Author: Zhou, ChainCatcher

Last week, Hyperliquid's trading volume reached about $15 billion, with commodity-related contracts like crude oil, gold, and silver being the main drivers.

With the volatility of oil prices, the daily trading volume of crude oil perpetual contracts on Hyperliquid broke $2.2 billion, second only to Bitcoin.

As the situation in Iran escalated and the Strait of Hormuz became critical, CME closed over the weekend, leading global traders to flock to a decentralized exchange on the blockchain for price discovery.

Meanwhile, GMX Labs, which once held nearly a quarter of the decentralized perpetual contract market, is publicly seeking a CEO, admitting that the original founder-driven model has become difficult to sustain, and is looking to shift toward a traditional leadership structure.

One is capitalizing on the spillover demand to take over traditional finance, while the other is still rebuilding its foundation.

Why did GMX and dYdX fail?

A closer look at GMX Labs' announcement shows that the range of CEO candidates covers DeFi, CeFi, traditional finance, and technology industries, with a base salary of $150,000 to $200,000 paid in stablecoins, and performance directly linked to protocol fee growth. This proposal passed the DAO governance vote with 96.42% approval.

A decentralized protocol, with overwhelming community consensus, has decided to introduce a traditional career manager. This indicates that the community has realized that the original improvised model can no longer hold up, and the solution they can think of is to align closer to traditional corporate management.

dYdX's situation is even more dire. At the beginning of 2023, dYdX held 73% of the decentralized perpetual contract market, almost monopolizing it; by the end of 2024, that number had dropped to single digits, with its token price plummeting over 90%.

Nowadays, the news about the two protocols is not product updates or market shares, but token buybacks. When a protocol focuses its main energy on maintaining token value rather than capturing market share, its strategic focus has fundamentally shifted.

The decline of GMX and dYdX is due to complex reasons.

The decline of GMX and dYdX is due to complex reasons.

Firstly, there is the issue of the starting point. A report from OKX Ventures shows that in 2021, dYdX pushed its daily trading volume to about $9 billion through trading mining, even exceeding Coinbase at one point. This figure was generated by token incentives, with users inflating volumes for rewards rather than engaging in real trading.

The more serious consequence is not the falsity of the data itself, but that the team took the fake user feedback as real product signals to respond to, so the iteration direction has been skewed from the very beginning.

Secondly, there is the structural issue. GMX adopts a multi-asset liquidity pool with oracle pricing model. This design was reasonable in 2021 when order books could not function on the Ethereum chain, and the AMM model was a viable choice.

However, this architecture has a quantifiable ceiling; the total open contract size that the protocol can support is about five times the TVL, and the TVL limit locks in the upper limit of trading scale.

LPs in this model inherently face information disadvantages, acting as a collective counterparty to all traders, but lack the ability to actively manage risks, while professional market makers are unwilling to enter under such conditions, resulting in limited liquidity depth.

dYdX recognized the direction of order books and decided to migrate to a self-built application chain on Cosmos. The technical judgment was correct, but there were issues in execution. After migration, users needed to adapt to new wallets and cross-chain asset bridging, which significantly increased friction costs. More critically, the v4 version's protocol fees flowed to validators instead of token holders, causing the community's perception of growth dividends to go to zero.

The third point concerns the judgment of decisive strengths. GMX bet on the liquidity model, while dYdX bet on a self-built chain, but there are only two real decisive points in this track: performance and the density of the market maker ecosystem.

According to OKX Ventures, most perpetual DEXs merely shift centralized risks from the custody layer to the less visible execution and clearing layer, with decentralization treated as a narrative rather than a genuine product problem to solve.

dYdX's shift to synthetic stock perpetual contracts and opening up to U.S. users is trading compliance for survival space, bypassing direct competition. GMX's hiring of a CEO is an attempt to rectify strategic misjudgments through organizational upgrades. These are correct self-rescue actions, but they are still addressing the outcomes rather than the causes.

The Logic of Newcomers

When Hyperliquid launched in 2023, GMX and dYdX were still the dominant players in this track. It had no financing, no VC endorsements, and no large-scale launch activities.

Early growth was slow. Without using token incentives to inflate volumes, the number of traders and market makers accumulated during the cold start period was limited, leading to long-term poor platform data. The profit and loss of the HLP treasury is available on-chain in real-time, attracting those willing to put real money in, but at that time, this was not a prominent advantage.

Early growth was slow. Without using token incentives to inflate volumes, the number of traders and market makers accumulated during the cold start period was limited, leading to long-term poor platform data. The profit and loss of the HLP treasury is available on-chain in real-time, attracting those willing to put real money in, but at that time, this was not a prominent advantage.

On the technical front, founder Jeff chose from the beginning to build L1 and create a fully on-chain order book. The logic behind it is to enable market makers to identify different types of trading flows through a fully transparent on-chain environment, allowing them to adjust pricing strategies.

This approach determined that it could not take the path of dYdX migrating to an application chain, nor could it rely on GMX's oracle pricing, and could only build from the ground up. Although this theory is still controversial in the industry, it provides a clear mainline for Hyperliquid's product direction.

In terms of traditional asset layout, HIP-3 will launch in October 2025, first accumulating a market maker ecosystem with crypto assets, and then sequentially adding gold, silver, and crude oil.

Reports point out that when dYdX launches a permissionless traditional asset market in 2024, the daily trading volume of Tesla synthetic stock is $4,000, and that of the Turkish lira is zero. Without market makers present, asset launches amount to nothing.

Hyperliquid's approach is to expand asset categories only after the market maker ecosystem matures, which is why it caught this wave of trading volume when the Iran crisis erupted.

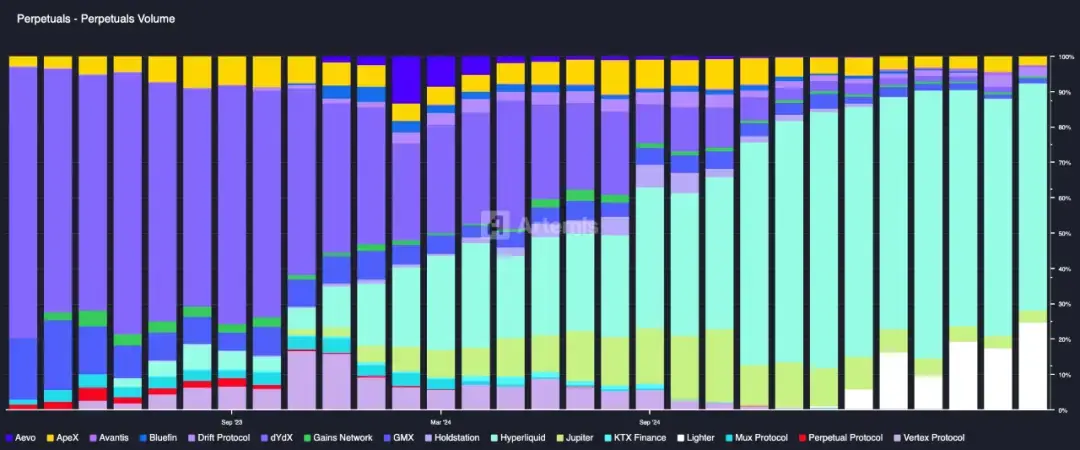

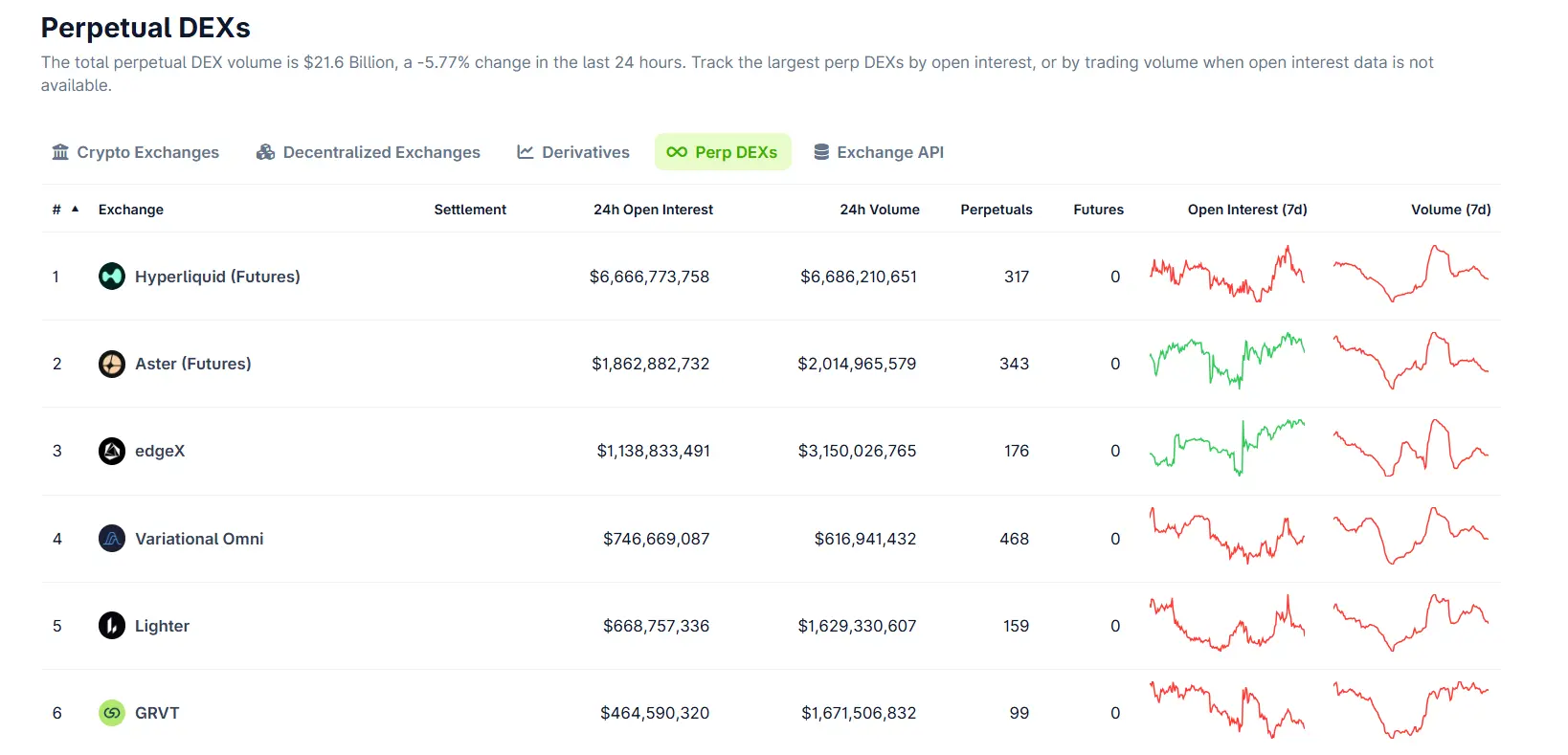

According to CoinGecko data, as of March 26, based on the 24-hour open contracts, Hyperliquid occupies about 54% of the top ten perpetual DEXs, with Aster ranking second at about 15%, and Hyperliquid's scale still exceeds the total of the other nine.

According to CoinGecko data, as of March 26, based on the 24-hour open contracts, Hyperliquid occupies about 54% of the top ten perpetual DEXs, with Aster ranking second at about 15%, and Hyperliquid's scale still exceeds the total of the other nine.

Aster, ranked second, and Hyperliquid entered the market almost simultaneously, but why did Hyperliquid surpass later?

Aster, ranked second, and Hyperliquid entered the market almost simultaneously, but why did Hyperliquid surpass later?

Aster CEO Leonard mentioned in an interview, "When dYdX emerged, we began trying to build our own things on-chain, and Aster's first version emerged, which is Apollo X. Since then, the perpetual contract DEX has gone through several cycles, with projects like GMX representing an era. We have always tried to build what the market truly needs, which is why we now have Aster."

From his words, it is evident that Aster's path has been gradual. Starting from the AMM model, it iterated step by step, adding an order book and then addressing the limitations of transparent markets with private order features. Every step responds to market feedback, and every step is a reasonable product decision.

Simply put, it has always been following the evolution of the track rather than defining its evolution.

Don't Release Your Product Too Early

In the crypto industry, the pace of technological paradigm shifts is too fast, and gradual iteration means you are always chasing the decisive points of the previous era.

This track has always had people searching for answers, and it still does.

The crypto industry is currently not favored, with many talents and capital withdrawing. However, because people are leaving, the technical window won't be quickly filled, giving builders more time. Each iteration of infrastructure, L2 maturation, application chain feasibility, and operational on-chain order books will open up new product possibility spaces.

First mover advantages are much weaker in this industry than in traditional industries; this is both a risk for old players and a genuine opportunity for new players. Especially in an era when AI tools are leveling productivity gaps, homogenized competition is intensifying, making it harder for just-right products to establish themselves.

The founder of Particle, summarizing the entrepreneurial lessons of the past year, quoted a statement by Google founder Sergey Brin at Stanford: "Don't release your product too early." His point is that once you release signals prematurely, you are tied to a delivery timeline, leaving no time to complete what truly needs to be done.

Thus, the real issue in entrepreneurship is not how fast you run, but rather clarifying where the endgame of this track lies.

Conclusion

The hiring of a CEO by GMX is not significant, but it may be looked back upon at some point as a footnote.

The entrepreneurial bounty period for the first generation of perpetual DEXs has ended; the era of improvisation, founder-driven dynamics, and rapid iterations has arrived at a point that requires professional management.

New windows are opening elsewhere, just as Hyperliquid captured this wave of geopolitical trading with commodity contracts, decentralized exchanges are transitioning from internal competition within the crypto industry to genuinely replacing traditional financial infrastructure. This direction is just beginning.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。