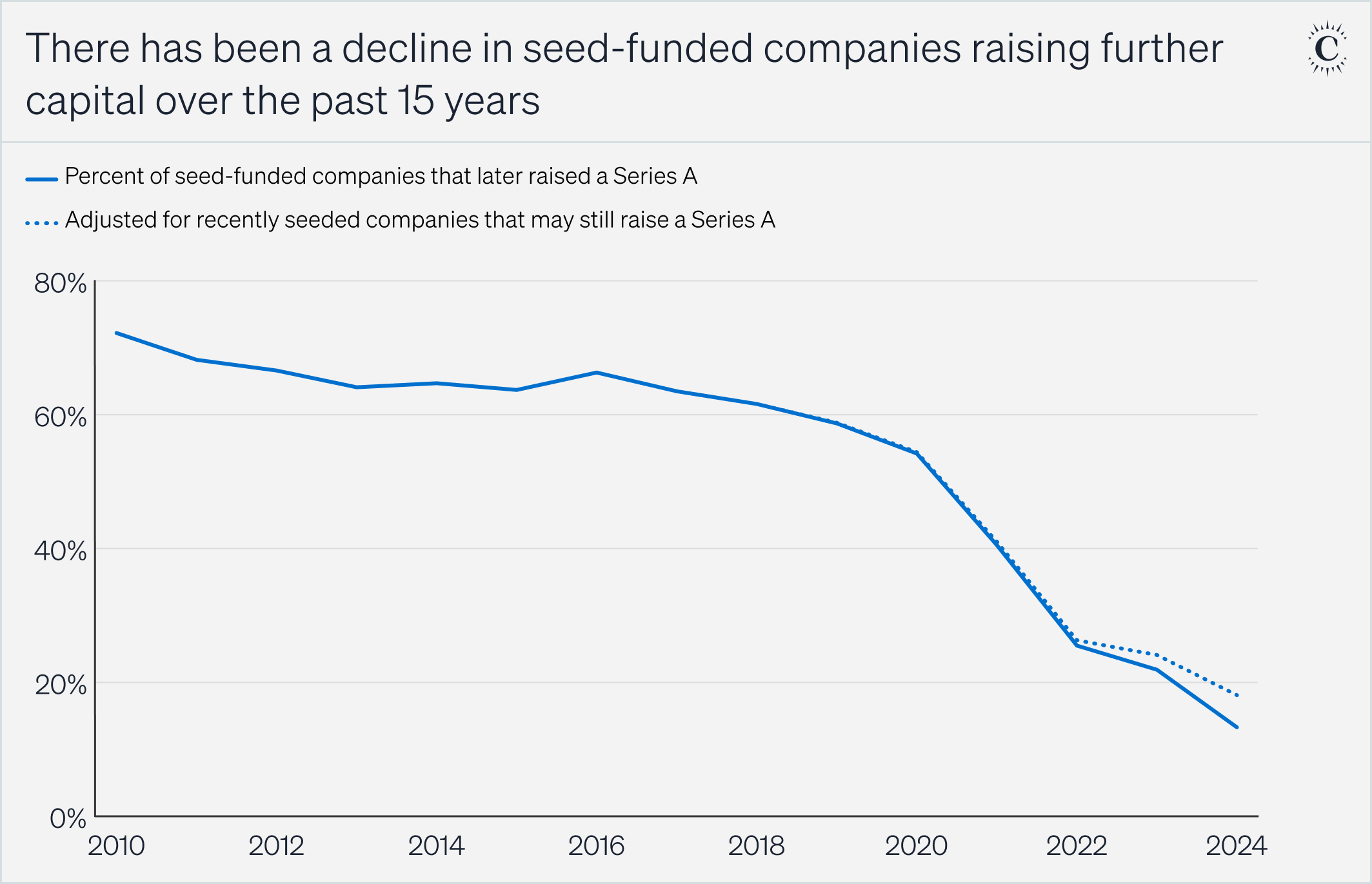

The government data counts all American startups, including restaurants, dry cleaners, law firms, and landscape design companies—not just venture-capital-backed, high-growth potential technology startups. The entrepreneurship evangelists have not claimed that their methods only apply to Silicon Valley-type companies, but these techniques are most often tailored to that extreme uncertainty that founders are only willing to undertake when potential rewards are sufficiently large. Therefore, we adopt a more targeted metric: the proportion of U.S. venture-backed startups that continue to complete follow-on funding rounds after completing their initial financing. Given how venture capital works, we can reasonably assume that most companies that fail to complete follow-on funding did not survive.

The solid line represents raw data; the dashed line adjusts for recent seed-stage companies that may still complete Series A funding.

The proportion of seed-stage companies continuing to complete follow-on funding has sharply declined, which does not support the claim that venture-backed startups have become more successful over the past 15 years. If there has been any change, they seem to have failed even more frequently. Of course, venture capital deployment is not solely determined by the quality of the startups: shocks from the pandemic, the end of the zero-interest-rate era, and the concentrated capital demands of AI, etc.

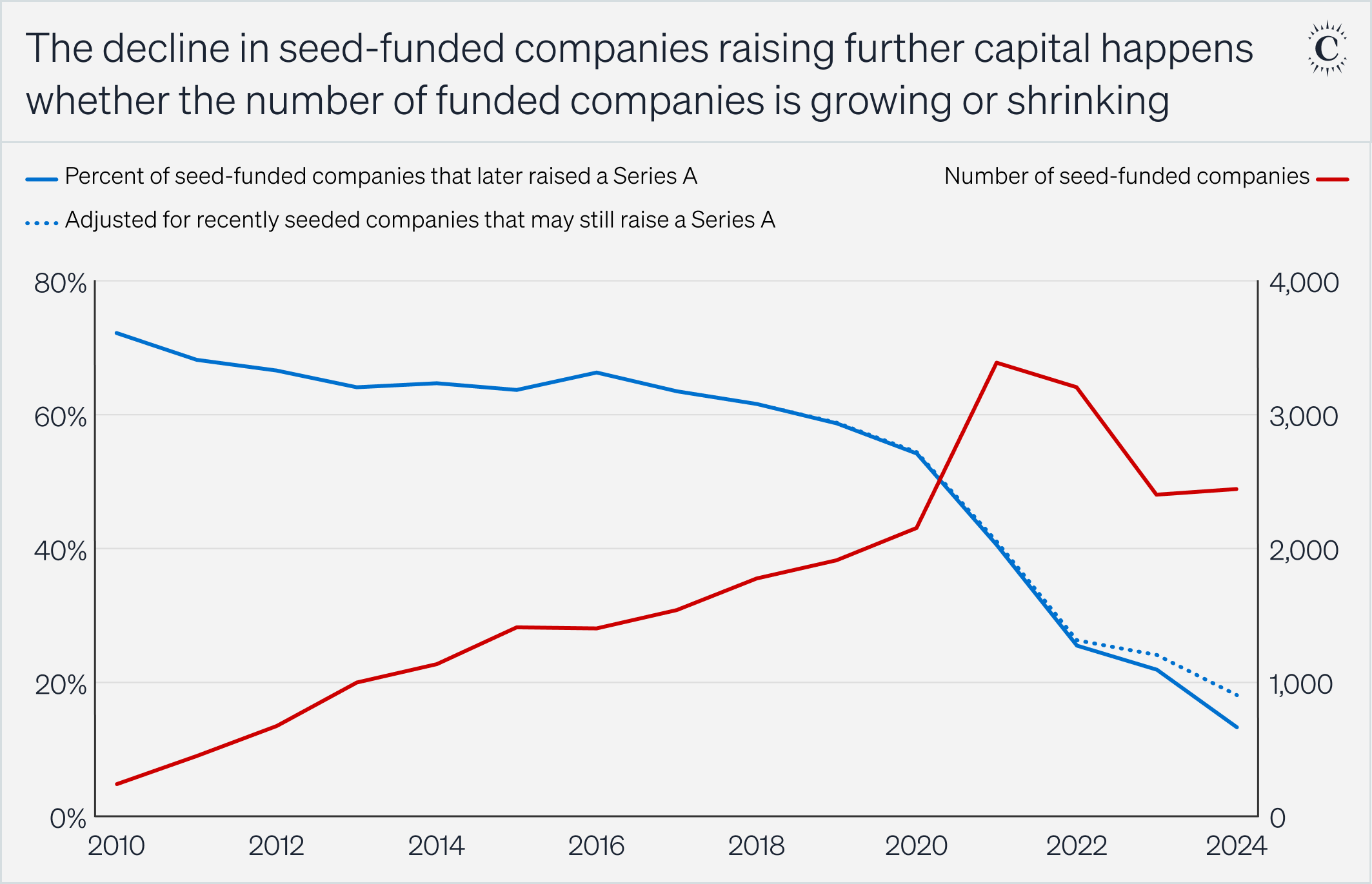

People might argue that the overall increase in venture capital has flooded the market with more underqualified entrepreneurs, offsetting any rise in success rates. However, in the chart below, the decline in success rates occurs during both periods of increasing and decreasing numbers of funded companies. If an oversupply of underqualified founders was dragging down the average, then when the number of funded companies dropped after 2021, the success rate should have rebounded. It did not.

But isn’t the increasing number of founders itself a sign of success? Try telling that to entrepreneurs who followed the evangelists' advice and ultimately failed. These are real people who risked their time, savings, and reputations; they have the right to know what they are up against. Top venture capitalists may have made more money—there are now more unicorns than ever—but part of this is due to longer exit times and part is due to the power law distribution of exits mathematically meaning that the more companies start, the higher the probability of extreme successes. For founders, this is a cold comfort. The system may be generating more big winners, but it hasn’t improved the odds for individual entrepreneurs.

We must seriously confront the fact that the new generation of evangelists has failed to make startups more likely to succeed. The data indicates in the best case, they have had no impact at all. We have spent an incalculable amount of time and billions of dollars on a fundamentally unworkable conceptual framework.

Toward a science of entrepreneurship

Evangelists claim they are giving us a science of entrepreneurship, but by the standards they themselves have set, we have made no progress: we do not know how to make startups more successful. Boyle would say that if our garden has not yet grown better herbs or flowers, then there is no science. This is disappointing and perplexing. Given the time invested, widespread adoption, and the evident intellectual caliber behind these ideas, it seems hard to imagine they are utterly ineffective. Yet the data suggests we have indeed learned nothing.

If we want to construct a true science of entrepreneurship, we need to understand the reasons why. There are three possibilities. First, perhaps these theories are simply wrong. Second, perhaps these theories are too obvious for systematization to be meaningful. Third, perhaps once everyone uses the same theories, they no longer confer any advantage. After all, the essence of strategy is to do things differently from competitors.

Perhaps the theories themselves are wrong

If these theories are simply wrong, then their widespread adoption should have led to a decline in entrepreneurial success rates. Our data suggests this is not the case for overall startups, whereas the failure rate of venture-backed companies appears to have risen for other reasons. Setting data aside, these theories do not appear to be wrong. Talking to customers, conducting experiments, and constant iteration all seem obviously beneficial. But Galen's theories also did not seem wrong to doctors in the year 1600. Unless we test these frameworks like we test other scientific hypotheses, we cannot be sure.

This is the standard set by Karl Popper in "The Logic of Scientific Discovery": a theory is scientific if and only if it can, in principle, be proven wrong. You have a theory, you test it. If experiments do not support it, you discard it and try something else. A theory that cannot be falsified is not a theory at all, but a belief.

Few have attempted to apply this standard to entrepreneurship research. There are a few randomized controlled trials, but they often lack statistical power and define "effectiveness" in ways that differ from what true success for startups would be. Given that venture capital bets billions of dollars every year, not to mention the years of time that founders invest in testing their ideas, it seems strange that no one has seriously attempted to verify whether what startups are taught to use is genuinely effective.

But evangelists have little incentive to test their theories: they profit from selling books and accumulating influence. Startup accelerators profit by sending large numbers of entrepreneurs into a power law funnel, reaping a handful of extraordinarily successful cases. Academic researchers face their own perverse incentives: proving their theories wrong would cause them to lose funding, with no compensatory return. The entire industry has the structure that physicist Richard Feynman describes as "cargo cult science": a building that mimics the form of science but lacks its substance, deriving rules from anecdotes rather than establishing fundamental causal relationships. Just because a handful of successful startups conducted customer interviews does not mean that your startup will succeed if it does the same.

However, unless we acknowledge that existing answers are insufficient, we will have no motivation to pursue new answers. We need to discover through experimentation what works and what does not. This will be costly because startups are poor test subjects. It is hard to compel a startup to do something or refrain from doing something (can you stop founders from iterating, or talking to customers, or asking users what design they prefer?), and when companies are fighting for survival, keeping strict records is often a low priority. Each theory also has numerous subtleties that need to be tested. In practice, these experiments may not be performed well at all. But if that is the case, then we need to admit what we would say without hesitation about any other unfalsifiable theory: this is not science, but pseudoscience.

Perhaps the theories are too obvious

To some extent, founders do not need to formally learn these techniques. Long before Blank proposed "customer development," founders were already developing customers by talking to them. Similarly, they had already been building minimum viable products and iterating before Ries named this practice. They had already been designing products for users before anyone called it "design thinking." The natural laws of business often compel these behaviors, and millions of business professionals have independently reinvented these practices to address the problems they face daily. Perhaps these theories are obvious, and the evangelists are merely putting old wine in new bottles.

This is not necessarily a bad thing. Holding effective theories, even if they are obvious, is the first step toward better theories. Contrary to Popper, scientists do not simply discard a promising theory the moment it is proven wrong; they seek to refine or expand it. Historian and philosopher of science Thomas Kuhn powerfully articulated this idea in "The Structure of Scientific Revolutions": after Newton published the theory of gravity, its predictions about the motion of the moon were incorrect for over 60 years until mathematician Alexis Clairaut recognized it as a three-body problem and corrected it. Popper's standard would have led us to discard Newton. But this did not happen because the theory was sufficiently supported in other respects. Kuhn argued that scientists are stubborn within a framework of beliefs that he called a paradigm. Because it provides a structure that allows scientists to build and improve upon existing theories, scientists will not easily abandon a paradigm unless absolutely necessary. Paradigms provide a path forward.

Entrepreneurship research lacks a paradigm. Or rather, it has too many paradigms, none of which are convincing enough to unify the entire field. This means that for those who want to think of entrepreneurship as a science, there is no common guide to direct which questions are worth solving, what observations mean, or how to improve those theories that are not entirely correct. Without a paradigm, researchers are just spinning their wheels and talking past each other. To become a science, entrepreneurship needs a dominant paradigm: a sufficiently compelling set of ideas that can organize collective efforts under a common framework. This is a more challenging question than simply deciding to test theories because, for a set of ideas to become a paradigm, it must answer some pressing open questions. We cannot achieve this out of thin air, but we should encourage more people to try.

Perhaps the theories are self-defeating

Economics tells us that if you are doing the same things as everyone else—selling the same products to the same customers, using the same production processes and the same suppliers—competition will drive your profits toward zero. This concept is the cornerstone of business strategy, from George Soros's theory of "reflexivity"—whereby the beliefs of market participants change the market itself, eroding the advantages they attempt to exploit—to Peter Thiel's Schumpeterian assertion that "competition is for losers." Michael Porter encoded this necessity in his landmark "Competitive Strategy" by identifying the need to find an unoccupied market position. Kim, Mauborgne, and René Moboigné advanced this idea in their "Blue Ocean Strategy," asserting that businesses should create completely uncontested market space rather than compete in existing arenas.

However, if everyone is using the same methods to build their companies, they will typically compete directly. If every founder is interviewing customers, they will converge on the same answers. If every team is releasing minimum viable products and iterating, they will ultimately iterate toward the same final product. Success in a competitive market must be relative, which means effective practices must be distinct from what everyone else is doing.

The method of reductio ad absurdum makes this evident: If there existed a flowchart that guarantees the success of a startup, people would be churning out successful startups around the clock. It would be a perpetual money machine. But in a competitive environment, the sheer number of new companies emerging results in most failing. The flawed premise must be that such a flowchart could exist.

There is an exact analogy in evolutionary theory. In 1973, evolutionary biologist Leigh Van Valen proposed what he termed the Red Queen hypothesis: in any ecosystem, when a species evolves advantages at the expense of another species, the disadvantaged species will evolve to offset that improvement. The name comes from Lewis Carroll's "Through the Looking-Glass," where the Red Queen tells Alice, "You must run as fast as you can just to stay in place." Species must constantly innovate with a multitude of diverse strategies to survive against the innovative strategies of competitors.

Similarly, when new entrepreneurial methods are swiftly adopted by everyone, no one gains a relative advantage, and the success rate remains flat. To win, startups must develop novel differentiated strategies and establish sustainable barriers to imitation before competitors catch up. This often means that the winning strategies are either internally developed (rather than found in publicly available publications that anyone can read) or so unique that no one would think to replicate them.

This sounds like a daunting task for establishing a science...

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。