Written by: Matty

Translated by: Chopper, Foresight News

Last year, Apple spent $100 billion to repurchase its own shares. Stock buybacks are indeed effective; they reduce the circulating supply, concentrate equity rights, and return value to investors who adhere to long-term holdings.

For more than a century, the dividend mechanism has continuously driven the compound growth of wealth; preferred stocks balance the interests of investors at different levels; vesting lock-up rules prevent employees from cashing out and exiting. These models have long matured.

They are not exactly innovative; they are just drab and time-tested operational mechanisms of the stock market. And now, this classic mechanism is being implemented on-chain.

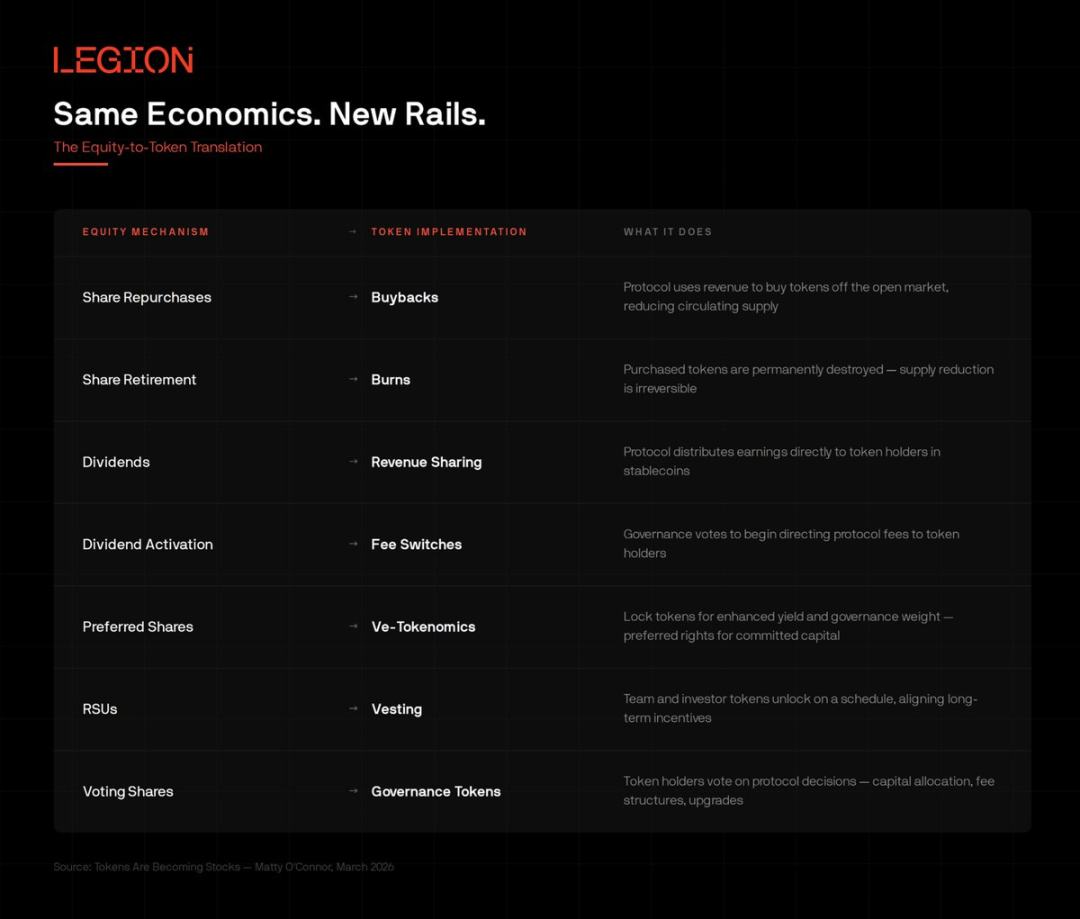

Buyback destruction, profit dividends, fee switches, vesting unlocking plans, preferred shares converting to common shares... Web3 projects are fully replicating this set of financial logic, with all settlements completed in real-time, and anyone can verify publicly through the blockchain explorer. The economic model has never been the core of innovation; the underlying infrastructure is key. The logic of equity operation has been verified; the real transformation lies in the transfer channels that carry this logic, which directly changes the capital entry threshold, settlement speed, and operational transparency.

Logical Comparison

Most discussions about cryptocurrencies start from the token level and then attempt to explain to traditional finance. I believe this approach is reversed. Based on the fundamental logic familiar to traditional equity investors, and then understanding the landing form of tokens, everything will become clear and comprehensible.

This comparison framework is the core benchmark for analyzing the entire track: as long as a certain token mechanism can accurately match the classic equity logic, its value foundation is solid; conversely, an unlimited issuance without asset backing, cyclical return revenue, and a points system with no ultimate value are doomed to fail, without exception.

Over a century of corporate finance history has already confirmed the core rule: only a value return model tied to real revenue can achieve the accumulation of wealth through compounding; all other play styles are essentially value dilution packaged in a more attractive form.

Practical Cases

The theory is simple to understand; let’s look at the real-world landing status in the industry.

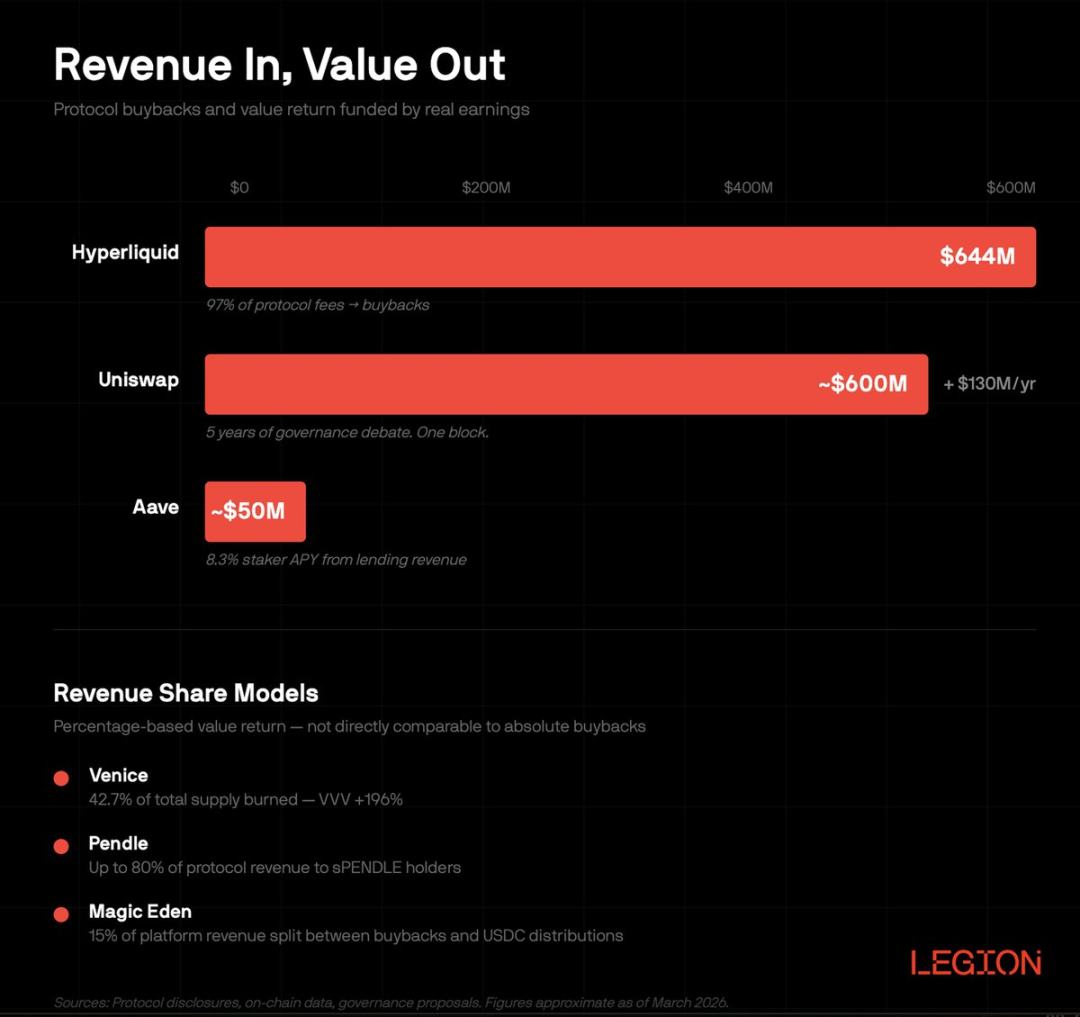

Hyperliquid uses 97% of the protocol fees entirely for the repurchase of HYPE tokens, not just 10% or a small percentage, but as high as 97%. Its cumulative repurchase amount has exceeded $644 million, accounting for 46% of the total scale of token buybacks in the entire cryptocurrency industry. The project’s treasury holds about 29.8 million HYPE tokens, valued at over $1.5 billion, and this substantial capital comes entirely from the protocol's real revenue, not from the foundation's arbitrary issuance.

This is exactly replicating Apple's capital return strategy: the underlying logic is consistent, settlement speed is faster, and the entire process is open and transparent. There is no need to wait for public companies to release annual 10-K reports to review data; on-chain information is updated in real-time and can be checked at any time.

Uniswap, the largest decentralized exchange in the crypto space, had not returned a single cent to token holders for five consecutive years. For five years, UNI was merely a governance token without any real economic governance powers. It wasn’t until December 2025 that the proposal for a fee switch was approved. In the same proposal, the project directly destroyed 100 million UNI (approximately $600 million in market value), and subsequently, it will continue to reduce the circulating supply by about $130 million annually.

In the context of traditional finance, this is equivalent to the board voting to initiate a dividend plan and massively cancel the total stock capital. A decision that took five years of governance struggle can be completed on-chain in just one block.

Aave takes $1 million weekly from the treasury surplus to conduct token buybacks, equivalent to an annual scale of about $50 million. Staked users can rely on real lending business revenue to earn about 8.3% annual yield, far from token inflationary benefits. Borrowers pay interest that generates real business revenue, which accumulates dividend returns, with a return rate even exceeding the average dividend level of the S&P 500 index.

The above cases share a unified core: real income is counted, and value returns to holders; there is no equity dilution and no Ponzi-like circular economy. This capital return logic, which has supported the stable operation of the stock market for decades, relies on blockchain's underlying channel, compressing settlement time from several days to several seconds.

Let me add a few noteworthy projects. Venice relies on revenue buybacks, having cumulatively destroyed 42.7% of the total circulation while reducing token issuance by 40%, resulting in a 196% surge in its native token VVV in February. Supply contraction combined with profit growth exemplifies the strong implementation of classic equity operation logic. Pendle abolished its long-term vePENDLE lock-up mechanism in January this year, upgrading to a liquid sPENDLE, allowing up to 80% of protocol revenue to be allocated to staked users with a vesting period reduced to 14 days, saying goodbye to the two-year long lock-up. The project’s revenue surged 60-fold in two years, while only 20% of users were willing to lock-up long-term under the old mechanism; the optimization of converting preferred stock to common stock directly activated the remaining 80% of those participating in the ecosystem. Magic Eden launched a mixed model in February:

15% of platform revenue is used for buybacks and direct distribution of USDC to stakers.

Why Mature Mechanisms Came Late

Given that the equity economic model has been validated for a century, why did the token designs in the first decade of the crypto industry almost completely ignore it?

The root cause lies in a fundamental accounting trap that has long blinded many practitioners.

Early token models were akin to companies issuing new stocks to users as dividends. The seemingly high returns from token issuance are essentially not profit sharing. What users receive are newly minted tokens, while the value of their own holdings continues to shrink due to inflation.

Calculating any annual yield supported by issuance reveals that, when accounting for token circulation inflation, the actual yield is inevitably negative. Traditional listed companies cannot maintain such a model for long; the vast majority of token projects ultimately cannot escape the fate of extinction.

Point systems and re-staking narratives are later iterations of packaging; the shell is upgraded, but the flaws remain unchanged. Points are equivalent to options rights of a company with no profits, and when redeemed, there is no asset backing, rendering the value nearly zero. Even if this cycle is packaged with more complex professional terms, the underlying economic logic has never changed.

The so-called model innovation fundamentally does not stand up. Minting tokens to generate yield is just a blatant dilution of equity without a prospectus. The entire industry spent ten years to regain the basic knowledge that every corporate CFO has already known; frankly, this is indeed embarrassing.

And the era of real revenue has reversed the overall landscape. Projects like Hyperliquid and Aave deeply tie value return to real business profits: protocol revenue is put on the books → start token buybacks; fee earnings are settled → dividends are distributed to staked holders.

The arrival of this transformation is a necessary result. As some projects prove that real revenue can empower token value just as corporate profits boost stock prices, the market no longer chases idle narratives. The story will eventually come to an end; facing real earnings is the norm for the industry.

Bilateral Integration Has Become Inevitable

Web3 projects connecting with mature equity economics is only half the story; the other half is traditional stock markets embracing the tokenization of underlying infrastructure, which is often overlooked by the market.

T+2 settlement has long been a product of a backward era. Real-time settlement technology for financial transactions has already matured and is now being fully implemented on the blockchain; as protocol data refreshes in real-time with each block, quarterly 10-Q reports appear outdated and inefficient; traditional stock markets have fixed trading hours (Monday to Friday from 9:30 am to 4:00 pm, closed on holidays) which inherently has shortcomings, while the crypto market operates 24/7 all year round.

These inherent shackles of traditional finance stem from outdated underlying technical limitations; the technical barriers have now been eliminated, and only the path dependence at the institutional level remains, rather than objective technical challenges.

Integration has already left the theoretical stage: the current on-chain tokenized stock volume has reached approximately $1 billion. On March 9, 2026, Nasdaq and Kraken jointly launched a stock gateway channel, bridging the compliant traditional stock market with permissionless DeFi infrastructure. As the second-largest securities exchange globally, Nasdaq received approval from the U.S. SEC to move some stocks on-chain. This is solely due to the overwhelmingly advantageous attributes of blockchain channels.

The most symbolic signal comes from BlackRock; its tokenized government bond fund BUIDL has reached an asset management scale of $2.9 billion, distributing dividends in stablecoins every month and directly distributing over $100 million in earnings to investors' wallets. To put it plainly, BlackRock is now paying investment dividends in USDC.

Integration has always been a two-way journey: token projects build rigorous economic systems tailored to traditional equity, while traditional stock markets reuse the efficient underlying framework of tokenization. The endgame is not one side replacing the other but both types of assets sharing a unified fast-moving underlying channel.

The Natural Divide in Capital Entry

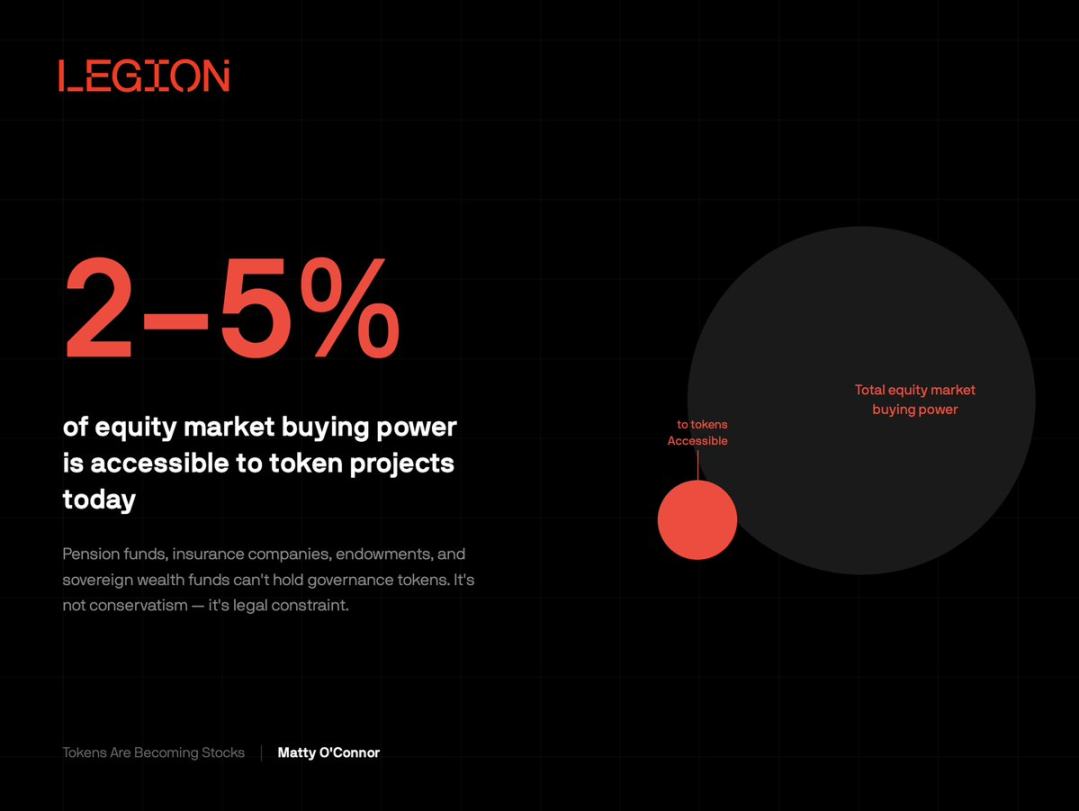

The funds that can be reached in the current token market account for only 2% to 5% of the purchasing power of the traditional stock market, which is a structural shortcoming.

Pension funds cannot hold governance tokens; insurance institutions cannot count income dividend tokens as fixed-income assets; there is no exclusive category for "DeFi earnings" in the allocation criteria for endowment funds. University endowment funds, sovereign wealth funds, insurance reserves... these are the largest long-term capitals globally, still watching from the sidelines. Based on entrusted duties and compliance requirements, even if some token economic models are of high quality and robust, large institutions cannot legally lay out most token categories.

A turning point has emerged. Combining the native distribution advantages of tokens with the compliance and legal security of equities can unlock capital scales that are 10 to 100 times that of purely token structures. Currently, the models for genuine revenue economics and real-time settlement infrastructure have been completed; the only thing lacking is the regulatory compliance framework that accommodates institutional capital entry.

The complementary advantages of both sides are clear to see. The underlying aspect of tokens provides real-time settlement, 24/7 liquidity, global access without intermediaries, on-chain cash flow transparency, and programmable distribution rules; while traditional stock markets offer clear legal definitions, compliance trust systems, institutional need for custodial standards, and a century-long foundation for guaranteeing investor rights.

Neither side can alone construct a complete closed loop, but both are well aware of each other's complementary value. The ultimate winning track will surely be a new form that takes into account the advantages of both.

Future Directions

Dividend-bearing tokens are essentially equity with a fully upgraded settlement experience; tokenized stocks are fundamentally digital tokens within an increasingly完善 legal framework. The two types of financial assets are continuously converging, and their differences are narrowing each quarter.

The core debate is no longer whether "tokens can replicate stock logic"; the answer has already been achieved. What truly matters is: who can bridge the connectivity between capital and infrastructure, and how quickly legal regulations can keep pace with economic innovations.

The mechanism has matured, the tracks have been laid, and the funds are in place.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。