Author: Huobi Growth Academy

Abstract

In March 2026, the global cryptocurrency market exhibited severe polarization amidst a dual game of macroeconomic and geopolitical forces. This month’s focus concentrated on the dramatic turn in the conflict between the United States and Iran: after issuing a 48-hour ultimatum, the Trump administration suddenly announced a "five-day delay" in military strikes, claiming to have had "productive dialogue" with Iran, only for Iran to deny any direct or indirect contact. This action, widely interpreted by analysts as a "strategic pause," fundamentally reflects the forced compromise of the U.S. government in the face of oil prices soaring to $110 and increased pressure from the midterm elections. Simultaneously, the Federal Reserve maintained interest rates during the March FOMC meeting, with the dot plot indicating that 14 officials expect zero or only one rate cut in 2026. Powell acknowledged that the conflict in the Middle East has heightened inflationary risks and made it clear that "there will be no rate cuts until progress is made on inflation." Thus, the macroeconomic environment has fallen into a typical "stagflation" narrative—slow growth coupled with persistent inflation. In this context, cryptocurrencies have shown significant internal structural differentiation: Bitcoin has demonstrated astonishing resilience under the persistent support of institutional funds..

1. Geopolitical "Strategic Pause": Trump's "Reversal" and the Game in the Strait of Hormuz

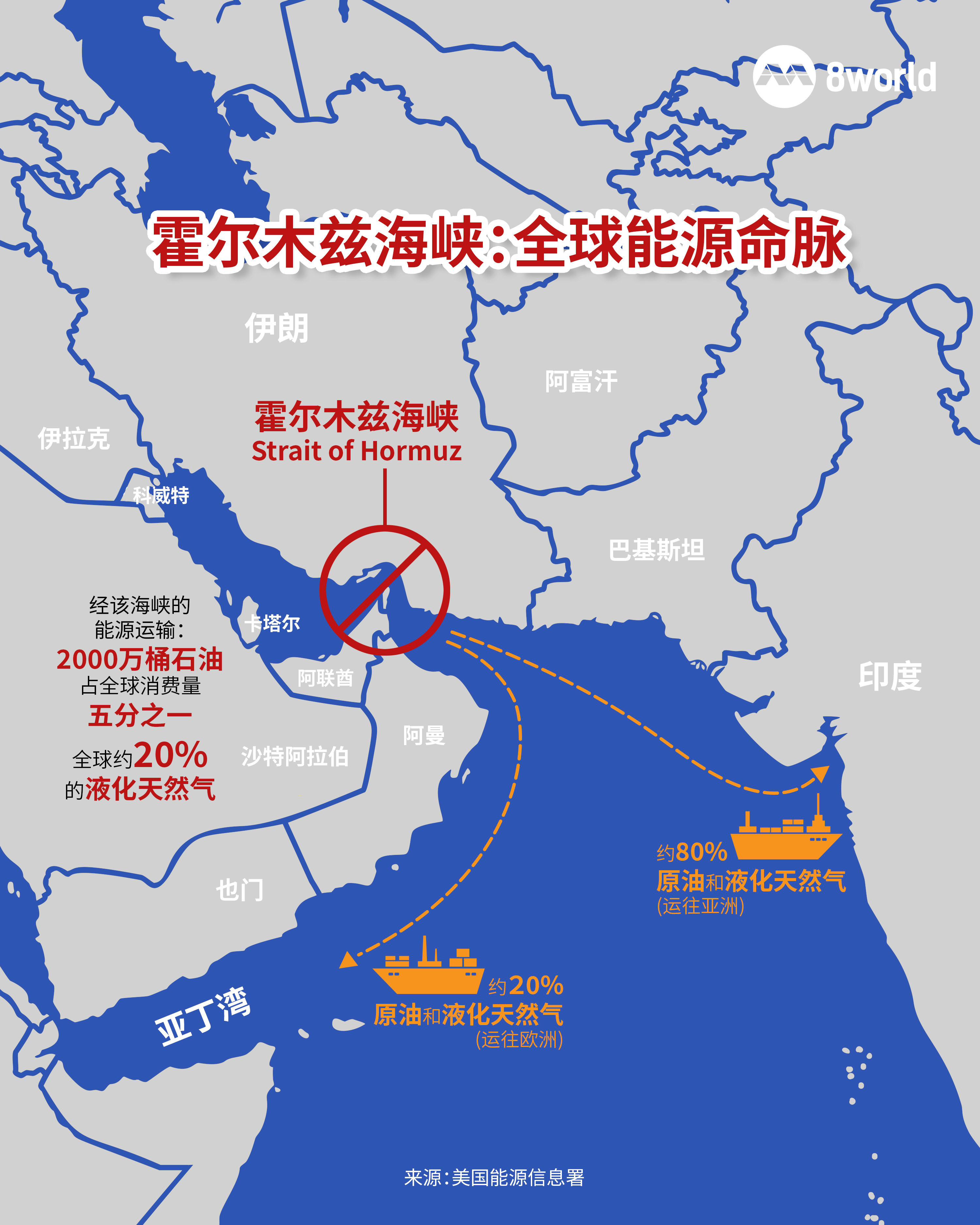

The situation in the Middle East in March 2026 became a core variable disturbing global risk assets. On March 21, U.S. President Trump issued an "ultimatum" to Iran, demanding that it open the Strait of Hormuz within 48 hours, or else it would destroy Iran's "various power plants." Iran responded firmly, stating that if the U.S. took action, all energy and oil facilities in the Middle East would be regarded as legitimate targets. However, as the deadline approached, Trump dramatically announced on March 23 that the U.S. would "delay by five days" its strikes on Iran's power plants, claiming that the U.S. and Iran had engaged in "very good and productive" dialogue over the past two days and had formed the main points of an agreement.

Behind this "last-minute reversal" reflects the multiple pressures faced by the U.S. government. Firstly, ongoing hostilities have pushed global oil prices above $110 per barrel, with the average price of gasoline in the U.S. nearing $4 per gallon, having risen more than $1 since late February, directly exacerbating domestic inflation. Secondly, high oil prices pose a threat to the midterm election prospects, and the conservative think tank Heritage Foundation warned that if the conflict escalated, the Democrats could "gain control of Congress" in the midterm elections. Additionally, U.S. Gulf allies privately warned Trump that bombing Iranian power plants could lead to a "catastrophic escalation" of the situation. These factors collectively contributed to Trump's stance softening.

However, there is a fundamental divergence in the official statements from both the U.S. and Iran. Iranian Foreign Ministry spokesman Baghaei made it clear that Iran has not engaged in any negotiations with the U.S., and that over the past few days, only certain messages from friendly nations were relayed. Iranian parliamentary speaker Ghalibaf also denied any negotiations with the U.S. This contradiction has raised significant market vigilance— as analyzed by Professor Liang Yabin from the International Strategy Research Institute of the Central Party School, Trump's move is likely a "strategic pause": on one hand, after more than 20 days of airstrikes, U.S. missile stockpiles may be insufficient and need time to replenish; on the other hand, the U.S. Marine Corps' 31st Expeditionary Unit is scheduled to arrive in the Middle East on March 27, coinciding with Trump's newly reset deadline.

For the energy and cryptocurrency markets, the fate of the Strait of Hormuz has become central to pricing. This global oil transport "throat" accounts for about 20% of global energy flows. Iranian officials have clearly stated that the Strait of Hormuz will not return to its pre-war state, and the energy market will remain unstable for the long term. The market reacted quickly to this: Brent crude oil continued to hover around $110, while WTI crude oil stabilized above $100. Market analysis from Wintermute pointed out that the news of a five-day suspension of strikes on Iranian energy infrastructure temporarily lowered the geopolitical risk premium, leading to a pullback in Brent crude prices and a subsequent rebound of Bitcoin to above $70,000. However, whether this "easing" is a temporary window or an escalating trap remains highly uncertain in the market.

2. The Federal Reserve's "Hawkish Claw" and the Shadow of Stagflation: A Significant Retreat in Rate Cut Expectations

As geopolitical disturbances intensified, the Federal Reserve further tightened expectations for macro liquidity. In the early hours of March 19, U.S. time, the Federal Reserve released its March policy meeting decision, maintaining the policy rate at 3.5% to 3.75%, in line with market expectations. However, the dot plot sent clear hawkish signals: of the 19 FOMC members, 7 expect no rate cuts in 2026, an increase of 1 from December of last year; the number of committee members supporting more than one rate cut has significantly decreased. The median forecast indicates that there may only be one rate cut in 2026, with another in 2027, ultimately stabilizing interest rates at around 3.1% long-term level.

Of further concern is that the Federal Reserve has significantly raised its inflation expectations, increasing the Q4 2026 PCE inflation rate from 2.4% to 2.7%, with core PCE also raised by 0.2 percentage points. This adjustment directly reflects the impact of rising oil prices due to the Middle East conflict. Powell acknowledged in the press conference that "the rise in energy prices is directly affecting the central bank's outlook" and emphasized that "energy inflation cannot be recklessly ignored." He made it clear that there would be no consideration of rate cuts until progress on inflation is seen. There have even been discussions within the committee about the possibility of future rate hikes, although this is not the baseline scenario for most officials.

Following the FOMC meeting, on March 24, the U.S. March Purchasing Managers Index (PMI) data further exacerbated market concerns about stagflation. The data showed that while U.S. business activity was slowing, price pressures accelerated again—the emergence of a situation with weak economic growth and persistent inflation is in the making. The market reacted negatively: the 5-year Treasury yield was pushed up to a nine-month high of 4.10%, the NASDAQ Composite Index fell by 1.5%, and Bitcoin briefly dropped to $70,900. Even more concerning for the market, futures in the bond market indicated that the implied probability of the Fed raising rates in July soared from nearly 0% a week prior to 20.5%.

This macro environment imposes dual constraints on cryptocurrency assets. On one hand, the high interest rate environment suppresses the valuation expansion of risk assets; on the other hand, persistent inflation means the Fed has no room for easing. Powell specifically pointed out that the conflict in the Middle East poses a downside risk to the economy and employment while posing an upside risk to inflation, creating a "dual tension" that puts monetary policy in a bind. For the cryptocurrency market, this means that in the short term, there is little expectation for a liquidity release from monetary policy, and the market must rely on endogenous strength and structural narratives to support prices.

3. The Divergence Path of Institutional Funds: Bitcoin ETF Resilience vs. Ethereum's Predicament

Amid sustained macro pressures, the flow of institutional funds has shown clear divergence. According to data as of the week ending March 22, the U.S. Bitcoin spot ETF recorded a net inflow of $93.1 million, maintaining a positive inflow for the second consecutive week, with total assets under management reaching $90.3 billion. This data contrasts with previous market concerns—during mid-March, the Bitcoin ETF experienced a single-day outflow of $708 million, the largest in two months. Yet institutions did not flee, and instead, increased their allocation during market panic. BlackRock's IBIT saw a net inflow of $190 million in a single week, becoming a major driver of inflows.

In sharp contrast, the Ethereum spot ETF recorded a net outflow of $60 million during the same period, with BlackRock’s ETHA seeing an outflow of $69.6 million. This divergence in fund flows is directly reflected in price performance: Bitcoin rebounded to around $74,500 in late March, while Ethereum dropped to the $2,180 level, with a weekly decline of 6%. Even more concerning is the leveraged structure of the Ethereum market—according to CryptoQuant data, 75% of the Ethereum held on Binance is leveraged, making Ethereum particularly vulnerable to negative fund flows.

The difference in institutional preferences reflects two entirely different investment logics. Bitcoin is being viewed by institutions as an alternative to "digital gold" and a macro hedging tool, its scarcity and post-halving supply-demand structure aligning more closely with traditional asset allocation logic. Morgan Stanley’s Global Investment Committee even suggested that the proportion of cryptocurrency assets in model portfolios should not exceed 4%, with Bank of America also supporting a range of 1% to 4%. In contrast, Ethereum is viewed more as a "technology asset" or "beta asset," which often gets hit first in an environment of economic uncertainty and high interest rates.

Another noteworthy signal is that despite Bitcoin ETF seeing continued net inflows, market sentiment indicators are in an "extreme fear" state. Data compiled by Coinglass shows that for 25 out of the past 30 days, market sentiment has remained at an "extreme fear" level. This pattern of institutional buying amid retail fear creates a typical "wall of worry." Apollo Crypto's research director Pratik Kala noted that "historically, these areas have always been excellent accumulation zones for Bitcoin." Institutional funds seem to be using the market's panic to methodically accumulate positions.

4. Bitcoin's Macro Positioning: Risk Asset or Safe Haven Asset?

This round of geopolitical shocks provides a new testing ground for Bitcoin's asset attributes. Traditional logic holds that geopolitical conflicts should push funds towards "safe haven assets" like gold and Bitcoin. However, the market performance following the escalation of the Middle East situation in March overturned this narrative: gold experienced its largest weekly decline since 1983, dropping over 10%, with spot gold nearly erasing all gains made in the year. Bitcoin also dropped to a two-week low of $67,371 during the Asian trading session on March 23, only to rebound later in response to the "delay in strikes" news.

This synchronous decline reveals Bitcoin's current core positioning—it is still a risk asset, not a mature safe haven asset. Haider Rafique, Global Managing Partner at cryptocurrency exchange OKX, pointed out that "weeks of severe fluctuations like this often test the new narrative logic of Bitcoin as a 'new safe haven,' especially as its trading price trend has been more aligned with risk assets rather than inversely correlated." During the market turbulence in March, Bitcoin exhibited a clear positive correlation with U.S. stocks and Asian stock markets, contrasting with its ideal positioning as "digital gold."

However, compared to the stock market, Bitcoin still showed a degree of resilience. Thus far in March, Bitcoin has increased by approximately 4%, whereas the NASDAQ index has dropped over 5% during the same period. This relative performance may stem from two factors: one, the continued inflow of institutional funds providing price support; two, Bitcoin's supply-side structure (post-halving scarcity) and demand side (institutional allocation through ETF channels) creating a unique microfoundation. In other words, Bitcoin's pricing is shifting from purely macro-driven to a "macro + institutional supply-demand" dual driver.

Another key variable is the relationship between oil prices and Bitcoin. According to Wintermute's analytical framework, the navigation conditions of the Strait of Hormuz transmit to Bitcoin prices through oil prices. The logical chain is: blockage of the Strait of Hormuz → oil prices rise → inflation expectations rise → the Fed maintains tightening → risk assets come under pressure → Bitcoin falls. Therefore, after Trump's announcement to "delay strikes," the pullback in oil prices saw Bitcoin rebound, confirming this transmission mechanism. If oil prices stabilize around $100 rather than soar further, Bitcoin may benefit from the "containment" of geopolitical risk.

5. Outlook: Three Paths and Key Observation Points

Integrating the dual variables of geopolitical and macro liquidity, the cryptocurrency market may evolve along three scenario paths in the next 1-2 months, with each path corresponding to different price ranges and allocation strategies.

Scenario One: The situation continues to ease, oil prices stabilize. If Trump's "delay in strikes" genuinely translates into a sustained diplomatic negotiation process, with navigation in the Strait of Hormuz gradually normalizing, Brent crude is expected to stabilize around $100. In this scenario, the geopolitical risk premium decreases, and the marginal inflation pressures faced by the Fed are alleviated, providing breathing room for risk assets. Wintermute expects Bitcoin to test the resistance range of $74,000 to $76,000. If institutional buying momentum continues, it may even push Bitcoin to $80,000. Key observation points for this scenario include: the operational choices of U.S. reinforcements upon arrival in the Middle East on March 27, whether indirect negotiations between the U.S. and Iran will restart, and whether U.S. gasoline prices will retreat from the $4 high.

Scenario Two: The situation deteriorates again, conflict escalates. Trump’s "strategic pause" may only be buying time for military action. If, upon the arrival of U.S. reinforcements on March 27, the U.S. takes a harder stance, Iran may fulfill its threat to "block the Strait of Hormuz." In this scenario, oil prices could exceed $120 and even approach $140, global inflation expectations could surge sharply, forcing the Fed to tighten monetary policy further. Bitcoin may fall back to the $65,000 range, or even test the psychological level of $60,000. In this scenario, the market would replay a "Black Monday" style wholesale sell-off, further reinforcing the co-movement of Bitcoin and risk assets.

Scenario Three: Stagflation deepens, macro dominates. Regardless of how the Middle East situation evolves, the emerging stagflation characteristics evident in the U.S. economy may become the dominant factor. March PMI data shows a coexistence of slow growth and rising prices, while the Fed’s dot plot indicates only one possible rate cut in 2026. If this "stagflation" pattern continues to deepen, the Fed may maintain unchanged interest rates throughout 2026 or even reconsider raising rates. Under this macro environment, Bitcoin will face dual pressures of valuation compression and liquidity tightening, but structural factors (halving effects, ETF channels, institutional allocations) may provide a hedge. The market will enter a tug-of-war stage of "macro pressure vs. institutional support," with volatility remaining high.

In terms of key observation points, investors need to closely monitor several time points and indicators: first, the evolution of the situation after the arrival of U.S. reinforcements on March 27, which serves as the first window to test the authenticity of Trump’s "strategic pause"; second, the weekly U.S. inflation data (CPI/PCE) and employment data to assess the evolution of stagflation pressures; third, the sustainability of fund flows into Bitcoin ETFs, particularly the inflow strength of leading products like BlackRock’s IBIT; fourth, the actual navigation conditions in the Strait of Hormuz and micro-indicators like tanker premiums, which reflect real risks more accurately than official statements.

In summary, the cryptocurrency market in March 2026 stands at the crossroads of geopolitical and macro liquidity. Trump’s “strategic pause” has provided a brief respite for the market, but the divergences in positions between the U.S. and Iran suggest that the conflict is far from over. The Federal Reserve's hawkish stance and the shadow of stagflation constitute a persistent macro-level constraint. In such an environment, Bitcoin has shown unique resilience— the continued inflow of institutional funds is reshaping its supply-demand structure, allowing it to remain relatively strong among risk assets. However, claiming that Bitcoin has evolved into a mature safe haven asset is premature; its co-movement with risk assets remains a key characteristic in the short term. For investors, the key in the coming weeks lies in distinguishing between "real easing" and "false pauses," seeking balance between geopolitical risk premiums and macro liquidity. As Wintermute's analysis suggests, the fate of the Strait of Hormuz may become the "compass" for Bitcoin's short-term price direction.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。