Today, I just finished reading the global macro strategy report released by UBS this week, which contained a lot of information. At the same time, I also watched an interview video with the CEO of BlackRock, both pointing to one thing: everyone is currently overly optimistic, still pricing the market based on the belief that the "Middle East conflict can be resolved quickly," but in fact, the probability of "economic recession" is rising.

The logic chain is very direct. If oil prices soar to 150 dollars, it will lead to a severe global recession. Because oil is embedded in everything in our daily lives—food production, transportation, manufacturing, heating, fertilizers, chemicals, and plastics. When oil prices skyrocket, almost all prices related to human life will rise. Central banks in various countries will raise interest rates to combat inflation, companies will freeze investments, and consumers will stop spending. At the same time, job opportunities will decrease, GDP will decline sharply, and the negative cycle will strengthen itself.

Currently, the Strait of Hormuz is still firmly blocked by Iran, with a supply gap of 9 million barrels per day relying entirely on depleting inventories. At this rate, global inventories will hit bottom by the end of April. If it drags on until then, the entire logic of global asset pricing will have to be redone, and the most frightening timing for a recession may emerge in early May!

👇 Here are some investment notes and thoughts we've put together, hoping to be helpful to everyone:

🚨 Core Pain Point: The "Nonlinear" Shock Triggered by Inventory Depletion

Currently, various asset ETFs still show resilience; although there has been a slight outflow of funds, it hasn’t reached panic selling. Everyone has confidence that the U.S. will be able to resolve the battle in the short term, and the overall capital market has a feeling of being like a frog in warm water. But UBS broke down the harsh reality of the energy market:

Panic Buying: Historical experience shows that once crude oil inventories fall to extremely low levels, oil prices will diverge from the fundamental supply and demand because everyone will start hoarding. Crude oil could soar to 150 dollars or even higher, and this is not a joke.

Nonlinear Amplification of Destructive Power: UBS's model calculates that if oil prices rise from 100 dollars to 150 dollars, the destructive power to the economy is not 1.5 times but 3 times. If we add the probability of recession, the destructive power could reach as high as 5 times.

Secondary Inflation in Fertilizers and Food: Currently, the Gulf region accounts for 30% of global fertilizer exports. When oil prices rise, the cost of fertilizers will immediately transfer to global food prices, which this inflationary pressure has not fully priced into the market.

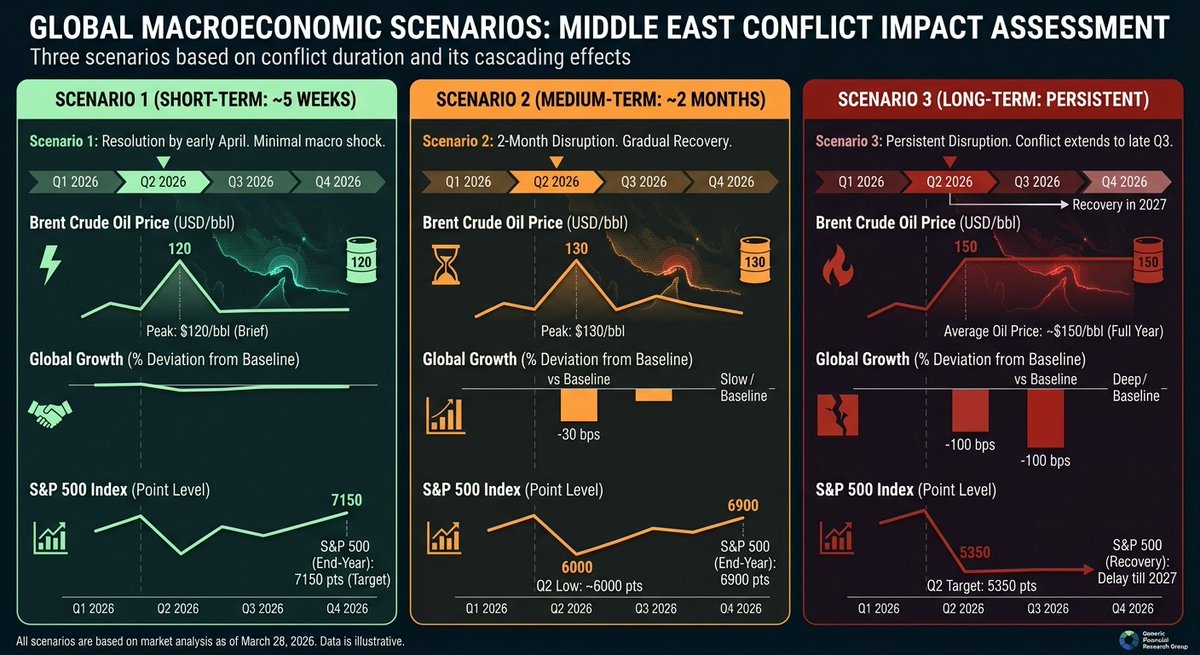

📊 UBS's Three Scenarios:

Scenario 1 (Quick Resolution within 5 Weeks): Resolve by early April. Oil prices briefly spike to 120 dollars before retreating. The S&P 500 could touch 7150 points by year-end.

Scenario 2 (Stalemate for 2 Months): Oil price peaks at 130 dollars. The S&P 500 retests 6000 points in the second quarter and closes at around 6900 points by the end of the year.

Scenario 3 (Prolonged War Lasting Until the End of Q3): Oil prices maintain around 150 dollars for the year. Global economic growth cut by nearly 100 basis points. The S&P 500 plunges directly to 5350 points in the second quarter, with the P/E ratio dropping from 22 times to 18 times, and a real recovery won't happen until 2027.

🏦 Global Central Bank Actions Begin to Diverge

Inflation is definitely rising, but how each central bank responds entirely depends on their national conditions. Overall, once facing a recession, their actions are generally consistent, with only widespread monetary easing (except for Europe):

Federal Reserve: U.S. employment has shown signs of fatigue; as long as the economy falters, the Federal Reserve is likely to pivot directly. Under the extreme recession of Scenario 3, they may revert to zero interest rates by 2027.

European Central Bank: The European Central Bank firmly clings to a single inflation target, coupled with a tight job market. Even if the economy is poor, they prefer to raise interest rates to combat inflation or stubbornly refuse to cut rates, showing a much tougher stance than the Federal Reserve.

Bank of Japan: After completing the last interest rate hike this year, they will basically stop and later follow the Federal Reserve in turning dovish.

💼 Our Recent Investment Recommendations

1. Stocks: Hold onto defensive positions, embrace high cash flow and dividends, and avoid Asian and European markets.

Geographically: Asia is most severely affected by energy channel blockades, Europe is dragged down by natural gas, while the U.S. stock market remains relatively resilient.

By sector: Avoid automobiles, durable consumer goods, financial services, and heavy asset industries, as these are the hardest hit by rising oil prices.

2. Bonds: The earliest assets appear to have good value.

UBS believes the bond market has now dropped into a value range worth paying attention to.

Short-term interest rate bonds: The market expects central banks to take action due to high inflation, potentially resulting in short-term rate hikes, which feels a bit overdone. Short-term government bonds from Switzerland, the UK, the U.S., and India currently have a good value proposition.

Long-term U.S. Treasuries: The yield curve peaked in Q2 of this year, and short to medium term will experience a transition from "bear flattening" to "bull steepening." If Scenario 3 occurs, the 10-year U.S. Treasury yield could ultimately drop back to 2.50% (but this depends on 2027).

3. Forex and Gold: The dollar will be strong initially then weaken, with gold waiting for the right moment.

Forex: The dollar will reap the short-term benefits of safe-haven demand, remaining strong against Asian emerging market currencies. However, if the Federal Reserve begins violent rate cuts in the second half of the year, the dollar will trend towards significant depreciation. The Euro/USD rate is expected to be 1.10, and the Yen/USD rate is expected to be 175.

Gold: Currently suppressed by high interest rates and a strong dollar, temporarily not serving as a safe haven. But UBS believes that once market panic about recession overcomes concerns about inflation and long-term yields turn downwards, gold will surge. It is recommended to consider 4000 to 4250 dollars as a medium-term strategic allocation range.

Other precious metals: Silver, platinum, and palladium have strong industrial characteristics; in a bad economy, they will also fall, so they are not recommended for investment.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。