Written by: Thejaswini MA

Translated by: Plain Blockchain

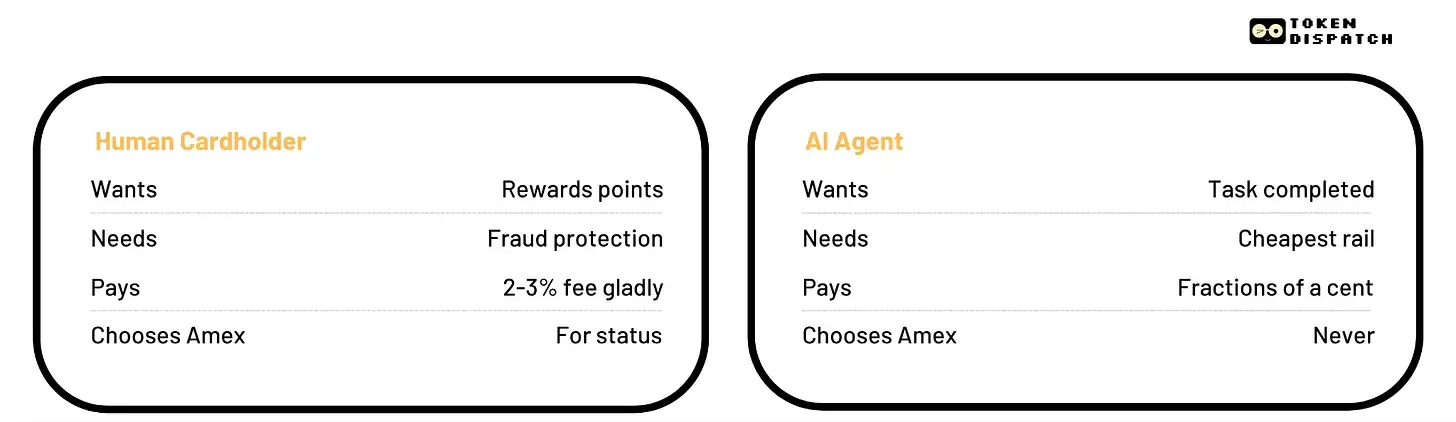

The entire Visa business is a bet on behavior. It involves human consumption habits and psychology. The reward points you accumulate, the human reward protections you rely upon, the coveted American Express Centurion Card, and the "zero" liability policy that makes you feel secure when withdrawing cash from ATMs abroad—these exist not because "moving money" is so difficult, but because humans are anxious, status-driven, and not good at reading terms and conditions. Visa has built a $500 billion company on this tower.

However, AI entities lack all of these traits.

They do not collect points, are not safer due to fraud protection, and do not pursue black cards. They have only one directive: complete any task. When tasks involve payments, intelligent interfaces perform the calculations that people are too lazy to do: the cheapest route, the fastest settlement, the lowest fees. Each time, it is done automatically, unemotionally, and with precision.

2028 Global Intelligence Crisis

Last month, an article titled "2028 Global Intelligence Crisis" on SubStack caused Visa's stock to drop by 4%, Mastercard by 6%, and American Express by 12%. Although the report referred to it as a "scenario imagining" rather than a prediction, the market did not buy it. The technological statement itself is not what matters; the core issue is that by 2027, AI entities will reroute through the Tokyo system (swapping) to settle using stablecoins. Visa took fifty years to craft the perfect product for a customer base that is being replaced.

In "machine-to-machine" (M2M) commerce, the 2-3% card swipe fee (interchange rate) is an extremely obvious attack target. As Citrini Research stated: this does not mean AI will destroy Visa tomorrow; it means that the fee structure that built Visa's empire is essentially a tax on "human irrationality," while the entities are perfectly rational beings. That is their significance.

What is Visa Selling?

To understand why this is crucial, you must understand what fees really are. When you use a credit card to buy something, the merchant pays a fee of 2-3% to the card organization and the issuing bank. Earlier money paid for your reward points, gift protection, shopping insurance, and dispute resolution services. The whole consumer value of credit cards is agreed to be funded by purchasing, and merchants pass costs back through slightly increased prices. A beautiful and stable system that has run for fifty years has all of this paid for by the human being in the transaction; they just are willing not to do it directly.

AI entities do not need these things. They do not initiate disputes and do not require cash back. The protections that underpin fees are essentially defenses against human error, human fraud, and alarms. Once humans are removed from the transaction, these fees entirely lose their value.

American Express is the most typical embodiment of this issue. Its customers are elite groups with high income, high spending, and a pursuit of status. Its rates are higher than those of Visa or Mastercard because the customers are willing to pay for privileged status and identity. The whole model assumes a conscious purchase behavior, as individuals choose American Express over Visa for lounge access. But the entity will not choose American Express; the entity targets the high-end crowd for the cheapest options to complete tasks. In the world of software cardholders, so-called tiers do not exist at all.

Business driven by entities circumventing fees poses a huge threat to banks and single-issue issuers dependent on rewards. A large portion of these institutions' profits comes from the 2-3% fees and entire business segments are built around owning independent rewards programs. Visa and Mastercard may have the networks to transform, but issuers that have constructed their profit and loss models entirely on fees and reward points will be left with no way forward.

Weekly Accumulated Shipment Volume

The report from Citrini coincides with the dense infrastructure being published in the same three-week window.

Tempo launched on the mainnet on Wednesday. This is a payment blockchain co-launched by Stripe and Paradigm, designed for high-frequency stablecoin settlements.

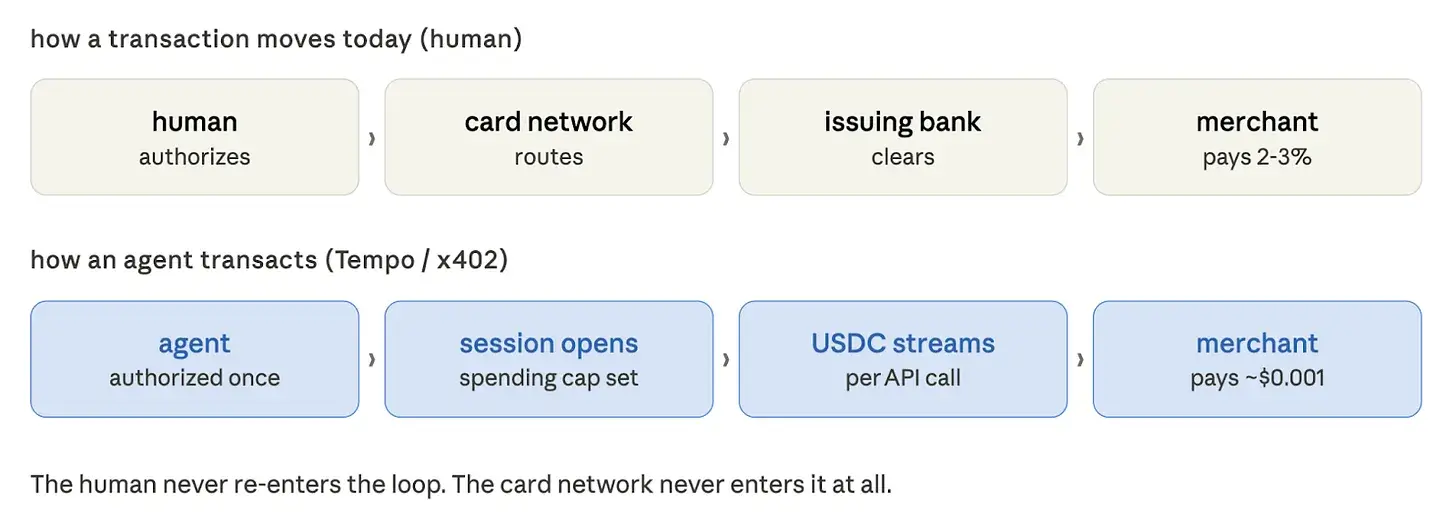

Also launched was the Machine Payments Protocol, an open standard that allows AI entities to autonomously pay while consuming human confirmations at every step. This protocol introduces a "session" model: humans authorize a single spending limit, and the entity continues to make streaming micropayments while consuming data, computing, or API calls. This is comparable to "money's version of OAuth." Authorization layout, entity spending, each step consumes swipe.

Anthropic, DoorDash, Mastercard, Nubank, OpenAI, Ramp, Revolut, Shopify, Standard Chartered, and Visa have all been default partners for Tempo. The entire stack of payment business recognizes this structural change.

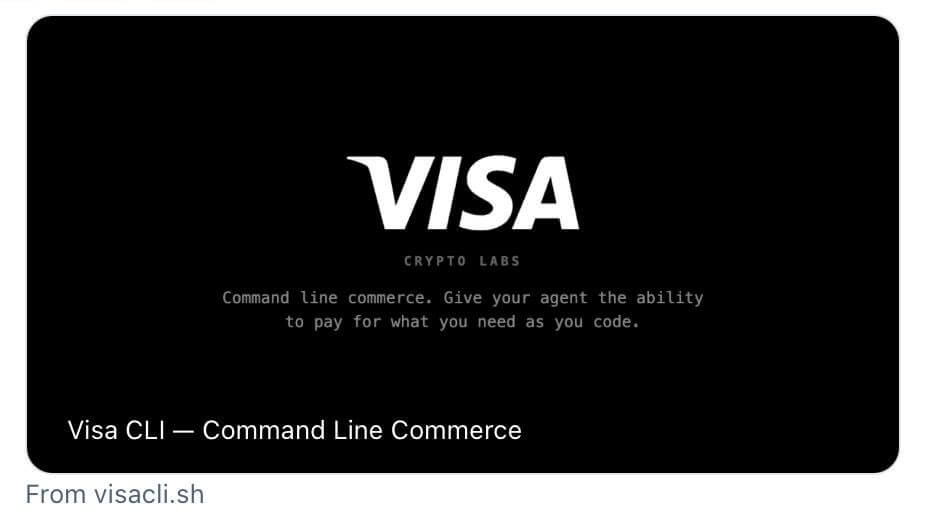

On the same day Tempo launched, Visa's crypto division released a command line interface (CLI) tool aimed at AI entities. Entities can make payments directly in the terminal without API switches, without accounts, and without human authorization for single transactions. Visa calls it "Command Line Commerce"—machines transact without human intervention.

Additionally:

Mastercard agreed to acquire the stablecoin infrastructure company BVNK for $1.8 billion.

Circle has launched a trial of Nano payments online. Sub-divisional, zero Gas fee USDC transactions are designed for AI entities to pay for this API call.

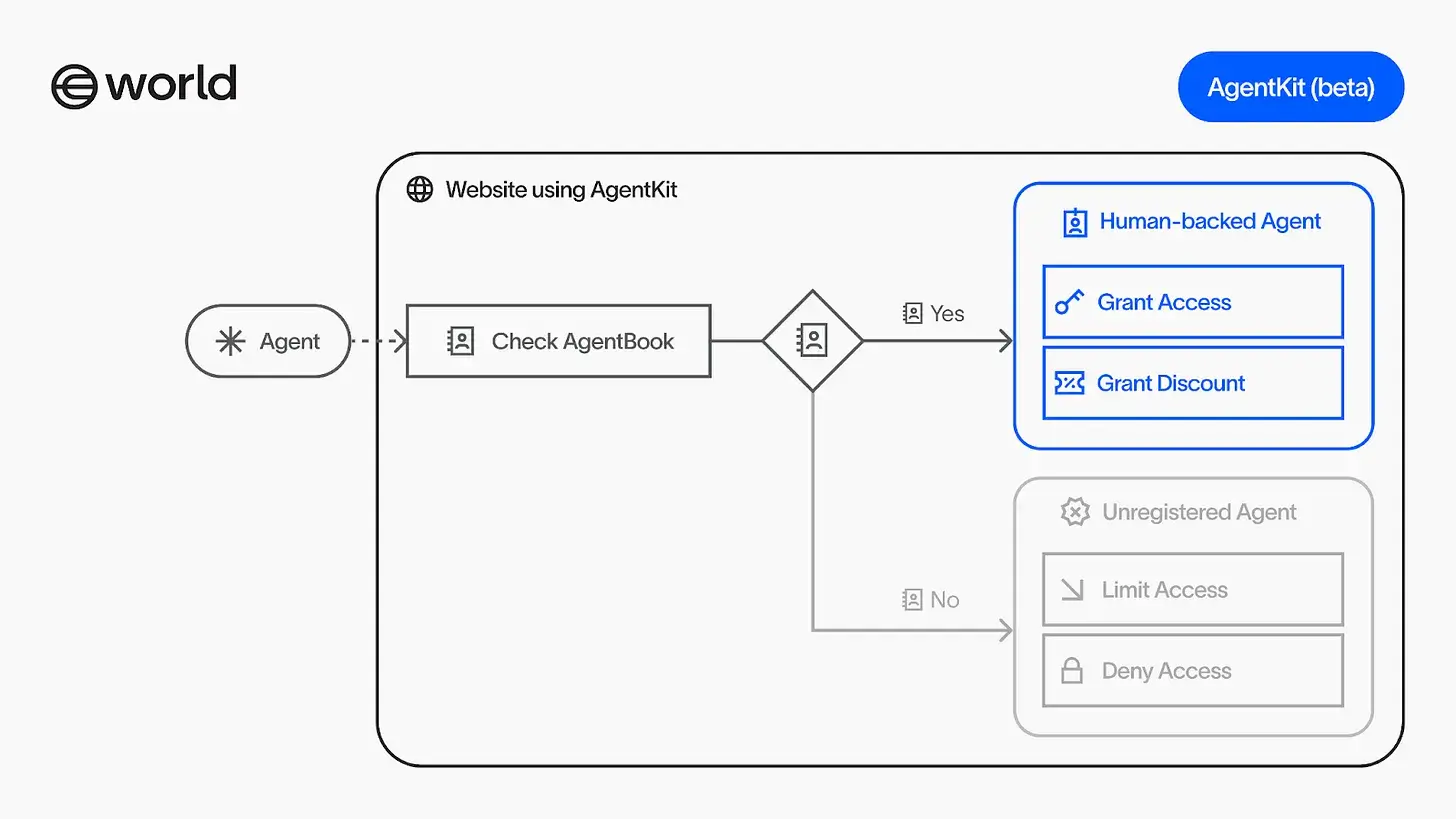

Sam Altman's world project (originally Worldcoin) launched AgentKit, allowing entities to demonstrate their representation of real humans using cryptographic technology and directly integrate into Coinbase's payment rails.

In my opinion, what happened this week is that companies are racing to become the new Visa, because Visa realizes it has lost everything.

The Obedience of Origins Theory

Now, it has not been pointed out clearly: Visa is not sitting idly by.

It is involved in the Tempo machine payments protocol and has established the Visa Crypto Lab, where the head of its crypto division explained in Fortune magazine how entities can make payments using synchronized rails through new standards. Mastercard's $1.8 billion layout for stablecoins, and Stripe acquiring Bridge and Privy. Legacy organizations understand this shift and are embedding themselves in the new infrastructure ahead of the full arrival of technology.

Visa's argument is: it can expand its own rails to cover entity transactions before building new rails that make Visa connections irrelevant.

The argument is not currently flawed. Stripe reached a figure of $19 trillion by 2025 (a 34% year-over-year increase). The channel advantages (distribution advantages) of card organizations are difficult to replicate. But I must admit, I am less willing to vocalize this viewpoint, because historically, as soon as someone does, a new product comes along and makes you look foolish.

The flaw in this argument lies in Visa's channel advantages being built on merchant relationships and consumer trust. Merchants accept Visa because consumers hold Visa; consumers hold Visa because merchants accept it. At the core of the entire flywheel is "humans in the transaction." Once entities become core buyers in certain important commercial categories, the flywheel will terminate. Entities have no brand loyalty, no wallets; what they have are layouts and directives. Whichever rails are cheapest and fastest win their business, and the switching costs are very clear.

The Gap Between Data and Narrative

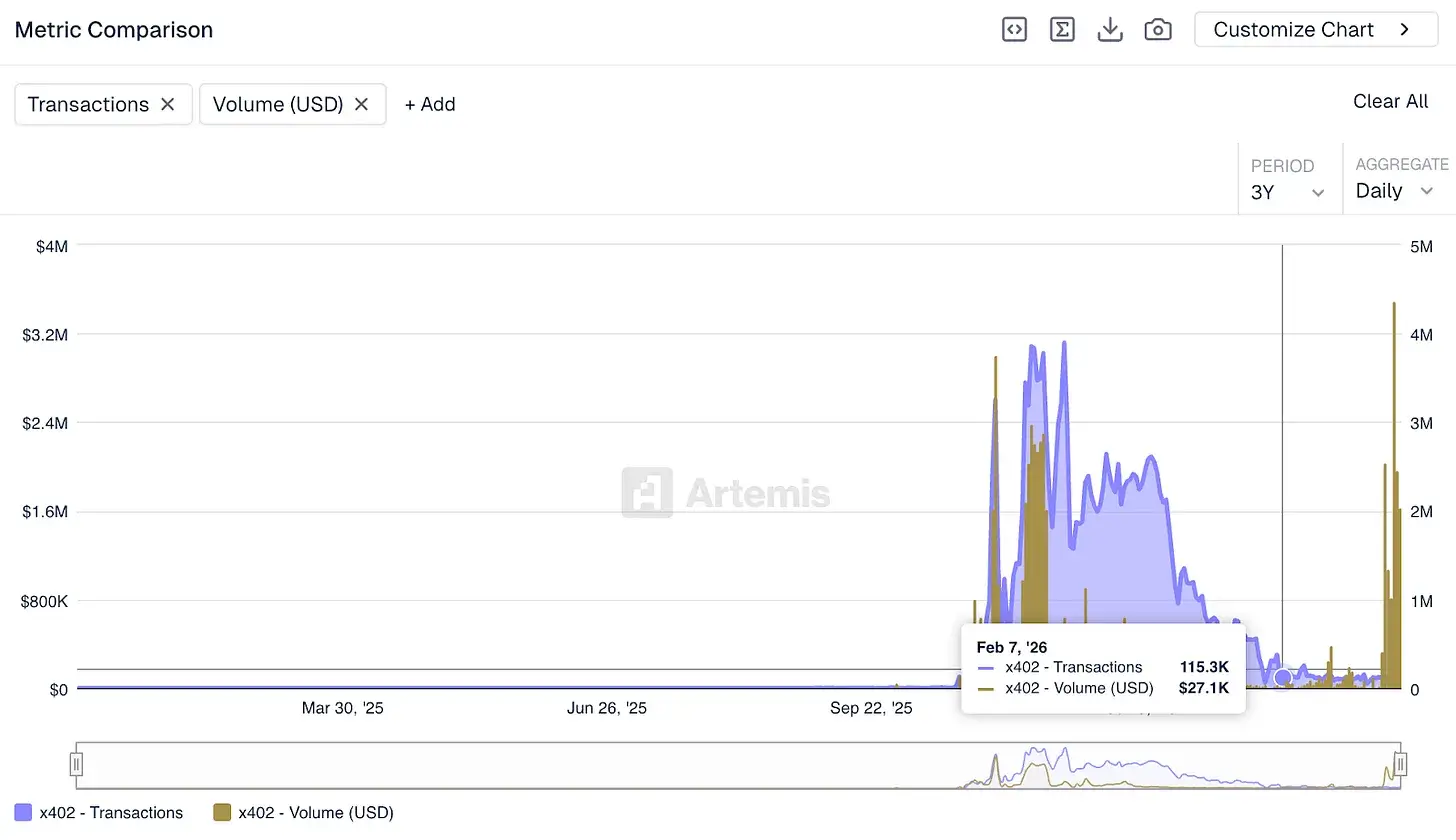

I want to accurately describe our phase because narratives often get ahead of data. Although the ecosystem valuation around the x402 protocol (note: the original text refers to a certain smart payment protocol) is about $7 billion, on-chain data shows that last week the protocol's daily processing volume was $28,000, most of which came from testing. This figure does not even compare to Visa's daily processing volume; they are not in the same league.

However, the transaction count for x402 has already exceeded 50 million. While the individual amounts are negligible, the frequency of transactions indicates that the foundation is in use, and developers are building on it. The merchant side accepting AI payments is increasing. This is how payment networks are born.

McKinsey predicts that by 2030, AI entities may intervene in $3 trillion to $5 trillion of global consumer commerce. This valuation may be accurate or overly optimistic. However, the undeniable contention is that AI-driven commerce has not yet scaled. Those building businesses that effectively serve entities, deploying entities as primary buyers, and those large transactions that will genuinely challenge the fee economy are still under construction.

The reason Citrini's report simulated a disturbance in the market is that it triggered a series of reliable chain reactions. The first quarterly report of 2027 may not make entity-driven price optimization a fearsome reason. It is not time yet.

The shock will first occur in the micropayments space of AI infrastructure, in the non-consumer sectors. An entity executing a research task might call a professional data API hundreds of times in one session. Each call costs just a few dollars. By the end of the week, it might generate $40 in revenue. Traditional card organization networks cannot handle these types of transactions. The lowest economic model for these types of transactions is unfeasible, the merchant onboarding process is unfeasible, and the fee structure is unfeasible. This category of business specification will not run on Visa's rails. It needs something entirely new, which x402, Nano payments, and Tempo are building.

As for the innovations concerning consumer spending simulated by Citrini, that will come a bit later. It requires entities to handle a considerable proportion of autonomous spending, which depends on whether humans are willing to trust and authorize the purchasing decision of current consumer operations to entities.

Visa is being disrupted by a "better customer"—this customer is for those who once established Visa's greatness as a non-racial national interest. The 2-3% fee is not a transaction tax but a tax on human rationality. AI entities are perfectly rational beings.

How do I know this is important? Because Visa spent $1.8 billion this week to ensure it is not excluded from the answer.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。